Dog Wet Food Market

Dog Wet Food Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705473 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

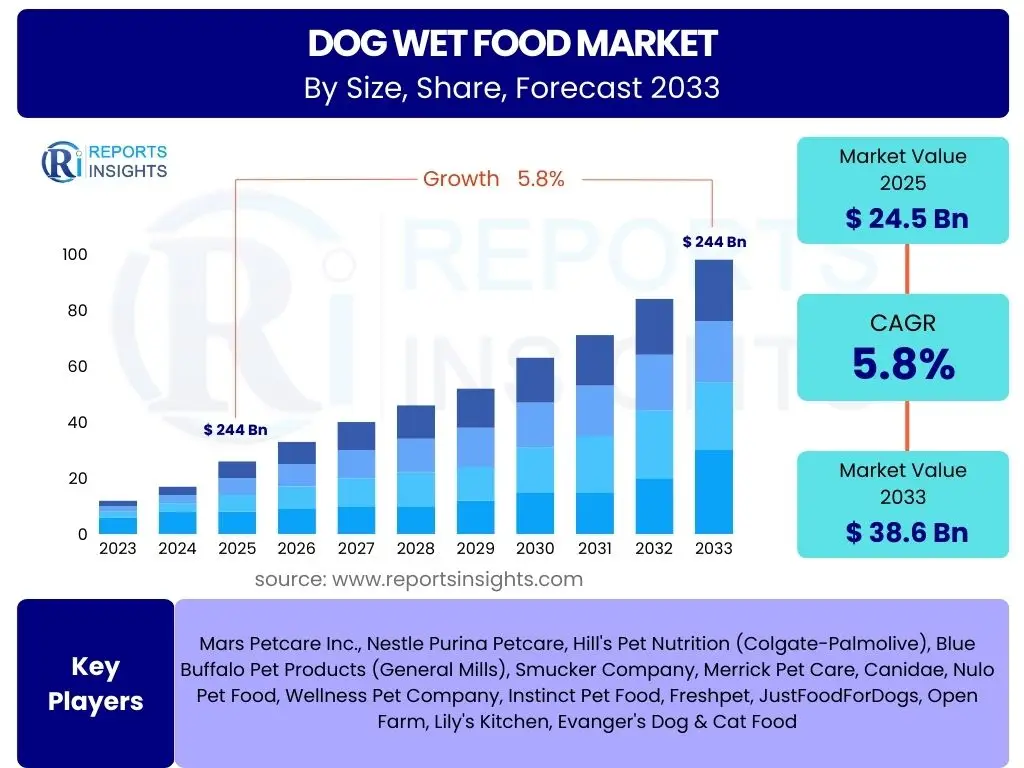

Dog Wet Food Market Size

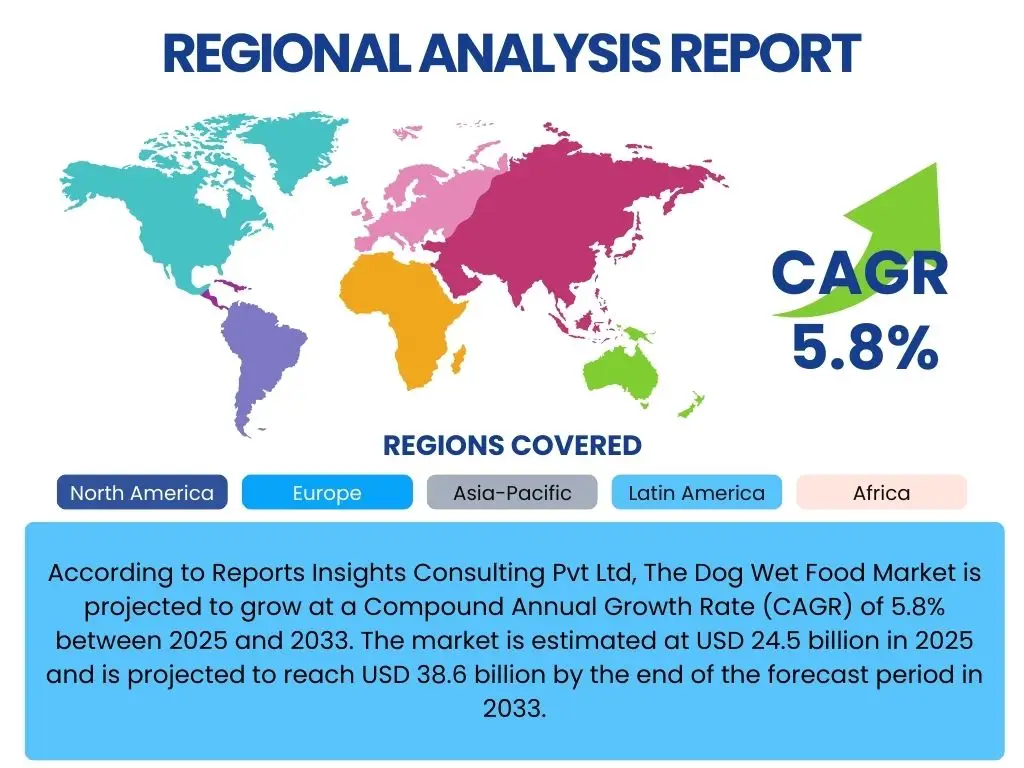

According to Reports Insights Consulting Pvt Ltd, The Dog Wet Food Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 24.5 billion in 2025 and is projected to reach USD 38.6 billion by the end of the forecast period in 2033.

Key Dog Wet Food Market Trends & Insights

The Dog Wet Food market is currently undergoing significant transformation driven by evolving pet owner preferences, technological advancements, and a heightened focus on pet health and wellness. Consumers are increasingly seeking premium, natural, and specialized wet food options that mirror human dietary trends, such as grain-free, organic, and limited ingredient diets. This humanization of pets is a pivotal trend, compelling manufacturers to innovate with high-quality protein sources, functional ingredients, and sustainable packaging. The shift towards e-commerce and direct-to-consumer models is also reshaping distribution strategies, offering convenience and broader product accessibility to a growing base of tech-savvy pet parents.

Moreover, there is a rising awareness among pet owners regarding the benefits of wet food, including its hydration properties, palatability, and suitability for various life stages and health conditions. This understanding is driving demand for specific formulations tailored for puppies, senior dogs, or those with sensitivities. The integration of advanced nutritional science and ingredient traceability is becoming more prominent, assuring consumers of product quality and safety. Furthermore, sustainable sourcing and environmentally friendly manufacturing processes are emerging as crucial considerations for both brands and consumers, influencing purchasing decisions and fostering a more ethical market landscape.

- Humanization of pets driving demand for premium, human-grade ingredients.

- Increased focus on functional ingredients for specific health benefits (e.g., joint health, digestion).

- Growth in e-commerce and direct-to-consumer (D2C) sales channels.

- Rising popularity of sustainable and ethically sourced product lines.

- Demand for limited ingredient and allergen-friendly formulations.

- Innovations in packaging for convenience and extended shelf life.

- Personalization of dog food based on breed, age, and activity level.

AI Impact Analysis on Dog Wet Food

Artificial intelligence (AI) is poised to revolutionize the Dog Wet Food market by enhancing various aspects from product development to supply chain management and consumer engagement. AI-driven analytics can process vast amounts of data on pet health, dietary needs, and consumer preferences, enabling manufacturers to formulate highly targeted and effective wet food products. This capability extends to predicting ingredient efficacy, optimizing nutrient profiles, and even simulating product palatability before physical production. Furthermore, AI can streamline manufacturing processes by optimizing production lines, reducing waste, and ensuring consistent quality control, leading to greater efficiency and cost savings for producers.

In the realm of supply chain and logistics, AI algorithms can predict demand fluctuations, optimize inventory levels, and enhance distribution routes, ensuring timely delivery of fresh products while minimizing spoilage. This is particularly crucial for wet food, which often has specific storage and transportation requirements. For consumer interaction, AI-powered chatbots and virtual assistants can provide personalized dietary recommendations, answer pet owner queries, and facilitate seamless purchasing experiences. Moreover, AI can analyze market trends in real-time, helping brands to quickly adapt to changing consumer behaviors and competitive landscapes, thus fostering innovation and maintaining market relevance. The integration of AI also supports advanced traceability systems, enhancing transparency from farm to bowl and building greater trust with consumers.

- AI-driven personalized nutrition recommendations for dogs.

- Optimized ingredient sourcing and supply chain management through predictive analytics.

- Enhanced quality control and safety monitoring in manufacturing.

- Automated demand forecasting and inventory management.

- Development of new product formulations based on data-driven insights.

- Improved customer service via AI-powered chatbots and virtual nutritionists.

- Real-time market trend analysis for agile product development.

Key Takeaways Dog Wet Food Market Size & Forecast

The Dog Wet Food market is on a robust growth trajectory, propelled by increasing pet ownership, the growing trend of pet humanization, and a heightened focus on pet health and wellness. The substantial projected CAGR of 5.8% underscores a strong and sustained demand for premium and specialized wet food products globally. Pet owners are increasingly willing to invest in high-quality nutrition for their companions, leading to a significant shift towards products offering specific health benefits, natural ingredients, and superior palatability. This growth is further amplified by the expanding accessibility of products through diverse retail channels, particularly e-commerce platforms.

The forecast from 2025 to 2033 highlights the long-term potential of this market, indicating that manufacturers and stakeholders will need to continuously innovate and adapt to evolving consumer expectations. Key growth drivers include rising disposable incomes in developing regions, increased awareness about the nutritional advantages of wet food, and ongoing product diversification. The market's resilience is also attributed to its ability to cater to various life stages, dietary needs, and health conditions of dogs, making wet food a versatile and essential component of pet diets. Sustained investment in research and development, alongside strategic marketing initiatives, will be crucial for companies to capitalize on this optimistic market outlook and secure a competitive edge.

- Market projected for substantial growth at a 5.8% CAGR from 2025 to 2033.

- Estimated market value to increase from USD 24.5 billion in 2025 to USD 38.6 billion by 2033.

- Humanization of pets is a primary growth catalyst.

- Strong demand for premium, natural, and functional wet food formulations.

- E-commerce channels are pivotal in driving market expansion and accessibility.

- Continued innovation in product development and packaging is anticipated.

Dog Wet Food Market Drivers Analysis

The Dog Wet Food market is primarily driven by the escalating trend of pet humanization, where pets are increasingly treated as family members, leading owners to prioritize their nutrition and well-being. This societal shift translates into a willingness to spend more on high-quality pet food, including premium wet formulations that offer superior taste, hydration, and tailored nutritional benefits. Consumers are actively seeking products with natural ingredients, transparent sourcing, and specific health claims, mirroring their own dietary preferences. This focus on premiumization fuels innovation and expands the market for specialized wet food products across various price points.

Another significant driver is the growing awareness among pet owners about the specific health advantages of wet food. Its high moisture content contributes to better hydration and urinary tract health, while its palatability makes it ideal for picky eaters or dogs with dental issues. The rising geriatric dog population, which often requires softer, more digestible food, further bolsters demand for wet food options. Additionally, the increasing disposable incomes in emerging economies, coupled with a rise in pet ownership, are creating new consumer bases eager to provide optimal nutrition for their pets, thus driving overall market expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Pet Humanization Trend | +1.5% | North America, Europe, Asia Pacific | Short to Long Term |

| Rising Awareness of Wet Food Benefits | +1.2% | Global | Medium to Long Term |

| Increasing Disposable Income & Pet Ownership | +1.0% | Asia Pacific, Latin America, Middle East | Medium to Long Term |

| Growth in Senior & Special Needs Dog Population | +0.8% | North America, Europe | Medium Term |

| E-commerce Expansion & Accessibility | +0.7% | Global | Short to Medium Term |

Dog Wet Food Market Restraints Analysis

Despite robust growth, the Dog Wet Food market faces several restraints, most notably the higher cost associated with wet food compared to dry kibble. The premium pricing often deters price-sensitive consumers, particularly in developing regions or during economic downturns, leading them to opt for more economical dry food alternatives. This cost differential is driven by factors such as higher ingredient expenses, more complex manufacturing processes, and the cost of specialized packaging required to maintain freshness and prevent spoilage. The bulk and weight of wet food also contribute to higher transportation and storage costs, which are often passed on to consumers, further impacting affordability.

Another significant restraint is the relatively shorter shelf life of wet food once opened, requiring refrigeration and prompt consumption, which can be inconvenient for some pet owners. This often leads to concerns about food waste if large cans are not consumed quickly. Furthermore, the higher packaging volume of wet food compared to its nutritional density means it takes up more storage space for consumers and retailers, and presents environmental challenges related to waste disposal. Regulatory complexities and varying food safety standards across different regions can also pose a barrier to market entry and expansion for manufacturers, increasing compliance costs and limiting global reach.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Higher Cost Compared to Dry Food | -1.0% | Global, particularly emerging economies | Short to Long Term |

| Shorter Shelf Life After Opening | -0.7% | Global | Short Term |

| Perceived Inconvenience (Storage, Travel) | -0.6% | North America, Europe | Short to Medium Term |

| Environmental Concerns (Packaging Waste) | -0.5% | Europe, North America | Medium to Long Term |

| Supply Chain & Storage Logistical Challenges | -0.4% | Global | Short Term |

Dog Wet Food Market Opportunities Analysis

The Dog Wet Food market presents significant opportunities for innovation and expansion, particularly through the development of specialized and functional food formulations. As pet owners become more educated about canine nutrition, there is a growing demand for wet food designed to address specific health concerns such as digestive sensitivities, weight management, joint health, and allergies. This niche market allows for premium pricing and fosters brand loyalty among owners seeking tailored solutions for their pets. Furthermore, the incorporation of novel ingredients like alternative proteins (insect-based, plant-based) and superfoods offers avenues for differentiation and caters to evolving consumer preferences for sustainable and ethically sourced products.

Expansion into emerging markets, particularly in Asia Pacific and Latin America, represents a substantial growth opportunity. These regions are experiencing rapid urbanization, rising disposable incomes, and an increasing trend of pet ownership, creating a burgeoning consumer base for pet food. Manufacturers can capitalize on this by adapting product offerings to local tastes and dietary customs, as well as establishing strong distribution networks. The continued growth of e-commerce platforms and direct-to-consumer models also provides an opportunity to reach a wider audience, reduce logistical overheads, and build direct relationships with customers, offering personalized recommendations and subscription services to enhance convenience and retention.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Functional & Therapeutic Formulations | +1.3% | Global | Medium to Long Term |

| Expansion in Emerging Markets | +1.1% | Asia Pacific, Latin America, MEA | Medium to Long Term |

| Growth of E-commerce & Subscription Models | +0.9% | Global | Short to Medium Term |

| Sustainable & Ethical Product Innovation | +0.8% | Europe, North America | Medium Term |

| Personalized & Customized Diet Solutions | +0.7% | North America, Europe | Long Term |

Dog Wet Food Market Challenges Impact Analysis

The Dog Wet Food market faces significant challenges related to intense competition and market fragmentation. The presence of numerous established global players alongside a proliferation of smaller, specialized brands creates a highly competitive landscape. This necessitates continuous innovation in product development, marketing, and pricing strategies to maintain market share and attract new customers. Brands must constantly differentiate their offerings and communicate unique value propositions to stand out in a crowded market, which often requires substantial investment in R&D and promotional activities, squeezing profit margins for some participants.

Consumer skepticism regarding ingredient transparency and product claims poses another notable challenge. As pet owners become more discerning, they demand clear and verifiable information about ingredient sourcing, manufacturing processes, and nutritional content. This requires robust traceability systems and transparent communication, which can be complex and costly for manufacturers to implement and maintain. Furthermore, fluctuating raw material prices, particularly for high-quality protein sources, can impact production costs and retail pricing, creating instability for both manufacturers and consumers. Navigating diverse and evolving regulatory landscapes across different countries also presents a significant hurdle, adding to compliance costs and potentially limiting market access for certain products.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Competition & Market Fragmentation | -0.9% | Global | Short to Long Term |

| Raw Material Price Volatility | -0.8% | Global | Short Term |

| Consumer Skepticism & Demand for Transparency | -0.7% | North America, Europe | Medium Term |

| Stringent Regulatory Compliance | -0.6% | Europe, North America | Medium Term |

| Perceived Lack of Convenience vs. Dry Food | -0.5% | Global | Short Term |

Dog Wet Food Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Dog Wet Food market, covering market size estimations, historical trends, and future growth projections up to 2033. It examines key market drivers, restraints, opportunities, and challenges influencing the industry's trajectory. The report offers detailed segmentation analysis by product type, ingredient, distribution channel, and life stage, providing a granular view of market dynamics. Furthermore, it highlights regional market performance, identifying growth hotspots and key contributing countries, alongside profiles of leading market participants and their strategic initiatives, offering valuable insights for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 24.5 Billion |

| Market Forecast in 2033 | USD 38.6 Billion |

| Growth Rate | 5.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Mars Petcare Inc., Nestle Purina Petcare, Hill's Pet Nutrition (Colgate-Palmolive), Blue Buffalo Pet Products (General Mills), Smucker Company, Merrick Pet Care, Canidae, Nulo Pet Food, Wellness Pet Company, Instinct Pet Food, Freshpet, JustFoodForDogs, Open Farm, Lily's Kitchen, Evanger's Dog & Cat Food |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Dog Wet Food market is extensively segmented to provide a detailed understanding of its diverse components and consumer preferences. This segmentation includes analysis by product type, which distinguishes between gravy, pate, jelly, and stew formulations, each catering to different palatability preferences and textures. Ingredient-based segmentation further breaks down the market into meat-based (e.g., chicken, beef, lamb) and plant-based options, reflecting the growing demand for diverse protein sources and dietary choices. The market is also analyzed by distribution channel, identifying the dominant routes through which products reach consumers, such as specialty pet stores, supermarkets, online retail, and veterinary clinics, each with unique operational dynamics and consumer reach.

Furthermore, the segmentation by life stage (puppy, adult, senior) addresses the specific nutritional requirements of dogs at different phases of their lives, allowing manufacturers to tailor products for optimal health and development. Packaging type, including cans, pouches, and trays, is also a crucial segment, influencing consumer convenience, product freshness, and environmental impact considerations. This comprehensive segmentation helps stakeholders identify specific growth opportunities within niche categories and develop targeted strategies to effectively penetrate various market segments, catering to the evolving needs and preferences of a diverse pet owner base.

- By Product Type: Gravy, Pate, Jelly, Stew, Others, each offering distinct textures and palatability.

- By Ingredient: Meat-based (Chicken, Beef, Lamb, Fish, Turkey, Pork, Others), Plant-based, and Grain-free options, reflecting diverse dietary needs and preferences.

- By Distribution Channel: Specialty Pet Stores, Supermarkets/Hypermarkets, Online Retail, Veterinary Clinics, Others, showcasing varied consumer purchasing habits.

- By Life Stage: Puppy, Adult, Senior, addressing specific nutritional requirements at different canine life phases.

- By Packaging Type: Cans, Pouches, Trays, influencing convenience, shelf life, and environmental considerations.

Regional Highlights

- North America: Dominates the Dog Wet Food market, driven by high pet ownership rates, significant disposable incomes, and the strong humanization trend. Consumers in this region increasingly demand premium, natural, and functional wet food options, leading to robust market growth and innovation. The widespread adoption of e-commerce channels further bolsters market penetration.

- Europe: A mature market characterized by a growing focus on organic, sustainable, and ethically sourced pet food. Countries like Germany, the UK, and France are key contributors, driven by stringent pet welfare standards and a high willingness among owners to invest in high-quality nutrition. The market also benefits from a strong veterinary channel for specialized diets.

- Asia Pacific (APAC): Emerging as the fastest-growing region due to rapidly increasing pet ownership, urbanization, and rising disposable incomes, particularly in countries like China, India, and Japan. Westernization of pet care practices and a growing awareness of pet health are fueling demand for premium and convenient wet food formats.

- Latin America: Experiencing steady growth in the Dog Wet Food market, primarily driven by increasing pet adoption rates and a rising middle class. Brazil and Mexico are key markets, with a growing preference for processed and packaged pet food over traditional homemade diets.

- Middle East & Africa (MEA): A nascent but growing market, influenced by changing lifestyles, increasing disposable incomes, and the gradual acceptance of pets as companions. While smaller in scale, the region presents future growth opportunities as pet care practices evolve and organized retail channels expand.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Dog Wet Food Market.- Mars Petcare Inc.

- Nestle Purina Petcare

- Hill's Pet Nutrition (Colgate-Palmolive)

- Blue Buffalo Pet Products (General Mills)

- Smucker Company

- Merrick Pet Care

- Canidae

- Nulo Pet Food

- Wellness Pet Company

- Instinct Pet Food

- Freshpet

- JustFoodForDogs

- Open Farm

- Lily's Kitchen

- Evanger's Dog & Cat Food

- Royal Canin (Mars Petcare)

- Nutro (Mars Petcare)

- Iams (Mars Petcare)

- Cesar (Mars Petcare)

- Pedigree (Mars Petcare)

Frequently Asked Questions

What is the projected growth rate of the Dog Wet Food market?

The Dog Wet Food market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033, indicating robust expansion.

What are the primary drivers of the Dog Wet Food market?

Key drivers include the pet humanization trend, increasing awareness of wet food's health benefits (e.g., hydration, palatability), rising disposable incomes, and the growth in senior and special needs dog populations.

Which regions are leading the Dog Wet Food market?

North America currently dominates the market, while Asia Pacific is projected to be the fastest-growing region due to increasing pet ownership and rising incomes.

How is artificial intelligence impacting the Dog Wet Food industry?

AI is transforming the industry by enabling personalized nutrition, optimizing supply chains, enhancing quality control, automating demand forecasting, and improving customer service through data-driven insights.

What are the main segments analyzed in the Dog Wet Food market report?

The report segments the market by product type (gravy, pate), ingredient (meat-based, plant-based), distribution channel (online, specialty stores), life stage (puppy, adult, senior), and packaging type (cans, pouches).

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted