Driverless Tractor Market

Driverless Tractor Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708696 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

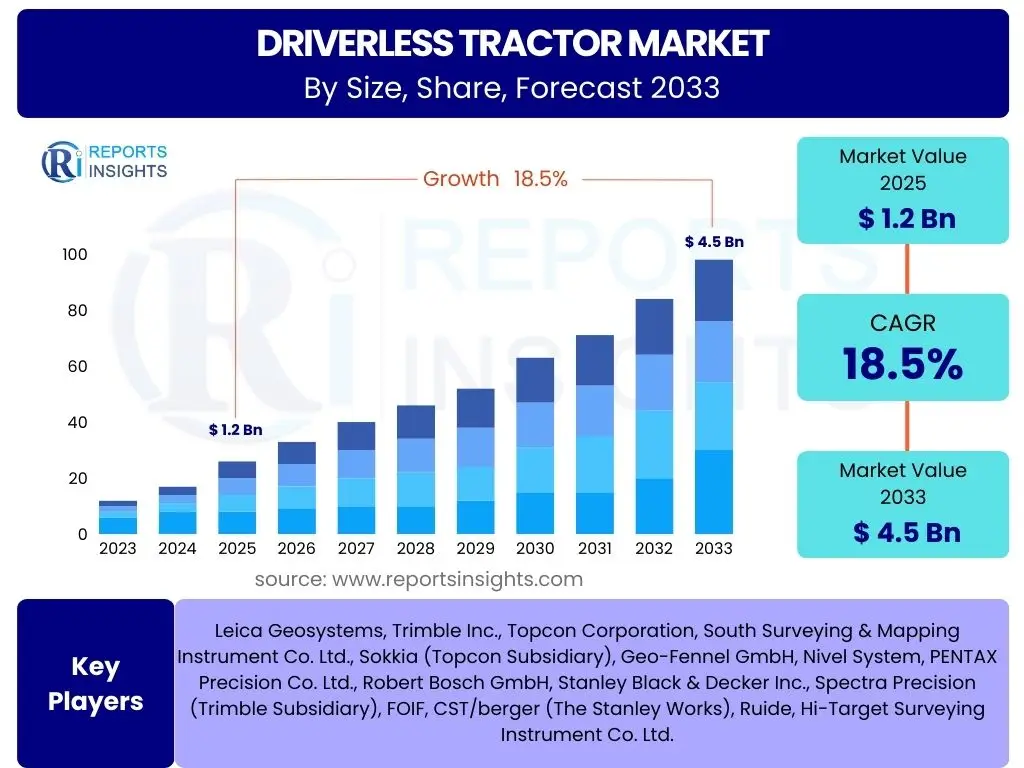

Driverless Tractor Market Size

According to Reports Insights Consulting Pvt Ltd, The Driverless Tractor Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.5% between 2025 and 2033. The market is estimated at USD 1.2 Billion in 2025 and is projected to reach USD 4.5 Billion by the end of the forecast period in 2033.

Key Driverless Tractor Market Trends & Insights

Users frequently inquire about the evolving landscape of agricultural technology, specifically seeking to understand the primary forces shaping the driverless tractor market. Common questions revolve around the adoption rates of autonomous farming equipment, the integration of complementary technologies, and the broader economic and environmental implications. Insights reveal a significant push towards enhancing operational efficiency, mitigating labor shortages, and optimizing resource utilization in modern agriculture. The market is witnessing a profound transformation driven by technological advancements and a growing emphasis on precision farming practices globally.

The convergence of advanced robotics, artificial intelligence, and sophisticated sensor technologies is creating a robust ecosystem for driverless tractors. This trend extends beyond mere automation, encompassing data-driven decision-making, predictive analytics, and seamless integration with broader farm management systems. Furthermore, increasing awareness regarding sustainable agricultural practices and the necessity for higher crop yields with fewer inputs is accelerating the demand for these innovative solutions. These trends are not isolated but are interconnected, forming a comprehensive shift in how agricultural operations are perceived and executed.

- Increasing adoption of precision agriculture techniques.

- Integration of advanced IoT sensors and GPS for enhanced navigation and field mapping.

- Rising demand for automation due to labor shortages and increasing labor costs.

- Development of electric and hybrid autonomous tractors for sustainable farming.

- Emphasis on data analytics and AI for optimized farming decisions.

- Shift towards "Tractor-as-a-Service" and subscription-based models.

- Enhanced connectivity solutions for real-time monitoring and control.

AI Impact Analysis on Driverless Tractor

User inquiries frequently explore how Artificial Intelligence fundamentally redefines the capabilities of driverless tractors, with questions often centering on AI's role in navigation, decision-making, and fault detection. There is a strong interest in understanding how AI contributes to the autonomy of these machines, enabling them to operate with minimal human intervention and adapt to dynamic environmental conditions. Concerns about the reliability and safety of AI-driven systems in real-world agricultural settings are also prevalent, alongside expectations for increased efficiency and yield optimization.

AI serves as the intellectual core of driverless tractors, processing vast amounts of sensory data from cameras, LiDAR, radar, and GPS to enable precise movement, obstacle avoidance, and task execution. Machine learning algorithms allow these tractors to continuously learn from operational data, improving performance over time in areas such as optimal planting patterns, targeted spraying, and efficient harvesting routes. Furthermore, AI-powered predictive analytics contribute significantly to machine health monitoring, forecasting potential failures and enabling proactive maintenance, thereby reducing downtime and operational costs.

The integration of AI also facilitates advanced decision support systems that can analyze soil conditions, weather forecasts, and crop health metrics to recommend optimal actions. This level of intelligent automation transforms farming into a highly optimized and data-driven process, moving beyond simple mechanization to truly smart agriculture. As AI technologies mature, their impact on the precision, efficiency, and sustainability of driverless tractor operations is expected to grow exponentially, addressing complex agricultural challenges with unprecedented accuracy.

- Enhanced navigation and path planning through advanced algorithms.

- Real-time obstacle detection and avoidance using computer vision.

- Predictive analytics for machine maintenance and operational efficiency.

- Optimized planting, spraying, and harvesting based on field data.

- Adaptive learning capabilities to improve performance over time.

- Integration with drone and satellite imagery for comprehensive field analysis.

- Automated decision-making for variable rate applications of inputs.

Key Takeaways Driverless Tractor Market Size & Forecast

Users often seek concise summaries of the most critical insights from market size and forecast data, frequently asking about the overall growth trajectory, the primary drivers of this growth, and the most promising future prospects. They are particularly interested in understanding where significant investments are being made and which technological advancements are expected to have the greatest impact on market expansion. The overarching goal is to grasp the market's trajectory and its implications for agricultural stakeholders and technology providers.

The market is poised for substantial expansion, driven by the imperative for increased agricultural productivity, the scarcity of skilled labor, and rapid technological innovations in automation and artificial intelligence. The forecasted growth reflects a global shift towards adopting advanced farming techniques that promise higher yields, reduced operational costs, and improved environmental stewardship. This trajectory is supported by favorable government policies promoting smart agriculture and rising private sector investments in agritech solutions, signaling a robust and sustained growth period for driverless tractors.

- Significant market growth anticipated over the next decade, indicating a strong adoption curve.

- Technology advancements in AI, IoT, and robotics are core enablers of market expansion.

- Labor shortages and the pursuit of operational efficiency are primary demand drivers.

- Increasing investments from both public and private sectors are fueling innovation.

- North America and Europe currently lead, but Asia Pacific is emerging as a high-growth region.

- Sustainability and environmental impact considerations are becoming increasingly influential.

Driverless Tractor Market Drivers Analysis

The driverless tractor market is propelled by a confluence of factors, primarily stemming from the evolving needs of the agricultural sector. A significant driver is the increasing global population, which demands higher food production, placing immense pressure on farmers to enhance efficiency and yield. This necessity is exacerbated by the shrinking availability of skilled agricultural labor, leading many farms to seek automated solutions to maintain productivity. Driverless tractors address this challenge by enabling continuous operation and optimizing resource allocation, thereby reducing dependency on manual labor.

Furthermore, the growing adoption of precision agriculture techniques plays a crucial role. These techniques, which involve managing inputs like water, fertilizers, and pesticides more precisely, are inherently supported by the high accuracy and repeatability offered by autonomous machinery. Government initiatives and subsidies promoting the modernization of agriculture, coupled with a rising awareness among farmers about the long-term cost benefits and environmental advantages of smart farming, also act as strong market drivers. These elements collectively foster an environment conducive to the widespread integration of driverless tractor technology.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Labor Scarcity in Agriculture | +4.2% | North America, Europe, Australia, Japan | Short to Mid-term |

| Growing Adoption of Precision Agriculture | +3.8% | Global, particularly developed economies | Mid to Long-term |

| Increasing Operational Efficiency & Productivity | +3.5% | Global, large-scale farming operations | Short to Mid-term |

| Advancements in AI, IoT, and Robotics | +3.0% | Global, technology-driven agricultural sectors | Ongoing |

| Government Support & Subsidies for Smart Farming | +2.5% | Europe (CAP), North America (USDA), India (PM-KISAN) | Short to Mid-term |

Driverless Tractor Market Restraints Analysis

Despite the significant growth prospects, the driverless tractor market faces several notable restraints that could temper its expansion. One of the most prominent challenges is the high initial investment cost associated with autonomous agricultural machinery. The advanced technology, sophisticated sensors, and integrated software required for these tractors make them considerably more expensive than traditional models, posing a barrier to adoption for smaller farms or those with limited capital. This financial hurdle often necessitates significant upfront expenditure or access to specialized financing, which is not universally available.

Another critical restraint involves regulatory complexities and the lack of standardized legal frameworks for autonomous vehicles in agriculture across different regions. Issues such as liability in case of accidents, operating permits for driverless machinery on public roads or shared land, and safety protocols are still evolving, creating uncertainty for both manufacturers and potential adopters. Furthermore, technical challenges such as ensuring robust connectivity in remote rural areas, developing foolproof cybersecurity measures, and addressing farmer skepticism regarding the reliability and ease of use of these advanced systems also contribute to market restraints. These factors collectively require comprehensive solutions to unlock the market's full potential.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment Cost | -3.5% | Global, especially small and medium-sized farms | Ongoing |

| Regulatory Hurdles and Lack of Standardization | -2.8% | Europe, North America (state-level variances), developing regions | Mid to Long-term |

| Technical Complexities and Connectivity Issues | -2.2% | Remote rural areas, developing economies | Ongoing |

| Farmer Acceptance and Training Requirements | -1.8% | Global, particularly older generation farmers | Short to Mid-term |

| Cybersecurity Risks and Data Privacy Concerns | -1.5% | Global, technology-reliant farming operations | Ongoing |

Driverless Tractor Market Opportunities Analysis

The driverless tractor market presents numerous compelling opportunities for growth and innovation. One significant area lies in the expansion into emerging agricultural markets, particularly in Asia Pacific and Latin America, where rapid agricultural modernization and increasing farm mechanization rates are creating fertile ground for advanced solutions. These regions, often facing labor shortages and a need for improved efficiency, can leapfrog traditional farming methods by directly adopting autonomous technologies. The potential for integrating these systems into diverse farming practices, from large-scale monoculture to specialized horticulture, offers a broad scope for market penetration.

Another key opportunity is the development of innovative business models, such as "Tractor-as-a-Service" (TaaS) or subscription-based offerings, which can significantly lower the upfront cost barrier for farmers. This approach not only makes driverless technology more accessible but also generates recurring revenue streams for manufacturers and service providers. Furthermore, the continuous evolution of sensor technology, artificial intelligence, and battery-electric powertrains promises to enhance the capabilities and reduce the environmental footprint of driverless tractors, opening doors for specialized applications like vineyard management, orchard farming, and indoor agriculture. These advancements will drive further adoption and create new value propositions for the agricultural sector.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Emerging Agricultural Markets | +4.0% | Asia Pacific, Latin America, Middle East & Africa | Mid to Long-term |

| Development of Subscription & Service Models (TaaS) | +3.5% | Global, particularly for small & medium farms | Short to Mid-term |

| Integration with Broader Smart Farming Ecosystems | +3.2% | Global, technology-forward farms | Mid to Long-term |

| Growth in Niche Applications (Orchards, Vineyards) | +2.8% | Europe, North America, specific agricultural regions | Mid-term |

| Advancements in Electric and Hybrid Autonomous Tractors | +2.0% | Global, driven by sustainability goals | Long-term |

Driverless Tractor Market Challenges Impact Analysis

The driverless tractor market faces a range of challenges that necessitate careful consideration and strategic solutions. One significant hurdle is the need for robust and widespread digital infrastructure in rural areas. Autonomous tractors heavily rely on stable GPS signals, high-speed internet for data transfer, and reliable communication networks, which are often underdeveloped or non-existent in remote farming regions. This lack of infrastructure can severely limit the operational capabilities and broader adoption of these advanced machines, hindering the market's geographic expansion.

Another critical challenge pertains to the ethical and social implications of widespread automation, particularly regarding the potential for job displacement in the agricultural sector. While driverless tractors address labor shortages, they also raise concerns about the future of farm labor, requiring thoughtful policy development and workforce retraining initiatives. Furthermore, navigating complex data privacy regulations and ensuring the security of sensitive farm data collected by autonomous systems remain paramount. The reliability of software and hardware under diverse and often unpredictable environmental conditions, alongside the high technical skill set required for operation and maintenance, also presents a substantial challenge for widespread adoption. Addressing these multifaceted issues will be key to sustainable market growth.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Lack of Adequate Digital Infrastructure in Rural Areas | -3.0% | Developing countries, remote regions globally | Ongoing |

| Societal and Ethical Concerns (e.g., Job Displacement) | -2.5% | Global, particularly regions with high agricultural employment | Mid to Long-term |

| Data Privacy and Cybersecurity Vulnerabilities | -2.0% | Global, technology-reliant farming operations | Ongoing |

| High Complexity of Maintenance and Required Skill Set | -1.8% | Global, small farms, regions with limited technical education | Short to Mid-term |

| Adverse Weather Conditions and Environmental Variability | -1.5% | Global, extreme climate zones | Ongoing |

Driverless Tractor Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global driverless tractor market, offering critical insights into its current size, historical performance, and future growth projections from 2025 to 2033. The report meticulously examines market trends, drivers, restraints, opportunities, and challenges that shape the industry landscape. It also includes a detailed impact analysis of Artificial Intelligence on the market, segmentations by component, automation level, application, and power output, alongside a thorough regional and competitive analysis to provide a holistic view of the market's dynamics and future outlook for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.2 Billion |

| Market Forecast in 2033 | USD 4.5 Billion |

| Growth Rate | 18.5% |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | AGCO Corporation, CNH Industrial N.V., Deere & Company, Kubota Corporation, Fendt (AGCO), Case IH (CNH Industrial), Monarch Tractor, Yanmar Holdings Co. Ltd., SDF Group, CLAAS Group, autonomous_TRACTOR, Blue River Technology (Deere & Company), AI-Robotics AG, SwarmFarm Robotics, AutoAgri AS, Kinze Manufacturing Inc., Valtra Inc., Versatile (Buhler Industries), ZTractor, Agbot (Digital Harvest) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The driverless tractor market is intricately segmented to provide a granular understanding of its diverse components and evolving demand patterns. This segmentation allows for targeted analysis of technological preferences, application-specific requirements, and regional adoption rates, revealing key areas of growth and market saturation. By breaking down the market into its constituent parts, stakeholders can better identify niche opportunities, understand competitive landscapes, and formulate precise market entry or expansion strategies, ensuring that product development and marketing efforts are highly effective and aligned with actual market needs.

Understanding these segments is crucial for both manufacturers seeking to innovate and farmers looking to adopt the most suitable technology for their operations. For instance, the distinction between semi-autonomous and fully autonomous systems reflects varying levels of technological maturity and regulatory acceptance, influencing procurement decisions. Similarly, segmenting by power output caters to the diverse scale of farming operations, from small-scale specialized agriculture to large-acreage crop production. This detailed approach enables a more accurate forecast and a deeper insight into the market's complex structure.

- By Component:

- Hardware (GPS, Sensors, Cameras, Telematics, Actuators)

- Software (Farm Management Software, Autonomy Software, Data Analytics Platforms)

- Services (Consulting, Maintenance & Support, Training, Integration Services)

- By Automation Level:

- Semi-Autonomous (Operator-assisted with autonomous features)

- Fully Autonomous (No human intervention required during operation)

- By Application:

- Plowing & Tillage

- Seeding & Planting

- Spraying & Fertilizing

- Harvesting & Threshing

- Crop Monitoring & Scouting

- Material Handling & Logistics

- Others (e.g., Mowing, Weeding)

- By Power Output:

- Less than 30 HP (Compact and specialized tractors)

- 30-100 HP (Mid-range, versatile farm tasks)

- More than 100 HP (High-power, large-scale operations)

- By Region:

- North America (U.S., Canada, Mexico)

- Europe (Germany, UK, France, Italy, Spain, Rest of Europe)

- Asia Pacific (China, India, Japan, Australia, South Korea, Rest of APAC)

- Latin America (Brazil, Argentina, Rest of Latin America)

- Middle East & Africa (South Africa, Saudi Arabia, UAE, Rest of MEA)

Regional Highlights

The global driverless tractor market exhibits significant regional variations, influenced by factors such as agricultural practices, economic development, regulatory frameworks, and technological adoption rates. North America stands out as a pioneering region, largely due to its extensive farmlands, high adoption of precision agriculture, and early investments in agricultural automation. The presence of major agricultural machinery manufacturers and a proactive approach towards integrating advanced technologies further solidify its leading position. Farmers in this region are often early adopters, driven by labor shortages and the pursuit of maximizing efficiency on large-scale operations.

Europe also represents a substantial market, characterized by its strong emphasis on sustainable farming practices, stringent environmental regulations, and a robust framework for smart agriculture initiatives. Countries such as Germany, France, and the Netherlands are at the forefront of adopting driverless technologies, propelled by EU policies that support agricultural modernization and environmental stewardship. While initial costs remain a consideration, the long-term benefits in terms of resource optimization and reduced ecological footprint are key motivators for adoption across the continent.

The Asia Pacific region is poised for the most rapid growth, primarily driven by the modernization of agricultural practices in populous countries like China and India, where increasing food demand and rural labor migration necessitate automation. Government initiatives to promote farm mechanization and provide subsidies for advanced equipment are accelerating market penetration. Latin America, particularly Brazil and Argentina, also presents a promising market with its vast agricultural lands and a growing interest in improving farm productivity. The Middle East and Africa, while nascent, show potential with selective large-scale agricultural projects and increasing investments in food security technologies.

- North America: Leading the market due to large farm sizes, high labor costs, early adoption of precision agriculture, and strong R&D in agritech. The U.S. is a dominant player.

- Europe: Significant market share driven by sustainable farming initiatives, favorable government policies (e.g., CAP), and technological advancements in countries like Germany, France, and the UK.

- Asia Pacific (APAC): Fastest-growing region, propelled by agricultural modernization in China and India, increasing demand for food, and government support for farm mechanization.

- Latin America: Emerging market with substantial growth potential, particularly in Brazil and Argentina, due to vast agricultural areas and the need for efficiency gains.

- Middle East & Africa (MEA): Nascent market, but with growing investments in large-scale agricultural projects and smart farming technologies to enhance food security.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Driverless Tractor Market.- Deere & Company

- AGCO Corporation

- CNH Industrial N.V.

- Kubota Corporation

- Fendt (AGCO)

- Case IH (CNH Industrial)

- Monarch Tractor

- Yanmar Holdings Co. Ltd.

- SDF Group

- CLAAS Group

- autonomous_TRACTOR

- Blue River Technology (Deere & Company)

- AI-Robotics AG

- SwarmFarm Robotics

- AutoAgri AS

- Kinze Manufacturing Inc.

- Valtra Inc.

- Versatile (Buhler Industries)

- ZTractor

- Agbot (Digital Harvest)

Frequently Asked Questions

What is a driverless tractor?

A driverless tractor, also known as an autonomous or robotic tractor, is an agricultural vehicle designed to operate without a human operator in the cab. It uses technologies like GPS, AI, sensors, and machine learning to navigate, detect obstacles, and perform various farming tasks such as plowing, planting, spraying, and harvesting with high precision.

How do driverless tractors benefit farmers?

Driverless tractors offer numerous benefits including increased operational efficiency, reduced labor costs, extended operating hours (even at night), optimized resource utilization through precision farming, lower fuel consumption, and improved crop yields due to highly accurate and consistent operations. They also address the growing shortage of skilled agricultural labor.

What are the main challenges for driverless tractor adoption?

Key challenges include the high initial investment cost, regulatory complexities and the lack of standardized legal frameworks for autonomous vehicles, the need for robust digital infrastructure in rural areas, cybersecurity risks, and issues related to farmer acceptance and the training required for operating and maintaining these advanced machines.

What is the role of AI in driverless tractors?

AI is crucial for driverless tractors, enabling intelligent navigation, real-time obstacle detection and avoidance, predictive maintenance, and optimized task execution. AI algorithms process sensor data to make autonomous decisions, adapt to changing field conditions, and contribute to precision agriculture by analyzing data for informed input applications and yield management.

Which regions are leading in driverless tractor adoption?

North America and Europe currently lead in driverless tractor adoption due to their large-scale farming operations, high labor costs, proactive government support for agricultural technology, and well-developed technological infrastructure. The Asia Pacific region is projected to be the fastest-growing market, driven by agricultural modernization and increasing demand for efficiency.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted