Diesel Engine Turbocharger Market

Diesel Engine Turbocharger Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700529 | Last Updated : July 25, 2025 |

Format : ![]()

![]()

![]()

![]()

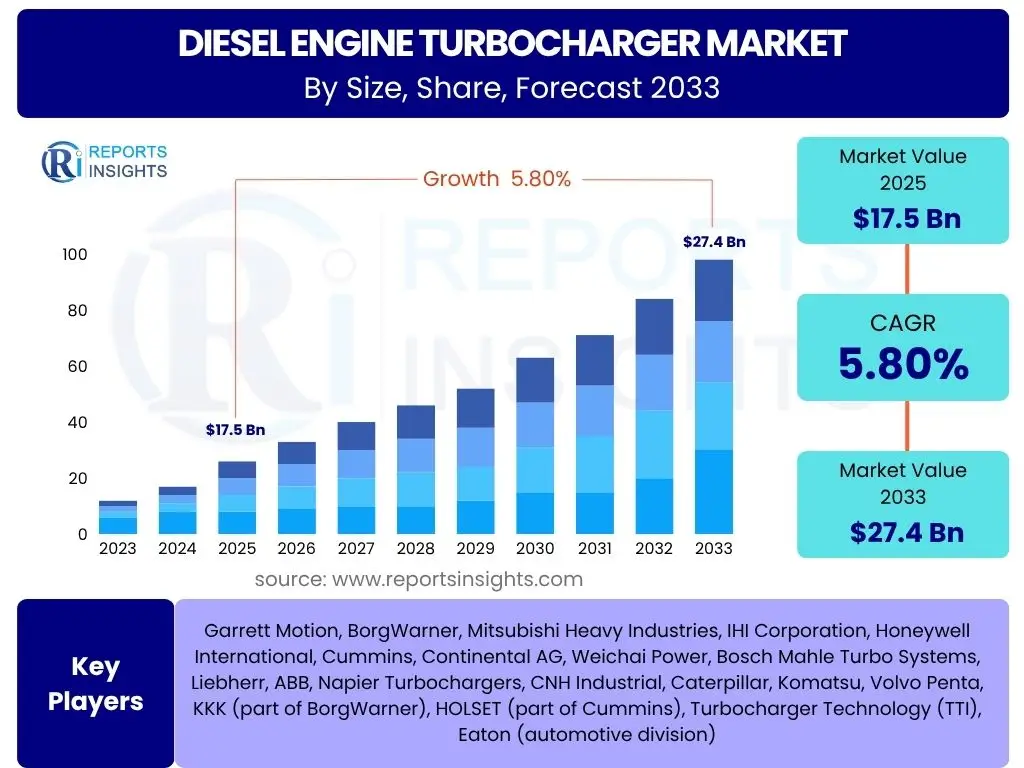

Diesel Engine Turbocharger Market Size

Diesel Engine Turbocharger Market is projected to grow at a Compound annual growth rate (CAGR) of 5.8% between 2025 and 2033, reaching USD 17.5 billion in 2025 and is projected to grow to USD 27.4 billion by 2033 the end of the forecast period.

Key Diesel Engine Turbocharger Market Trends & Insights

The Diesel Engine Turbocharger Market is undergoing significant evolution driven by several key trends; increasing demand for fuel-efficient and low-emission engines across commercial vehicles and industrial machinery; advancements in turbocharger technology enhancing performance and durability; the growing adoption of variable geometry turbochargers and electric turbochargers for optimal power delivery; stringent global emission regulations driving innovation in exhaust gas recirculation (EGR) and selective catalytic reduction (SCR) compatible solutions; and the expanding aftermarket for turbocharger maintenance and replacement services reflecting a large installed base.

AI Impact Analysis on Diesel Engine Turbocharger

Artificial Intelligence (AI) is set to significantly influence the Diesel Engine Turbocharger Market; predictive maintenance models leveraging AI for early fault detection and reduced downtime; optimized engine control units (ECUs) using AI algorithms for real-time performance tuning and efficiency gains; AI-driven design and simulation tools accelerating the development of next-generation turbochargers with improved aerodynamics and thermal management; supply chain optimization through AI forecasting demand and managing inventory more effectively; and enhanced quality control and manufacturing processes through AI-powered anomaly detection and automation in production lines.

Key Takeaways Diesel Engine Turbocharger Market Size & Forecast

- Significant market expansion anticipated at a CAGR of 5.8% from 2025 to 2033.

- Market valuation expected to grow from USD 17.5 billion in 2025 to USD 27.4 billion by 2033.

- Growth primarily propelled by stringent emission norms and the escalating demand for power-dense, fuel-efficient diesel engines.

- Technological advancements, including variable geometry and electric turbochargers, are crucial growth enablers.

- Asia Pacific is poised to remain a dominant region, driven by robust industrial and commercial vehicle sectors.

- The aftermarket segment represents a substantial revenue stream due to the extended operational lifespan of diesel engines.

- AI integration is fostering smarter maintenance, optimized performance, and accelerated product development.

Diesel Engine Turbocharger Market Drivers Analysis

The Diesel Engine Turbocharger Market is fundamentally shaped by a confluence of powerful drivers, primarily stemming from evolving regulatory landscapes and the continuous pursuit of enhanced engine performance. These factors collectively create a robust demand environment for advanced turbocharging solutions, pushing manufacturers to innovate and expand their product portfolios. The imperative for fuel efficiency and reduced emissions remains paramount, directly influencing design and material choices within the industry. Global infrastructure development and the increasing adoption of commercial vehicles also play a pivotal role in sustaining market momentum, particularly in emerging economies where diesel engines are workhorses.| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Emission Regulations | +1.5% to +2.0% | Global, particularly North America, Europe, China, India | Short to Medium Term (2025-2028) |

| Rising Demand for Fuel-Efficient Engines | +1.0% to +1.5% | Global, strong in commercial transport and construction | Medium to Long Term (2026-2033) |

| Growth in Commercial Vehicle Production | +0.8% to +1.2% | Asia Pacific (China, India), Latin America | Short to Medium Term (2025-2029) |

| Technological Advancements in Turbochargers | +0.7% to +1.0% | Developed economies (Europe, North America, Japan) | Medium to Long Term (2027-2033) |

| Increasing Off-Highway Equipment Sales | +0.5% to +0.8% | Developing nations, infrastructure-driven regions | Medium Term (2026-2030) |

Diesel Engine Turbocharger Market Restraints Analysis

Despite its robust growth trajectory, the Diesel Engine Turbocharger Market faces several significant restraints that could impede its full potential. The increasing global shift towards electric vehicles (EVs) and alternative fuels presents a long-term existential challenge to diesel engine dominance, directly impacting the demand for associated components. Volatile raw material prices, particularly for specialized alloys and rare earth elements used in turbocharger manufacturing, introduce cost instabilities. Furthermore, the inherent complexity and higher maintenance requirements of turbocharger systems, compared to naturally aspirated engines, can be a deterrent for some end-users. The global economic uncertainties and geopolitical tensions can also disrupt supply chains and dampen investment in new diesel vehicle production.| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Adoption of Electric Vehicles (EVs) | -1.2% to -1.8% | Global, prominent in Europe, North America, China | Medium to Long Term (2027-2033) |

| Volatile Raw Material Prices | -0.8% to -1.3% | Global, impacting manufacturing hubs | Short to Medium Term (2025-2029) |

| High Maintenance and Repair Costs | -0.5% to -0.9% | Developing economies with cost-sensitive markets | Medium Term (2026-2030) |

| Stagnation in New Diesel Passenger Vehicle Sales | -0.4% to -0.7% | Europe, North America | Short to Medium Term (2025-2028) |

| Supply Chain Disruptions | -0.3% to -0.6% | Global, with specific regional impact based on origin | Short Term (2025-2026) |

Diesel Engine Turbocharger Market Opportunities Analysis

Opportunities within the Diesel Engine Turbocharger Market primarily revolve around technological innovation, market diversification, and strategic partnerships. The development of next-generation turbochargers, including electric and variable geometry models, offers significant avenues for growth by catering to evolving engine designs and performance demands. Expanding into the aftermarket segment, particularly for replacement parts and refurbishment services, presents a stable and growing revenue stream. Furthermore, the increasing focus on hybridization of heavy-duty vehicles, even with diesel powertrains, opens new integration possibilities for turbocharger manufacturers. Emerging markets, with their ongoing industrialization and infrastructure projects, also provide fertile ground for market penetration and expansion.| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Electric Turbochargers (e-turbos) | +1.0% to +1.5% | Global, especially in premium vehicle segments and heavy-duty | Medium to Long Term (2027-2033) |

| Expansion in the Aftermarket Sector | +0.8% to +1.2% | Global, particularly in regions with large existing vehicle fleets | Short to Long Term (2025-2033) |

| Growth in Off-Highway and Industrial Applications | +0.7% to +1.0% | Asia Pacific, Africa, Latin America | Medium Term (2026-2030) |

| Integration with Hybrid Diesel Powertrains | +0.6% to +0.9% | Europe, North America, emerging in Asia | Medium to Long Term (2028-2033) |

| Technological Upgrades in Existing Engines | +0.5% to +0.7% | All regions, driven by fleet modernization | Short to Medium Term (2025-2028) |

Diesel Engine Turbocharger Market Challenges Impact Analysis

The Diesel Engine Turbocharger Market faces a complex array of challenges, largely stemming from environmental concerns, technological shifts, and intense competitive pressures. The overarching societal and regulatory push away from fossil fuels, particularly diesel, represents a significant hurdle, as it questions the long-term viability of the core product. Developing cost-effective solutions that meet increasingly stringent emission standards while maintaining performance and durability poses a constant engineering challenge. Counterfeit products in the aftermarket also erode legitimate sales and can damage brand reputation. Additionally, managing the intricate global supply chains for specialized components and navigating diverse regional regulations adds layers of operational complexity.| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Public Perception and Anti-Diesel Sentiments | -1.0% to -1.5% | Europe, North America, increasingly global urban centers | Medium to Long Term (2027-2033) |

| High Research and Development Costs | -0.7% to -1.1% | Global, impacting leading manufacturers | Short to Medium Term (2025-2029) |

| Threat of Counterfeit Products | -0.5% to -0.8% | Asia Pacific, Middle East, and Africa | Short to Long Term (2025-2033) |

| Complexity of Integrating New Technologies | -0.4% to -0.7% | Global, particularly in collaboration with engine OEMs | Medium Term (2026-2030) |

| Skilled Workforce Shortage for Advanced Turbocharger Systems | -0.3% to -0.6% | Developed economies, specific industrial clusters | Short to Medium Term (2025-2028) |

Diesel Engine Turbocharger Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Diesel Engine Turbocharger Market, covering historical data, current trends, and future projections. It offers strategic insights into market dynamics, segmentation, competitive landscape, and regional growth opportunities, empowering stakeholders with critical information for informed decision-making. The report thoroughly examines the impact of key drivers, restraints, opportunities, and challenges, providing a holistic view of the market's trajectory and potential.| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 17.5 billion |

| Market Forecast in 2033 | USD 27.4 billion |

| Growth Rate | 5.8% CAGR from 2025 to 2033 |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Garrett Motion, BorgWarner, Mitsubishi Heavy Industries, IHI Corporation, Honeywell International, Cummins, Continental AG, Weichai Power, Bosch Mahle Turbo Systems, Liebherr, ABB, Napier Turbochargers, CNH Industrial, Caterpillar, Komatsu, Volvo Penta, KKK (part of BorgWarner), HOLSET (part of Cummins), Turbocharger Technology (TTI), Eaton (automotive division) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Diesel Engine Turbocharger Market is extensively segmented to provide granular insights into its diverse components, allowing for targeted strategic planning and investment. This segmentation helps in understanding the demand patterns across different vehicle types, the impact of various turbocharging technologies, and the distinction between original equipment and aftermarket sales channels. Each segment exhibits unique growth drivers and market dynamics, contributing distinctively to the overall market trajectory. For instance, while heavy commercial vehicles remain a steadfast segment due to their robust usage, the emerging focus on hybrid diesel powertrains hints at future technological integration opportunities.- By Vehicle Type:

- Passenger Cars: Focus on smaller, more efficient turbochargers for enhanced performance and fuel economy in consumer vehicles.

- Light Commercial Vehicles: Demand driven by last-mile delivery and light-duty transport, balancing power and efficiency.

- Heavy Commercial Vehicles: Largest segment, demanding robust and high-performance turbochargers for long-haul transport and heavy-duty applications.

- Off-Highway Vehicles:

- Construction Equipment: Turbochargers for excavators, loaders, and dozers requiring high torque and durability.

- Agricultural Equipment: Solutions for tractors and harvesters, focusing on power and fuel efficiency in demanding environments.

- By Technology:

- Variable Geometry Turbocharger (VGT): Allows optimization of turbine geometry for improved performance across varying engine speeds, gaining traction due to efficiency benefits.

- Wastegate Turbocharger: Traditional and cost-effective, widely used for basic boost control in diesel engines.

- Electric Turbocharger: Emerging technology utilizing an electric motor to assist or replace the turbine, offering instant boost and improved transient response.

- Twin Turbocharger: Employs two turbochargers (sequential or parallel) for enhanced power delivery across a broader RPM range.

- Supercharger: Mechanically driven compressor, providing immediate boost without turbo lag, often complementing turbochargers in advanced setups.

- By Fuel Type:

- Diesel: The primary application for turbochargers, driving the market due to the inherent characteristics of diesel combustion.

- Hybrid (Diesel-Electric): Growing segment where turbochargers are integrated with electric powertrains to optimize efficiency and emissions in heavy-duty and commercial applications.

- By Sales Channel:

- Original Equipment Manufacturer (OEM): Sales to vehicle and engine manufacturers for new vehicle assembly, representing the largest volume.

- Aftermarket: Sales of replacement parts, remanufactured units, and performance upgrades, offering stable revenue post-initial sale.

- By End Use:

- Automotive: Encompasses both OEM and aftermarket sales for passenger and commercial road vehicles.

- Industrial: Includes applications in power generation (diesel generators), marine propulsion, and heavy construction equipment, where durability and consistent performance are critical.

Regional Highlights

The global Diesel Engine Turbocharger Market exhibits significant regional variations in growth, adoption rates, and technological advancements, influenced by differing regulatory environments, economic development, and industrial landscapes. Each region presents unique opportunities and challenges for market participants, necessitating tailored strategies for successful penetration and sustained growth. Understanding these regional dynamics is crucial for businesses looking to optimize their market presence and capitalize on emerging trends.- Asia Pacific (APAC): The leading and fastest-growing region, APAC’s dominance is fueled by robust industrialization, rapid urbanization, and significant growth in commercial vehicle production, particularly in China and India. Stringent emission norms in these countries are accelerating the adoption of advanced turbocharging technologies. The region's expanding construction and agricultural sectors also contribute substantially to the demand for off-highway diesel engines equipped with turbochargers.

- Europe: A mature market characterized by stringent emission regulations (e.g., Euro VI, Euro 7 discussions) and a strong emphasis on fuel efficiency. While passenger vehicle diesel sales face headwinds due to electrification trends, demand remains solid for heavy commercial vehicles, buses, and industrial machinery. Innovation in advanced variable geometry and electric turbochargers is prevalent here.

- North America: Driven by a robust heavy-duty truck market and a strong demand for powerful off-highway equipment. The region's focus on reducing emissions and improving fuel economy, especially in the commercial sector, sustains the need for high-performance turbochargers. Regulatory alignment with EPA standards dictates technological shifts.

- Latin America: An emerging market with growing industrial and commercial vehicle sectors. Brazil and Mexico are key contributors, driven by infrastructure development and increasing logistics activities. The demand is primarily for cost-effective and durable turbocharger solutions, with a gradual shift towards more efficient technologies.

- Middle East and Africa (MEA): Characterized by significant infrastructure projects and a growing mining sector, especially in Africa, leading to steady demand for off-highway vehicles and industrial engines. The Middle East's focus on fleet modernization and power generation also supports market growth, though regulatory landscapes are less harmonized than in other major regions.

Top Key Players:

The market research report covers the analysis of key stake holders of the Diesel Engine Turbocharger Market. Some of the leading players profiled in the report include -:- Garrett Motion

- BorgWarner

- Mitsubishi Heavy Industries

- IHI Corporation

- Honeywell International

- Cummins

- Continental AG

- Weichai Power

- Bosch Mahle Turbo Systems

- Liebherr

- ABB

- Napier Turbochargers

- CNH Industrial

- Caterpillar

- Komatsu

- Volvo Penta

- KKK

- HOLSET

- Turbocharger Technology (TTI)

- Eaton

Frequently Asked Questions:

What is a diesel engine turbocharger?

A diesel engine turbocharger is a forced induction device that increases an internal combustion engine's power output by forcing extra air into the combustion chamber. It uses the engine's exhaust gases to spin a turbine, which in turn drives a compressor, drawing in more air and significantly improving efficiency, performance, and reducing emissions compared to naturally aspirated engines.What factors are driving the growth of the Diesel Engine Turbocharger Market?

The market's growth is primarily driven by stringent global emission regulations mandating cleaner engines, increasing demand for fuel-efficient and high-performance diesel engines across commercial and off-highway vehicles, and continuous technological advancements in turbocharger design, including variable geometry and electric turbochargers. The expansion of the commercial vehicle sector and industrial machinery globally also significantly contributes to this growth.How does AI impact the Diesel Engine Turbocharger Market?

AI is revolutionizing the Diesel Engine Turbocharger Market by enabling predictive maintenance for reduced downtime, optimizing engine control units for real-time performance and efficiency, accelerating new turbocharger design through AI-driven simulations, and enhancing supply chain management and quality control processes. This integration leads to more reliable, efficient, and technologically advanced turbocharging solutions.Which vehicle types are the primary consumers of diesel engine turbochargers?

Heavy Commercial Vehicles (HCVs) and Off-Highway Vehicles, including construction and agricultural equipment, are the primary consumers of diesel engine turbochargers. These vehicles heavily rely on diesel engines for robust power, high torque, and fuel efficiency in demanding operations, making turbochargers essential components for their performance and regulatory compliance.What are the main challenges facing the Diesel Engine Turbocharger Market?

Key challenges include the growing global shift towards electric vehicles and alternative fuels, leading to declining new diesel passenger car sales in some regions. Volatility in raw material prices, the high research and development costs for advanced technologies, and the prevalence of counterfeit products in the aftermarket also pose significant hurdles for market participants.| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted