Digital Process Automation Software Market

Digital Process Automation Software Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700978 | Last Updated : July 29, 2025 |

Format : ![]()

![]()

![]()

![]()

Digital Process Automation Software Market Size

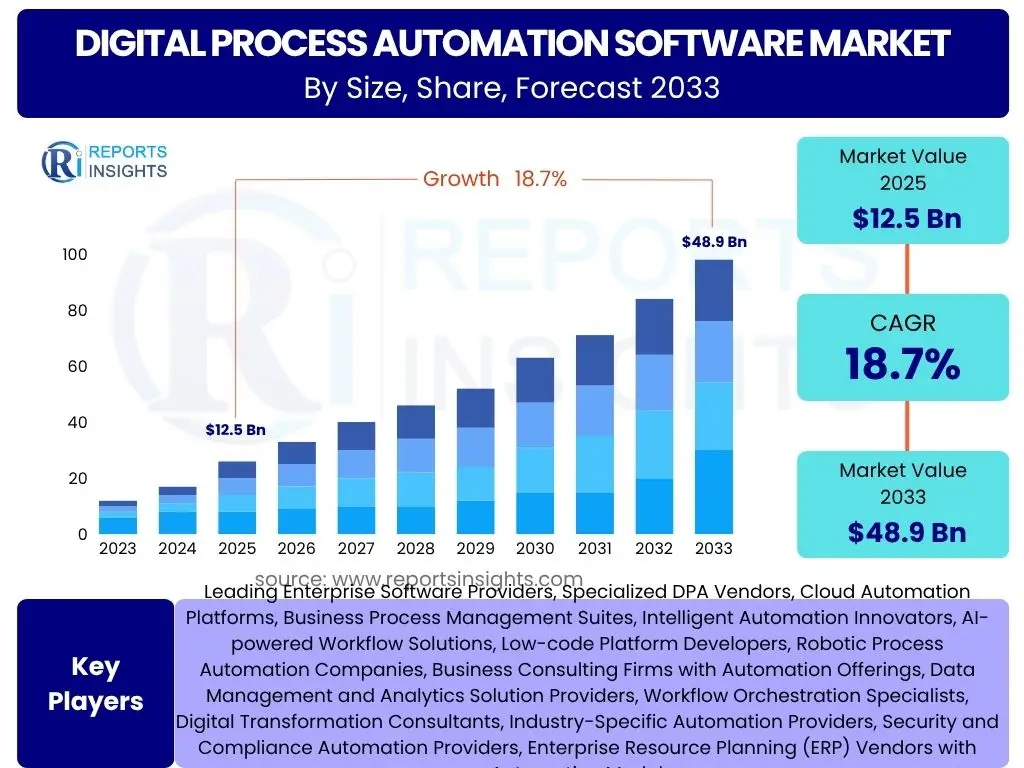

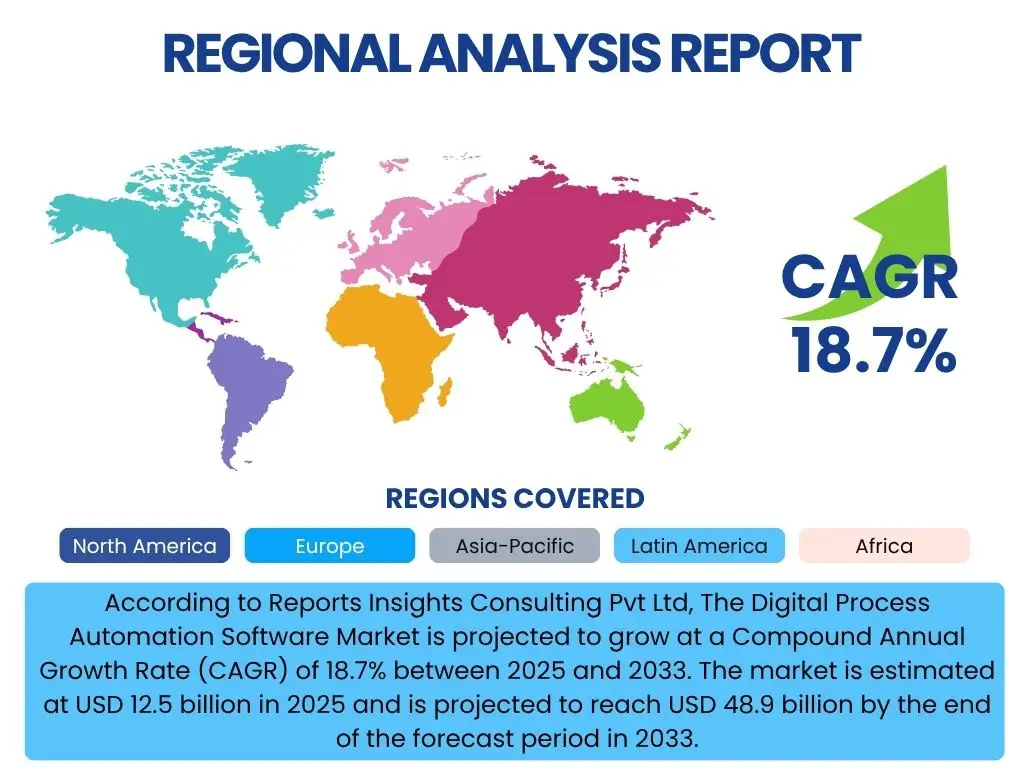

According to Reports Insights Consulting Pvt Ltd, The Digital Process Automation Software Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.7% between 2025 and 2033. The market is estimated at USD 12.5 billion in 2025 and is projected to reach USD 48.9 billion by the end of the forecast period in 2033.

This robust growth is primarily driven by the escalating demand for operational efficiency, enhanced customer experiences, and the imperative for organizations to accelerate their digital transformation initiatives. Businesses are increasingly recognizing the strategic value of automating complex, end-to-end processes to reduce manual errors, improve compliance, and free up human resources for more strategic tasks. The market's expansion reflects a global shift towards agile and resilient business models, where automation plays a pivotal role in optimizing workflows across various departments, from finance and HR to customer service and supply chain management.

The significant projected increase in market valuation underscores a pervasive organizational need to overcome traditional operational bottlenecks and achieve greater agility in dynamic market conditions. As enterprises continue to invest in advanced technologies to streamline their operations, the adoption of digital process automation (DPA) software is becoming a cornerstone of competitive advantage. This growth trajectory is further supported by the increasing accessibility and scalability of cloud-based DPA solutions, making them viable for a broader spectrum of businesses, including small and medium-sized enterprises (SMEs).

Key Digital Process Automation Software Market Trends & Insights

Users frequently inquire about the emerging trends shaping the Digital Process Automation Software market, seeking insights into technological advancements, evolving business needs, and the impact of these on market dynamics. Common questions revolve around the convergence of DPA with artificial intelligence, the rise of low-code/no-code platforms, and the increasing focus on end-to-end process orchestration. These inquiries highlight a collective desire to understand how DPA is evolving beyond simple task automation to become a strategic enabler of enterprise-wide digital transformation, emphasizing intelligence, flexibility, and user accessibility.

A significant trend observed is the move towards hyperautomation, which involves combining DPA with other advanced technologies like AI, Machine Learning (ML), Robotic Process Automation (RPA), and Intelligent Document Processing (IDP) to automate an ever-increasing number of business and IT processes. This holistic approach aims to achieve maximum efficiency and agility by orchestrating various automation capabilities across the enterprise. Furthermore, there is a growing emphasis on process mining and discovery tools, which help organizations identify, map, and analyze current processes to pinpoint automation opportunities and measure the impact of implemented solutions. This data-driven approach ensures that automation efforts are targeted and yield optimal returns.

Another crucial insight is the accelerating adoption of low-code/no-code DPA platforms, empowering business users and citizen developers to create and deploy automated workflows without extensive coding knowledge. This democratization of development significantly reduces IT backlogs, accelerates time-to-market for new automated processes, and fosters greater collaboration between business and IT departments. The focus is shifting from merely automating individual tasks to orchestrating complex, human-centric processes, ensuring seamless collaboration between human workers and automated systems, thereby improving overall operational flow and employee experience.

- Hyperautomation strategy integrating DPA with AI, ML, and RPA.

- Increased adoption of low-code/no-code DPA platforms for business users.

- Emphasis on process mining and discovery for identifying automation opportunities.

- Shift towards end-to-end process orchestration rather than discrete task automation.

- Focus on AI-driven intelligent process automation for enhanced decision-making.

AI Impact Analysis on Digital Process Automation Software

User queries regarding the impact of Artificial Intelligence (AI) on Digital Process Automation Software frequently center on how AI enhances automation capabilities, improves decision-making, and addresses complex, unstructured data. Concerns often include the ethical implications of AI-driven automation, the need for robust data governance, and the potential for job displacement. Users are keen to understand if AI primarily augments human capabilities or replaces them, and how it contributes to creating more adaptive and intelligent automated processes within organizations.

AI is profoundly transforming DPA by injecting intelligence into automated workflows, moving beyond rule-based automation to enable adaptive and predictive capabilities. AI-powered DPA solutions can analyze vast amounts of data, identify patterns, and make informed decisions, allowing for the automation of more complex and variable processes that previously required human intervention. For instance, AI can be used for intelligent document processing (IDP) to extract and interpret unstructured data from various sources, such as invoices, contracts, or customer emails, feeding this information directly into DPA workflows and significantly reducing manual data entry and processing times. This capability enhances accuracy and accelerates response times, particularly in customer-facing operations.

Furthermore, AI-driven analytics and machine learning algorithms are enabling DPA systems to continuously learn and optimize processes over time. By analyzing performance data, AI can identify bottlenecks, suggest improvements, and even automatically adjust workflows to achieve better outcomes, making automation initiatives more efficient and effective. The integration of conversational AI and natural language processing (NLP) into DPA allows for more intuitive human-machine interactions, facilitating automated customer service, virtual assistants, and improved employee self-service portals. While concerns about job displacement exist, the prevailing view is that AI in DPA will largely augment human capabilities, allowing employees to focus on higher-value, strategic tasks while repetitive processes are handled by intelligent automation.

- Enhanced decision-making and predictive capabilities within automated workflows.

- Intelligent document processing (IDP) for unstructured data extraction.

- Continuous process optimization through machine learning and analytics.

- Improved human-machine interaction via conversational AI and NLP.

- Shift towards more adaptive and resilient automated business processes.

Key Takeaways Digital Process Automation Software Market Size & Forecast

Users commonly seek concise summaries of the Digital Process Automation Software market's future outlook, focusing on what key factors will drive or impede its growth and where the most significant opportunities lie. Questions frequently address the long-term viability of DPA as a foundational technology, the sectors most likely to see accelerated adoption, and the strategic implications for businesses planning their digital transformation journeys. These inquiries highlight a need for clear, actionable insights into the market's trajectory and its relevance to organizational growth and efficiency.

The market is poised for sustained, significant growth through 2033, driven by the increasing complexity of business operations and the universal imperative for digital transformation across industries. This sustained expansion indicates that DPA is no longer a niche technology but a core component of modern enterprise infrastructure, enabling organizations to achieve unparalleled operational agility and cost efficiencies. The shift towards cloud-native DPA solutions and consumption-based models is lowering entry barriers, making advanced automation accessible to a wider array of businesses, including small and medium-sized enterprises (SMEs) that are keen to leverage automation without heavy upfront investments.

Strategic investments in DPA are expected to yield substantial returns in terms of productivity gains, reduced operational costs, and improved compliance, making it a critical investment for businesses aiming to remain competitive. The market's future will be characterized by greater integration with emerging technologies such as Artificial Intelligence and the Internet of Things, leading to more intelligent and interconnected automation ecosystems. Organizations that prioritize DPA as part of a broader hyperautomation strategy will be better positioned to adapt to rapid market changes, enhance customer experiences, and achieve sustainable growth in the evolving global economy, reinforcing DPA's role as a strategic differentiator.

- Robust and sustained market growth through 2033, underscoring DPA's strategic importance.

- Increasing adoption across industries driven by digital transformation and efficiency needs.

- Lowered barriers to entry due to prevalent cloud-based and low-code DPA solutions.

- Significant ROI potential through operational cost reduction and productivity gains.

- Future growth fueled by deeper integration with AI, IoT, and advanced analytics.

Digital Process Automation Software Market Drivers Analysis

The Digital Process Automation Software market is significantly propelled by several key drivers, primarily the escalating global emphasis on digital transformation initiatives across all sectors. Organizations are realizing that traditional manual processes are bottlenecks to agility and efficiency, leading them to aggressively adopt DPA solutions to streamline operations, reduce human error, and accelerate workflows. This shift is not merely about cost reduction but about fundamentally reimagining how work is done, enabling faster decision-making and improved responsiveness to market demands. The competitive landscape mandates that businesses achieve greater operational fluidity, which DPA inherently facilitates by automating routine and complex processes.

Another major driver is the increasing demand for enhanced customer experience (CX) and employee experience (EX). DPA plays a crucial role in improving CX by automating customer-facing processes, leading to faster service delivery, personalized interactions, and reduced wait times. Similarly, by automating mundane and repetitive tasks, DPA frees employees from tedious work, allowing them to focus on more strategic, creative, and fulfilling activities, thereby boosting EX and overall productivity. This dual focus on improving both external and internal stakeholder experiences serves as a powerful incentive for DPA adoption.

Furthermore, the growing regulatory compliance requirements and the need for greater transparency and auditability in business operations are strong drivers. DPA software helps organizations meet these demands by ensuring that processes adhere to defined rules and regulations, maintaining an immutable audit trail of all automated activities. The rapid adoption of cloud computing and Software-as-a-Service (SaaS) models also contributes significantly, making DPA solutions more accessible, scalable, and cost-effective for businesses of all sizes, reducing the need for significant upfront infrastructure investments and accelerating deployment cycles.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Accelerated Digital Transformation Initiatives | +4.2% | Global, particularly North America, Europe, Asia Pacific | Short to Long-term (2025-2033) |

| Demand for Operational Efficiency and Cost Reduction | +3.8% | Global, all industries | Short to Mid-term (2025-2029) |

| Focus on Enhanced Customer and Employee Experience | +3.5% | Global, particularly service-oriented sectors | Mid to Long-term (2026-2033) |

| Increasing Cloud and SaaS Adoption | +3.0% | Global, especially emerging economies | Short to Mid-term (2025-2030) |

| Stringent Regulatory Compliance Requirements | +2.5% | Highly regulated industries (Finance, Healthcare) across all regions | Short to Long-term (2025-2033) |

Digital Process Automation Software Market Restraints Analysis

Despite its significant growth potential, the Digital Process Automation Software market faces several restraints that could impede its widespread adoption and impact its CAGR. A primary restraint is the significant initial investment required for sophisticated DPA solutions, which includes not only software licenses but also implementation costs, integration with legacy systems, and employee training. For small and medium-sized enterprises (SMEs) or organizations with limited IT budgets, this upfront financial commitment can be a substantial barrier, often leading them to delay or reconsider DPA initiatives, despite the long-term benefits.

Another crucial restraint is the complexity associated with integrating DPA platforms with existing diverse IT landscapes. Many organizations operate with fragmented systems and legacy applications that were not designed for seamless integration, leading to significant challenges in achieving end-to-end process automation. The technical complexities of data migration, API development, and ensuring interoperability can be time-consuming and resource-intensive, requiring specialized expertise that may not always be readily available within an organization. This integration hurdle can lead to project delays, increased costs, and even failure if not properly managed.

Furthermore, resistance to change within organizations poses a significant non-technical restraint. Employees may fear job displacement or perceive automation as a threat, leading to reluctance in adopting new processes and tools. Overcoming this cultural inertia requires robust change management strategies, clear communication, and reskilling programs to highlight the benefits of DPA for employees, such as freeing them for higher-value tasks. Additionally, concerns around data security and privacy, particularly with sensitive information processed by DPA systems, can act as a significant barrier. Organizations are increasingly wary of potential data breaches or non-compliance issues, necessitating stringent security measures and robust governance frameworks for DPA deployments.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment and Implementation Costs | -2.8% | Global, particularly SMEs and budget-constrained organizations | Short to Mid-term (2025-2030) |

| Complexity of Integration with Legacy Systems | -2.5% | Mature markets with entrenched IT infrastructures (e.g., North America, Europe) | Short to Long-term (2025-2033) |

| Resistance to Change and Skill Gap | -2.0% | Global, varies by organizational culture and industry | Short to Mid-term (2025-2029) |

| Data Security and Privacy Concerns | -1.5% | Global, especially highly regulated industries | Short to Long-term (2025-2033) |

| Lack of Clear ROI Measurement Frameworks | -1.0% | Global, all industries seeking clear business cases | Short to Mid-term (2025-2028) |

Digital Process Automation Software Market Opportunities Analysis

The Digital Process Automation Software market presents numerous growth opportunities stemming from evolving technological landscapes and burgeoning business needs. A significant opportunity lies in the expanding scope of hyperautomation, which involves integrating DPA with other advanced technologies like AI, machine learning, and robotic process automation (RPA) to automate complex, end-to-end processes that span across multiple systems and departments. This holistic approach unlocks greater efficiency gains and business agility than standalone automation initiatives, creating a fertile ground for vendors offering comprehensive, integrated solutions that can orchestrate diverse automation components. The ability to provide solutions that facilitate true enterprise-wide automation will be a key differentiator.

Another substantial opportunity is the continued growth in demand for industry-specific DPA solutions. While generic DPA platforms offer broad applicability, vertical-specific solutions tailored to the unique regulatory requirements, workflows, and data structures of industries such as healthcare, finance, manufacturing, and public sector can address specific pain points more effectively. These specialized solutions resonate well with clients seeking rapid deployment and high relevance, reducing the need for extensive customization. Developing and marketing such niche-focused DPA offerings allows vendors to capture significant market share within these specialized segments by demonstrating deep industry understanding and delivering targeted value.

Furthermore, the increasing adoption of cloud-based DPA as a service (DPAaaS) models provides significant expansion opportunities. DPAaaS lowers the entry barrier for small and medium-sized enterprises (SMEs) by reducing upfront costs and IT infrastructure requirements, offering scalability and flexibility. This model also allows for faster deployment and updates, enabling businesses to quickly adapt to changing market conditions. The growing focus on citizen development, facilitated by low-code/no-code DPA platforms, empowers business users to build and modify their own automated workflows, significantly accelerating process improvements and reducing reliance on IT departments. This trend democratizes automation and broadens the addressable market, as more internal stakeholders can contribute directly to automation initiatives.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion of Hyperautomation Ecosystems | +3.5% | Global, all large enterprises | Mid to Long-term (2026-2033) |

| Growing Demand for Industry-Specific Solutions | +3.0% | Global, particularly healthcare, finance, manufacturing, public sector | Short to Long-term (2025-2033) |

| Increased Adoption of Cloud-based DPA (DPAaaS) | +2.8% | Global, especially SMEs and digital-native companies | Short to Mid-term (2025-2030) |

| Rise of Citizen Development with Low-code/No-code Platforms | +2.5% | Global, all organizational sizes | Short to Mid-term (2025-2029) |

| Untapped Market Potential in Emerging Economies | +2.0% | Asia Pacific, Latin America, Middle East & Africa | Mid to Long-term (2027-2033) |

Digital Process Automation Software Market Challenges Impact Analysis

The Digital Process Automation Software market faces several inherent challenges that can impact its growth trajectory and adoption rates. One significant challenge is managing the complexity of change within organizations, as implementing DPA often requires a fundamental shift in how employees perform their tasks and interact with processes. This cultural transformation can be difficult, leading to resistance from employees who may fear job displacement or simply be uncomfortable with new technologies and workflows. Effective change management strategies, clear communication, and robust training programs are essential but often underestimated in their complexity and resource requirements.

Another critical challenge revolves around data quality and governance. DPA solutions rely heavily on accurate and consistent data to function effectively. Organizations often struggle with fragmented data sources, inconsistent data formats, and poor data quality, which can lead to flawed automation outcomes or require extensive pre-processing. Ensuring robust data governance frameworks, including data standardization, cleansing, and security protocols, is crucial but can be a complex and ongoing effort. Without high-quality data, the full potential of DPA cannot be realized, potentially leading to skepticism about its value proposition.

Furthermore, vendor lock-in and interoperability issues present a significant challenge for organizations. As DPA solutions become deeply embedded in an enterprise's operational fabric, switching vendors can be costly, time-consuming, and disruptive. This creates a reliance on a single vendor, potentially limiting flexibility and competitive pricing. The lack of standardized integration protocols across different DPA platforms and other enterprise systems can also hinder seamless end-to-end automation, requiring custom integrations that are expensive to develop and maintain. These challenges necessitate careful strategic planning and selection of DPA solutions that offer flexibility and open integration capabilities.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Managing Organizational Change and Resistance | -2.2% | Global, all organizational cultures | Short to Mid-term (2025-2029) |

| Data Quality and Governance Issues | -1.8% | Global, particularly data-intensive industries | Short to Long-term (2025-2033) |

| Vendor Lock-in and Interoperability Concerns | -1.5% | Global, larger enterprises with complex IT landscapes | Mid to Long-term (2026-2033) |

| Scalability and Performance Optimization | -1.0% | Global, rapidly growing organizations | Mid-term (2027-2031) |

| Cybersecurity Risks and Compliance with Regulations | -0.8% | Global, all industries, especially those handling sensitive data | Short to Long-term (2025-2033) |

Digital Process Automation Software Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Digital Process Automation Software market, covering historical performance, current market dynamics, and future projections. It offers detailed insights into market size, growth drivers, restraints, opportunities, and challenges, with a specific focus on the transformative impact of AI and emerging technologies. The scope encompasses market segmentation by component, deployment, organization size, industry vertical, and regional analysis, providing a holistic view of the market landscape to aid strategic decision-making for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 12.5 billion |

| Market Forecast in 2033 | USD 48.9 billion |

| Growth Rate | 18.7% CAGR |

| Number of Pages | 267 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Leading Enterprise Software Providers, Specialized DPA Vendors, Cloud Automation Platforms, Business Process Management Suites, Intelligent Automation Innovators, AI-powered Workflow Solutions, Low-code Platform Developers, Robotic Process Automation Companies, Business Consulting Firms with Automation Offerings, Data Management and Analytics Solution Providers, Workflow Orchestration Specialists, Digital Transformation Consultants, Industry-Specific Automation Providers, Security and Compliance Automation Providers, Enterprise Resource Planning (ERP) Vendors with Automation Modules |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Digital Process Automation Software market is comprehensively segmented to provide a nuanced understanding of its various facets, enabling stakeholders to pinpoint specific areas of growth, opportunity, and challenge. This detailed segmentation allows for a granular analysis of market dynamics across different components, deployment models, organizational sizes, and industry verticals, reflecting the diverse applications and adoption patterns of DPA solutions globally. Understanding these segments is critical for developing targeted strategies and identifying specific market niches for product development and expansion.

The segmentation by component differentiates between the core DPA platform and associated services, including professional and managed services, highlighting the comprehensive support ecosystem required for successful DPA implementation and ongoing optimization. Deployment models distinguish between traditional on-premise solutions, favored by organizations with stringent data security requirements or extensive legacy infrastructure, and the rapidly growing cloud-based solutions, preferred for their scalability, flexibility, and reduced upfront costs. This distinction is crucial as cloud adoption continues to accelerate across industries, shaping future market trends.

Further segmentation by organization size, categorizing enterprises into Small and Medium-sized Enterprises (SMEs) and Large Enterprises, reveals distinct needs and investment capacities, influencing the types of DPA solutions sought and adopted. Lastly, the breakdown by industry vertical provides critical insights into the unique drivers and challenges faced by sectors such as BFSI, Healthcare, IT & Telecom, Manufacturing, and Retail, among others. Each industry has specific processes ripe for automation, and this segmentation helps identify the most promising vertical markets for DPA solution providers, allowing for highly specialized and effective market engagement strategies.

- Component:

- Platform

- Services

- Professional Services

- Managed Services

- Deployment:

- On-premise

- Cloud-based

- Organization Size:

- Small and Medium-sized Enterprises (SMEs)

- Large Enterprises

- Industry Vertical:

- BFSI (Banking, Financial Services, and Insurance)

- Healthcare and Life Sciences

- IT and Telecommunications

- Manufacturing and Automotive

- Retail and Consumer Goods

- Government and Public Sector

- Others (e.g., Energy & Utilities, Education)

Regional Highlights

- North America: This region is a dominant force in the Digital Process Automation Software market, primarily driven by early adoption of advanced technologies, a strong focus on digital transformation, and the presence of numerous key market players. The United States and Canada lead in terms of innovation and investment in DPA solutions, particularly in large enterprises across BFSI, healthcare, and IT sectors. The high awareness of automation benefits and a competitive business environment foster continuous DPA adoption to enhance operational efficiency and customer experience.

- Europe: Europe represents a significant market for DPA software, characterized by stringent regulatory landscapes and a strong emphasis on data privacy (e.g., GDPR), which drives demand for compliant and secure automation solutions. Western European countries like the UK, Germany, and France are prominent adopters, with increasing investment in DPA across manufacturing, public sector, and financial services to streamline processes and ensure compliance. The region is witnessing a steady shift towards cloud-based DPA solutions, though on-premise deployment remains relevant in certain highly regulated industries.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region in the DPA market, fueled by rapid digital transformation initiatives, increasing industrialization, and growing awareness of automation benefits in emerging economies like China, India, and Southeast Asian countries. Government support for digitalization, expanding IT infrastructure, and a large number of SMEs looking for scalable and cost-effective solutions are key drivers. The region offers immense untapped potential, with significant investments in DPA for optimizing supply chains, enhancing customer service, and boosting productivity in manufacturing and retail sectors.

- Latin America: This region is experiencing a gradual but steady adoption of DPA software, driven by the need for operational efficiency and competitive advantage in a challenging economic landscape. Brazil and Mexico are leading the charge, with growing investments from BFSI, telecommunications, and retail sectors. While budget constraints and legacy infrastructure pose challenges, the increasing understanding of DPA's ROI and the availability of flexible cloud-based solutions are contributing to market expansion.

- Middle East and Africa (MEA): The MEA region is emerging as a growth hub for DPA, spurred by government-led digital transformation visions (e.g., Saudi Vision 2030, UAE's smart city initiatives) and diversification efforts away from oil economies. Countries in the GCC are investing heavily in DPA to modernize public services, enhance smart city operations, and optimize processes in sectors like finance and energy. While still nascent in some parts, increasing foreign investment and a rising tech-savvy population are paving the way for substantial DPA market expansion in the coming years.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Digital Process Automation Software Market.- Leading Enterprise Software Providers

- Specialized DPA Vendors

- Cloud Automation Platforms

- Business Process Management Suites

- Intelligent Automation Innovators

- AI-powered Workflow Solutions

- Low-code Platform Developers

- Robotic Process Automation Companies

- Business Consulting Firms with Automation Offerings

- Data Management and Analytics Solution Providers

- Workflow Orchestration Specialists

- Digital Transformation Consultants

- Industry-Specific Automation Providers

- Security and Compliance Automation Providers

- Enterprise Resource Planning (ERP) Vendors with Automation Modules

- Customer Relationship Management (CRM) Solution Providers with Automation

- Supply Chain Management Software Providers

- Human Capital Management (HCM) System Vendors

- Enterprise Content Management (ECM) Solution Providers

- Integrated Suite Providers

Frequently Asked Questions

What is Digital Process Automation Software?

Digital Process Automation (DPA) Software automates and optimizes end-to-end business processes, typically involving complex workflows and human-centric tasks. It goes beyond simple task automation by orchestrating processes, managing data, and integrating with various systems to improve efficiency, reduce errors, and enhance user experiences. DPA often leverages capabilities like workflow management, forms, content management, and analytics to streamline operations.

How does AI impact Digital Process Automation?

AI significantly enhances Digital Process Automation by adding intelligence and adaptive capabilities. AI enables DPA platforms to handle unstructured data through Intelligent Document Processing (IDP), make smarter decisions based on data analysis, and continuously optimize processes through machine learning. This transforms DPA from rule-based automation to more predictive, adaptive, and human-like process execution.

What are the primary benefits of implementing DPA software?

Implementing DPA software offers numerous benefits, including significant improvements in operational efficiency and cost reduction through automated workflows. It enhances customer and employee experiences by speeding up service delivery and reducing manual tasks. DPA also improves regulatory compliance, data accuracy, and business agility, enabling organizations to adapt quickly to market changes and drive digital transformation.

Which industries are most actively adopting DPA solutions?

Industries most actively adopting DPA solutions include Banking, Financial Services, and Insurance (BFSI) for enhanced compliance and customer onboarding; Healthcare and Life Sciences for patient data management and claims processing; IT and Telecommunications for service delivery and network operations; Manufacturing and Automotive for supply chain optimization; and Government and Public Sector for public service delivery and administrative efficiency.

What are the key challenges in DPA implementation?

Key challenges in DPA implementation include the high initial investment and integration complexities with existing legacy systems. Organizational resistance to change, often due to fear of job displacement or discomfort with new technologies, can also impede adoption. Furthermore, ensuring high data quality and addressing cybersecurity concerns are critical for successful and secure DPA deployment.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted