Display Glass Market

Display Glass Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709340 | Last Updated : December 08, 2025 |

Format : ![]()

![]()

![]()

![]()

Display Glass Market Size

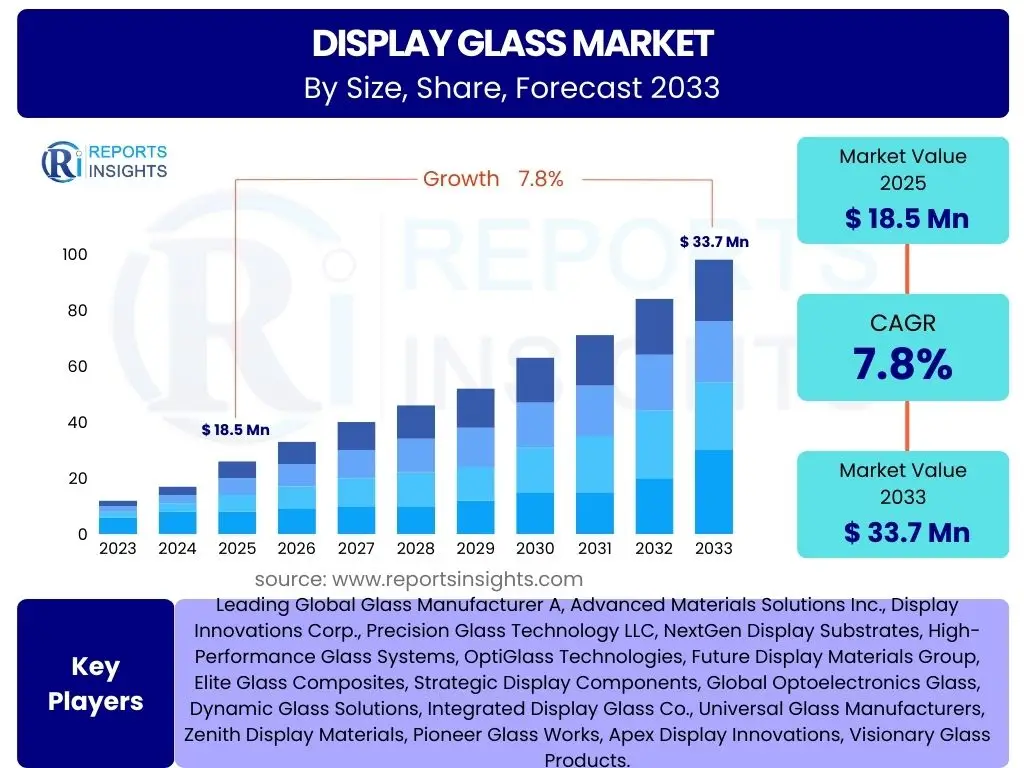

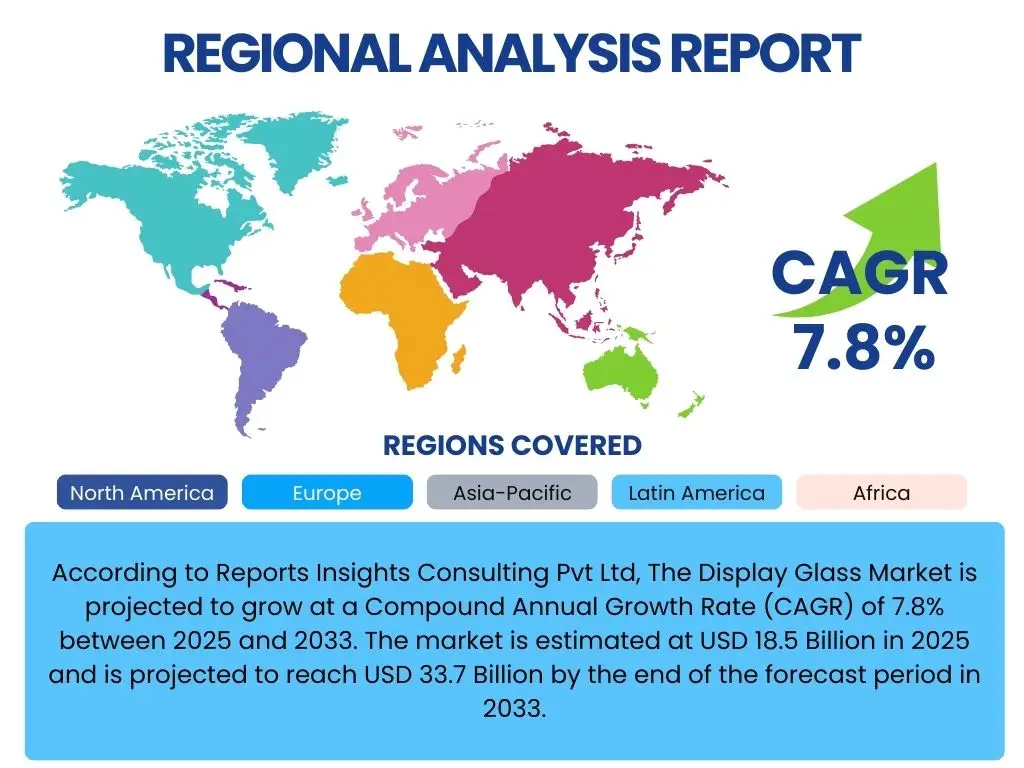

According to Reports Insights Consulting Pvt Ltd, The Display Glass Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033. The market is estimated at USD 18.5 Billion in 2025 and is projected to reach USD 33.7 Billion by the end of the forecast period in 2033.

Key Display Glass Market Trends & Insights

The Display Glass market is currently undergoing significant transformation, driven by evolving consumer demands and technological advancements across various industries. Users are actively seeking information regarding the latest innovations in display durability, flexibility, and energy efficiency, particularly in emerging applications like foldable smartphones, advanced automotive infotainment systems, and immersive AR/VR devices. There is a strong interest in how material science breakthroughs are enabling thinner, lighter, and more robust display solutions that can withstand diverse environmental conditions and user interactions.

Beyond material properties, the market is also influenced by trends in display form factors and integration. The push towards bezel-less designs, larger display areas, and the incorporation of haptic feedback and integrated sensors within the glass itself are prominent themes. Additionally, the increasing focus on sustainability and eco-friendly manufacturing processes for display glass is gaining traction, reflecting broader industry commitments to environmental responsibility. These trends collectively shape the trajectory of market growth and innovation, dictating research and development priorities for manufacturers.

- Demand for ultra-thin and flexible glass substrates for foldable and rollable displays.

- Increasing adoption of durable and scratch-resistant glass in smartphones and wearables.

- Growing integration of display glass in automotive dashboards and infotainment systems.

- Advancements in augmented reality (AR) and virtual reality (VR) devices driving demand for specialized optical glass.

- Emergence of large-format display solutions for public information and digital signage.

- Emphasis on eco-friendly manufacturing processes and recyclable glass materials.

AI Impact Analysis on Display Glass

Artificial intelligence (AI) is poised to significantly impact the Display Glass market by revolutionizing various stages of the product lifecycle, from design and manufacturing to quality control and material innovation. Users frequently inquire about AI's role in optimizing production efficiency, reducing defects, and accelerating the discovery of novel glass compositions with enhanced properties. AI-driven simulation and modeling tools are becoming crucial for predicting material behavior under different conditions, thereby shortening development cycles for next-generation display glass. This computational approach allows for rapid prototyping and testing of new designs and material combinations, leading to more efficient resource utilization.

Furthermore, AI algorithms are instrumental in implementing predictive maintenance for manufacturing equipment, minimizing downtime, and ensuring consistent product quality. In terms of end-user experience, AI could also facilitate the development of smarter, more adaptive displays that respond dynamically to user preferences and environmental contexts, though this is a more indirect impact on the glass itself. The long-term influence of AI extends to fostering innovation in material science, enabling the creation of advanced glass with previously unattainable optical, electrical, and mechanical characteristics, thereby expanding the application possibilities for display technology across diverse sectors.

- AI-driven optimization of manufacturing processes for increased efficiency and reduced waste.

- Enhanced quality control and defect detection through AI-powered vision systems.

- Accelerated material discovery and formulation using AI for novel glass compositions.

- Predictive maintenance of display glass production machinery, reducing downtime.

- Simulation and modeling of glass properties and performance using AI algorithms.

Key Takeaways Display Glass Market Size & Forecast

An analysis of user questions regarding the Display Glass market size and forecast reveals a keen interest in understanding the primary drivers behind the projected growth and the long-term sustainability of current market trends. Users seek clarity on which application segments will contribute most significantly to market expansion and how regional economic developments might influence demand. The consistent growth trajectory projected indicates robust opportunities, particularly within consumer electronics and automotive sectors, signaling continued innovation and adoption of advanced display technologies globally. The forecast period highlights a market characterized by both technological evolution and increasing market maturity in certain segments, balanced by emerging growth areas.

A crucial insight is the dual impact of innovation: while it drives demand for new display glass products, it also necessitates significant R&D investment and can lead to rapid product obsolescence if companies fail to adapt. The market is not merely expanding in volume but also in complexity and specialization, requiring manufacturers to develop diverse solutions for specific end-use requirements. This implies that companies with strong intellectual property and adaptable manufacturing capabilities are best positioned to capitalize on the predicted growth, navigating potential challenges such as supply chain vulnerabilities and intense competitive pressures. The underlying message is one of dynamic growth, underscored by the necessity for continuous innovation and strategic market positioning.

- The Display Glass market is poised for substantial growth, driven by technological advancements and increasing display adoption.

- Consumer electronics, especially smartphones and wearables, remain a primary growth engine for display glass.

- The automotive sector is emerging as a significant market for advanced display glass solutions.

- Innovations in flexible, ultra-thin, and durable glass are critical for future market expansion.

- Asia Pacific is expected to maintain its dominance due to strong manufacturing bases and consumer demand.

Display Glass Market Drivers Analysis

The Display Glass market is propelled by a confluence of technological advancements and increasing consumer and industrial demand for sophisticated display solutions. The ubiquitous nature of smartphones, coupled with the rapid evolution of display technologies such as OLED and Micro-LED, continuously fuels the need for high-performance, durable, and aesthetically pleasing glass substrates. Furthermore, the expansion of the automotive sector, with its growing emphasis on advanced infotainment systems, digital dashboards, and head-up displays, creates a robust demand for specialized, robust display glass that can withstand harsh environmental conditions while offering superior optical clarity and touch responsiveness. This ongoing innovation cycle in key end-use industries is a primary catalyst for market expansion.

Beyond traditional applications, the advent of new product categories like smart wearables, augmented reality (AR) and virtual reality (VR) headsets, and smart home devices further broadens the application landscape for display glass. These emerging segments often require highly customized glass solutions, including flexible or curved designs, specialized coatings for anti-glare or privacy, and enhanced impact resistance. The global trend towards digitalization and the increasing reliance on visual interfaces across various domains, from healthcare diagnostics to retail signage, ensures a sustained and diversified demand for display glass, driving both volume and value growth in the market.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Consumer Electronics Demand | +2.3% | Asia Pacific, North America, Europe | Short to Mid-term |

| Advancements in Display Technologies (OLED, Micro-LED, Foldable) | +1.9% | Global | Mid to Long-term |

| Increasing Adoption in Automotive Industry | +1.5% | Europe, North America, China | Mid to Long-term |

| Emergence of Smart Wearables and AR/VR Devices | +1.2% | North America, Europe, Asia Pacific | Short to Mid-term |

| Demand for Large Format Displays and Digital Signage | +0.9% | Global, particularly urban areas | Mid-term |

Display Glass Market Restraints Analysis

Despite robust growth drivers, the Display Glass market faces several significant restraints that could impede its overall expansion. One primary concern is the high manufacturing cost associated with advanced display glass, particularly for specialized applications like ultra-thin flexible substrates or custom optical components. The sophisticated processes, stringent quality control measures, and energy-intensive production facilities contribute to higher unit costs, which can translate into higher end-product prices, potentially limiting adoption in price-sensitive markets or for mass-market consumer electronics. This cost factor becomes increasingly relevant as competition from alternative materials or lower-cost display solutions emerges.

Another notable restraint is the inherent fragility of glass, even with advancements in toughening technologies. While modern display glass is significantly more durable, it remains susceptible to damage from severe impacts or bending beyond its designed limits, especially in consumer electronics where accidental drops are common. This fragility necessitates additional protective measures, such as screen protectors or robust device casings, adding to the overall product bulk and cost. Furthermore, supply chain disruptions, often triggered by geopolitical events, trade disputes, or natural disasters, can severely impact the availability of raw materials and the timely delivery of finished glass products, leading to production delays and increased operational complexities for display manufacturers globally.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Manufacturing Costs of Advanced Glass | -1.1% | Global, particularly emerging markets | Mid-term |

| Fragility and Susceptibility to Damage | -0.8% | Global (Consumer Electronics) | Short to Mid-term |

| Supply Chain Volatility and Raw Material Scarcity | -0.7% | Asia Pacific, Europe (Manufacturing Hubs) | Short-term |

| Competition from Alternative Display Technologies/Materials | -0.5% | Global | Long-term |

Display Glass Market Opportunities Analysis

The Display Glass market is rife with opportunities stemming from continuous innovation and the proliferation of display technology into new applications. The most significant opportunity lies in the burgeoning market for foldable and flexible displays, which demands entirely new categories of ultra-thin, bendable glass substrates. As major electronics manufacturers invest heavily in these form factors, the demand for specialized flexible glass capable of enduring millions of folds without compromising optical or mechanical integrity presents a substantial growth avenue. This technological frontier requires significant research and development, but promises high-value returns for innovators in the field.

Another compelling opportunity arises from the expanding ecosystem of augmented reality (AR) and virtual reality (VR) devices. These applications require high-precision optical glass components that offer superior clarity, minimal distortion, and often integrate advanced features like eye-tracking or transparent overlays. The automotive sector also offers immense potential, as vehicles transform into sophisticated mobile entertainment and information hubs. The increasing integration of larger, curved, and interactive display surfaces in vehicle interiors, along with external display applications for communication or autonomous vehicle status, will drive demand for robust, optically advanced, and customizable display glass solutions, creating a long-term growth trajectory for the market.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rising Demand for Foldable and Flexible Displays | +1.8% | Global (Key Tech Markets) | Mid to Long-term |

| Expansion of AR/VR and Mixed Reality Devices | +1.4% | North America, Europe, Asia Pacific | Mid to Long-term |

| Advanced Automotive Display Integration (e.g., HUDs, Large Infotainment) | +1.3% | Europe, North America, East Asia | Mid to Long-term |

| Development of Sustainable and Eco-friendly Glass Solutions | +0.9% | Global (Regulatory Pressure) | Long-term |

Display Glass Market Challenges Impact Analysis

The Display Glass market faces several critical challenges that require strategic navigation to sustain growth and innovation. One significant hurdle is the intense competition and the rapid pace of technological obsolescence. Manufacturers must continually invest heavily in research and development to keep pace with evolving display technologies and material science, leading to high capital expenditures and shorter product lifecycles. Failure to innovate swiftly can result in loss of market share and reduced profitability, particularly as competitors introduce superior or more cost-effective solutions. This dynamic environment places immense pressure on companies to remain at the forefront of material engineering.

Another major challenge involves managing the complex and often geographically dispersed supply chain. The sourcing of high-purity raw materials, specialized processing chemicals, and the intricate global logistics of manufacturing and distributing display glass can be susceptible to disruptions. Geopolitical tensions, trade tariffs, and the rising cost of energy and labor can all impact the supply chain, leading to increased operational costs and potential delays. Additionally, environmental regulations are becoming increasingly stringent, requiring display glass manufacturers to adopt more sustainable practices, which can involve significant investment in new technologies and processes to comply with emissions and waste reduction targets, adding another layer of complexity to operations.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Technological Obsolescence and R&D Costs | -1.0% | Global | Short to Mid-term |

| Intense Competition and Price Pressure | -0.9% | Asia Pacific (Key Manufacturing Region) | Short-term |

| Supply Chain Disruptions and Geopolitical Risks | -0.8% | Global | Short to Mid-term |

| Stringent Environmental Regulations and Sustainability Demands | -0.6% | Europe, North America, East Asia | Mid to Long-term |

Display Glass Market - Updated Report Scope

This comprehensive report delves into the intricate dynamics of the global Display Glass market, providing an in-depth analysis of its current state, historical performance, and future projections. It meticulously examines market size, growth drivers, restraints, opportunities, and challenges across various segments and key regions. The scope extends to a detailed assessment of the competitive landscape, profiling leading market participants and their strategic initiatives, alongside an evaluation of the impact of emerging technologies such as AI on the industry. The objective is to offer actionable insights for stakeholders seeking to navigate the evolving market and capitalize on upcoming trends.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 18.5 Billion |

| Market Forecast in 2033 | USD 33.7 Billion |

| Growth Rate | 7.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Leading Global Glass Manufacturer A, Advanced Materials Solutions Inc., Display Innovations Corp., Precision Glass Technology LLC, NextGen Display Substrates, High-Performance Glass Systems, OptiGlass Technologies, Future Display Materials Group, Elite Glass Composites, Strategic Display Components, Global Optoelectronics Glass, Dynamic Glass Solutions, Integrated Display Glass Co., Universal Glass Manufacturers, Zenith Display Materials, Pioneer Glass Works, Apex Display Innovations, Visionary Glass Products. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Display Glass market is comprehensively segmented to provide granular insights into its diverse components and applications. These segmentations are critical for understanding market dynamics, identifying growth pockets, and assessing the competitive landscape. The market is primarily bifurcated by the type of glass material used, which includes various compositions each optimized for specific performance characteristics. Furthermore, the segmentation by application details the wide array of electronic devices and systems that incorporate display glass, reflecting evolving consumer and industrial needs. Lastly, the end-use industry segmentation offers a macroscopic view of how different sectors drive demand, highlighting the economic forces at play and allowing for a targeted analysis of market opportunities and challenges within each vertical.

- By Type: Aluminosilicate Glass, Borosilicate Glass, Soda-lime Glass, Flexible Glass, Quartz Glass, Other Specialty Glass.

- By Application: Smartphones & Tablets, Laptops & PCs, Televisions, Wearable Devices, Automotive Displays, Industrial Displays, Medical Displays, Digital Signage & Large Format Displays, AR/VR Devices, Smart Home Devices, Others.

- By End-Use Industry: Consumer Electronics, Automotive, Healthcare, Industrial, Aerospace & Defense, Retail, Others.

Regional Highlights

- Asia Pacific: This region dominates the Display Glass market, primarily due to the presence of major electronics manufacturing hubs in countries like China, South Korea, Japan, and Taiwan. Rapid urbanization, a massive consumer base, and increasing disposable income further fuel the demand for consumer electronics and automotive displays. The region also benefits from significant investments in advanced display R&D and production capabilities, making it a pivotal area for market growth and innovation.

- North America: Characterized by high adoption rates of advanced technologies and a strong presence of leading technology companies, North America is a key market for display glass. The demand is driven by innovation in smartphones, smart wearables, and the burgeoning AR/VR segment. Significant R&D investment, coupled with a focus on premium and specialized display solutions, contributes to the region's strong market position. The automotive sector's shift towards digital cockpits also provides substantial growth opportunities.

- Europe: The European market for display glass is significantly influenced by its robust automotive industry, which increasingly integrates advanced display technologies into vehicles. Furthermore, demand from the consumer electronics and industrial sectors, alongside a growing emphasis on sustainable manufacturing practices, contributes to regional market expansion. Strict regulatory frameworks regarding material safety and environmental impact also drive innovation towards greener display glass solutions.

- Latin America: This region represents an emerging market for display glass, driven by increasing smartphone penetration and the expansion of consumer electronics markets. While smaller in comparison to other regions, steady economic growth and rising disposable incomes are gradually increasing the demand for devices incorporating display glass. Local manufacturing and assembly operations are also contributing to market development.

- Middle East and Africa (MEA): The MEA region is witnessing gradual growth in the display glass market, propelled by infrastructure development, increasing internet penetration, and a rising demand for consumer electronics. Investment in smart city initiatives and the hospitality sector also contributes to the adoption of digital signage and large-format displays, though the market is still in its nascent stages compared to developed regions.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Display Glass Market.- Leading Global Glass Manufacturer A

- Advanced Materials Solutions Inc.

- Display Innovations Corp.

- Precision Glass Technology LLC

- NextGen Display Substrates

- High-Performance Glass Systems

- OptiGlass Technologies

- Future Display Materials Group

- Elite Glass Composites

- Strategic Display Components

- Global Optoelectronics Glass

- Dynamic Glass Solutions

- Integrated Display Glass Co.

- Universal Glass Manufacturers

- Zenith Display Materials

- Pioneer Glass Works

- Apex Display Innovations

- Visionary Glass Products

Frequently Asked Questions

What is display glass?

Display glass is a specialized type of glass, typically thin and optically clear, designed as the substrate or protective layer for electronic displays such as LCDs, OLEDs, and plasma screens. It provides structural support, protection, and allows for light transmission critical for visual output.

What are the primary types of display glass?

The primary types of display glass include aluminosilicate glass (known for strength, e.g., smartphone screens), borosilicate glass (heat resistance, e.g., high-temperature applications), and soda-lime glass (cost-effective, for basic displays). Flexible glass is an emerging type for bendable devices.

Which industries widely use display glass?

Display glass is extensively used across various industries, notably consumer electronics (smartphones, TVs, laptops), automotive (infotainment, digital dashboards), medical (diagnostic equipment), industrial (control panels), and digital signage (public displays).

How do advancements in display technology impact display glass demand?

Advancements like OLED, Micro-LED, and foldable displays significantly impact demand by requiring specialized glass with properties such as ultra-thinness, flexibility, enhanced durability, and improved optical performance, driving innovation and market growth.

What are the key factors driving growth in the display glass market?

Key growth drivers include the increasing global demand for consumer electronics, the expansion of display integration in the automotive sector, the emergence of smart wearables and AR/VR devices, and ongoing technological innovations in display panel manufacturing.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted