Dry Film Market

Dry Film Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701581 | Last Updated : July 30, 2025 |

Format : ![]()

![]()

![]()

![]()

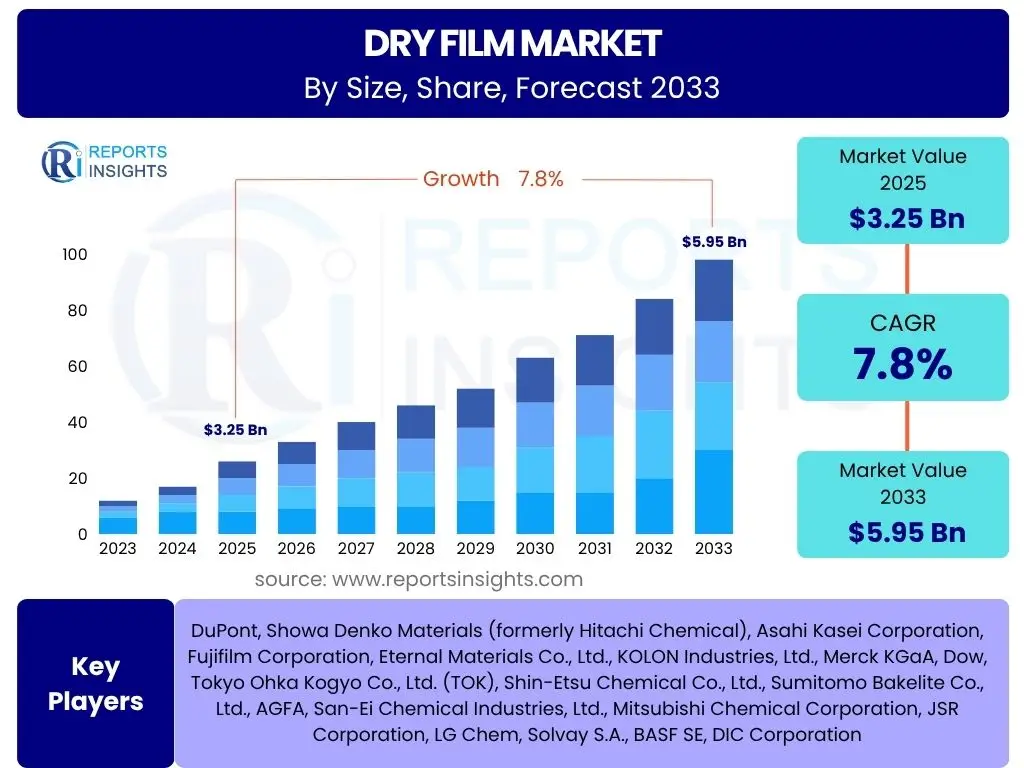

Dry Film Market Size

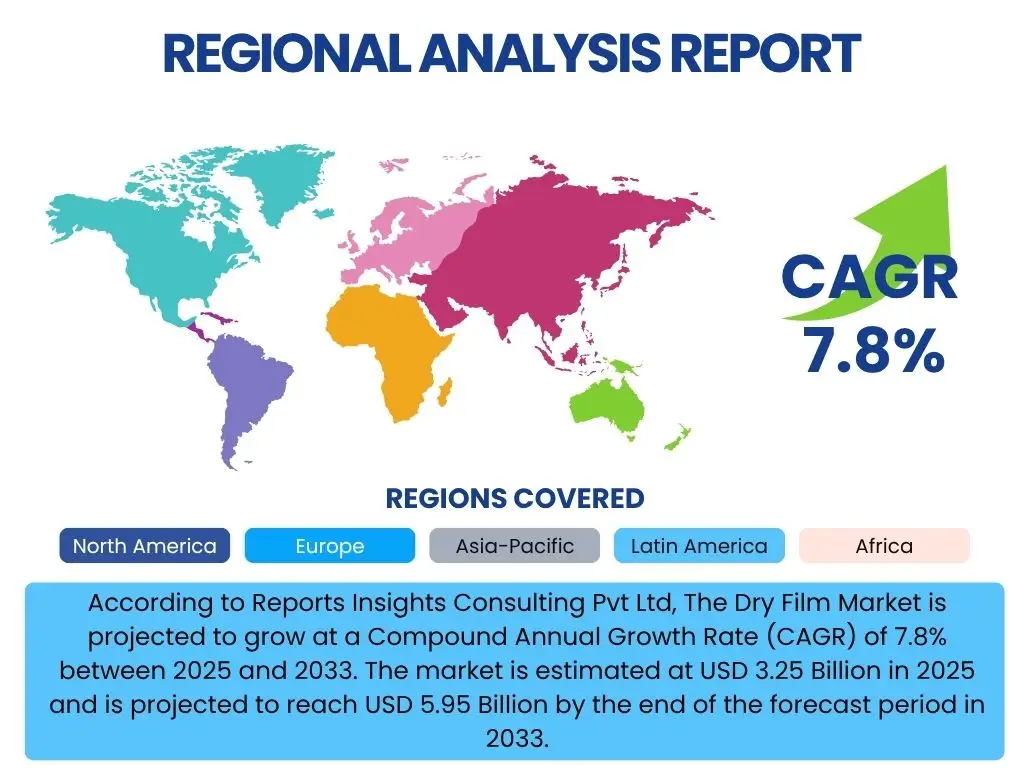

According to Reports Insights Consulting Pvt Ltd, The Dry Film Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033. The market is estimated at USD 3.25 Billion in 2025 and is projected to reach USD 5.95 Billion by the end of the forecast period in 2033.

Key Dry Film Market Trends & Insights

The Dry Film market is undergoing significant transformations, driven by technological advancements and evolving industry demands. Users frequently inquire about the leading trends shaping this sector, particularly concerning miniaturization, sustainability, and integration into advanced electronic systems. Key insights reveal a strong emphasis on developing thinner, more flexible, and high-performance dry films to meet the stringent requirements of modern electronics, alongside a growing shift towards eco-friendly manufacturing processes and materials.

The push for higher density interconnects and more compact electronic devices is a primary driver for innovation in dry film technology. This includes the development of ultra-thin films and advanced photoresists that can achieve finer line widths and spaces. Furthermore, the industry is increasingly focusing on enhancing the functional properties of dry films, such as improved adhesion, chemical resistance, and thermal stability, to ensure reliability and performance in demanding applications like automotive electronics and high-frequency communication devices.

Another prominent trend is the adoption of automated and intelligent manufacturing processes for dry film production and application. This not only improves efficiency and reduces waste but also ensures consistent quality, which is crucial for high-precision electronic components. The convergence of these trends suggests a market poised for continuous innovation, driven by the relentless pace of technological evolution in the electronics industry.

- Miniaturization and high-density packaging in electronics manufacturing.

- Development of eco-friendly and halogen-free dry film solutions.

- Increasing adoption in flexible electronics and wearable devices.

- Advancements in automotive electronics and electric vehicle (EV) components.

- Integration of advanced materials for improved performance and reliability.

- Growing demand for higher resolution and thinner dry films for next-generation PCBs.

AI Impact Analysis on Dry Film

Common inquiries regarding AI's impact on the Dry Film market center on how artificial intelligence can revolutionize manufacturing processes, optimize material development, and enhance quality control. Users are keen to understand if AI can accelerate research and development cycles, improve predictive maintenance of production equipment, or offer more precise process control. The general expectation is that AI will streamline operations, reduce defects, and enable the creation of more sophisticated dry film products tailored to specific application requirements.

The integration of AI in the dry film industry is primarily focused on optimizing production efficiencies and improving product quality. AI-powered analytics can process vast amounts of sensor data from manufacturing lines to identify patterns, predict equipment failures before they occur, and fine-tune process parameters in real-time. This predictive maintenance and process optimization can significantly reduce downtime, minimize material waste, and ensure consistent output, leading to substantial cost savings and improved operational reliability.

Furthermore, AI is poised to play a crucial role in the R&D of new dry film formulations. Machine learning algorithms can analyze material properties, simulate molecular interactions, and predict the performance of novel chemical compounds, thereby accelerating the discovery of innovative dry film materials with enhanced characteristics. This intelligent approach to material science can shorten development cycles, reduce experimental costs, and bring advanced dry film solutions to market more rapidly, addressing the ever-evolving demands of the electronics and semiconductor industries.

- AI-driven optimization of manufacturing processes, improving yield and efficiency.

- Predictive maintenance for dry film production machinery, reducing downtime.

- Enhanced quality control through AI-powered visual inspection systems.

- Accelerated material discovery and formulation development using machine learning.

- Supply chain optimization and demand forecasting for raw materials.

- Improved defect detection and classification in dry film application.

Key Takeaways Dry Film Market Size & Forecast

Analysis of common user questions regarding the Dry Film market size and forecast reveals a strong interest in understanding the primary drivers of growth, the segments offering the most promising opportunities, and the geographical regions expected to lead market expansion. Users seek clarity on how macroeconomic factors, technological advancements, and shifts in end-use industries will influence the market trajectory over the forecast period. The insights gathered emphasize the robust growth potential driven by the electronics sector's continuous innovation and the increasing adoption of advanced packaging technologies.

A significant takeaway is the consistent and healthy Compound Annual Growth Rate (CAGR) projected for the dry film market, indicating sustained demand across its various applications. This growth is predominantly fueled by the global proliferation of consumer electronics, the rapid expansion of the automotive electronics segment, and the ongoing demand for high-performance Printed Circuit Boards (PCBs) in various industries. The market's resilience is further supported by its critical role in advanced manufacturing processes, where precision and reliability are paramount.

Moreover, the forecast highlights the Asia Pacific region as the dominant force in the dry film market, attributable to its robust electronics manufacturing ecosystem and significant investments in semiconductor fabrication. This regional leadership is expected to continue, driven by industrial expansion and technological advancements within countries like China, Japan, South Korea, and Taiwan. The insights also underscore the importance of continuous innovation in dry film formulations to meet emerging requirements for thinner, more flexible, and environmentally sustainable solutions, thereby sustaining long-term market growth.

- The Dry Film Market is projected for strong growth, driven primarily by the electronics industry.

- Asia Pacific is expected to remain the largest and fastest-growing regional market.

- Key growth segments include high-density interconnect (HDI) PCBs and advanced semiconductor packaging.

- Innovation in material science and manufacturing processes will be crucial for competitive advantage.

- Sustainability and environmental regulations are increasingly influencing product development.

Dry Film Market Drivers Analysis

The Dry Film market's expansion is fundamentally propelled by the relentless pace of innovation and demand within the electronics and semiconductor industries. As electronic devices become more sophisticated, compact, and powerful, the need for high-performance interconnect solutions intensifies. Dry films, with their precision and reliability, are indispensable for manufacturing advanced Printed Circuit Boards (PCBs) and semiconductor components, directly benefiting from the global surge in consumer electronics, data centers, and advanced communication infrastructure.

Additionally, the burgeoning automotive electronics sector represents a significant growth catalyst. Modern vehicles are increasingly integrated with complex electronic systems for infotainment, safety, connectivity, and autonomous driving. This proliferation of electronic content in automobiles necessitates high-quality, durable PCBs and semiconductor packages that can withstand harsh operating conditions, thereby driving the demand for specialized dry films. The transition towards electric vehicles (EVs) further amplifies this trend, as EVs require advanced power electronics and battery management systems.

Furthermore, the global rollout of 5G technology and the expansion of IoT ecosystems are creating new avenues for dry film consumption. These technologies require high-frequency and high-speed circuit boards, demanding dry films capable of finer resolution, better dielectric properties, and enhanced thermal stability. The continuous advancements in display technologies, including flexible and OLED displays, also contribute significantly, as dry films are essential for their intricate manufacturing processes.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Consumer Electronics | +2.5% | Global, particularly Asia Pacific (China, India) | Short to Medium Term (2025-2029) |

| Growth in Automotive Electronics Industry | +2.0% | North America, Europe, Asia Pacific (Japan, South Korea) | Medium to Long Term (2027-2033) |

| Advancements in Semiconductor Manufacturing | +1.8% | Asia Pacific (Taiwan, South Korea, Japan), North America | Short to Medium Term (2025-2030) |

| Expansion of 5G Technology and IoT Devices | +1.5% | Global, especially China, USA, Europe | Medium Term (2026-2031) |

| Miniaturization and High-Density Interconnect (HDI) PCBs | +1.0% | Global | Short to Long Term (2025-2033) |

Dry Film Market Restraints Analysis

Despite robust growth drivers, the Dry Film market faces several restraints that could potentially impede its expansion. One significant concern is the volatility of raw material prices, particularly for petrochemical derivatives and specialty polymers. Fluctuations in the cost of these essential components can directly impact manufacturing expenses and profit margins for dry film producers, leading to pricing instability and affecting market competitiveness. Geopolitical events, supply chain disruptions, and global economic shifts often exacerbate this volatility, making long-term planning challenging for market players.

Another key restraint involves the increasing stringency of environmental regulations worldwide. Governments and regulatory bodies are imposing stricter norms on chemical usage, waste disposal, and emissions, particularly for industries involved in electronics manufacturing. Dry film manufacturers are under pressure to develop more environmentally friendly formulations, such as halogen-free or low-VOC (Volatile Organic Compound) products, which often entails significant research and development investments and can sometimes compromise performance or increase production costs. Compliance with these evolving regulations can be a costly and complex endeavor, especially for smaller market participants.

Furthermore, intense competition from alternative technologies, such as liquid photoresists, poses a continuous challenge. While dry films offer distinct advantages in certain applications, liquid photoresists may be more cost-effective or suitable for specific processes, particularly in high-volume, less intricate applications. The high capital expenditure required for setting up advanced dry film manufacturing facilities, coupled with the need for continuous investment in research and development to keep pace with technological advancements, can also act as a barrier to entry for new players and a restraint for existing ones, impacting market growth potential.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in Raw Material Prices | -1.5% | Global | Short to Medium Term (2025-2029) |

| Stringent Environmental Regulations | -1.2% | Europe, North America, parts of Asia Pacific | Medium to Long Term (2027-2033) |

| Competition from Liquid Photoresists | -1.0% | Global | Short to Medium Term (2025-2030) |

| High Research & Development Costs | -0.8% | Global | Short to Long Term (2025-2033) |

Dry Film Market Opportunities Analysis

The Dry Film market is ripe with opportunities, primarily driven by the emergence of new technologies and expanding applications across diverse industries. One significant area of opportunity lies in the burgeoning flexible electronics and wearable devices sector. As consumers increasingly adopt smartwatches, flexible displays, and other bendable electronic gadgets, the demand for highly adaptable and durable dry films that can conform to unconventional shapes without compromising performance is escalating. This niche but rapidly growing segment offers manufacturers a chance to innovate with novel materials and processing techniques, creating customized dry film solutions.

Another substantial opportunity stems from the growth of emerging markets, particularly in Asia Pacific, Latin America, and Africa. Rapid industrialization, increasing disposable incomes, and the widespread adoption of digital technologies in these regions are fueling demand for consumer electronics, automotive components, and IT infrastructure. Localized manufacturing expansion in these areas creates a fertile ground for dry film suppliers to establish new partnerships, expand distribution networks, and cater to a growing customer base, often with less stringent regulatory landscapes compared to developed regions, initially allowing for quicker market penetration.

Furthermore, advancements in display technologies, such as OLEDs and micro-LEDs, present significant opportunities. These next-generation displays often require more precise and intricate manufacturing processes where dry films excel in enabling ultra-fine patterning and enhanced layer protection. The ongoing research and development in bio-based and sustainable dry film alternatives also open new market segments. As industries worldwide prioritize sustainability, dry film manufacturers investing in eco-friendly products stand to gain a competitive edge and capture market share from environmentally conscious end-users, aligning with global green initiatives.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emerging Markets Expansion | +1.8% | Asia Pacific (India, Southeast Asia), Latin America | Medium to Long Term (2027-2033) |

| Demand from Flexible & Wearable Electronics | +1.5% | Global, particularly North America, Asia Pacific | Medium Term (2026-2031) |

| Advancements in Display Technologies (OLED, Micro-LED) | +1.3% | Asia Pacific (South Korea, China, Japan), Europe | Short to Medium Term (2025-2030) |

| Development of Bio-based & Sustainable Dry Films | +1.0% | Europe, North America, Japan | Long Term (2029-2033) |

Dry Film Market Challenges Impact Analysis

The Dry Film market faces several inherent challenges that can affect its growth trajectory and operational efficiency. One of the primary challenges is the complexity of manufacturing processes involved in dry film production. Achieving consistent thickness, uniform coating, and defect-free surfaces for high-performance applications requires highly specialized equipment, advanced cleanroom environments, and stringent quality control protocols. Any deviation in these processes can lead to significant waste and increased production costs, making it difficult for manufacturers to scale operations efficiently while maintaining product integrity.

Another significant challenge is the rapid pace of technological change within the electronics and semiconductor industries. End-user applications are constantly evolving, demanding dry films with increasingly sophisticated properties, such as finer resolution, improved thermal stability, and enhanced chemical resistance. This necessitates continuous and substantial investment in research and development to keep product portfolios competitive and relevant. Companies that fail to innovate swiftly risk obsolescence, as new materials and processing techniques can quickly disrupt existing market positions, leading to a constant pressure to adapt and evolve.

Furthermore, the global nature of the dry film supply chain introduces vulnerabilities, particularly in times of geopolitical instability or global crises. Disruptions in the supply of critical raw materials from specific regions, trade disputes, or logistical bottlenecks can severely impact production schedules and material availability. Intellectual property (IP) protection is also a considerable concern, as dry film formulations often involve proprietary chemical compositions and manufacturing techniques, making them susceptible to counterfeiting or unauthorized replication, which can erode market share and profitability for innovators. Navigating these challenges requires robust risk management strategies and a commitment to continuous innovation.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complex Manufacturing Processes | -1.3% | Global | Short to Medium Term (2025-2029) |

| Rapid Technological Obsolescence | -1.0% | Global | Short to Long Term (2025-2033) |

| Global Supply Chain Disruptions | -0.9% | Global | Short to Medium Term (2025-2028) |

| Intellectual Property (IP) Issues | -0.7% | Global | Medium to Long Term (2027-2033) |

Dry Film Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Dry Film Market, offering a detailed overview of its current size, historical performance, and future growth projections. It delves into the key market dynamics, including drivers, restraints, opportunities, and challenges, providing a holistic understanding of the factors influencing market trajectory. The report also covers a detailed segmentation analysis, regional insights, and profiles of key market players, equipping stakeholders with actionable intelligence for strategic decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 3.25 Billion |

| Market Forecast in 2033 | USD 5.95 Billion |

| Growth Rate | 7.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | DuPont, Showa Denko Materials (formerly Hitachi Chemical), Asahi Kasei Corporation, Fujifilm Corporation, Eternal Materials Co., Ltd., KOLON Industries, Ltd., Merck KGaA, Dow, Tokyo Ohka Kogyo Co., Ltd. (TOK), Shin-Etsu Chemical Co., Ltd., Sumitomo Bakelite Co., Ltd., AGFA, San-Ei Chemical Industries, Ltd., Mitsubishi Chemical Corporation, JSR Corporation, LG Chem, Solvay S.A., BASF SE, DIC Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Dry Film Market is comprehensively segmented by type, application, and end-use industry, providing a granular view of its diverse landscape and enabling precise market analysis. This detailed segmentation helps in understanding the varying demands and growth patterns across different product categories and their specific uses. Each segment reflects unique technological requirements, market drivers, and competitive dynamics, contributing to the overall market structure.

The segmentation by type typically includes Photoresist Dry Film, Solder Mask Dry Film, and Dielectric Dry Film, each serving distinct functions in the fabrication of electronic components. Photoresist dry films are crucial for patterning circuits, while solder mask dry films protect circuit boards from oxidation and facilitate soldering processes. Dielectric dry films, on the other hand, provide electrical insulation and enhance signal integrity. Understanding the market share and growth trajectories of these film types is vital for strategic planning.

Furthermore, the segmentation by application highlights the primary industries and product categories where dry films are extensively utilized, such as Printed Circuit Boards (PCBs), Semiconductors, Flexible Displays, and Automotive Electronics. The end-use industry segmentation provides a macro perspective, classifying consumption across sectors like Electronics & Electrical, Automotive, and Healthcare. This multi-faceted segmentation allows for targeted market strategies, identifying high-growth areas and emerging opportunities within the Dry Film market landscape.

- By Type:

- Photoresist Dry Film

- Solder Mask Dry Film

- Dielectric Dry Film

- By Application:

- Printed Circuit Boards (PCBs)

- Semiconductors

- Flexible Displays

- Automotive Electronics

- Medical Devices

- Consumer Electronics

- By End-Use Industry:

- Electronics & Electrical

- Automotive

- Aerospace & Defense

- Healthcare

- Telecommunications

Regional Highlights

The Dry Film Market exhibits significant regional disparities in terms of production, consumption, and growth potential, primarily influenced by the distribution of the global electronics and semiconductor manufacturing industry. The Asia Pacific region stands as the undisputed leader, accounting for the largest market share and demonstrating the highest growth rate. This dominance is attributed to the presence of major electronics manufacturing hubs in countries like China, Taiwan, South Korea, and Japan, which are at the forefront of PCB, semiconductor, and display production. Robust governmental support, significant investments in R&D, and a large consumer base further solidify APAC's position as the powerhouse of the dry film market.

North America and Europe also hold substantial market shares, driven by their advanced automotive electronics, aerospace & defense, and high-tech medical device industries. These regions are characterized by a strong emphasis on innovation, research, and the adoption of high-performance, specialized dry film solutions. While their manufacturing volumes may not match those of Asia Pacific, the demand for premium and custom-engineered dry films for niche applications ensures steady growth. Furthermore, increasing awareness and stricter environmental regulations in these regions drive the adoption of more sustainable and eco-friendly dry film products, fostering a market for advanced, compliant materials.

Latin America, the Middle East, and Africa represent emerging markets with nascent but growing electronics manufacturing capabilities. While currently smaller in market size, these regions offer future growth opportunities as industrialization progresses and consumer electronics adoption increases. Investments in telecommunications infrastructure, including 5G rollout, and the development of local manufacturing ecosystems are expected to gradually increase the demand for dry films in these regions over the forecast period. However, market penetration and growth will depend on economic stability, regulatory frameworks, and the establishment of robust supply chains.

- Asia Pacific (APAC): Dominates the market due to its extensive electronics manufacturing base, including China, Taiwan, South Korea, and Japan. High demand from PCB fabrication, semiconductor packaging, and display industries. Expected to maintain the highest growth rate.

- North America: Significant market share driven by advanced semiconductor manufacturing, automotive electronics, and aerospace & defense industries in the United States and Canada. Focus on high-performance and specialized dry films.

- Europe: Strong presence in automotive, industrial electronics, and medical device sectors, particularly in Germany, France, and the UK. Increasing focus on sustainable and environmentally compliant dry film solutions.

- Latin America: Emerging market with growing electronics assembly activities, particularly in Brazil and Mexico. Potential for growth driven by local consumer electronics and automotive industries.

- Middle East & Africa (MEA): Nascent market with opportunities in telecommunications infrastructure development and limited electronics manufacturing. Growth potential tied to economic development and diversification initiatives.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Dry Film Market.- DuPont

- Showa Denko Materials (formerly Hitachi Chemical)

- Asahi Kasei Corporation

- Fujifilm Corporation

- Eternal Materials Co., Ltd.

- KOLON Industries, Ltd.

- Merck KGaA

- Dow

- Tokyo Ohka Kogyo Co., Ltd. (TOK)

- Shin-Etsu Chemical Co., Ltd.

- Sumitomo Bakelite Co., Ltd.

- AGFA

- San-Ei Chemical Industries, Ltd.

- Mitsubishi Chemical Corporation

- JSR Corporation

- LG Chem

- Solvay S.A.

- BASF SE

- DIC Corporation

Frequently Asked Questions

Analyze common user questions about the Dry Film market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is dry film and its primary use?

Dry film is a thin, photosensitive polymer material applied to substrates like Printed Circuit Boards (PCBs) or semiconductor wafers. Its primary use is in photolithography processes to transfer circuit patterns onto these substrates with high precision, acting as a temporary resist or permanent dielectric/protective layer.

What are the key factors driving the growth of the Dry Film Market?

The Dry Film Market growth is primarily driven by the increasing global demand for consumer electronics, the rapid expansion of the automotive electronics industry, advancements in semiconductor manufacturing, and the widespread adoption of 5G technology and IoT devices, all requiring high-density, precise circuit components.

Which region holds the largest market share in the Dry Film Market?

The Asia Pacific (APAC) region currently holds the largest market share in the Dry Film Market. This dominance is due to the presence of major electronics and semiconductor manufacturing hubs in countries like China, Taiwan, South Korea, and Japan, which are significant consumers of dry films.

What are the main challenges faced by the Dry Film Market?

Key challenges for the Dry Film Market include the inherent complexity of manufacturing processes, the rapid pace of technological obsolescence in the electronics industry, potential disruptions in the global supply chain, and the ongoing need for robust intellectual property protection for innovative formulations.

How is sustainability impacting the Dry Film Market?

Sustainability is increasingly impacting the Dry Film Market by driving the development of eco-friendly, halogen-free, and low-VOC (Volatile Organic Compound) dry film solutions. Manufacturers are focusing on green chemistry and responsible production practices to meet stringent environmental regulations and consumer demand for sustainable products.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted