DNA Paternity Testing Market

DNA Paternity Testing Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709763 | Last Updated : December 17, 2025 |

Format : ![]()

![]()

![]()

![]()

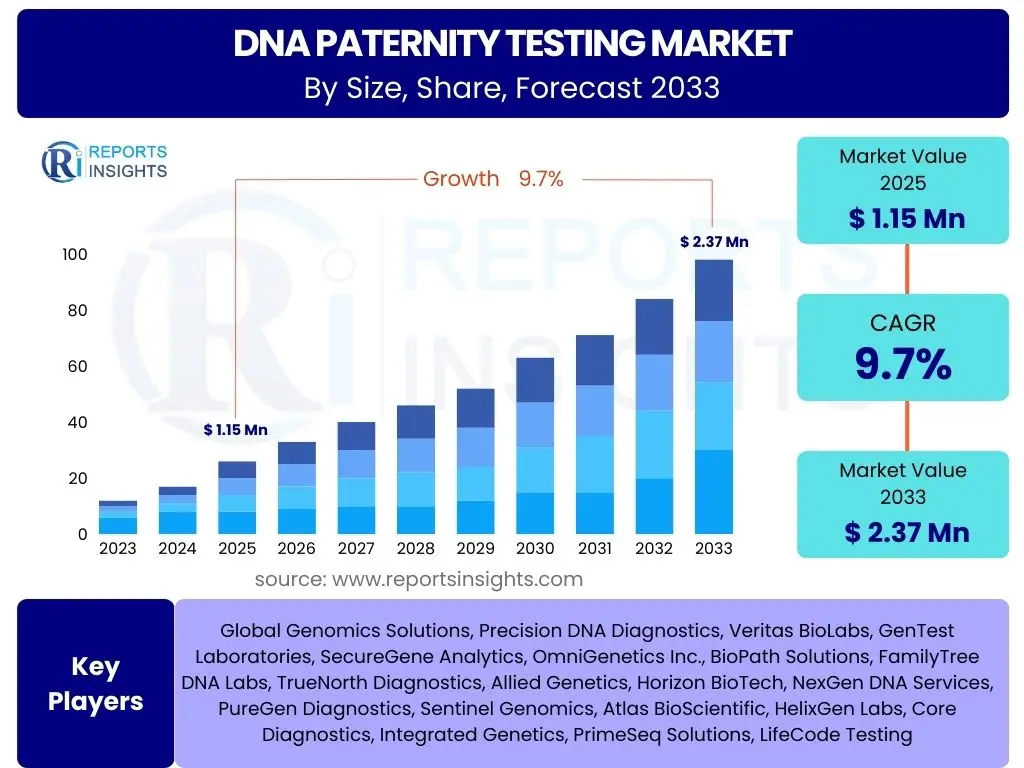

DNA Paternity Testing Market Size

According to Reports Insights Consulting Pvt Ltd, The DNA Paternity Testing Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.7% between 2025 and 2033. The market is estimated at USD 1.15 Billion in 2025 and is projected to reach USD 2.37 Billion by the end of the forecast period in 2033.

Key DNA Paternity Testing Market Trends & Insights

The DNA Paternity Testing market is experiencing dynamic shifts driven by technological advancements, evolving legal frameworks, and increasing public awareness. Users frequently inquire about the latest innovations making tests more accessible and accurate, as well as the societal and ethical implications of widespread testing. The trend towards non-invasive prenatal paternity testing (NIPPT) is a significant point of interest, alongside the growing demand for direct-to-consumer (DTC) services. Additionally, there is a clear interest in understanding how global regulatory landscapes are adapting to these new testing methodologies and the associated data privacy concerns.

Key insights reveal a market moving towards greater convenience and precision, with a notable shift from traditional methods to advanced molecular diagnostics. The expansion into emerging economies also presents substantial growth opportunities, as diagnostic infrastructure improves and disposable incomes rise. Furthermore, the integration of genetic counseling services alongside testing results is becoming more prevalent, addressing the emotional and psychological aspects for individuals and families involved in paternity disputes or confirmations.

- Increased adoption of Non-Invasive Prenatal Paternity Testing (NIPPT) due to safety and accuracy benefits.

- Growing popularity of direct-to-consumer (DTC) DNA testing kits offering convenience and privacy.

- Technological advancements in sequencing and bioinformatics improving test accuracy and reducing turnaround times.

- Rising demand for legal and immigration-related paternity testing globally.

- Expansion of services into emerging markets with developing healthcare infrastructure.

- Greater emphasis on data privacy and ethical considerations in genetic information management.

AI Impact Analysis on DNA Paternity Testing

Common user questions regarding AI's impact on DNA Paternity Testing often revolve around its potential to enhance accuracy, speed, and cost-effectiveness. Users are keen to understand how artificial intelligence and machine learning algorithms can refine genetic data analysis, identify complex genetic markers more efficiently, and minimize human error in laboratory settings. There is also significant curiosity about AI's role in processing vast amounts of genomic data, making it more interpretable for diagnostic purposes, and potentially predicting outcomes or identifying anomalies more rapidly than conventional methods.

Concerns, however, frequently emerge concerning data security, algorithmic bias, and the ethical implications of AI-driven decisions in sensitive areas like paternity. Users want to know if AI could introduce new forms of error, how their genetic privacy would be maintained, and the extent to which human oversight would remain critical. Expectations are high for AI to revolutionize the field, particularly in streamlining workflows and reducing the analytical burden on human experts, while simultaneously upholding the highest standards of accuracy and ethical conduct. The ability of AI to learn from diverse datasets also promises to improve the reliability of tests across various ethnic backgrounds, addressing a long-standing challenge in genetic diagnostics.

- Enhanced data analysis for complex genetic markers, leading to improved accuracy and reduced false positives/negatives.

- Automation of laboratory processes and data interpretation, significantly accelerating turnaround times for results.

- Cost reduction through optimized resource utilization and minimized manual labor in genetic sequencing and analysis.

- Improved predictive modeling for genetic relationships and identification of rare genetic mutations affecting paternity.

- Development of AI-powered diagnostic tools assisting in interpreting intricate genetic patterns and variations.

- Challenges in ensuring data privacy and preventing algorithmic bias, necessitating robust ethical guidelines and regulatory oversight.

Key Takeaways DNA Paternity Testing Market Size & Forecast

Users frequently inquire about the overarching conclusions from market size and forecast reports, particularly seeking insights into growth drivers, regional performance, and future opportunities. The central takeaway from the DNA Paternity Testing market analysis is a robust and sustained growth trajectory, primarily fueled by technological innovation and increasing global accessibility. The market is poised for significant expansion, driven by advancements in non-invasive techniques and the broadening scope of applications beyond traditional legal cases to include personal curiosity and immigration requirements.

Forecasts indicate a continued shift towards more user-friendly and accurate testing methods, with a notable increase in demand across developing regions. While ethical and regulatory challenges remain, the market's fundamental drivers, such as the increasing global population, greater awareness of genetic testing, and improving healthcare infrastructure, are expected to propel it towards substantial valuation by 2033. Investors and stakeholders should recognize the increasing importance of digital platforms and direct-to-consumer models as key channels for market penetration and growth.

- The DNA Paternity Testing market is projected for substantial growth, nearly doubling its valuation by 2033, underscoring strong underlying demand.

- Non-Invasive Prenatal Paternity Testing (NIPPT) is a critical growth segment, reflecting a preference for safer and earlier testing options.

- Technological innovation, particularly in genomic sequencing and bioinformatics, remains a primary catalyst for market expansion and improved test reliability.

- North America and Europe currently dominate the market, but Asia Pacific is emerging as a high-growth region due to increasing awareness and healthcare investments.

- Addressing ethical concerns, data privacy, and establishing clear regulatory frameworks are crucial for sustainable market development and public trust.

DNA Paternity Testing Market Drivers Analysis

The DNA Paternity Testing market is primarily propelled by several key factors that contribute to its consistent growth. Increased public awareness regarding the accuracy and reliability of DNA testing has significantly boosted demand, moving it from a niche service to a more widely accepted diagnostic tool. Technological advancements, especially in non-invasive methods and rapid sequencing, have made testing safer, faster, and more accessible, further broadening its appeal to a wider demographic. The global rise in legal disputes, immigration requirements, and forensic investigations requiring definitive proof of biological relationships also acts as a substantial market driver, ensuring a steady stream of demand from institutional clients.

Moreover, the expansion of direct-to-consumer (DTC) genetic testing services has democratized access to paternity tests, catering to personal curiosity and family relationship verification without the need for extensive medical or legal intervention. This shift empowers individuals to obtain information discreetly and conveniently. Improving healthcare infrastructure in emerging economies, coupled with a growing middle class and increasing disposable incomes, further fuels market expansion by making these services more attainable across various regions. These combined forces create a robust demand environment for DNA paternity testing services globally.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increased Awareness and Acceptance of DNA Testing | +1.2% | Global, particularly North America, Europe | Mid-term (3-5 years) |

| Technological Advancements in Non-Invasive Methods | +1.5% | Global, especially developed economies | Short-term (1-3 years) |

| Growing Demand for Legal and Immigration Purposes | +0.9% | North America, Europe, Asia Pacific | Long-term (5-8 years) |

| Expansion of Direct-to-Consumer (DTC) Services | +0.8% | Global, with strong presence in US, UK, Canada | Mid-term (3-5 years) |

DNA Paternity Testing Market Restraints Analysis

Despite its robust growth, the DNA Paternity Testing market faces several significant restraints that could impede its full potential. High costs associated with advanced genetic testing methodologies, particularly for non-invasive prenatal tests, often act as a barrier to wider adoption, especially in regions with limited healthcare budgets or low insurance coverage. Ethical concerns and privacy issues surrounding genetic data collection, storage, and usage represent a substantial challenge. Public apprehension about the misuse of sensitive genetic information can lead to hesitation in undergoing tests, impacting market volume.

Furthermore, stringent regulatory frameworks and varying legal requirements across different countries can create complexities for service providers, affecting market entry and operational scalability. The need for accreditation, specific consent protocols, and data protection laws adds layers of compliance that can be costly and time-consuming. Additionally, the emotional and psychological impact of paternity test results on individuals and families, combined with potential societal stigma, may deter some individuals from seeking these services. These factors collectively present challenges that stakeholders must navigate to ensure sustained market expansion.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of Advanced DNA Paternity Tests | -0.8% | Global, particularly emerging economies | Long-term (5-8 years) |

| Ethical Concerns and Data Privacy Issues | -1.0% | Global, especially EU, US | Mid-term (3-5 years) |

| Stringent Regulatory Landscape and Varied Legal Requirements | -0.7% | Global, country-specific impact | Short-term (1-3 years) |

| Lack of Public Awareness or Misinformation | -0.5% | Developing regions, rural areas | Mid-term (3-5 years) |

DNA Paternity Testing Market Opportunities Analysis

Significant opportunities exist within the DNA Paternity Testing market, poised to drive further innovation and expansion. The continuous development of more advanced and affordable sequencing technologies presents a chance to reduce test costs, making them accessible to a broader consumer base and stimulating demand. Expanding applications beyond traditional legal and personal verification, such as in forensic science for identifying victims or perpetrators, or in medical genetics for complex inherited conditions, offers new avenues for market growth. The increasing focus on personalized medicine and genetic health also subtly contributes to a greater societal acceptance and understanding of genetic information, which benefits the paternity testing sector.

Moreover, the untapped potential in emerging economies, characterized by improving healthcare infrastructure, increasing disposable incomes, and a growing understanding of genetic science, represents a substantial market expansion opportunity. Providers can leverage digital platforms and telemedicine solutions to reach remote populations and offer services more efficiently. Strategic partnerships between diagnostic laboratories, healthcare providers, and technology companies can facilitate the development of integrated solutions, enhance service delivery, and capitalize on these evolving market dynamics. Customization of services for specific cultural or regional needs can also unlock new segments.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of More Affordable and Rapid Technologies | +1.8% | Global | Mid-term (3-5 years) |

| Expansion into Emerging Economies | +1.5% | Asia Pacific, Latin America, MEA | Long-term (5-8 years) |

| Integration with Telemedicine and Digital Health Platforms | +1.0% | Global, particularly post-pandemic | Short-term (1-3 years) |

| Untapped Market for Non-Legal/Personal Verification Tests | +0.7% | Global, especially urban areas | Mid-term (3-5 years) |

DNA Paternity Testing Market Challenges Impact Analysis

The DNA Paternity Testing market faces a distinct set of challenges that require strategic navigation for continued growth. Maintaining data security and ensuring the privacy of highly sensitive genetic information is a paramount concern, with increasing cyber threats and evolving global data protection regulations posing constant hurdles. Public trust can be significantly eroded by data breaches or perceived misuse of genetic data, directly impacting market adoption. Another major challenge involves the ethical dilemmas associated with genetic testing, particularly regarding consent, implications for family members, and the potential for discrimination.

Moreover, the market contends with intense competition from numerous established and emerging players, leading to pricing pressures and the need for continuous innovation to differentiate services. The complexity of interpreting genetic data, particularly in non-standard cases or with limited reference populations, demands highly skilled personnel and advanced bioinformatics infrastructure, representing a significant operational challenge. Additionally, ensuring consistent quality and accuracy across all testing facilities and methodologies worldwide remains a critical task, especially with the proliferation of direct-to-consumer options that may not always adhere to the same rigorous standards as accredited laboratories. Addressing these challenges is vital for market stability and consumer confidence.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Ensuring Data Privacy and Cybersecurity | -1.2% | Global, especially highly regulated regions | Long-term (5-8 years) |

| Ethical and Societal Implications of Genetic Testing | -0.9% | Global | Mid-term (3-5 years) |

| High Competition and Pricing Pressures | -0.7% | Developed markets, urban centers | Short-term (1-3 years) |

| Maintaining Quality and Accreditation Standards | -0.6% | Global, particularly emerging markets | Mid-term (3-5 years) |

DNA Paternity Testing Market - Updated Report Scope

This report provides an in-depth analysis of the global DNA Paternity Testing market, encompassing a comprehensive study of market size, trends, drivers, restraints, opportunities, and challenges across various segments and key geographical regions. It offers a strategic outlook on the market's trajectory from 2025 to 2033, highlighting the impact of technological advancements, regulatory changes, and evolving consumer preferences. The scope includes detailed segmentation by test type, application, and end-user, alongside a competitive landscape analysis of major market participants to provide actionable insights for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.15 Billion |

| Market Forecast in 2033 | USD 2.37 Billion |

| Growth Rate | 9.7% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Genomics Solutions, Precision DNA Diagnostics, Veritas BioLabs, GenTest Laboratories, SecureGene Analytics, OmniGenetics Inc., BioPath Solutions, FamilyTree DNA Labs, TrueNorth Diagnostics, Allied Genetics, Horizon BioTech, NexGen DNA Services, PureGen Diagnostics, Sentinel Genomics, Atlas BioScientific, HelixGen Labs, Core Diagnostics, Integrated Genetics, PrimeSeq Solutions, LifeCode Testing |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The DNA Paternity Testing market is comprehensively segmented to provide a granular view of its diverse landscape and cater to varying user needs and applications. This segmentation allows for a deeper understanding of market dynamics, identifying specific growth areas and competitive advantages within each category. The primary segments include analyses by test type, distinguishing between postnatal and prenatal methodologies, and further breaking down prenatal options into non-invasive and invasive techniques. Each test type presents unique benefits and challenges, influencing their adoption rates across different scenarios.

Further segmentation by application highlights the distinct purposes for which DNA paternity tests are conducted, ranging from legally mandated procedures for court cases and immigration to private or "peace of mind" tests for personal verification. Additionally, the market is segmented by end-user, identifying the key entities consuming these services, such as diagnostic laboratories, hospitals, government agencies, and the burgeoning direct-to-consumer channel. This multi-faceted approach ensures a holistic market assessment, revealing intricate patterns of demand and supply within the industry.

- By Test Type:

- Postnatal Paternity Testing (Blood Sample, Buccal Swab)

- Prenatal Paternity Testing (Non-Invasive Prenatal Paternity Test (NIPPT), Invasive Prenatal Paternity Test (Amniocentesis, Chorionic Villus Sampling (CVS)))

- By Application:

- Legal Testing (Court-ordered, Immigration)

- Private/Peace of Mind Testing (Personal Verification)

- Forensic Testing

- By End-User:

- Diagnostic Laboratories

- Hospitals & Clinics

- Government Agencies

- Direct-to-Consumer (DTC) Channels

Regional Highlights

Regional analysis of the DNA Paternity Testing market reveals distinct patterns of growth, adoption, and regulatory landscapes across various geographies. North America currently holds the largest market share, driven by high awareness, advanced healthcare infrastructure, significant R&D investments, and a robust legal framework supporting paternity testing for various purposes. The United States, in particular, leads in the adoption of cutting-edge technologies like NIPPT and has a mature direct-to-consumer market. Consumers in this region also exhibit a higher propensity for discretionary spending on health-related and personal verification services, further bolstering market growth.

Europe follows closely, characterized by stringent regulatory standards, high diagnostic testing volumes, and increasing public acceptance of genetic testing. Countries like Germany, the UK, and France are key contributors, with well-established diagnostic laboratory networks and increasing demand for both legal and private paternity tests. The Asia Pacific region is projected to exhibit the highest growth rate during the forecast period. This surge is attributed to improving healthcare infrastructure, rising disposable incomes, increasing awareness of genetic testing benefits, and a large population base in countries such as China and India, which are rapidly expanding their diagnostic capabilities. Latin America, the Middle East, and Africa also present nascent but growing markets, driven by improving access to healthcare services and increasing urbanization.

- North America: Dominant market share due to advanced healthcare infrastructure, high awareness, and significant adoption of NIPPT and DTC services, particularly in the United States and Canada.

- Europe: Strong market presence with stringent regulatory frameworks and high demand from countries like Germany, the UK, and France for both legal and personal paternity testing.

- Asia Pacific (APAC): Fastest-growing region, propelled by improving healthcare access, rising disposable incomes, and increasing awareness in densely populated countries such as China and India.

- Latin America: Emerging market with increasing investments in healthcare infrastructure and growing awareness of genetic testing, notably in Brazil and Mexico.

- Middle East and Africa (MEA): Gradually expanding market, driven by improvements in healthcare facilities and increasing demand for diagnostic services in countries like Saudi Arabia and South Africa.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the DNA Paternity Testing Market.- Global Genomics Solutions

- Precision DNA Diagnostics

- Veritas BioLabs

- GenTest Laboratories

- SecureGene Analytics

- OmniGenetics Inc.

- BioPath Solutions

- FamilyTree DNA Labs

- TrueNorth Diagnostics

- Allied Genetics

- Horizon BioTech

- NexGen DNA Services

- PureGen Diagnostics

- Sentinel Genomics

- Atlas BioScientific

- HelixGen Labs

- Core Diagnostics

- Integrated Genetics

- PrimeSeq Solutions

- LifeCode Testing

Frequently Asked Questions

Analyze common user questions about the DNA Paternity Testing market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is DNA Paternity Testing?

DNA Paternity Testing is a scientific method used to determine if a man is the biological father of a child. It compares the DNA profiles of the potential father, mother (optional), and child to identify genetic markers that are passed down from parent to child, providing a highly accurate determination of biological parentage.

How accurate are DNA Paternity Tests?

DNA Paternity Tests are highly accurate, typically reporting an accuracy of 99.9% or higher for inclusion (confirming paternity) and 100% for exclusion (ruling out paternity). This high degree of accuracy makes them widely accepted in legal, medical, and personal contexts, relying on established genetic science and rigorous laboratory protocols.

What are the different types of DNA Paternity Tests available?

The main types include Postnatal Paternity Testing, which uses buccal (cheek) swabs or blood samples after birth, and Prenatal Paternity Testing. Prenatal options include non-invasive prenatal paternity testing (NIPPT) using maternal blood, and invasive methods like amniocentesis or chorionic villus sampling (CVS) performed during pregnancy, with NIPPT being increasingly preferred due to its safety.

How long does it take to get DNA Paternity Test results?

The turnaround time for DNA Paternity Test results typically ranges from 3 to 7 business days, depending on the testing facility and the type of test performed. Some providers offer expedited services for an additional fee, which can deliver results in as little as 1 to 2 business days, catering to urgent needs for legal or personal matters.

Can DNA Paternity Tests be used for legal purposes?

Yes, DNA Paternity Tests are widely accepted for legal purposes, including child support, custody disputes, inheritance claims, and immigration. For a test to be legally admissible, it must be performed by an accredited laboratory following a strict chain-of-custody protocol, ensuring proper identification and collection of samples by a neutral third party.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted