Digital Grocery Market

Digital Grocery Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702091 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

Digital Grocery Market Size

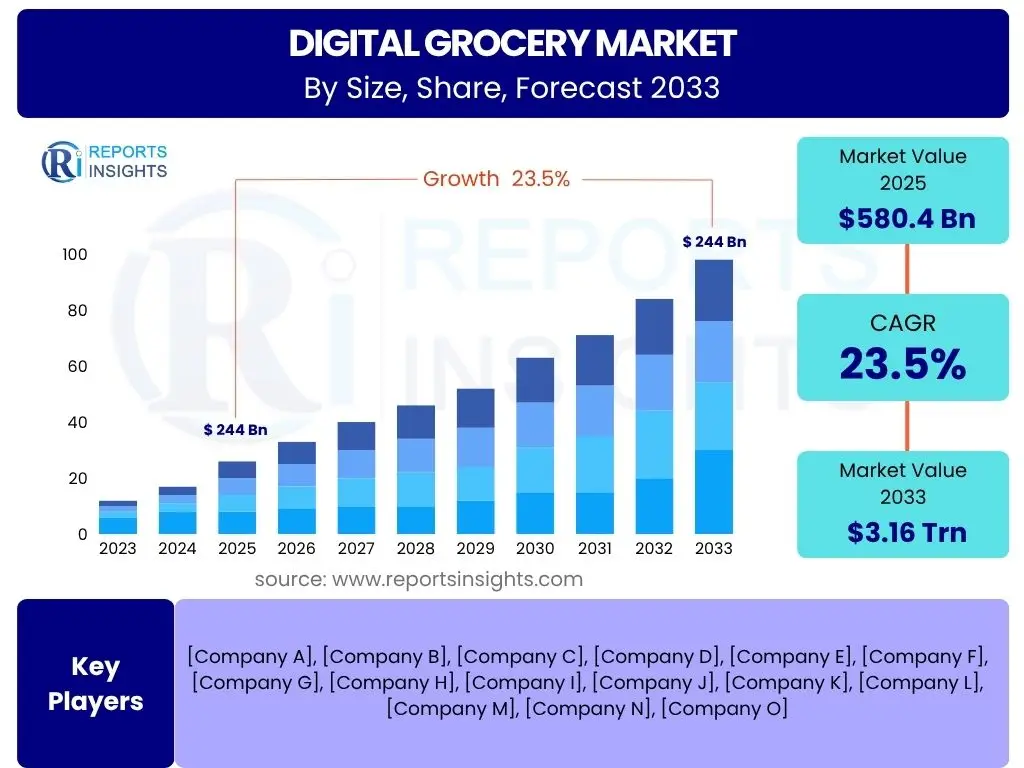

According to Reports Insights Consulting Pvt Ltd, The Digital Grocery Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 23.5% between 2025 and 2033. This robust growth is primarily driven by shifting consumer preferences towards convenience, advancements in e-commerce infrastructure, and the increasing penetration of digital technologies across various demographics. The market's expansion is further fueled by innovations in last-mile delivery and personalized shopping experiences.

The market is estimated at USD 580.4 billion in 2025 and is projected to reach USD 3.16 trillion by the end of the forecast period in 2033. This significant increase underscores the accelerating adoption of online grocery platforms globally. Factors such as urbanization, busier lifestyles, and enhanced digital literacy contribute to this upward trajectory, positioning digital grocery as a fundamental component of future retail landscapes. Investments in logistics and supply chain optimization by key players are also pivotal in supporting this growth projection.

Key Digital Grocery Market Trends & Insights

The digital grocery market is experiencing transformative shifts, primarily driven by evolving consumer expectations for convenience and personalized services. Users are increasingly seeking frictionless shopping experiences, from intuitive mobile applications to flexible delivery options. This includes a growing demand for same-day and even ultra-fast delivery services, pushing retailers to optimize their logistical capabilities and fulfillment networks. The emphasis on healthy and sustainable product choices is also a significant trend, with consumers actively looking for transparency in sourcing and eco-friendly packaging.

Another prominent trend involves the integration of advanced technologies like AI and machine learning to enhance customer engagement and operational efficiency. Retailers are leveraging these tools for personalized recommendations, predictive inventory management, and optimized delivery routes, directly addressing user desires for tailored experiences and timely product availability. Furthermore, the rise of subscription-based models for recurring purchases and the expansion of click-and-collect options demonstrate a diversification of service offerings designed to meet varied consumer lifestyles and preferences.

- Hyper-personalization of shopping experiences and product recommendations.

- Expansion of quick commerce and ultra-fast delivery services.

- Increased adoption of subscription models for recurring grocery purchases.

- Growing consumer demand for sustainable and ethically sourced products.

- Integration of advanced analytics and AI for supply chain optimization and predictive inventory.

- Diversification of fulfillment options, including expanded click-and-collect networks.

- Enhanced focus on seamless mobile shopping and user-friendly app interfaces.

AI Impact Analysis on Digital Grocery

The impact of Artificial Intelligence (AI) on the digital grocery sector is profound, fundamentally reshaping operations, customer interactions, and market dynamics. Users frequently inquire about how AI streamlines the online grocery experience, its role in personalization, and its potential to reduce food waste. AI-powered systems are enabling sophisticated demand forecasting, optimizing inventory levels to minimize spoilage and stockouts, and automating warehouse operations, leading to greater efficiency and cost savings for retailers. This directly translates into better product availability and fresher produce for consumers.

From a customer perspective, AI is central to delivering highly personalized shopping journeys. Algorithms analyze purchase history, browsing behavior, and even external factors like weather to offer tailored product recommendations, suggest meal plans, and personalize promotional offers. This capability significantly enhances user satisfaction and encourages repeat purchases. While there are concerns about data privacy and the potential for job displacement in certain operational roles, the overarching expectation among users is that AI will continue to make online grocery shopping more intuitive, efficient, and aligned with individual needs, driving the evolution towards a truly smart retail environment.

- Enhanced demand forecasting and inventory optimization, reducing waste.

- Personalized product recommendations and targeted marketing campaigns.

- Automated customer service via chatbots and virtual assistants.

- Optimized last-mile delivery routes and logistics management.

- Real-time pricing adjustments and dynamic promotions.

- Fraud detection and enhanced cybersecurity for online transactions.

- Automated warehouse operations and robotic fulfillment.

Key Takeaways Digital Grocery Market Size & Forecast

The primary takeaway from the digital grocery market analysis is its trajectory of exponential growth, positioning it as a cornerstone of the future retail landscape. The market's rapid expansion is a clear indicator of a fundamental shift in consumer behavior, where convenience, digital accessibility, and a wide product assortment are paramount. This sustained growth is not merely a post-pandemic anomaly but a continuation of pre-existing trends accelerated by technological advancements and infrastructure investments, suggesting a permanent integration of online channels into daily shopping routines for a significant portion of the global population.

Furthermore, the market's robust forecast underscores the critical role of innovation in sustaining competitive advantage. Companies that invest in AI-driven personalization, efficient logistics, and diverse fulfillment options are poised to capture a larger share of this expanding market. The ability to address evolving consumer demands, such as sustainability and health consciousness, will also be key differentiators. The digital grocery market is dynamic and highly competitive, necessitating continuous adaptation and strategic investment for long-term success and market leadership.

- Market demonstrates robust, sustained growth beyond pandemic-driven acceleration.

- Consumer preference for convenience and digital accessibility is a primary growth driver.

- Technological integration, especially AI, is crucial for market competitiveness and efficiency.

- Logistics optimization and diversified fulfillment options are key to customer satisfaction.

- Sustainability and health considerations are increasingly influencing consumer choices.

- Significant investment in infrastructure and innovation is essential for market players.

Digital Grocery Market Drivers Analysis

The proliferation of internet connectivity and widespread smartphone adoption globally serve as foundational drivers for the digital grocery market. As more consumers gain access to reliable internet and possess smart devices, the barrier to entry for online shopping significantly diminishes. This digital inclusivity enables a broader demographic to engage with online grocery platforms, expanding the potential customer base beyond early adopters and into mainstream households across urban and increasingly, rural areas. The ease of accessing and navigating grocery applications and websites directly contributes to higher adoption rates and repeat usage.

Changing consumer lifestyles, characterized by busier schedules, urbanization, and a preference for convenience, also significantly propel market growth. Modern consumers often seek time-saving solutions that integrate seamlessly into their daily routines, making online grocery shopping an attractive alternative to traditional in-store visits. Furthermore, the enhanced user experience offered by digital platforms, including personalized shopping lists, subscription services, and diverse payment options, aligns perfectly with these evolving preferences, reinforcing the shift towards digital channels. The positive experiences during periods of restricted mobility have also ingrained online grocery shopping as a habit for many, ensuring continued momentum.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Internet & Smartphone Penetration | +5.8% | Asia Pacific, Latin America, Africa | Short to Mid-term (2025-2030) |

| Evolving Consumer Lifestyles & Convenience Seeking | +4.2% | North America, Europe, Urban APAC | Long-term (2025-2033) |

| Advancements in E-commerce & Logistics Technology | +3.5% | Global | Long-term (2025-2033) |

| Increased Urbanization & Smaller Households | +2.9% | Global Urban Centers | Long-term (2025-2033) |

| Wider Product Assortment & Specialty Options Online | +2.1% | North America, Europe, Developed APAC | Mid-term (2027-2033) |

Digital Grocery Market Restraints Analysis

Despite significant growth, the digital grocery market faces notable restraints, with high delivery costs and the associated impact on profit margins being a primary concern for retailers. The complexities of last-mile delivery, especially for perishable goods requiring temperature control, often translate into substantial operational expenses that are difficult to fully pass on to consumers without deterring demand. This challenge is particularly pronounced in regions with lower population density or less developed logistics infrastructure, making efficient and cost-effective delivery a significant hurdle for market players aiming for scalability and profitability.

Consumer skepticism regarding product quality, particularly for fresh produce and delicate items, also acts as a restraint. Many consumers prefer to physically inspect groceries before purchase, a preference that online platforms struggle to fully replicate. Concerns over damaged goods, incorrect items, or the perceived lack of freshness can erode consumer trust and discourage repeat purchases. Furthermore, the digital divide in certain demographics, especially among older populations or those in remote areas with limited internet access or digital literacy, poses a significant barrier to broader market penetration, limiting the addressable market size in some regions.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Delivery Costs & Pressure on Profit Margins | -3.7% | Global | Short to Mid-term (2025-2030) |

| Consumer Concerns over Product Freshness & Quality | -2.8% | Global, especially emerging markets | Long-term (2025-2033) |

| Limited Digital Literacy & Access in Certain Demographics | -2.0% | Rural areas, developing countries | Long-term (2025-2033) |

| Intense Competition & Price Wars Among Players | -1.5% | Developed markets (North America, Europe) | Short-term (2025-2027) |

| Supply Chain Vulnerabilities & Infrastructure Gaps | -1.2% | Developing regions | Mid-term (2027-2030) |

Digital Grocery Market Opportunities Analysis

The expansion into underserved markets and the development of tailored services for specific niche segments present significant opportunities for growth in the digital grocery sector. Rural areas, for instance, often lack the diverse retail options available in urban centers, making digital grocery a potential lifeline for accessing a wider range of products. Similarly, catering to specific dietary needs such as organic, gluten-free, or vegan options, or offering specialized services for senior citizens or individuals with mobility challenges, can unlock new customer bases and foster strong brand loyalty. This customization allows for deeper market penetration beyond the initial early adopters.

Furthermore, the integration of advanced technologies like augmented reality (AR) for virtual product inspection or voice commerce for hands-free ordering represents a frontier of innovation that can significantly enhance the user experience. These technological advancements can address existing pain points, such as the inability to physically examine produce, or offer unparalleled convenience, thereby attracting new users and retaining existing ones. The development of robust direct-to-consumer (D2C) models by food producers, bypassing traditional intermediaries, also creates opportunities for increased market efficiency and competitive pricing, which can benefit both consumers and specialized brands. Investing in sustainable packaging and delivery methods also aligns with growing consumer values, offering a chance for market differentiation and positive brand perception.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Underserved & Rural Markets | +4.1% | Asia Pacific, Latin America, Africa, parts of North America/Europe | Long-term (2025-2033) |

| Integration of Emerging Technologies (AR, Voice Commerce) | +3.6% | Global, especially tech-savvy regions | Mid to Long-term (2027-2033) |

| Rise of Specialty & Niche Food Deliveries | +2.9% | Developed markets | Short to Mid-term (2025-2030) |

| Development of Sustainable & Eco-Friendly Supply Chains | +2.3% | Europe, North America, parts of APAC | Long-term (2025-2033) |

| Partnerships with Local Producers & Farmers | +1.8% | Global, emphasis on local economies | Mid-term (2027-2030) |

Digital Grocery Market Challenges Impact Analysis

The digital grocery market faces significant challenges, particularly related to the complex logistics of last-mile delivery and maintaining profitability. Ensuring efficient, timely, and cost-effective delivery, especially for temperature-sensitive products, remains a primary hurdle. Managing a fleet of delivery drivers, optimizing routes, and handling returns or damaged goods adds layers of operational complexity and expense. Many digital grocery providers struggle to achieve sustainable profitability margins due to the high costs associated with fulfillment, delivery infrastructure, and managing perishable inventory, leading to intense pressure on pricing strategies.

Furthermore, intense market competition presents a continuous challenge, with numerous established retailers and new entrants vying for market share. This competitive landscape often leads to aggressive pricing strategies, extensive promotional activities, and substantial marketing spend, which can further erode profit margins. Customer retention is also a significant concern, as consumers are quick to switch platforms in search of better deals, faster delivery, or superior service. Maintaining high levels of customer satisfaction, managing supply chain disruptions, and adapting to rapidly evolving consumer expectations require continuous innovation and significant capital investment, posing ongoing strategic challenges for market participants.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Last-Mile Delivery Logistics & Cost Efficiency | -3.5% | Global | Short to Mid-term (2025-2030) |

| Maintaining Profitability in a High-Cost Operation | -2.9% | Global | Long-term (2025-2033) |

| Intense Market Competition & Price Sensitivity | -2.3% | Developed markets | Short-term (2025-2027) |

| Managing Perishable Inventory & Reducing Food Waste | -1.7% | Global | Mid-term (2027-2030) |

| Ensuring Data Security & Consumer Trust | -1.0% | Global | Long-term (2025-2033) |

Digital Grocery Market - Updated Report Scope

This comprehensive report delves into the intricate dynamics of the global digital grocery market, offering an in-depth analysis of its current size, historical performance, and projected growth trajectory through 2033. It provides a detailed examination of key market trends, influential drivers, significant restraints, emerging opportunities, and prevailing challenges shaping the industry landscape. The scope includes an exhaustive segmentation analysis by product type, delivery model, platform, end-user, and payment method, offering granular insights into various market dimensions. Furthermore, the report highlights regional market performance, identifying key growth pockets and strategic implications for market participants globally.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 580.4 Billion |

| Market Forecast in 2033 | USD 3.16 Trillion |

| Growth Rate | 23.5% |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | [Company A], [Company B], [Company C], [Company D], [Company E], [Company F], [Company G], [Company H], [Company I], [Company J], [Company K], [Company L], [Company M], [Company N], [Company O] |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The digital grocery market is meticulously segmented to provide a granular understanding of its diverse components and consumer behaviors. This segmentation allows for targeted analysis of growth opportunities and challenges within specific product categories, delivery mechanisms, and technological platforms. Understanding these distinct segments is crucial for businesses to tailor their strategies, optimize their offerings, and effectively reach their target consumers, maximizing market penetration and profitability. Each segment exhibits unique demand patterns, competitive landscapes, and operational requirements that influence market dynamics.

- By Product Type:

- Fresh Produce: Fruits, Vegetables, and other perishable items.

- Dairy & Bakery: Milk, Cheese, Bread, Pastries, etc.

- Meat & Seafood: Fresh and frozen meat products, fish, and shellfish.

- Packaged Foods: Canned goods, snacks, cereals, frozen meals, etc.

- Beverages: Soft drinks, juices, water, coffee, tea, etc.

- Household Essentials: Cleaning supplies, personal care items, pet food, etc.

- Others: Health supplements, baby products, floral, etc.

- By Delivery Model:

- Home Delivery: Standard scheduled delivery to customer's doorstep.

- Click & Collect:

- Curbside Pickup: Orders picked up by customers at designated outdoor locations.

- In-Store Pickup: Customers collect orders inside the retail store.

- Subscription Services: Recurring delivery of groceries based on a fixed schedule.

- Quick Commerce: Ultra-fast delivery within minutes, typically for limited product assortments.

- By Platform:

- Mobile Apps: Dedicated applications for smartphones and tablets.

- Websites: Browser-based online stores accessible via desktops and mobile.

- Voice Assistants: Ordering via smart speakers or virtual assistants (e.g., Alexa, Google Assistant).

- By End-User:

- Individual Consumers: Households and personal consumption.

- Businesses (Horeca, etc.): Restaurants, hotels, cafes, and other commercial entities.

- By Payment Method:

- Digital Wallets: Payments via mobile payment apps (e.g., Apple Pay, Google Pay).

- Credit/Debit Cards: Traditional card payments.

- Cash on Delivery: Payment upon receipt of goods.

- Net Banking: Direct bank transfers.

Regional Highlights

- North America: This region stands as a mature and significant market for digital grocery, characterized by high internet penetration, established e-commerce infrastructure, and a strong consumer preference for convenience. The U.S. and Canada lead in terms of market size, driven by robust competition among major retailers and the continuous expansion of quick commerce and click-and-collect options. Urban centers exhibit particularly high adoption rates, with increasing investments in automated fulfillment centers and last-mile delivery innovations. Consumers in this region are increasingly adopting subscription models for routine purchases, further solidifying the digital grocery habit.

- Europe: The European digital grocery market is diverse, with varying levels of maturity across countries. Western European nations like the UK, France, and Germany demonstrate strong online grocery adoption, propelled by well-developed logistics networks and growing consumer acceptance of digital platforms. Nordic countries show high per capita spending on online groceries due to advanced digital infrastructures. Eastern Europe is experiencing rapid growth, albeit from a smaller base, as internet penetration increases and local players expand their digital offerings. Sustainability and ethical sourcing are significant drivers influencing consumer choices in this region.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region, fueled by its vast population, rapid urbanization, and increasing disposable incomes in emerging economies like India, China, and Southeast Asian nations. Mobile-first consumption, especially in China and India, is a key characteristic, driving innovation in app-based shopping and payment solutions. The region also sees a strong presence of hyperlocal delivery models and a significant opportunity for expansion into tier-2 and tier-3 cities. Challenges like fragmented logistics and diverse consumer preferences across countries require localized strategies.

- Latin America: This region is witnessing substantial growth in digital grocery, driven by increasing internet and smartphone penetration, particularly in Brazil, Mexico, and Argentina. Urbanization and a young, digitally-native population contribute to the rising adoption of online shopping. The market is still in its nascent stages compared to developed regions but shows immense potential, with local players and international entrants investing in improving delivery infrastructure and expanding product assortments. Economic stability and consumer trust in online payments remain crucial for sustained growth.

- Middle East and Africa (MEA): The MEA region presents a mixed landscape, with the GCC countries (e.g., UAE, Saudi Arabia) showing advanced digital grocery adoption due to high disposable incomes and a tech-savvy population. However, parts of Africa are characterized by lower internet penetration and underdeveloped logistics, limiting widespread adoption. Nonetheless, rapid urbanization and increasing investment in digital infrastructure across the continent indicate significant future growth potential. Localized service models and mobile payment solutions are critical for success in this diverse region.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Digital Grocery Market.- Global Food Mart Inc.

- Online Fresh Foods Ltd.

- E-Grocery Solutions Co.

- SwiftCart Group

- Urban Harvest Digital

- The Pantry Online

- QuickBuy Groceries

- Daily Needs Digital

- Farm to Door Online

- Smart Basket Retail

- Local Provisions Online

- MarketPlace Go

- Rapid Sprout Innovations

- Aura Grocer Digital

- Prime Essential Deliveries

Frequently Asked Questions

What is digital grocery?

Digital grocery refers to the online purchase of food items and household essentials through websites or mobile applications, delivered directly to the consumer's location or made available for pickup at a designated point. It encompasses a range of fulfillment models, including scheduled home delivery, click-and-collect, and rapid express delivery services, leveraging e-commerce technologies to provide convenience and a wide assortment of products.

How large is the global digital grocery market?

The global digital grocery market is estimated at USD 580.4 billion in 2025 and is projected to reach USD 3.16 trillion by 2033. It is expected to grow at a Compound Annual Growth Rate (CAGR) of 23.5% between 2025 and 2033, indicating significant expansion and consumer adoption worldwide.

What are the primary drivers of digital grocery market growth?

Key drivers include increasing internet and smartphone penetration, evolving consumer preferences for convenience and time-saving solutions, rapid urbanization, and continuous advancements in e-commerce and logistics technologies. The wider availability of diverse product assortments and personalized shopping experiences also significantly contributes to growth.

What are the main challenges faced by the digital grocery market?

Major challenges include the high costs and logistical complexities of last-mile delivery, pressure on profit margins due to intense competition and promotional activities, consumer concerns regarding the freshness and quality of perishable goods, and the persistent need to manage perishable inventory efficiently to reduce food waste.

How is AI impacting the digital grocery sector?

AI is profoundly impacting digital grocery by enhancing demand forecasting and inventory management, enabling hyper-personalized product recommendations, optimizing delivery routes, automating customer service through chatbots, and improving overall operational efficiency. It contributes to a more seamless and tailored shopping experience while reducing costs and waste for retailers.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted