Diesel Industrial Engine Market

Diesel Industrial Engine Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701141 | Last Updated : July 29, 2025 |

Format : ![]()

![]()

![]()

![]()

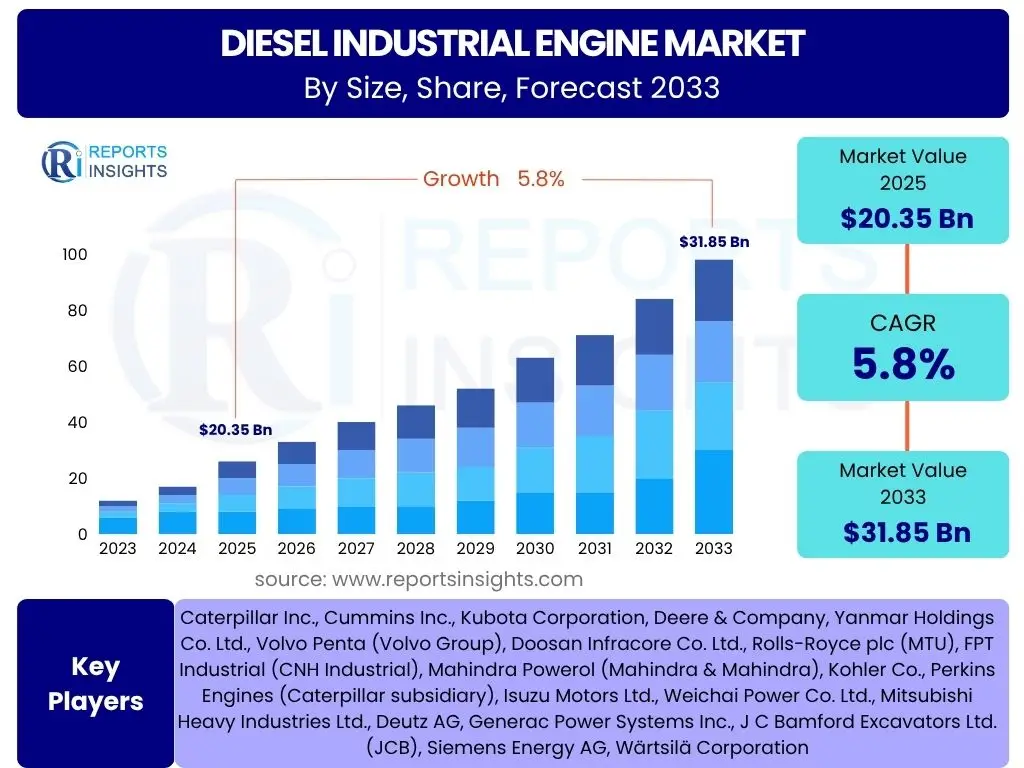

Diesel Industrial Engine Market Size

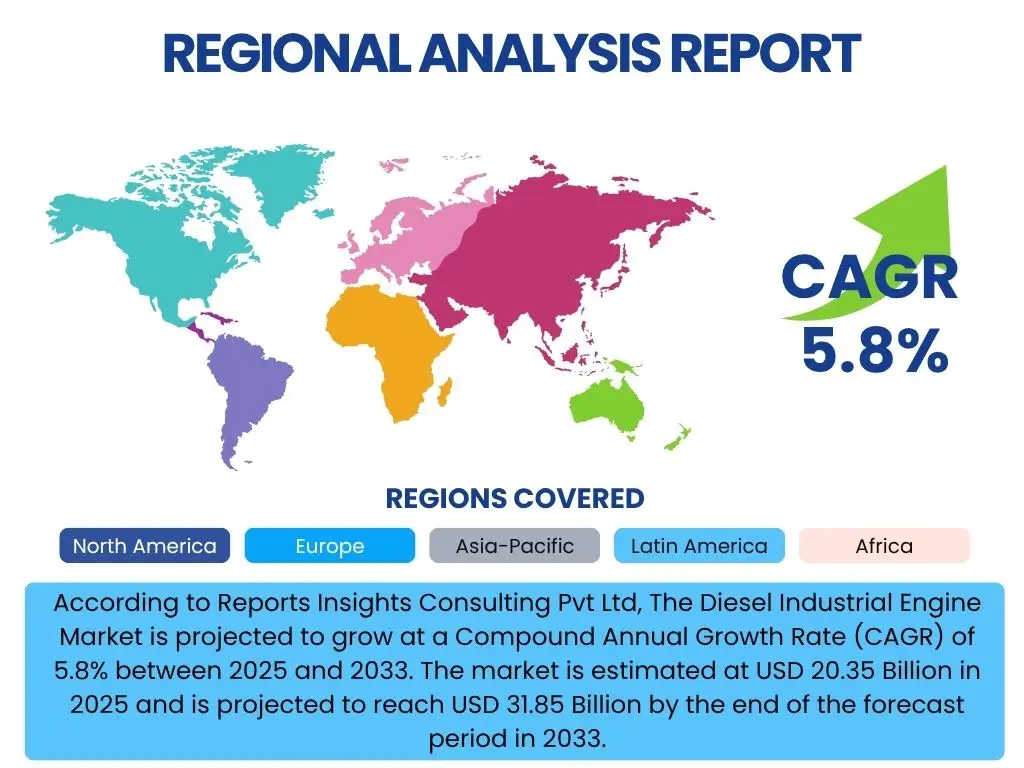

According to Reports Insights Consulting Pvt Ltd, The Diesel Industrial Engine Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 20.35 Billion in 2025 and is projected to reach USD 31.85 Billion by the end of the forecast period in 2033.

Key Diesel Industrial Engine Market Trends & Insights

The Diesel Industrial Engine market is currently experiencing significant transformative shifts driven by global sustainability initiatives, technological advancements, and evolving operational demands across various sectors. Market participants are increasingly focusing on developing engines that not only meet stringent emission standards but also offer enhanced fuel efficiency and operational longevity. This focus is leading to innovations in engine design, material science, and digital integration. Furthermore, the burgeoning demand for reliable power solutions in construction, mining, agriculture, and power generation continues to underscore the critical role of diesel industrial engines, despite the growing discourse around alternative energy sources.

A notable trend involves the hybridization of diesel engines with electric power, aiming to reduce emissions and improve fuel economy, particularly in stop-start applications or where silent operation is occasionally required. The shift towards greater connectivity and telematics in engine management systems is also prominent, allowing for real-time monitoring, predictive maintenance, and optimized performance. This connectivity is vital for maximizing uptime and reducing operational costs for end-users. Additionally, the increasing demand for compact and high-power-density engines, especially for space-constrained applications, is influencing product development and design strategies across the industry.

- Stringent emission regulations driving engine technology advancements.

- Growing adoption of telematics and IoT for enhanced engine monitoring and predictive maintenance.

- Increased focus on fuel efficiency and reduced operational costs.

- Development of hybrid diesel-electric power solutions for various industrial applications.

- Rising demand for compact and high-power-density engines.

AI Impact Analysis on Diesel Industrial Engine

The integration of Artificial Intelligence (AI) into the Diesel Industrial Engine sector is poised to revolutionize operational efficiencies, maintenance protocols, and overall performance optimization. Users frequently inquire about how AI can enhance engine reliability and reduce downtime, a critical concern for industries relying on continuous operation. AI algorithms, leveraging vast datasets from engine sensors, can identify subtle anomalies and predict potential component failures long before they escalate, transitioning maintenance from reactive to predictive. This proactive approach significantly minimizes unexpected breakdowns, extends engine lifespan, and lowers total cost of ownership, addressing key user priorities regarding operational continuity and cost-effectiveness.

Furthermore, AI plays a pivotal role in optimizing fuel consumption and emissions management, directly responding to user demand for more sustainable and economical engine solutions. Through real-time data analysis, AI can dynamically adjust engine parameters—such as fuel injection timing and air-fuel mixtures—to achieve optimal combustion efficiency under varying load conditions. This not only leads to significant fuel savings but also helps engines comply with increasingly strict environmental regulations by minimizing pollutant output. While concerns about data security and the complexity of AI integration exist among users, the overwhelming consensus points towards AI as a fundamental technology for futureproofing diesel industrial engines, making them smarter, more efficient, and environmentally responsible.

- Predictive maintenance and fault detection through real-time data analysis.

- Optimized fuel efficiency and emissions control via dynamic engine parameter adjustments.

- Enhanced operational insights and remote diagnostics capabilities.

- Automation of routine checks and performance tuning.

- Development of self-learning engine management systems for adaptive performance.

Key Takeaways Diesel Industrial Engine Market Size & Forecast

The Diesel Industrial Engine market is demonstrating resilient growth, driven by sustained demand from critical sectors such as construction, mining, agriculture, and power generation. A primary takeaway is the market's continuous adaptation to evolving environmental regulations, with significant investments in cleaner engine technologies and alternative fuel compatibility. This proactive approach ensures the enduring relevance of diesel power in industrial applications, particularly where high power output, durability, and robust performance are paramount, aligning with user expectations for reliable and compliant solutions.

Another crucial insight is the accelerating pace of technological integration, including advanced telematics, AI-driven diagnostics, and hybridization. These innovations are not merely incremental improvements but represent a fundamental shift towards smarter, more efficient, and connected industrial engines. This trend directly addresses user needs for reduced operational costs, increased uptime, and enhanced asset management. The market forecast underscores a steady expansion, indicating that while alternative energy sources are gaining traction, the unique advantages of diesel engines in demanding industrial environments will ensure their prominent position for the foreseeable future.

- Consistent market growth projected, driven by core industrial applications.

- Regulatory compliance and technological innovation are central to market evolution.

- Increasing integration of smart technologies (AI, IoT) for performance optimization.

- Emphasis on fuel efficiency and reduced emissions as key competitive differentiators.

- Strong demand from emerging economies fueling market expansion.

Diesel Industrial Engine Market Drivers Analysis

The global Diesel Industrial Engine market is primarily propelled by robust expansion in key end-use industries and the persistent demand for reliable, high-power energy solutions. Significant investments in infrastructure development, particularly in emerging economies, are fueling the need for heavy construction machinery, which predominantly relies on diesel engines. Similarly, the growing global population and urbanization trends necessitate increased output from the agricultural and mining sectors, further stimulating the demand for high-capacity equipment powered by industrial diesel engines. These foundational industrial activities are not only expanding in scale but also intensifying in operational complexity, requiring the dependable performance characteristics inherent to diesel powerplants.

Moreover, the increasing demand for uninterrupted power generation, especially in regions with unstable grid infrastructure or for critical backup applications, serves as a significant market driver. Diesel generators remain a preferred choice due to their rapid start-up capabilities, fuel accessibility, and proven reliability in diverse environmental conditions. Technological advancements enhancing fuel efficiency, durability, and lower maintenance requirements also contribute to the market's momentum by improving the overall cost-effectiveness and operational appeal of modern diesel engines. The integration of advanced diagnostics and telematics further adds value, enabling predictive maintenance and optimizing operational uptime, which are critical factors for industrial operators seeking maximum productivity.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Infrastructure Development & Construction Boom | +1.5-2.0% | APAC, Latin America, Middle East, Africa | Mid-term (3-6 years) |

| Growth in Mining & Agricultural Industries | +1.2-1.8% | North America, APAC, Africa | Mid-term (3-6 years) |

| Rising Demand for Backup Power Generation | +0.8-1.3% | Global, particularly emerging markets | Short-term (0-3 years) |

| Technological Advancements in Engine Efficiency & Durability | +0.7-1.0% | Global | Long-term (6+ years) |

| Expansion of Industrialization in Developing Economies | +1.0-1.5% | APAC, Africa, Latin America | Mid-term (3-6 years) |

Diesel Industrial Engine Market Restraints Analysis

The Diesel Industrial Engine market faces significant restraints primarily due to increasingly stringent global emission regulations and the growing environmental consciousness pushing for cleaner energy alternatives. Governments worldwide are imposing stricter limits on pollutants like nitrogen oxides (NOx) and particulate matter (PM), necessitating substantial investments in advanced exhaust after-treatment systems. While these technologies improve environmental performance, they also increase the manufacturing cost and operational complexity of diesel engines, which can deter some buyers, particularly in cost-sensitive applications. This regulatory pressure is a continuous challenge, requiring manufacturers to constantly innovate and adapt, potentially slowing market adoption in certain segments.

Furthermore, the accelerating shift towards electrification and the development of alternative fuel technologies, such as hydrogen fuel cells and battery-electric power, pose a long-term threat to the dominance of diesel engines. Although these alternatives are not yet universally viable for all heavy-duty industrial applications, ongoing research and development, coupled with supportive government policies and declining battery costs, are gradually expanding their applicability. Additionally, the volatile nature of global crude oil prices can impact the operational costs for end-users, making diesel engines less attractive compared to alternatives when fuel prices are high. Supply chain disruptions and geopolitical instabilities can also affect raw material availability and production, adding to the market's challenges.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Global Emission Regulations (e.g., Euro V, Tier 4 Final) | -1.0-1.5% | North America, Europe, China, India | Short-term (0-3 years) |

| Increasing Adoption of Electric & Alternative Fuel Technologies | -0.8-1.2% | Global, especially developed economies | Mid-term (3-6 years) |

| Volatile Fuel Prices & High Operating Costs | -0.5-0.8% | Global | Short-term (0-3 years) |

| High Initial Investment & Maintenance Complexity | -0.3-0.6% | Global | Short-term (0-3 years) |

| Supply Chain Disruptions & Geopolitical Instability | -0.4-0.7% | Global | Short-term (0-3 years) |

Diesel Industrial Engine Market Opportunities Analysis

The Diesel Industrial Engine market presents significant opportunities for growth and innovation, particularly through the development of hybrid power systems and the integration of advanced digital technologies. The burgeoning rental equipment market offers a substantial avenue for growth, as construction, agriculture, and other industrial sectors increasingly opt for rental models to manage capital expenditure and operational flexibility. This trend drives consistent demand for new, efficient, and technologically advanced diesel engines to power diverse machinery. Furthermore, the expansion into specialized applications, such as data centers requiring robust backup power, and marine propulsion systems, provides niche but high-value opportunities for manufacturers capable of customization and high performance.

Developing economies, especially in Asia Pacific, Africa, and Latin America, represent immense untapped potential due to ongoing industrialization, urbanization, and infrastructure development projects. These regions often lack extensive grid infrastructure, making reliable, self-contained power sources like diesel engines indispensable. Moreover, continuous innovation in engine design, focusing on modularity, enhanced connectivity, and compatibility with various biofuels, opens new markets and applications. Partnerships with technology providers to integrate IoT, AI, and telematics solutions can further unlock value by offering advanced predictive maintenance, remote diagnostics, and performance optimization services, thereby differentiating products and creating new revenue streams for engine manufacturers.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in the Rental Equipment Market | +0.9-1.3% | Global, particularly North America & Europe | Mid-term (3-6 years) |

| Development of Hybrid Diesel-Electric Systems | +0.7-1.1% | Global | Long-term (6+ years) |

| Expansion into Niche & Specialized Applications (e.g., Data Centers) | +0.5-0.9% | North America, Europe, APAC | Mid-term (3-6 years) |

| Market Penetration in Developing Economies | +1.0-1.5% | APAC, Africa, Latin America | Long-term (6+ years) |

| Integration of IoT, AI, and Advanced Telematics | +0.8-1.2% | Global | Mid-term (3-6 years) |

Diesel Industrial Engine Market Challenges Impact Analysis

The Diesel Industrial Engine market faces significant challenges primarily stemming from the global imperative for decarbonization and the associated regulatory pressures. The transition towards a low-carbon economy pushes industries to explore alternatives to fossil fuels, placing diesel engines under scrutiny despite their proven reliability and power density. This creates a complex environment for manufacturers, who must balance the need for continuous innovation in diesel technology with the increasing demand for, and investment in, cleaner energy solutions. Adapting to diverse and evolving regional emission standards also presents a considerable technical and financial hurdle, necessitating costly research, development, and compliance efforts.

Furthermore, a notable challenge is the skilled labor shortage in manufacturing, maintenance, and operation of advanced diesel engines. As engines become more sophisticated with integrated electronics and complex after-treatment systems, there is a growing need for specialized technicians and engineers, which can be difficult to source and retain. Geopolitical instability and trade disputes can also disrupt global supply chains, affecting the availability and cost of critical components, leading to production delays and increased operational expenses. The ongoing competitive pressure from emerging alternative power sources, while also an opportunity, necessitates substantial investment in R&D to maintain diesel's competitive edge and adapt to future energy landscapes.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Transition to Cleaner Energy Sources & Decarbonization Targets | -1.2-1.8% | Global | Long-term (6+ years) |

| Skilled Labor Shortage for Advanced Engine Technologies | -0.6-1.0% | North America, Europe, Developed APAC | Mid-term (3-6 years) |

| Geopolitical Instability & Supply Chain Vulnerabilities | -0.7-1.1% | Global | Short-term (0-3 years) |

| High R&D Costs for Emission Compliance & New Technologies | -0.5-0.9% | Global | Mid-term (3-6 years) |

| Public Perception & Environmental Lobbying Against Diesel | -0.4-0.8% | Europe, North America | Mid-term (3-6 years) |

Diesel Industrial Engine Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Diesel Industrial Engine Market, encompassing historical data from 2019 to 2023, current market estimations for 2024, and detailed forecasts spanning 2025 to 2033. The scope includes a thorough examination of market size, growth drivers, restraints, opportunities, and challenges influencing industry dynamics. Key market trends, including technological advancements, regulatory impacts, and competitive landscape analysis, are meticulously assessed to offer actionable insights. Furthermore, the report delves into detailed market segmentation by various attributes such as power output, end-use application, and engine type, alongside a robust regional analysis covering major global geographies.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 20.35 Billion |

| Market Forecast in 2033 | USD 31.85 Billion |

| Growth Rate | 5.8% CAGR |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Caterpillar Inc., Cummins Inc., Kubota Corporation, Deere & Company, Yanmar Holdings Co. Ltd., Volvo Penta (Volvo Group), Doosan Infracore Co. Ltd., Rolls-Royce plc (MTU), FPT Industrial (CNH Industrial), Mahindra Powerol (Mahindra & Mahindra), Kohler Co., Perkins Engines (Caterpillar subsidiary), Isuzu Motors Ltd., Weichai Power Co. Ltd., Mitsubishi Heavy Industries Ltd., Deutz AG, Generac Power Systems Inc., J C Bamford Excavators Ltd. (JCB), Siemens Energy AG, Wärtsilä Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Diesel Industrial Engine market is comprehensively segmented to provide granular insights into its diverse applications and operational characteristics. This segmentation allows for a detailed understanding of demand patterns across various power requirements and end-use industries, facilitating strategic decision-making for market participants. The division by power output reflects the varied needs from light-duty industrial equipment to heavy-duty machinery and large-scale power generation units, indicating specific technological requirements and market niches. Meanwhile, application-based segmentation highlights the primary sectors driving demand, from the earth-moving equipment in construction and mining to the critical backup power systems in commercial and industrial settings. This multi-dimensional analysis underscores the broad utility and adaptability of diesel industrial engines across the global economy.

- By Power Output: This segment delineates engines based on their horsepower ratings, catering to distinct industrial needs.

- Below 100 HP: Typically used in smaller construction equipment, agricultural machinery, and compact generators.

- 100-500 HP: Common in medium-duty construction equipment, agricultural tractors, and mid-sized power generation units.

- 500-1000 HP: Utilized in heavy construction machinery, large mining equipment, and substantial power generation applications.

- Above 1000 HP: Primarily found in very heavy-duty mining trucks, large marine vessels, and extensive industrial power plants.

- By Application: Categorizes the market based on the primary industries where these engines are employed.

- Construction: Earthmoving equipment, excavators, loaders, bulldozers, road construction machinery.

- Mining: Haul trucks, excavators, drills, loaders used in surface and underground mining.

- Agriculture: Tractors, harvesters, irrigation pumps, and other farm machinery.

- Power Generation (Gensets): Standby, prime, and continuous power solutions for commercial, industrial, and residential use.

- Oil & Gas: Drilling rigs, pumps, compressors, and auxiliary power for upstream and downstream operations.

- Marine: Propulsion and auxiliary power for commercial vessels, workboats, and pleasure crafts.

- Industrial & Manufacturing: Various industrial processes requiring reliable power, such as material handling and processing.

- Others: Includes diverse applications such as material handling, airport ground support equipment, and railway locomotives.

- By End-Use: Distinguishes between engines sold directly to equipment manufacturers and those sold for replacement or maintenance purposes.

- OEM (Original Equipment Manufacturer): Engines integrated into new machinery by equipment manufacturers.

- Aftermarket: Engines sold for replacement, repair, or upgrade in existing equipment.

- By Engine Type: Classifies engines based on their operational cycle.

- 2-Stroke Engine: Typically found in specific marine or smaller high-power applications.

- 4-Stroke Engine: Dominant in most industrial applications due to efficiency and emissions performance.

Regional Highlights

- North America: This region maintains a mature yet robust market, driven by significant investments in infrastructure upgrades, particularly in the United States and Canada. Stringent emission regulations here lead to high demand for technologically advanced and compliant engines. The strong agricultural and construction sectors, coupled with a developed rental equipment market, sustain consistent demand for diesel industrial engines, focusing on efficiency and connectivity.

- Europe: Europe is characterized by strict environmental regulations (e.g., Euro V, Stage V) which necessitate continuous innovation in engine design, particularly regarding emissions reduction and fuel efficiency. The region is a hub for R&D in hybrid and alternative fuel technologies, influencing the direction of diesel engine development. Strong markets in construction, agriculture, and manufacturing, especially in Germany, France, and the UK, contribute significantly to market revenue.

- Asia Pacific (APAC): APAC is the fastest-growing market for diesel industrial engines, propelled by rapid industrialization, urbanization, and large-scale infrastructure projects across countries like China, India, and Southeast Asian nations. The region's expanding mining and agricultural sectors, coupled with increasing demand for reliable power generation in developing areas, fuel substantial market growth, though cost-effectiveness often remains a key purchasing criterion.

- Latin America: This region demonstrates steady growth, primarily driven by expanding mining activities in countries like Brazil, Chile, and Peru, as well as ongoing infrastructure development projects. The agricultural sector also plays a vital role, especially in Brazil and Argentina. Demand here is often influenced by economic stability and commodity prices, with a focus on durable and high-performing engines suitable for challenging operational environments.

- Middle East and Africa (MEA): The MEA region exhibits significant potential, particularly due to investments in oil and gas infrastructure, construction projects, and the persistent need for reliable power generation solutions in energy-deficient areas. Countries in the GCC (Gulf Cooperation Council) are experiencing construction booms, while parts of Africa are undergoing industrialization, driving the demand for both new and used diesel industrial engines.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Diesel Industrial Engine Market.- Caterpillar Inc.

- Cummins Inc.

- Kubota Corporation

- Deere & Company

- Yanmar Holdings Co. Ltd.

- Volvo Penta (Volvo Group)

- Doosan Infracore Co. Ltd.

- Rolls-Royce plc (MTU)

- FPT Industrial (CNH Industrial)

- Mahindra Powerol (Mahindra & Mahindra)

- Kohler Co.

- Perkins Engines (Caterpillar subsidiary)

- Isuzu Motors Ltd.

- Weichai Power Co. Ltd.

- Mitsubishi Heavy Industries Ltd.

- Deutz AG

- Generac Power Systems Inc.

- J C Bamford Excavators Ltd. (JCB)

- Siemens Energy AG

- Wärtsilä Corporation

Frequently Asked Questions

Analyze common user questions about the Diesel Industrial Engine market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the forecast growth rate for the Diesel Industrial Engine Market?

The Diesel Industrial Engine Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033, reaching an estimated USD 31.85 Billion by 2033 from USD 20.35 Billion in 2025.

What are the primary drivers of growth in the Diesel Industrial Engine Market?

Key drivers include robust global infrastructure development, expansion in the construction, mining, and agricultural sectors, and increasing demand for reliable backup power generation, particularly in emerging economies.

How do emission regulations impact the Diesel Industrial Engine Market?

Strict global emission regulations (e.g., Euro V, Tier 4 Final) significantly influence the market by driving manufacturers to invest heavily in advanced technologies for reduced pollutants, which can increase engine cost and complexity but also fosters innovation.

What role does Artificial Intelligence (AI) play in modern industrial diesel engines?

AI is increasingly integrated into industrial diesel engines for predictive maintenance, optimizing fuel efficiency through dynamic parameter adjustments, enhancing diagnostic capabilities, and facilitating remote monitoring to improve operational uptime and reduce costs.

Which regions are leading the Diesel Industrial Engine Market, and why?

Asia Pacific (APAC) is the fastest-growing region due to rapid industrialization and large-scale infrastructure projects, while North America and Europe remain significant markets driven by technologically advanced engine demand and established industrial bases, albeit with stringent regulatory landscapes.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted