District Heating and Cooling Market

District Heating and Cooling Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_678310 | Last Updated : July 21, 2025 |

Format : ![]()

![]()

![]()

![]()

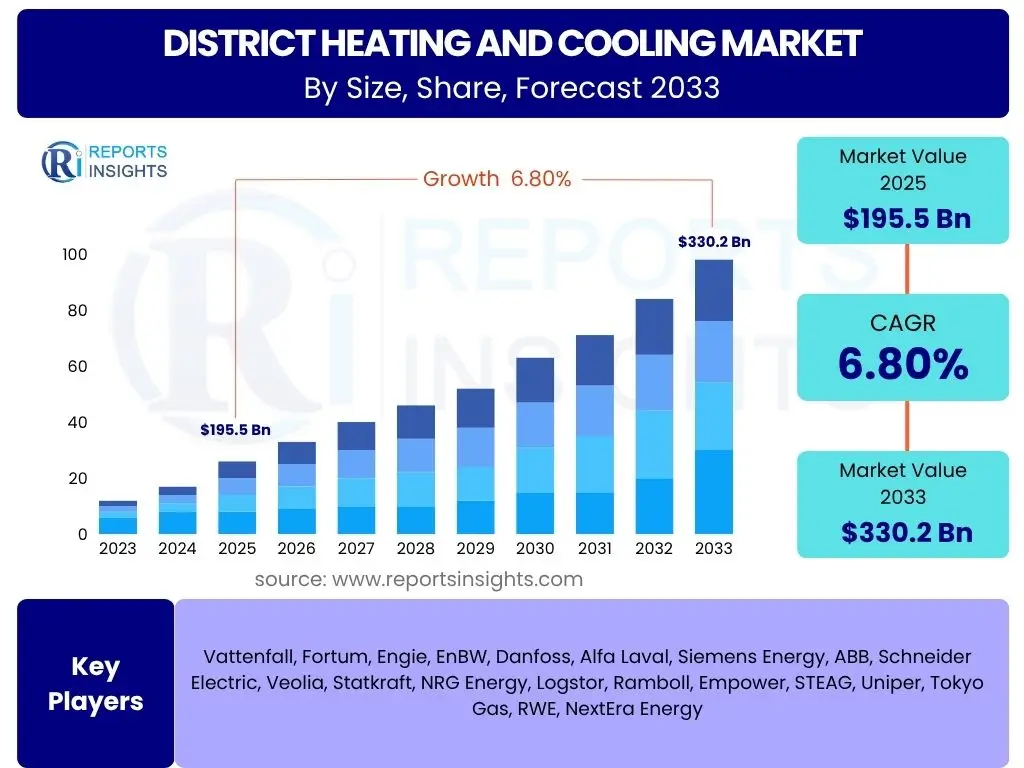

District Heating and Cooling Market is projected to grow at a Compound annual growth rate (CAGR) of 7.8% between 2025 and 2033, valued at USD 265 Billion in 2025 and is projected to grow to USD 485 Billion by 2033, the end of the forecast period.

Key District Heating and Cooling Market Trends & Insights

The District Heating and Cooling (DHC) market is currently undergoing a transformative phase, driven by a global imperative for sustainable energy solutions and enhanced urban infrastructure. Key trends reflect a strong shift towards decarbonization and efficiency, with policy frameworks increasingly favoring centralized energy systems that can integrate diverse heat and cool sources. Innovations in network design and material science are also playing a crucial role in expanding the reach and reliability of DHC systems, making them more attractive for both new developments and retrofitting existing urban areas.

- Increasing focus on energy efficiency and reduction of carbon emissions.

- Growing adoption of renewable and waste heat sources for DHC networks.

- Urbanization and the development of smart cities driving demand for integrated energy solutions.

- Technological advancements in heat pump technology and thermal storage solutions.

- Supportive government policies and financial incentives promoting DHC infrastructure.

- Digitalization and smart network management for optimized energy distribution.

AI Impact Analysis on District Heating and Cooling

Artificial Intelligence (AI) is set to revolutionize the District Heating and Cooling market by introducing unprecedented levels of optimization, efficiency, and resilience. AI-powered algorithms can analyze vast datasets from sensors, weather forecasts, and building occupancy patterns to predict energy demand with remarkable accuracy, allowing DHC operators to fine-tune production and distribution in real time. This capability leads to significant energy savings, reduced operational costs, and a smaller environmental footprint, moving DHC systems from reactive to predictive management.

- Predictive maintenance for DHC infrastructure, minimizing downtime and operational costs.

- Optimized energy distribution and demand forecasting, leading to enhanced efficiency.

- Intelligent control systems for smart grid integration and demand-side management.

- Data-driven decision-making for network expansion and investment planning.

- Enhanced cybersecurity measures for critical DHC infrastructure.

- Real-time performance monitoring and anomaly detection for proactive problem-solving.

Key Takeaways District Heating and Cooling Market Size & Forecast

- The District Heating and Cooling market exhibits robust growth, driven by global sustainability agendas.

- Significant market expansion is projected, reaching nearly double its current valuation by 2033.

- Investment in modernizing and expanding DHC networks is a primary growth catalyst.

- Europe and Asia Pacific are expected to remain leading markets due to strong regulatory support and rapid urbanization.

- Technological advancements and integration of diverse energy sources are crucial for future market trajectory.

- The market provides substantial opportunities for technology providers, infrastructure developers, and energy service companies.

- Demand for efficient and reliable heating and cooling solutions in commercial and residential sectors fuels market progression.

District Heating and Cooling Market Drivers Impact Analysis

The District Heating and Cooling market's growth is fundamentally propelled by a confluence of macroeconomic and technological factors. Government initiatives promoting energy efficiency and decarbonization, coupled with increasing urbanization and the imperative to upgrade aging energy infrastructure, form the cornerstone of this expansion. Furthermore, the rising integration of renewable energy sources and waste heat recovery systems into DHC networks significantly enhances their environmental and economic viability, attracting further investment and fostering widespread adoption across various regions.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Government Regulations and Policies for Decarbonization | +2.1% | Europe (Nordic, Germany), North America (Canada), Asia Pacific (China, Japan) | Long-term, Sustained |

| Growing Demand for Energy Efficiency and Reduced Emissions | +1.8% | Global, particularly developed and rapidly urbanizing regions | Medium to Long-term |

| Rapid Urbanization and Infrastructure Development | +1.5% | Asia Pacific (China, India), Middle East, Africa, Latin America | Medium to Long-term |

| Increasing Integration of Renewable Energy Sources and Waste Heat | +1.3% | Europe, North America, emerging economies with resource potential | Medium to Long-term |

| Advantages of Centralized Systems (Reliability, Cost-Effectiveness at Scale) | +1.1% | Urban centers globally | Medium-term |

District Heating and Cooling Market Restraints Impact Analysis

Despite its significant growth potential, the District Heating and Cooling market faces several notable restraints that can impede its expansion. The high initial capital outlay required for developing new DHC networks or upgrading existing ones remains a primary barrier, particularly for regions with limited public funding or private investment. Additionally, the complexities associated with acquiring land rights, navigating intricate regulatory frameworks, and coordinating with multiple stakeholders can significantly delay project implementation. Public perception and the need for extensive planning further add to these challenges, often limiting the pace of adoption.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Capital Investment and Long Payback Periods | -1.9% | Global, particularly challenging in developing economies | Long-term, Persistent |

| Complex Regulatory Frameworks and Permitting Processes | -1.5% | North America, Europe (varying by country), Asia Pacific | Medium to Long-term |

| Lack of Public Awareness and Acceptance in Some Regions | -1.2% | North America, parts of Asia Pacific and Latin America | Medium-term |

| Competition from Decentralized Heating and Cooling Solutions | -0.9% | Global, especially in areas with established individual systems | Medium-term |

District Heating and Cooling Market Opportunities Impact Analysis

The District Heating and Cooling market is rich with opportunities that can accelerate its growth trajectory and expand its global footprint. The integration of DHC systems into broader smart city initiatives presents a significant pathway for efficiency gains and sustainable urban development. Furthermore, continuous technological advancements, particularly in areas like high-temperature thermal storage, advanced heat pumps, and network optimization software, are enhancing the competitiveness and performance of DHC systems. Exploring untapped markets in emerging economies, alongside the potential for waste heat utilization from various industrial processes, also represents compelling avenues for future market expansion.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration with Smart City Initiatives and Urban Planning | +1.7% | Global, particularly in rapidly developing urban areas and smart city projects | Long-term, Transformative |

| Technological Advancements in DHC Systems and Components | +1.5% | Global, driven by R&D in developed economies | Medium to Long-term |

| Expansion into Emerging Economies with Growing Energy Demands | +1.3% | Asia Pacific, Latin America, Middle East, Africa | Medium to Long-term |

| Increasing Focus on Waste Heat Recovery and Utilization | +1.1% | Industrialized regions globally, with high energy consumption | Medium-term |

| Retrofitting Existing Buildings and Districts for DHC Connectivity | +0.9% | Developed urban centers with aging infrastructure | Medium-term |

District Heating and Cooling Market Challenges Impact Analysis

While opportunities abound, the District Heating and Cooling market must navigate several inherent challenges to sustain its growth trajectory. The significant upfront investment often deters potential developers and municipalities, requiring creative financing models and strong policy support. Furthermore, the complexity of planning, designing, and implementing large-scale DHC networks, especially in densely populated urban environments, presents considerable technical and logistical hurdles. Issues such as public acceptance and the coordination among numerous stakeholders also pose ongoing challenges, demanding comprehensive engagement and long-term commitment to overcome.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Upfront Investment and Difficulty in Securing Funding | -1.8% | Global, especially prevalent in emerging markets and regions with limited public funding. | Long-term, Persistent |

| Technical Complexities in Planning, Design, and Implementation | -1.4% | Global, particularly in dense urban environments or regions with diverse building types. | Medium to Long-term |

| Public Acceptance and Overcoming NIMBYism (Not In My Backyard) | -1.1% | Developed countries with strong community activism, varying regionally. | Medium-term |

| Coordination and Stakeholder Management in Large-Scale Projects | -0.8% | Global, complex urban projects requiring multiple municipal and private entities. | Medium-term |

District Heating and Cooling Market - Updated Report Scope

This comprehensive market research report on the District Heating and Cooling market offers in-depth analysis and strategic insights tailored for business professionals and decision-makers. It covers critical market dynamics, including detailed forecasts, technological advancements, and the impact of evolving regulatory landscapes. The report's scope is designed to provide a holistic view of the market, enabling stakeholders to identify growth opportunities, understand competitive landscapes, and formulate informed business strategies within this rapidly transforming energy sector.

| Report Attributes | Report Details |

|---|---|

| Report Name | District Heating and Cooling Market |

| Market Size in 2025 | USD 265 Billion |

| Market Forecast in 2033 | USD 485 Billion |

| Growth Rate | CAGR of 2025 to 2033 7.8% |

| Number of Pages | 280 |

| Key Companies Covered | ENGIE, NRG Energy, Fortum, STEAG, Empower, ADC Energy Systems, Ørsted A/S, Vattenfall, Tabreed, RWE AG, Logstor, Emicool, Shinryo, Keppel DHCS, Goteborg Energi, Statkraft, Ramboll |

| Segments Covered | By Type, By Application, By End-Use Industry, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Customization Scope | Avail customised purchase options to meet your exact research needs. Request For Customization |

Segmentation Analysis

The District Heating and Cooling market is segmented to provide a granular understanding of its diverse components and applications. This segmentation allows for targeted analysis of market dynamics within specific product types and end-use sectors, revealing nuanced growth drivers and regional preferences. Understanding these segments is crucial for stakeholders aiming to identify niche opportunities and develop tailored strategies to meet varied market demands.

Market Product Type Segmentation:-- District Heating

- District Cooling

- Residential

- Commercial

- Industrial

Regional Highlights

Geographically, the District Heating and Cooling market exhibits varying dynamics influenced by regional policies, climatic conditions, and existing infrastructure. Each region presents unique opportunities and challenges, shaping the adoption and growth trajectory of DHC systems. Understanding these regional specificities is vital for stakeholders to align their strategies with localized market needs and regulatory environments.

- Europe: Europe is a leading market for District Heating and Cooling, largely driven by aggressive decarbonization targets, well-established DHC networks (especially in Nordic countries, Germany, and Eastern Europe), and strong government support for renewable energy integration. Countries like Denmark, Sweden, and Finland have high penetration rates, benefiting from abundant biomass and waste heat sources. The continent's focus on energy independence and reducing reliance on fossil fuels further propels investment in DHC expansion and modernization.

- North America: The North American market is steadily growing, primarily in urban centers and university campuses, driven by desires for energy efficiency, reduced carbon footprint, and resilience. The United States and Canada are witnessing increased adoption, spurred by incentives for sustainable infrastructure and the renovation of aging building stock. While growth is robust, it faces challenges related to initial investment costs and regulatory hurdles, necessitating tailored funding mechanisms.

- Asia Pacific (APAC): Asia Pacific represents the fastest-growing region, fueled by rapid urbanization, industrialization, and increasing energy demands, particularly in China, South Korea, and Japan. Government initiatives to combat air pollution and promote cleaner energy solutions are key drivers. The region's vast population and expanding infrastructure projects provide immense opportunities for new DHC installations, with a growing emphasis on integrating waste heat from industrial processes and incorporating advanced technologies.

- Middle East and Africa (MEA): The Middle East is a significant market for District Cooling, driven by high ambient temperatures and the need for efficient air conditioning in rapidly developing cities like Dubai and Abu Dhabi. Massive construction projects and a focus on sustainable development are leading to significant investments in large-scale DHC systems. Africa's market is nascent but holds long-term potential, especially in urbanizing areas seeking resilient and efficient energy solutions.

- Latin America: Latin America's DHC market is in its early stages but shows promise, particularly in countries like Brazil and Chile. The demand for modern infrastructure, coupled with increasing awareness of energy efficiency and sustainable development, is gradually driving interest. While growth is currently limited by economic factors and existing energy infrastructure, future opportunities exist in new urban developments and industrial clusters.

Top Key Players:

The market research report covers the analysis of key stake holders of the District Heating and Cooling Market. Some of the leading players profiled in the report include -:- ENGIE

- NRG Energy

- Fortum

- STEAG

- Empower

- ADC Energy Systems

- Ørsted A/S

- Vattenfall

- Tabreed

- RWE AG

- Logstor

- Emicool

- Shinryo

- Keppel DHCS

- Goteborg Energi

- Statkraft

- Ramboll

Frequently Asked Questions:

What is District Heating and Cooling (DHC)?

District Heating and Cooling (DHC) is a centralized energy system that produces and distributes heating and cooling to multiple buildings within a district or city. It uses a network of insulated pipes to deliver hot water (for heating) and chilled water (for cooling) from a central plant to commercial, residential, and industrial consumers, replacing individual boilers and air conditioning units.

What are the main benefits of District Heating and Cooling systems?

The main benefits of DHC systems include enhanced energy efficiency through economies of scale and diverse energy source integration, reduced carbon emissions by utilizing renewable energy and waste heat, increased energy reliability and security, and lower operating and maintenance costs for end-users. DHC also supports urban planning and smart city development by centralizing energy infrastructure.

What is the projected growth rate for the District Heating and Cooling market?

The District Heating and Cooling market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033. This growth is driven by increasing global focus on decarbonization, energy efficiency, and smart urban infrastructure development, making DHC a pivotal component of future sustainable energy systems.

Which regions are leading the District Heating and Cooling market?

Europe, particularly the Nordic countries and Germany, currently leads the District Heating and Cooling market due to well-established networks, strong policy support for renewable energy, and aggressive climate targets. Asia Pacific, especially China and South Korea, is emerging as the fastest-growing region, driven by rapid urbanization and significant investments in modern energy infrastructure.

How does AI impact the District Heating and Cooling market?

AI significantly impacts the DHC market by enabling predictive maintenance, optimizing energy distribution through accurate demand forecasting, and facilitating intelligent control systems for smart grid integration. This leads to increased operational efficiency, reduced energy waste, lower costs, and enhanced resilience of DHC networks by allowing proactive management and data-driven decision-making.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted