Driverless Car Software Market

Driverless Car Software Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704125 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

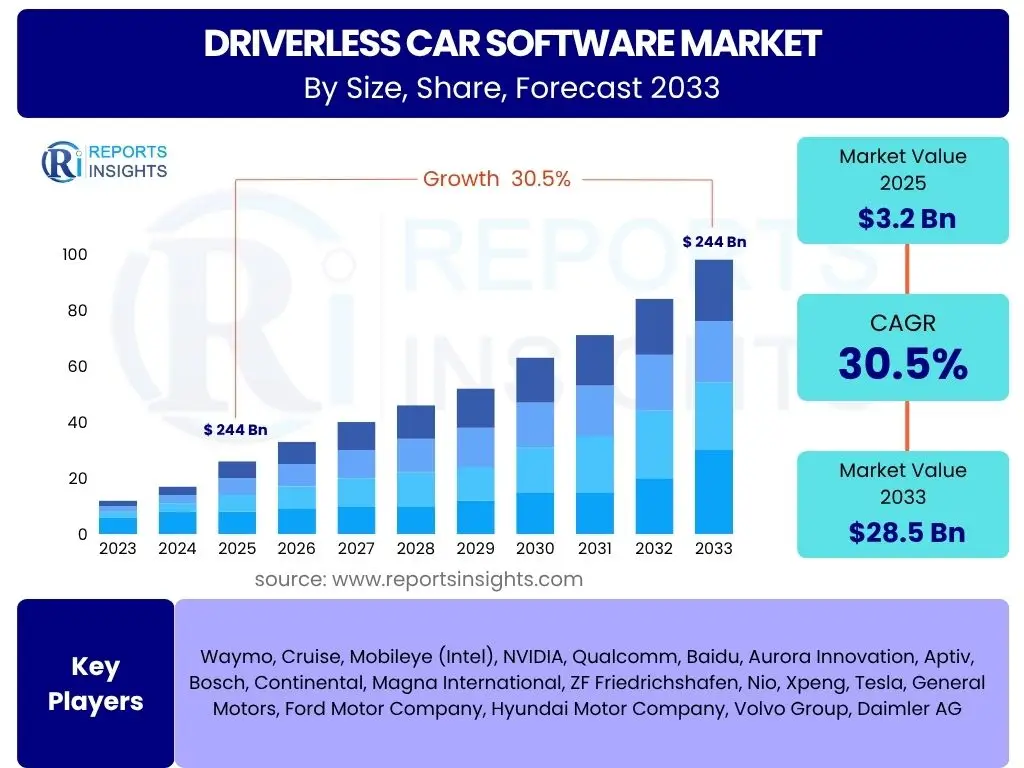

Driverless Car Software Market Size

According to Reports Insights Consulting Pvt Ltd, The Driverless Car Software Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 30.5% between 2025 and 2033. The market is estimated at USD 3.2 Billion in 2025 and is projected to reach USD 28.5 Billion by the end of the forecast period in 2033.

Key Driverless Car Software Market Trends & Insights

The driverless car software market is experiencing profound transformation, driven by a rapid evolution towards higher levels of autonomous capability. This involves a sophisticated integration of advanced algorithms for perception, decision-making, and vehicle control, moving beyond basic driver assistance systems to achieve conditional and eventually full self-driving functionalities. Innovations in sensor fusion, leveraging data from LiDAR, radar, cameras, and ultrasonic sensors, are crucial for robust environmental understanding, enabling vehicles to navigate complex and dynamic real-world scenarios with enhanced safety and reliability.

A significant trend observed is the increasing reliance on artificial intelligence and machine learning, particularly deep learning, to process vast amounts of data and enable predictive capabilities. This allows autonomous systems to anticipate the behavior of other road users, optimize routes in real-time, and adapt to unforeseen circumstances. Furthermore, the development of robust cybersecurity measures and secure over-the-air (OTA) update mechanisms is paramount, ensuring system integrity and facilitating continuous performance improvements and feature enhancements post-deployment.

The market is also shaped by evolving regulatory landscapes and the emergence of new business models. Governments worldwide are developing frameworks to govern autonomous vehicle testing and deployment, while the industry explores revenue streams beyond traditional car sales, such as Mobility-as-a-Service (MaaS) platforms, autonomous delivery, and long-haul trucking. Collaboration between automotive OEMs, technology companies, and software specialists is accelerating innovation, leading to more integrated and scalable software solutions for various autonomous applications.

- Progression towards Level 3, 4, and 5 autonomous driving capabilities.

- Deep integration of AI and Machine Learning for enhanced perception, decision-making, and path planning.

- Emphasis on sensor fusion technology for comprehensive environmental modeling.

- Rising importance of cybersecurity protocols and over-the-air (OTA) software updates.

- Development of robust simulation and validation platforms for testing autonomous software.

- Growth of Mobility-as-a-Service (MaaS) and autonomous fleet operations.

- Increased collaboration between automotive manufacturers and tech companies.

- Focus on ethical AI and explainable AI for autonomous systems.

- Standardization efforts for communication protocols and data formats (e.g., V2X).

AI Impact Analysis on Driverless Car Software

Artificial intelligence stands as the foundational pillar for driverless car software, fundamentally transforming capabilities in perception, localization, and decision-making. Deep learning algorithms power advanced object detection, classification, and tracking from various sensor inputs, enabling vehicles to accurately interpret their surroundings in complex and dynamic environments. This cognitive layer allows the software to identify pedestrians, other vehicles, traffic signals, and road signs with unprecedented precision, far exceeding traditional rule-based programming.

Beyond perception, AI significantly enhances the car's ability to predict behaviors and plan trajectories safely and efficiently. Reinforcement learning and predictive analytics enable the software to anticipate the actions of other road users, optimize routing, and execute complex maneuvers like lane changes and merges. This continuous learning capability, often facilitated by extensive simulation and real-world data, allows the system to adapt and improve its performance over time, addressing edge cases and enhancing overall system robustness and reliability.

The integration of AI also addresses critical safety aspects by enabling redundant systems and real-time anomaly detection. AI-driven fault diagnosis and predictive maintenance capabilities are becoming integral, ensuring the software operates reliably and identifies potential issues before they compromise safety. Furthermore, the development of explainable AI (XAI) is crucial for building trust and meeting regulatory requirements by providing transparency into the decision-making processes of autonomous systems, which is vital for widespread adoption and legal frameworks.

- Enhanced perception through deep learning for object detection, classification, and tracking.

- Improved decision-making and path planning using reinforcement learning and predictive analytics.

- Real-time adaptation to dynamic environments and unforeseen scenarios.

- Facilitation of continuous learning and system improvement via vast datasets and simulations.

- Advancements in sensor fusion algorithms for more accurate environmental understanding.

- Development of robust safety systems and anomaly detection capabilities.

- Enabling of explainable AI (XAI) for transparency and regulatory compliance.

- Optimization of energy efficiency and route planning in autonomous fleets.

- Creation of synthetic data for training AI models in challenging edge cases.

Key Takeaways Driverless Car Software Market Size & Forecast

The driverless car software market is poised for exceptional growth, driven by escalating investments in autonomous vehicle technology and a global push towards enhancing road safety and transportation efficiency. The forecasted substantial Compound Annual Growth Rate underscores the industry's rapid maturity and the increasing integration of sophisticated software solutions across various vehicle platforms. This growth is not merely incremental but represents a fundamental shift in automotive technology, where software becomes the central nervous system of future mobility, dictating performance, safety, and functionality.

A critical insight from the market forecast is the pivotal role of software as the differentiating factor and core intellectual property in the autonomous vehicle ecosystem. Unlike hardware, software offers continuous improvement through over-the-air updates, adapts to diverse environmental conditions, and enables novel service models such as Mobility-as-a-Service. Companies focusing on developing robust, scalable, secure, and continuously improvable software platforms are strategically positioned to capture significant market share and define the future landscape of autonomous driving, establishing a competitive edge.

The market's trajectory is heavily influenced by evolving regulatory developments and the critical factor of public acceptance. While technological advancements continue to accelerate, the pace of widespread commercial deployment and consumer adoption will largely depend on the establishment of clear legal frameworks, the development of universally accepted safety standards, and successful efforts to build consumer trust in autonomous systems. The forecast implicitly accounts for a gradual but steady resolution of these non-technical barriers, allowing the innovative software solutions to proliferate and realize their full market potential globally.

- Significant market expansion driven by technological advancements and investment.

- Software as the primary value driver and differentiator in autonomous vehicles.

- Crucial role of regulatory clarity and public trust for widespread adoption.

- Continuous innovation in AI, machine learning, and sensor fusion as growth catalysts.

- Emergence of new business models, particularly in autonomous fleet operations.

- Long-term shift from traditional vehicle ownership to service-based mobility.

- Cybersecurity and data privacy are increasingly central to software development.

- Global competition intensifying among technology firms and automotive OEMs.

Driverless Car Software Market Drivers Analysis

The driverless car software market is propelled by a confluence of technological advancements, economic imperatives, and societal demands. A primary driver is the pursuit of enhanced road safety, with autonomous software promising to drastically reduce human error-related accidents, which account for a vast majority of traffic fatalities. This safety imperative incentivizes significant investments in sophisticated software development aimed at achieving higher levels of autonomy and reliability. Furthermore, the increasing demand for advanced convenience features and hands-free driving experiences in passenger vehicles contributes substantially to market growth, as consumers seek more relaxed and productive travel times.

Economic benefits also serve as powerful drivers for this market. Autonomous vehicles, powered by advanced software, offer the potential for optimized fuel efficiency through smoother driving patterns, reduced traffic congestion, and lower operational costs for commercial fleets. The prospect of logistics companies realizing substantial savings by eliminating driver wages and optimizing routes is a strong incentive for the adoption of autonomous trucking and delivery solutions. Additionally, government initiatives and smart city projects worldwide are actively promoting autonomous vehicle research, development, and deployment, recognizing their potential to revolutionize urban planning, public transportation, and environmental sustainability.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Enhanced Safety and Accident Reduction | +3.0% | Global | Long-term (2025-2033) |

| Increasing Demand for Autonomous Features | +2.8% | North America, Europe, Asia Pacific | Mid-term (2025-2030) |

| Technological Advancements in AI and ML | +2.5% | Global | Long-term (2025-2033) |

| Government Initiatives and Smart City Projects | +2.0% | China, US, EU, Japan | Mid-term (2025-2030) |

| Cost Reduction for Commercial Fleets | +1.5% | North America, Europe, Asia Pacific | Mid-term (2025-2030) |

Driverless Car Software Market Restraints Analysis

Despite its significant potential, the driverless car software market faces several formidable restraints that could impede its growth trajectory. One of the most significant challenges is the immense cost associated with research and development, as well as the initial deployment of autonomous vehicle software. Developing, rigorously testing, and validating software capable of handling infinite real-world scenarios demands substantial financial investment in talent, computational resources, and extensive testing infrastructure, which can deter smaller players and slow down market penetration.

Regulatory hurdles and complex legal liabilities also present considerable obstacles. The absence of a harmonized global regulatory framework creates fragmentation, making it difficult for developers to create universally compliant software. Questions surrounding liability in the event of an accident involving an autonomous vehicle remain largely unresolved, posing significant legal risks for manufacturers and software providers. This regulatory uncertainty can lead to delays in product launches and limit the geographical scope of deployment for driverless car software solutions.

Furthermore, public acceptance and trust issues represent a substantial restraint. Incidents involving autonomous vehicles, even when rare, tend to garner significant media attention, eroding public confidence and fostering skepticism about the safety and reliability of driverless technology. Overcoming this perception challenge requires not only flawless technological performance but also comprehensive educational campaigns and transparent communication to build public trust. Cybersecurity threats and data privacy concerns also contribute to restraints, as the increasing connectivity of autonomous vehicles makes them potential targets for malicious attacks, raising concerns about the security of personal and operational data.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of R&D and Deployment | -2.5% | Global | Long-term (2025-2033) |

| Regulatory Hurdles and Legal Liabilities | -2.0% | Global (especially US, EU, China) | Long-term (2025-2033) |

| Public Acceptance and Trust Issues | -1.8% | Global | Long-term (2025-2033) |

| Cybersecurity Threats and Data Privacy Concerns | -1.5% | Global | Long-term (2025-2033) |

| Complexity of Real-World Scenario Handling | -1.2% | Global | Long-term (2025-2033) |

Driverless Car Software Market Opportunities Analysis

The driverless car software market is replete with significant opportunities stemming from expanding application areas and continuous technological evolution. A major opportunity lies in the burgeoning sector of logistics and commercial fleets, including autonomous trucking, last-mile delivery vehicles, and industrial automation. The potential for substantial operational cost reductions, increased efficiency, and 24/7 operability makes this segment highly attractive for software providers, driving demand for specialized and robust autonomous driving solutions tailored for commercial environments.

Furthermore, the development of advanced sensor fusion techniques and high-definition mapping capabilities presents a crucial opportunity for market players. As autonomous systems become more sophisticated, the ability to accurately fuse data from diverse sensors (LiDAR, radar, cameras) and integrate it with ultra-precise maps is paramount for safe and reliable navigation. Innovations in these areas, including real-time mapping updates and crowdsourced mapping solutions, will unlock higher levels of autonomy and expand operational design domains for driverless vehicles.

The growth of Mobility-as-a-Service (MaaS) platforms also offers a fertile ground for market expansion. Autonomous ride-hailing services, shared autonomous shuttles, and subscription-based mobility solutions are transforming urban transportation. Software providers can capitalize on this trend by developing comprehensive platforms that integrate fleet management, dispatch, payment systems, and user interfaces, moving beyond just the core driving software. The increasing integration with smart city infrastructure, such as intelligent traffic management systems and V2X (Vehicle-to-Everything) communication, further enhances the capabilities and safety of autonomous vehicles, opening new avenues for software development and deployment in interconnected urban environments.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Logistics and Commercial Fleets | +3.5% | North America, Europe, Asia Pacific | Mid-term (2025-2030) |

| Development of Advanced Sensor Fusion and Mapping | +3.0% | Global | Long-term (2025-2033) |

| Growth in Mobility-as-a-Service (MaaS) Platforms | +2.5% | Urban areas globally | Mid-term (2025-2030) |

| Integration with Smart Infrastructure (V2X) | +2.0% | Developed Nations, Smart Cities | Long-term (2025-2033) |

| Emergence of New Data Monetization Models | +1.5% | Global | Long-term (2025-2033) |

Driverless Car Software Market Challenges Impact Analysis

The driverless car software market faces several critical challenges that demand innovative solutions and persistent effort from industry stakeholders. One of the most significant challenges is the immense complexity of handling real-world scenarios, particularly edge cases that are rare but critical for safety. Autonomous software must reliably interpret and react to an infinite number of unforeseen situations, from unusual weather conditions and debris on the road to erratic pedestrian behavior and ambiguous traffic signals. Ensuring robust performance across such diverse and unpredictable environments requires extensive data collection, sophisticated AI model training, and rigorous validation, which is incredibly resource-intensive.

Another key challenge lies in ensuring the robust software validation and testing required to meet stringent safety standards and build public trust. Traditional testing methods are insufficient for autonomous systems; therefore, the industry relies heavily on simulation, closed-track testing, and vast public road mileage. Developing comprehensive testing methodologies that can definitively prove the safety and reliability of autonomous software, especially for higher levels of autonomy, remains a complex technical and logistical hurdle. Furthermore, achieving interoperability and standardization across various hardware platforms, sensor suites, and software components from different manufacturers poses a significant challenge, hindering seamless integration and economies of scale.

Finally, the driverless car software sector is grappling with a severe talent shortage in highly specialized fields such as AI engineering, robotics, cybersecurity, and advanced software development. The demand for experts in deep learning, computer vision, sensor fusion, and functional safety significantly outstrips the available supply, leading to intense competition for skilled professionals and escalating labor costs. This talent gap can slow down development cycles, limit innovation, and ultimately impact the pace of market growth and the deployment of advanced autonomous solutions.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complexity of Real-World Scenarios Handling | -3.0% | Global | Long-term (2025-2033) |

| Ensuring Robust Software Validation and Testing | -2.8% | Global | Long-term (2025-2033) |

| Interoperability and Standardization Issues | -2.2% | Global | Mid-term (2025-2030) |

| Talent Shortage in AI and Robotics Engineering | -1.7% | Global | Long-term (2025-2033) |

| High Computational Power Requirements | -1.0% | Global | Mid-term (2025-2030) |

Driverless Car Software Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global Driverless Car Software Market, offering crucial insights into its size, growth trajectory, key trends, and competitive landscape. The scope includes a detailed examination of market drivers, restraints, opportunities, and challenges that are shaping the industry. It covers historical data from 2019 to 2023, provides a base year analysis for 2024, and forecasts market performance up to 2033. The report meticulously segments the market by component, autonomy level, application, vehicle type, software type, and deployment, offering a granular view of market dynamics across various categories and key regions. It also profiles leading companies, providing strategic insights for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 3.2 Billion |

| Market Forecast in 2033 | USD 28.5 Billion |

| Growth Rate | 30.5% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Waymo, Cruise, Mobileye (Intel), NVIDIA, Qualcomm, Baidu, Aurora Innovation, Aptiv, Bosch, Continental, Magna International, ZF Friedrichshafen, Nio, Xpeng, Tesla, General Motors, Ford Motor Company, Hyundai Motor Company, Volvo Group, Daimler AG |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The driverless car software market is meticulously segmented to provide a comprehensive understanding of its diverse components and applications. This granular segmentation allows for a detailed analysis of market dynamics, growth potential, and emerging trends within specific categories. By breaking down the market based on various criteria, stakeholders can identify niche opportunities, assess competitive landscapes, and formulate targeted strategies to capitalize on the evolving demand for autonomous vehicle software solutions across different autonomy levels, vehicle types, and deployment models.

Understanding these segments is crucial for both technology developers and automotive manufacturers. For instance, the distinction between Level 2 and Level 5 autonomy software highlights the increasing complexity and capabilities required, influencing investment and development priorities. Similarly, the varying demands of passenger cars versus commercial vehicles necessitate specialized software functionalities, from routing algorithms for ride-hailing services to advanced object recognition for heavy-duty trucks. This structured approach to market analysis ensures that all key facets of the driverless car software ecosystem are thoroughly examined, providing actionable insights for strategic decision-making and innovation.

- By Component: Software, Services

- By Autonomy Level: Level 2, Level 3, Level 4, Level 5

- By Application: Passenger Cars, Commercial Vehicles (Trucks, Buses, Robotaxis, Delivery Vehicles)

- By Vehicle Type: Electric Vehicles (EVs), Hybrid Electric Vehicles (HEVs), Internal Combustion Engine (ICE) Vehicles

- By Software Type: Perception Software, Localization and Mapping Software, Path Planning Software, Control Software, Sensor Fusion Software, Operating Systems, Predictive Maintenance Software

- By Deployment: Embedded Software, Cloud-based Software

Regional Highlights

- North America: This region stands as a significant hub for driverless car software innovation and adoption, largely driven by substantial R&D investments, the presence of leading technology companies in Silicon Valley, and strong governmental support for autonomous vehicle testing. The United States, in particular, has seen extensive real-world testing of autonomous fleets, leading to advanced software development for Level 4 and Level 5 capabilities. Early regulatory frameworks in certain states have also fostered a conducive environment for market growth and rapid technological advancements in software solutions.

- Europe: Europe exhibits a strong focus on regulatory harmonization and safety standards for autonomous vehicles, which profoundly influences software development. Countries like Germany and the UK are investing heavily in smart infrastructure integration and developing advanced software for Level 3 autonomy. European automotive OEMs are at the forefront of integrating sophisticated driver assistance and partial automation software, with a growing emphasis on cybersecurity and data privacy in their autonomous systems.

- Asia Pacific (APAC): The APAC region, particularly China, Japan, and South Korea, is experiencing rapid growth in the driverless car software market due to strong government backing, massive investments in smart city initiatives, and a large consumer base. China is a leader in autonomous ride-hailing services and logistics, driving innovation in AI-powered perception and real-time mapping software. Japan and South Korea are focusing on advanced sensor technology and sophisticated control algorithms, aiming for high levels of automation in urban environments.

- Latin America: While an emerging market, Latin America presents potential for driverless car software adoption, especially in logistics and public transportation. Pilot programs for autonomous shuttles and last-mile delivery are gaining traction in major cities, driving demand for scalable and cost-effective software solutions. Challenges related to infrastructure and regulatory development are gradually being addressed, paving the way for future market expansion.

- Middle East and Africa (MEA): The MEA region is characterized by ambitious smart city projects and a strong emphasis on diversifying economies away from oil, leading to increasing interest in autonomous vehicle technology. Countries like the UAE and Saudi Arabia are exploring fully autonomous public transport systems and robotaxis, creating demand for robust and highly reliable driverless car software capable of operating in diverse urban and environmental conditions.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Driverless Car Software Market.- Waymo

- Cruise

- Mobileye (Intel)

- NVIDIA

- Qualcomm

- Baidu

- Aurora Innovation

- Aptiv

- Bosch

- Continental

- Magna International

- ZF Friedrichshafen

- Nio

- Xpeng

- Tesla

- General Motors

- Ford Motor Company

- Hyundai Motor Company

- Volvo Group

- Daimler AG

Frequently Asked Questions

What is the primary driver of growth in the driverless car software market?

The primary driver is the pursuit of enhanced road safety by reducing human error, alongside the potential for significant improvements in transportation efficiency, reduced congestion, and operational cost savings for commercial fleets.

What are the main challenges facing the widespread adoption of driverless car software?

Key challenges include navigating complex regulatory frameworks, overcoming public acceptance and trust issues, mitigating high development and deployment costs, ensuring robust cybersecurity, and reliably handling diverse real-world edge cases.

How does Artificial Intelligence contribute to driverless car software development?

AI is fundamental, enabling advanced perception (object detection, classification), intelligent decision-making, predictive behavior analysis, and adaptive path planning through deep learning and reinforcement learning, crucial for autonomous vehicle functionality and safety.

What is the difference between Level 3 and Level 5 autonomy in driverless cars?

Level 3 (Conditional Automation) means the vehicle can perform most driving tasks under specific conditions but requires human driver intervention when prompted. Level 5 (Full Automation) signifies the vehicle can drive itself under all conditions, without human intervention, in all environments.

Which regions are leading in driverless car software adoption and innovation?

North America (particularly the US), Asia Pacific (especially China, Japan, and South Korea), and Europe are leading regions due to significant R&D investments, supportive regulatory environments, and high demand for autonomous mobility solutions.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted