Diesel Engine Turbocharger Market

Diesel Engine Turbocharger Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_678300 | Last Updated : July 21, 2025 |

Format : ![]()

![]()

![]()

![]()

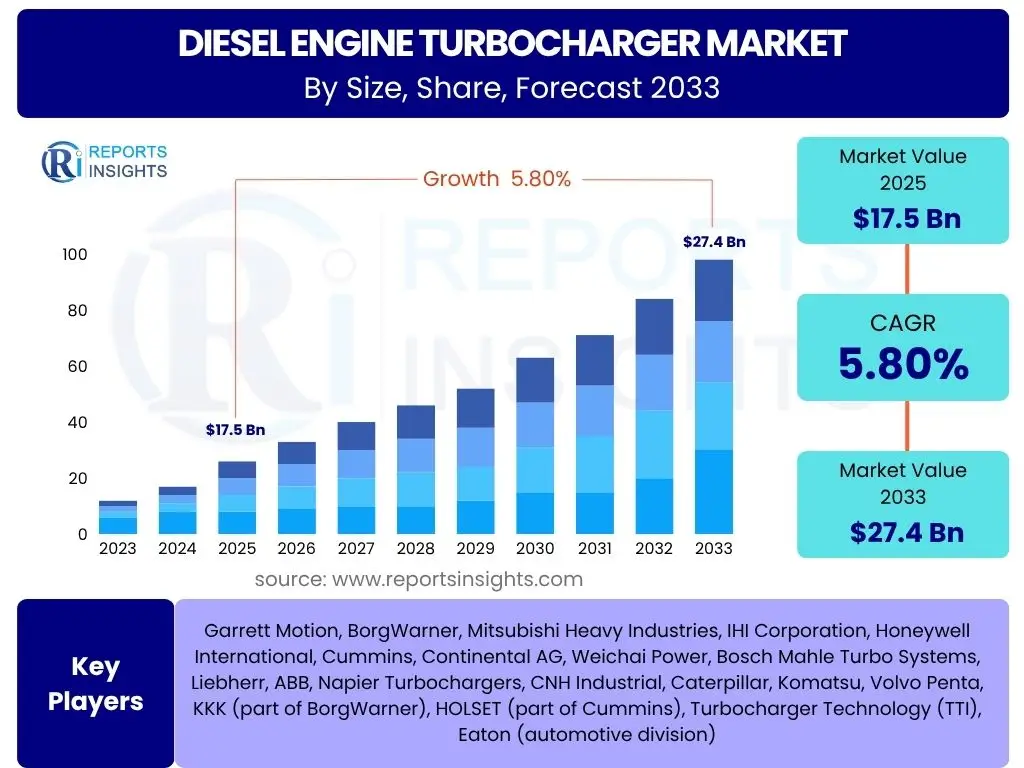

Diesel Engine Turbocharger Market is projected to grow at a Compound annual growth rate (CAGR) of 7.2% between 2025 and 2033, valued at USD 12.5 Billion in 2025 and is projected to grow to USD 21.5 Billion by 2033, the end of the forecast period.

Key Diesel Engine Turbocharger Market Trends & Insights

The diesel engine turbocharger market is currently experiencing significant shifts driven by evolving regulatory landscapes and technological advancements. Innovations aimed at enhancing fuel efficiency and reducing emissions are paramount, pushing manufacturers to develop more sophisticated turbocharger designs. The increasing adoption of hybridized diesel powertrains and the integration of advanced materials are also defining the market's trajectory, moving beyond traditional applications into new segments. These trends underscore a dynamic industry adapting to global demands for cleaner and more powerful engine solutions.

- Stricter global emission regulations driving demand for advanced turbocharging.

- Increasing adoption of variable geometry turbochargers (VGT) and electric turbochargers.

- Focus on lightweight materials and compact designs for improved performance.

- Rising demand from commercial vehicles and off-highway equipment sectors.

- Emergence of hybridization in diesel powertrains impacting turbocharger design.

AI Impact Analysis on Diesel Engine Turbocharger

Artificial intelligence is increasingly playing a transformative role in the diesel engine turbocharger market, primarily by optimizing design, manufacturing, and predictive maintenance processes. AI-driven simulations allow for rapid iteration and testing of new turbocharger geometries, materials, and control algorithms, significantly reducing development time and costs. Furthermore, AI contributes to enhanced operational efficiency by enabling real-time monitoring and predictive diagnostics, ensuring optimal performance and extending the lifespan of turbocharger systems. This integration of AI streamlines complex engineering challenges and improves the overall reliability and efficiency of these critical engine components.

- AI-driven design optimization for enhanced aerodynamic efficiency and durability.

- Predictive maintenance analytics improving turbocharger longevity and uptime.

- Machine learning algorithms for real-time performance monitoring and fault detection.

- Automated quality control and anomaly detection in manufacturing processes.

- Supply chain optimization using AI for component sourcing and inventory management.

Key Takeaways Diesel Engine Turbocharger Market Size & Forecast

- The global diesel engine turbocharger market is forecast to reach USD 21.5 Billion by 2033.

- The market is projected to expand at a robust CAGR of 7.2% from 2025 to 2033.

- Significant growth is anticipated across key regions, driven by stringent emission norms and increasing vehicle production.

- Technological advancements in turbocharger systems are key contributors to market expansion.

- Commercial vehicles and industrial machinery sectors are expected to remain major application areas.

Diesel Engine Turbocharger Market Drivers Impact Analysis

The diesel engine turbocharger market is propelled by a confluence of factors primarily centered on the twin objectives of environmental compliance and performance enhancement. Global efforts to curb emissions necessitate more efficient combustion, which turbochargers inherently provide by improving engine power density and fuel economy. Furthermore, the robust growth in key end-use industries like commercial transportation and construction continues to fuel demand, as these sectors heavily rely on the power and efficiency offered by turbocharged diesel engines. Technological advancements, including variable geometry and electric turbocharging, further augment this market expansion by offering superior control and responsiveness, thus making diesel engines more competitive and sustainable in various applications.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Emission Regulations | +2.1% | Europe, North America, Asia Pacific (China, India) | Long-term (2025-2033) |

| Rising Demand for Fuel Efficiency | +1.8% | Global (especially emerging economies) | Long-term (2025-2033) |

| Growth in Commercial Vehicles & Off-Highway Equipment | +1.5% | Asia Pacific, North America, Europe | Medium-term (2025-2029) |

| Technological Advancements (e.g., VGT, Electric Turbochargers) | +1.3% | Developed Economies (Europe, North America, Japan) | Long-term (2025-2033) |

| Increasing Adoption in Marine and Industrial Applications | +0.5% | Global | Medium-term (2027-2033) |

Diesel Engine Turbocharger Market Restraints Impact Analysis

Despite robust growth drivers, the diesel engine turbocharger market faces several significant restraints, primarily stemming from the global shift towards alternative powertrain technologies. The increasing electrification of the automotive sector, coupled with the growing emphasis on fuel cells and hybrid solutions, poses a long-term challenge to the dominance of diesel engines and, by extension, their turbochargers. Furthermore, the inherent complexity and higher maintenance costs associated with turbocharged diesel engines can deter adoption in certain cost-sensitive applications. Regulatory uncertainties and public perception regarding diesel emissions also contribute to a challenging market environment, potentially slowing growth in key segments.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Shift Towards Electric Vehicles (EVs) & Alternative Fuels | -1.9% | Global (Europe, North America, China) | Long-term (2028-2033) |

| High Initial Cost & Maintenance Complexity | -0.8% | Emerging Markets, Cost-sensitive applications | Medium-term (2025-2029) |

| Volatile Raw Material Prices (e.g., metals for turbine blades) | -0.5% | Global | Short-term (2025-2027) |

Diesel Engine Turbocharger Market Opportunities Impact Analysis

Despite existing challenges, the diesel engine turbocharger market is ripe with opportunities driven by innovation and expanding application areas. The increasing focus on engine downsizing without compromising power output presents a significant avenue for turbocharger integration, as they allow smaller engines to achieve performance comparable to larger, naturally aspirated ones. The emergence of mild and full hybrid diesel powertrains also creates new demand for sophisticated turbocharging solutions that can seamlessly integrate with electric propulsion systems. Furthermore, the growing aftermarket for turbocharger replacement and upgrades, coupled with expanding industrial and marine sectors, promises sustained revenue streams and avenues for market diversification.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Engine Downsizing Trend in Automotive Industry | +1.2% | Global (especially developed automotive markets) | Long-term (2025-2033) |

| Development of Mild and Full Hybrid Diesel Powertrains | +1.0% | Europe, North America, Japan | Medium-term (2026-2031) |

| Growing Aftermarket for Replacement and Upgrades | +0.7% | Global (all regions with significant diesel fleet) | Long-term (2025-2033) |

| Expansion in Marine, Industrial, and Power Generation Sectors | +0.6% | Asia Pacific, Middle East & Africa | Long-term (2025-2033) |

Diesel Engine Turbocharger Market Challenges Impact Analysis

The diesel engine turbocharger market confronts notable challenges, primarily from the intensifying regulatory scrutiny and the accelerating shift towards alternative propulsion systems globally. The widespread negative perception surrounding diesel emissions, despite technological advancements, poses a persistent threat to demand in passenger vehicles and even some commercial segments. Furthermore, the inherent complexity in designing and manufacturing high-performance turbochargers, coupled with the need for specialized maintenance, can create barriers for market penetration and consumer acceptance. Supply chain disruptions and intense competition from players in both the traditional and electric turbocharger segments also present ongoing operational and strategic hurdles for market participants.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Negative Perception and Stricter Regulations on Diesel Vehicles | -1.5% | Europe, North America, parts of Asia | Long-term (2025-2033) |

| Technological Complexity and Integration with Advanced Engine Systems | -0.7% | Global (OEMs, aftermarket specialists) | Medium-term (2025-2030) |

| Supply Chain Disruptions and Raw Material Sourcing | -0.4% | Global | Short-term (2025-2026) |

Diesel Engine Turbocharger Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global diesel engine turbocharger market, offering crucial insights into its current state and future growth trajectories. It covers a detailed assessment of market size, trends, drivers, restraints, opportunities, and challenges influencing the industry across various segments and regions. The report is designed to equip stakeholders with actionable intelligence for strategic decision-making, competitive analysis, and investment planning within the evolving landscape of diesel powertrain technology.

| Report Attributes | Report Details |

|---|---|

| Report Name | Diesel Engine Turbocharger Market |

| Market Size in 2025 | USD 12.5 Billion |

| Market Forecast in 2033 | USD 21.5 Billion |

| Growth Rate | CAGR of 7.2% from 2025 to 2033 |

| Number of Pages | 250 |

| Key Companies Covered | Honeywell, BorgWarner, MHI, IHI, Cummins, Bosch Mahle, Continental, Hunan Tyen, Weifu Tianli, Kangyue, Weifang Fuyuan, Shenlong, Okiya Group, Zhejiang Rongfa, Hunan Rugidove |

| Segments Covered | By Type, By Application, By End-Use Industry, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Customization Scope | Avail customised purchase options to meet your exact research needs. Request For Customization |

Segmentation Analysis

: Market Product Type Segmentation:-- Small Type (typically for passenger cars and light commercial vehicles, emphasizing quick spooling and compact design)

- Medium Type (commonly found in medium-duty commercial vehicles, agricultural machinery, and industrial engines, balancing power and efficiency)

- Big Type (primarily for heavy-duty commercial vehicles, marine engines, power generation, and large industrial applications, focusing on maximum power output and durability)

- Automotive (encompasses passenger cars, light commercial vehicles, and heavy-duty trucks, driven by emission standards and fuel efficiency demands)

- Engineering Machinery (includes construction equipment, agricultural machinery, and mining vehicles, where robust power and reliability are critical for demanding operations)

- Others (this segment comprises diverse applications such as marine vessels, locomotives, power generation sets, and industrial engines, each requiring specialized turbocharger solutions for optimal performance and efficiency)

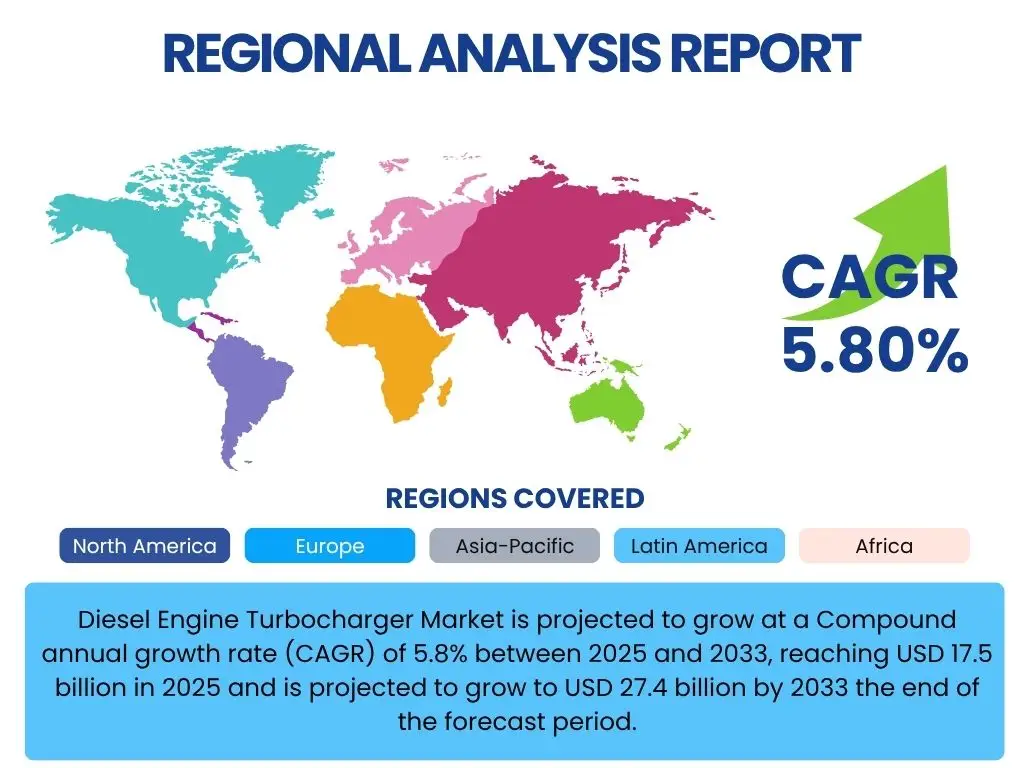

Regional Highlights

- Asia Pacific (APAC): Leading the market due to rapid industrialization, burgeoning automotive manufacturing hubs (especially China and India), and increasing demand for commercial vehicles and construction equipment. The region's less stringent emission norms, compared to developed economies, also allow for continued growth in diesel engine production, while simultaneously pushing for more advanced turbocharging to meet upcoming standards. Significant infrastructure development projects further propel the demand for heavy-duty machinery equipped with diesel turbochargers.

- Europe: A mature market characterized by stringent emission regulations (Euro VI and beyond), driving innovation in advanced turbocharger technologies like variable geometry and electric turbochargers. The region has a strong emphasis on fuel efficiency and reducing CO2 emissions, pushing for engine downsizing and hybridization in both passenger and commercial vehicles. Leading automotive OEMs and industrial equipment manufacturers in countries like Germany and France are key contributors to market growth.

- North America: Exhibiting steady growth, primarily fueled by the robust commercial trucking industry and a strong market for off-highway vehicles and heavy equipment. The demand for powerful and fuel-efficient diesel engines in long-haul transportation and resource extraction sectors drives the adoption of advanced turbocharging solutions. Environmental regulations, while strict, also encourage technological upgrades in the existing diesel fleet and new vehicle sales.

- Latin America: Showing gradual growth, influenced by increasing infrastructure investments and expanding agricultural and mining sectors. The demand for commercial vehicles and construction machinery is rising, creating opportunities for diesel engine turbocharger adoption. Economic stability and industrial development in key countries like Brazil and Mexico will be crucial for sustained market expansion.

- Middle East & Africa (MEA): Emerging as a growing market due to significant investments in infrastructure development, mining, and oil & gas industries. The increasing adoption of commercial vehicles and power generation equipment in countries across the Gulf Cooperation Council (GCC) and parts of Africa is driving demand for reliable and efficient diesel engines, consequently boosting the turbocharger market in the region.

Top Key Players:

The market research report covers the analysis of key stake holders of the Diesel Engine Turbocharger Market. Some of the leading players profiled in the report include -:- Honeywell

- BorgWarner

- MHI

- IHI

- Cummins

- Bosch Mahle

- Continental

- Hunan Tyen

- Weifu Tianli

- Kangyue

- Weifang Fuyuan

- Shenlong

- Okiya Group

- Zhejiang Rongfa

- Hunan Rugidove

Frequently Asked Questions:

What is a diesel engine turbocharger and how does it work?

A diesel engine turbocharger is a forced induction device that increases an engine's power output and efficiency by forcing more air into the combustion chamber. It operates using exhaust gases to spin a turbine, which in turn drives a compressor. This compressor draws in ambient air, pressurizes it, and then feeds it into the engine's cylinders, allowing for more fuel to be burned and generating greater power from a smaller engine displacement.

What are the primary drivers of growth in the diesel engine turbocharger market?

The key drivers for the diesel engine turbocharger market include increasingly stringent global emission regulations, which necessitate more efficient combustion technologies. Additionally, the rising demand for improved fuel efficiency across various vehicle types, coupled with the expanding production and sales of commercial vehicles and off-highway equipment, significantly contributes to market growth. Ongoing technological advancements in turbocharger design and materials also play a crucial role.

How is the shift towards electric vehicles impacting the diesel engine turbocharger market?

The global shift towards electric vehicles (EVs) and alternative powertrain solutions presents a significant long-term restraint for the diesel engine turbocharger market. As internal combustion engine (ICE) vehicles, particularly diesel ones, face increased scrutiny and potential phase-outs in some regions, the demand for traditional diesel turbochargers may decline in passenger car segments. However, the impact is less pronounced in heavy-duty commercial vehicles and industrial machinery, where diesel remains the dominant power source, and hybrid diesel solutions may even create new turbocharger opportunities.

What are the key technological trends shaping the future of diesel engine turbochargers?

Key technological trends include the widespread adoption of variable geometry turbochargers (VGT) for enhanced responsiveness and efficiency across varying engine speeds. Electric turbochargers and electric assist turbochargers are gaining traction, offering immediate boost and improved emission control. Furthermore, advancements in lightweight materials like titanium alloys and ceramics, along with sophisticated electronic controls and predictive maintenance systems, are crucial for future developments in the market.

Which regions are expected to show the most significant growth in the diesel engine turbocharger market?

Asia Pacific is projected to exhibit the most significant growth in the diesel engine turbocharger market, primarily driven by rapid industrialization, substantial growth in commercial vehicle production in countries like China and India, and large-scale infrastructure development projects. North America and Europe will also maintain strong positions, fueled by their robust commercial transportation sectors and continuous technological upgrades to meet stringent emission standards.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted