Drain Waste Vent System Market

Drain Waste Vent System Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_710296 | Last Updated : January 02, 2026 |

Format : ![]()

![]()

![]()

![]()

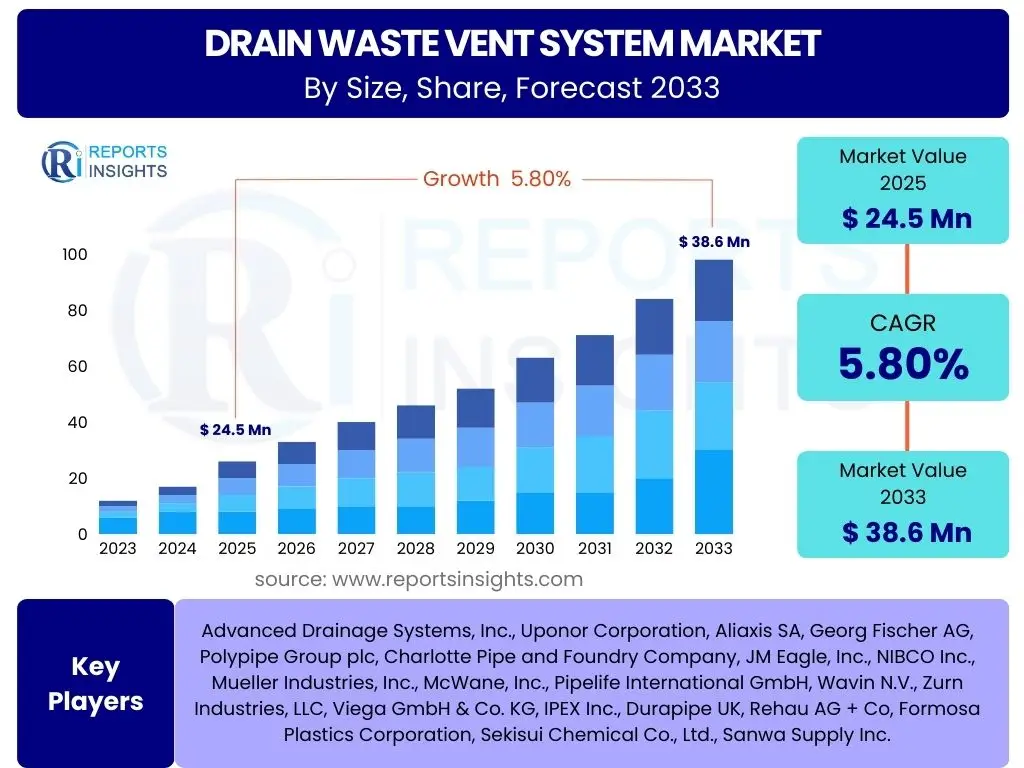

Drain Waste Vent System Market Size

According to Reports Insights Consulting Pvt Ltd, The Drain Waste Vent System Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 24.5 billion in 2025 and is projected to reach USD 38.6 billion by the end of the forecast period in 2033.

Key Drain Waste Vent System Market Trends & Insights

User inquiries frequently highlight evolving material preferences, the integration of smart building technologies, and increasing regulatory scrutiny as central themes within the Drain Waste Vent (DWV) system market. Stakeholders are particularly interested in understanding the shift towards sustainable and resilient piping materials, reflecting both environmental concerns and the demand for long-lasting infrastructure. Furthermore, the role of prefabrication and modular construction methods is gaining traction, driven by efficiency and cost-saving imperatives in large-scale projects.

Another significant area of interest revolves around the adoption of advanced monitoring and diagnostic tools for DWV systems, particularly in commercial and high-density residential buildings. This trend is fueled by the need for proactive maintenance, leak detection, and optimized system performance. The overall market is observing a push towards systems that offer ease of installation, improved hygienic properties, and enhanced resistance to corrosion and chemical degradation, responding to the persistent challenges faced in maintaining conventional plumbing infrastructure across diverse geographic and climatic conditions.

- Shift towards sustainable and recyclable piping materials such as high-density polyethylene (HDPE) and advanced plastics.

- Growing adoption of prefabricated DWV system components for faster installation and reduced on-site labor costs.

- Integration of smart plumbing solutions, including leak detection sensors and real-time monitoring systems.

- Increased demand for silent and low-noise DWV systems in residential and hospitality sectors.

- Stricter building codes and environmental regulations driving the need for more efficient and compliant DWV solutions.

AI Impact Analysis on Drain Waste Vent System

Common user questions regarding AI's impact on the Drain Waste Vent system market frequently revolve around predictive maintenance, optimized design, and enhanced operational efficiency. Users are keenly interested in how artificial intelligence can analyze data from smart sensors to anticipate potential blockages, leaks, or system failures before they occur, thereby reducing costly emergency repairs and downtime. There is also a significant focus on AI's ability to refine the design process for DWV systems, allowing for more precise sizing, routing, and material selection that adheres to complex building codes and optimizes flow dynamics.

Furthermore, inquiries often touch upon AI's role in improving the sustainability aspects of DWV systems, for example, by optimizing water usage in commercial buildings or identifying inefficiencies in wastewater management. The potential for AI-driven robotics in inspection and maintenance of inaccessible DWV components, particularly in large-scale industrial or municipal applications, also garners considerable attention. Overall, the expectation is that AI will transform DWV systems from passive infrastructure into intelligent, self-monitoring, and highly efficient networks, contributing to smarter, more resilient built environments.

- AI-powered predictive maintenance for early detection of potential DWV system failures and blockages.

- Optimized design and simulation of DWV layouts using AI algorithms, improving efficiency and material usage.

- Enhanced leak detection and water damage prevention through AI-driven sensor networks.

- Automated inspection and monitoring of complex DWV infrastructure using AI and robotics.

- Improved operational efficiency and resource management in large-scale buildings through AI-based system analytics.

Key Takeaways Drain Waste Vent System Market Size & Forecast

User queries regarding key takeaways from the Drain Waste Vent (DWV) system market size and forecast consistently point to the importance of material innovation, regulatory influence, and technological integration. Stakeholders are seeking concise information on the primary growth drivers, understanding that urbanization and infrastructure development are foundational. The market's resilience, even amidst economic fluctuations, is often a topic of interest, underscoring the essential nature of DWV systems in all types of construction.

Moreover, the forecast highlights a sustained demand for efficient and durable DWV solutions, propelled by global efforts towards sustainable building practices and public health. The increasing complexity of building designs and the need for systems that comply with stringent environmental standards are shaping both product development and market expansion strategies. The ability of manufacturers to adapt to these evolving demands, particularly in emerging economies, will be crucial for capturing future market share and sustaining growth throughout the forecast period.

- Consistent growth driven by urbanization, infrastructure development, and stringent health regulations.

- Material innovation, particularly in plastics and composites, remains a critical factor for market evolution.

- Technological advancements, including smart monitoring and predictive maintenance, are set to enhance system longevity and efficiency.

- Sustainability and environmental compliance are increasingly influencing product design and market demand.

- Emerging economies present significant opportunities due to rapid construction and evolving building standards.

Drain Waste Vent System Market Drivers Analysis

The Drain Waste Vent system market is propelled by several robust factors, predominantly stemming from global construction activities and escalating urbanization. Rapid expansion of residential, commercial, and industrial sectors, particularly in developing economies, directly translates into increased demand for new plumbing installations and system upgrades. Concurrently, the imperative for improved public health and sanitation standards, coupled with stricter regulatory mandates worldwide, necessitates the deployment of advanced and compliant DWV systems, ensuring safe and efficient waste removal.

Additionally, the burgeoning focus on sustainable building practices and green construction initiatives contributes significantly to market growth. This involves the adoption of more durable, energy-efficient, and environmentally friendly DWV materials and technologies. Furthermore, the aging infrastructure in many developed regions creates a substantial market for renovation, repair, and replacement projects, ensuring a continuous demand cycle for DWV components and systems. The ongoing innovation in material science also introduces better-performing and easier-to-install solutions, further stimulating market expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Construction Boom & Urbanization | +1.8% | Asia Pacific, North America, Middle East | Short to Mid-term (2025-2029) |

| Increasing Focus on Public Health & Sanitation | +1.5% | Global, particularly South Asia, Africa | Mid to Long-term (2027-2033) |

| Stricter Building Codes & Environmental Regulations | +1.2% | Europe, North America, East Asia | Short to Mid-term (2025-2028) |

| Aging Infrastructure Replacement in Developed Regions | +0.9% | North America, Western Europe | Mid to Long-term (2026-2033) |

| Technological Advancements in Piping Materials | +0.7% | Global | Short to Long-term (2025-2033) |

Drain Waste Vent System Market Restraints Analysis

The Drain Waste Vent system market faces several restraining factors that could impede its growth trajectory. Significant among these are the fluctuating raw material prices, particularly for metals like cast iron and copper, and petrochemical derivatives used in plastic piping. Such volatility directly impacts manufacturing costs and, consequently, the final product prices, potentially leading to project delays or budget cuts in construction. The intensity of competition from unorganized sectors, especially in developing regions, offering lower-cost, often substandard, products also presents a challenge, undermining quality standards and market integrity.

Furthermore, the long lifespan of existing DWV installations can defer replacement cycles, particularly in regions with established infrastructure and robust maintenance regimes. Economic downturns and geopolitical instabilities can also significantly slow down construction activities, thereby reducing immediate demand for new DWV systems. The labor-intensive nature of installation, coupled with a shortage of skilled plumbing professionals in various regions, adds another layer of constraint, leading to higher labor costs and potential project backlogs, impacting overall market efficiency and expansion.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile Raw Material Prices | -0.8% | Global | Short to Mid-term (2025-2028) |

| High Installation Costs & Labor Shortages | -0.6% | North America, Western Europe | Mid-term (2026-2030) |

| Slow Adoption of Advanced Technologies | -0.5% | Developing Regions | Mid to Long-term (2027-2033) |

| Stringent Environmental & Disposal Regulations | -0.4% | Europe, North America | Short-term (2025-2027) |

Drain Waste Vent System Market Opportunities Analysis

The Drain Waste Vent system market is poised for significant growth through several emerging opportunities that capitalize on global demographic and technological shifts. The rapid urbanization in emerging economies, particularly across Asia Pacific and parts of Africa, necessitates extensive new construction projects for residential, commercial, and public infrastructure, creating a substantial demand for DWV systems. This demand is further amplified by government initiatives aimed at improving sanitation and hygiene standards in these regions, often leading to large-scale public plumbing projects and modernization programs.

Furthermore, the growing emphasis on sustainable and green building certifications presents a lucrative opportunity for manufacturers to innovate with eco-friendly materials and energy-efficient DWV solutions. Smart city initiatives globally are also opening avenues for integrating intelligent DWV systems that feature real-time monitoring, predictive maintenance, and optimized resource management. The market also benefits from the increasing demand for prefabricated and modular construction, which streamline installation processes and reduce project timelines, offering a competitive edge for companies providing such integrated solutions.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand from Emerging Economies | +1.5% | Asia Pacific, Latin America, Africa | Mid to Long-term (2026-2033) |

| Investment in Smart City Infrastructure | +1.1% | North America, Europe, East Asia | Short to Mid-term (2025-2030) |

| Sustainable & Green Building Initiatives | +0.9% | Global | Short to Long-term (2025-2033) |

| Advancements in Prefabricated & Modular Construction | +0.8% | North America, Europe | Mid-term (2026-2031) |

Drain Waste Vent System Market Challenges Impact Analysis

The Drain Waste Vent system market encounters several inherent challenges that can affect its trajectory and operational efficiency. A primary concern is the complexity and variability of international and regional building codes and plumbing standards. Adherence to these diverse regulations requires significant R&D investment and can complicate market entry and product standardization for manufacturers operating across multiple geographies. The issue of illegal and substandard product proliferation, especially in less regulated markets, also poses a significant challenge, undermining fair competition and potentially leading to system failures and public health risks.

Moreover, the highly fragmented nature of the market, characterized by numerous small and medium-sized local players alongside large multinational corporations, creates intense price competition and can hinder technological innovation diffusion. The reluctance of traditional contractors and installers to adopt new, albeit more efficient, DWV technologies and materials also represents a barrier to market modernization. Finally, environmental concerns surrounding the disposal and recyclability of certain DWV materials, particularly plastics, are increasing, pushing manufacturers to invest in more sustainable, yet potentially more costly, solutions, which can impact profitability and market acceptance.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complex & Evolving Regulatory Landscape | -0.7% | Global | Short to Long-term (2025-2033) |

| Fragmented Market & Intense Competition | -0.5% | Asia Pacific, Latin America | Short to Mid-term (2025-2029) |

| Resistance to New Technologies & Materials | -0.4% | Developed & Developing Regions | Mid-term (2026-2031) |

| Environmental Disposal & Recyclability Concerns | -0.3% | Europe, North America | Mid to Long-term (2027-2033) |

Drain Waste Vent System Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Drain Waste Vent (DWV) System Market, encompassing its historical performance, current dynamics, and future projections. The scope includes a detailed examination of market size, growth drivers, restraints, opportunities, and challenges across various segments and key geographical regions. It delves into material types, application areas, and end-user industries, offering a holistic view of the market's evolving landscape and competitive environment, to empower strategic decision-making for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 24.5 Billion |

| Market Forecast in 2033 | USD 38.6 Billion |

| Growth Rate | 5.8% CAGR |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Advanced Drainage Systems, Inc., Uponor Corporation, Aliaxis SA, Georg Fischer AG, Polypipe Group plc, Charlotte Pipe and Foundry Company, JM Eagle, Inc., NIBCO Inc., Mueller Industries, Inc., McWane, Inc., Pipelife International GmbH, Wavin N.V., Zurn Industries, LLC, Viega GmbH & Co. KG, IPEX Inc., Durapipe UK, Rehau AG + Co, Formosa Plastics Corporation, Sekisui Chemical Co., Ltd., Sanwa Supply Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Drain Waste Vent (DWV) system market is comprehensively segmented to provide granular insights into its diverse components and applications. This segmentation analysis dissects the market based on material type, distinguishing between traditional materials like cast iron and copper and modern plastic alternatives such as PVC, ABS, and HDPE. Each material offers distinct advantages in terms of cost, durability, and ease of installation, catering to specific project requirements and regulatory environments. Understanding these material preferences is crucial for manufacturers to align their product portfolios with market demand and technological advancements.

Further segmentation by application categorizes the market into residential, commercial, industrial, and municipal sectors, highlighting the varying demands and scale of DWV systems required for each. For instance, residential applications often prioritize cost-effectiveness and ease of installation, while commercial and industrial projects focus on higher capacity, durability, and resistance to harsh environments. The end-use sector further differentiates between new construction and renovation/replacement projects, reflecting the ongoing cycles of building development and infrastructure upgrades across the globe. This layered segmentation allows for a precise evaluation of market trends, opportunities, and competitive landscapes within specific niches.

- By Material Type:

- PVC (Polyvinyl Chloride): Dominant for residential and light commercial use due to cost-effectiveness and ease of installation.

- ABS (Acrylonitrile Butadiene Styrene): Preferred in some regions for its impact resistance and suitability for colder temperatures.

- Cast Iron: Valued for its strength, sound-dampening properties, and fire resistance, primarily in commercial and high-rise buildings.

- Copper: Chosen for its durability and corrosion resistance, though less common now due to higher cost.

- HDPE (High-Density Polyethylene): Gaining traction for its flexibility, chemical resistance, and suitability for underground and commercial applications.

- Other Plastics (PEX, CPVC): Emerging for specific applications due to properties like flexibility and temperature resistance.

- By Application:

- Residential: Single-family homes, multi-family dwellings, apartments.

- Commercial: Offices, retail spaces, hospitality, healthcare facilities.

- Industrial: Manufacturing plants, processing facilities, warehouses.

- Municipal: Public utilities, wastewater treatment plants, storm drainage.

- By End-Use Sector:

- New Construction: Installation in newly built structures across all application types.

- Renovation & Replacement: Upgrading or replacing existing DWV systems in older buildings and infrastructure.

Regional Highlights

- North America: Characterized by mature infrastructure and a strong emphasis on renovation and replacement projects. Stringent building codes and a preference for durable, high-performance materials drive market demand. Significant adoption of smart plumbing technologies and prefabrication methods.

- Europe: Driven by strict environmental regulations and a focus on sustainable building practices. Germany, UK, and France are key markets, showing increasing demand for quiet DWV systems and eco-friendly piping solutions. Aging infrastructure also necessitates continuous upgrades.

- Asia Pacific (APAC): The fastest-growing region, fueled by rapid urbanization, massive infrastructure development, and a burgeoning construction industry in countries like China, India, and Southeast Asian nations. Cost-effectiveness and ease of installation are key considerations, leading to high adoption of plastic piping.

- Latin America: Experiencing steady growth due to increasing public and private investments in housing and commercial infrastructure. Brazil and Mexico are leading markets, with a focus on improving sanitation standards and adopting modern plumbing solutions.

- Middle East and Africa (MEA): Growth is primarily attributed to large-scale construction projects in the GCC countries and ongoing efforts to enhance sanitation facilities in African nations. Extreme climate conditions influence material choices, favoring durable and heat-resistant DWV systems.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Drain Waste Vent System Market.- Advanced Drainage Systems, Inc.

- Uponor Corporation

- Aliaxis SA

- Georg Fischer AG

- Polypipe Group plc

- Charlotte Pipe and Foundry Company

- JM Eagle, Inc.

- NIBCO Inc.

- Mueller Industries, Inc.

- McWane, Inc.

- Pipelife International GmbH

- Wavin N.V.

- Zurn Industries, LLC

- Viega GmbH & Co. KG

- IPEX Inc.

- Durapipe UK

- Rehau AG + Co

- Formosa Plastics Corporation

- Sekisui Chemical Co., Ltd.

- Sanwa Supply Inc.

Frequently Asked Questions

What are the primary materials used in Drain Waste Vent (DWV) systems?

The primary materials used in DWV systems include PVC, ABS, cast iron, copper, and HDPE. The choice of material depends on factors such as cost, application, local building codes, and desired durability and performance characteristics.

How do smart technologies impact the DWV system market?

Smart technologies, such as IoT sensors and AI-driven analytics, impact the DWV market by enabling predictive maintenance, real-time leak detection, and optimized system monitoring, leading to enhanced efficiency, reduced water damage, and extended system lifespan.

Which regions are expected to experience the highest growth in the DWV market?

The Asia Pacific region is anticipated to exhibit the highest growth in the DWV market, driven by rapid urbanization, significant infrastructure development, and increasing construction activities in countries like China and India.

What are the key drivers for the Drain Waste Vent System Market?

Key market drivers include global construction booms, increasing urbanization, rising awareness and stricter regulations concerning public health and sanitation, the need for aging infrastructure replacement, and ongoing advancements in piping materials.

What role does sustainability play in the evolution of DWV systems?

Sustainability is crucial, driving the demand for eco-friendly materials, recyclable components, and systems that promote water efficiency. Manufacturers are focusing on developing DWV solutions that minimize environmental impact and meet green building standards.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted