Data Centre Server Market

Data Centre Server Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_678119 | Last Updated : July 17, 2025 |

Format : ![]()

![]()

![]()

![]()

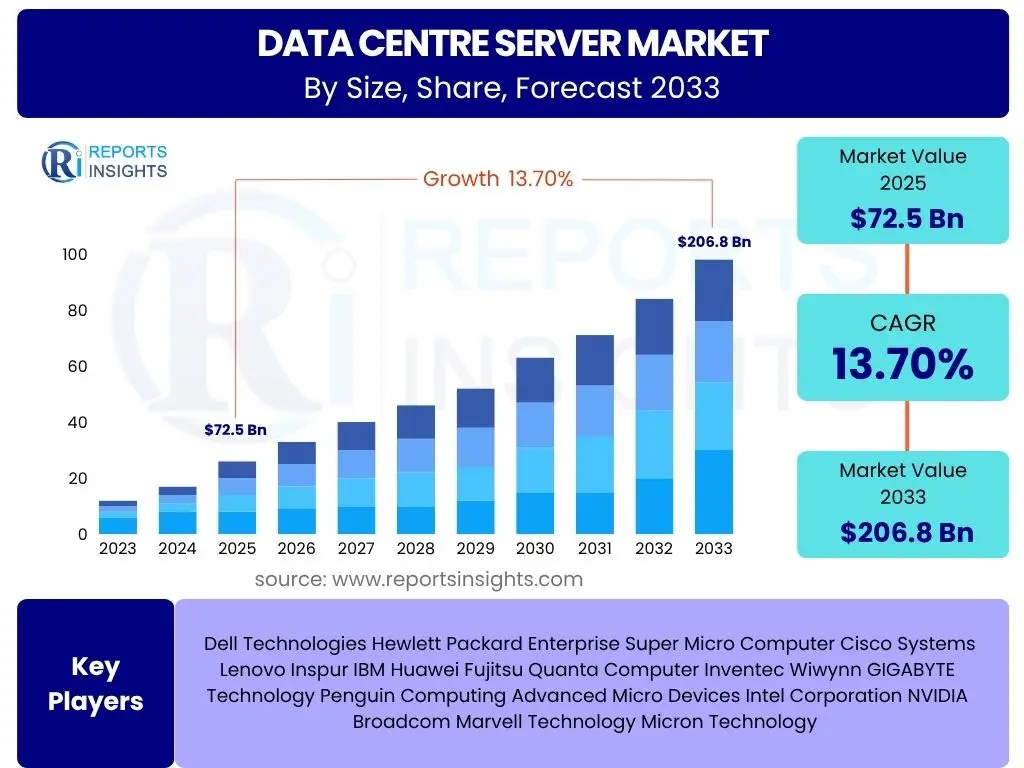

Data Centre Server Market is projected to grow at a Compound annual growth rate (CAGR) of 12.5% between 2025 and 2033, valued at USD 95.5 Billion in 2025 and is projected to grow by USD 245.0 Billion By 2033 the end of the forecast period.

Key Data Centre Server Market Trends & Insights

The global data centre server market is undergoing a profound transformation, driven by an escalating demand for digital services, cloud computing, and advanced analytics. Key trends shaping this landscape include a pervasive shift towards high-performance computing (HPC) and specialized server architectures designed to handle intensive workloads efficiently. Sustainability and energy efficiency are no longer niche concerns but fundamental design principles, pushing for innovations in cooling technologies and power management. Furthermore, the rapid decentralization of IT infrastructure through edge computing is creating new demand patterns for compact, robust server solutions closer to data sources, signaling a significant evolution from traditional centralized data centre models. This dynamic environment necessitates continuous adaptation in server technology and deployment strategies.

- Hyper-convergence of IT infrastructure.

- Increased adoption of cloud and hybrid cloud models.

- Proliferation of edge computing and decentralized data processing.

- Growing focus on energy efficiency and sustainable data centre operations.

- Demand for specialized server architectures for AI and machine learning workloads.

- Enhanced security measures integrated into server hardware and software.

- Transition to high-density server designs and liquid cooling solutions.

AI Impact Analysis on Data Centre Server

Artificial Intelligence (AI) is fundamentally reshaping the data centre server landscape, driving an unprecedented demand for specialized hardware capable of processing vast amounts of data at high speeds. This includes a significant surge in the adoption of Graphics Processing Units (GPUs), Tensor Processing Units (TPUs), and other AI accelerators that are critical for training complex machine learning models and performing real-time inference. The intensive computational requirements of AI workloads necessitate not only more powerful processors but also innovative server designs that can manage increased power consumption and dissipate significant heat effectively. As AI applications become more sophisticated and widespread, their integration is pushing the boundaries of traditional server architecture, spurring innovation in areas such as high-bandwidth memory, faster interconnects, and advanced thermal management solutions to support the next generation of AI-driven computing.

- Increased demand for GPU and specialized AI accelerator-equipped servers.

- Requirement for high-performance, low-latency computing infrastructure.

- Elevated power consumption and heat dissipation challenges.

- Innovation in server architecture for parallel processing.

- Development of AI-optimized software and hardware integration.

- Shift towards liquid cooling systems for dense AI clusters.

- Need for enhanced network bandwidth to support AI data flow.

Key Takeaways Data Centre Server Market Size & Forecast

- The Data Centre Server Market is poised for substantial growth, projected to achieve a CAGR of 12.5% from 2025 to 2033, indicating robust expansion.

- The market's valuation is expected to surge from USD 95.5 Billion in 2025 to USD 245.0 Billion by 2033, reflecting strong investment and adoption.

- Driving factors include accelerated digital transformation, the proliferation of cloud services, and the increasing sophistication of AI workloads demanding high-performance infrastructure.

- Key opportunities lie in specialized server solutions for edge computing, sustainable data centre technologies, and the continued integration of advanced AI/ML capabilities.

- North America and Asia Pacific are anticipated to remain leading regions, driven by significant technological advancements and expanding digital economies.

- The market will witness a continuous evolution in server types, with rack and blade servers maintaining dominance while microservers and Open Compute Project servers gain traction.

- Challenges such as high initial capital expenditure, complex integration, and stringent regulatory compliance will require strategic navigation by market participants.

Data Centre Server Market Drivers Impact Analysis

The data centre server market is propelled by a confluence of powerful drivers, each contributing significantly to its upward trajectory. The relentless pace of digital transformation across industries, coupled with the exponential growth in data generation, creates an undeniable demand for robust server infrastructure. The widespread adoption of cloud computing, encompassing both public and private cloud environments, requires scalable and efficient server solutions to underpin these services. Furthermore, the advent of cutting-edge technologies like Artificial Intelligence, Machine Learning, and the Internet of Things (IoT) necessitates high-performance servers capable of handling complex computational tasks and real-time data processing, driving innovation and investment in specialized hardware. These fundamental shifts in technology and business operations collectively serve as the primary catalysts for market expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Accelerated Digital Transformation | +1.8% | Global, particularly North America, Europe, Asia Pacific | Throughout forecast period |

| Growth of Cloud Computing and Hybrid Cloud Adoption | +1.5% | Global, strong in developed and emerging economies | Medium to Long-term |

| Increasing Demand for AI, ML, and Big Data Analytics | +1.7% | North America, Asia Pacific (China, India, Japan), Europe | Short to Long-term |

| Proliferation of Edge Computing | +1.2% | Global, growing relevance in manufacturing, retail, IoT sectors | Medium to Long-term |

| Expansion of Hyperscale Data Centres | +1.3% | North America, Asia Pacific, Western Europe | Throughout forecast period |

| Rise of 5G Technology and IoT Devices | +1.0% | Global, high impact in regions with 5G rollout | Medium-term |

Data Centre Server Market Restraints Impact Analysis

Despite the robust growth trajectory, the data centre server market faces several significant restraints that could potentially temper its expansion. The substantial initial capital expenditure required for server procurement, installation, and ongoing maintenance presents a considerable barrier, especially for smaller enterprises or those in developing regions. Furthermore, the complexities associated with integrating new server technologies into existing IT infrastructures, coupled with the need for specialized technical expertise, can deter rapid adoption. Environmental concerns surrounding the high energy consumption of data centres, leading to increased operational costs and carbon footprint, are also becoming increasingly scrutinized. These factors, alongside supply chain volatility and evolving regulatory landscapes, collectively pose challenges that market participants must strategically navigate to sustain growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Capital Expenditure and TCO | -0.9% | Global, higher impact on SMBs and emerging markets | Throughout forecast period |

| Growing Energy Consumption and Operational Costs | -0.8% | Global, especially in regions with high energy prices | Short to Medium-term |

| Complexities in Integration and Management | -0.7% | Global, particularly for hybrid and multi-cloud environments | Medium-term |

| Cybersecurity Risks and Data Privacy Concerns | -0.6% | Global, impacting sectors with sensitive data | Throughout forecast period |

| Supply Chain Disruptions and Component Shortages | -0.5% | Global, with fluctuating regional impact | Short-term to Medium-term |

Data Centre Server Market Opportunities Impact Analysis

Amidst the challenges, the data centre server market is rich with opportunities stemming from evolving technological landscapes and shifting enterprise demands. The burgeoning adoption of advanced technologies like AI, IoT, and 5G is creating a significant need for specialized, high-performance servers that can support these compute-intensive applications. Furthermore, the increasing focus on sustainability and energy efficiency presents a unique opportunity for innovation in server design, including the development of more power-efficient components and advanced cooling solutions. The expansion of edge computing and the decentralization of data processing are opening new markets for compact, rugged servers deployed closer to data sources. Additionally, the growing trend of server infrastructure as a service and customized server solutions offers avenues for market players to cater to diverse and specific client needs, fostering long-term growth and market penetration.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Energy-Efficient and Sustainable Servers | +1.4% | Global, driven by regulatory pressures and corporate sustainability goals | Medium to Long-term |

| Emergence of Edge Data Centres and Microservers | +1.1% | Global, strong in industries like retail, telecom, manufacturing | Short to Medium-term |

| Increased Adoption of High-Performance Computing (HPC) | +1.3% | North America, Europe, Asia Pacific, especially in research and development | Throughout forecast period |

| Customized Server Solutions for Specific Workloads (e.g., AI/ML) | +1.0% | Global, catering to enterprise-specific needs | Medium-term |

| Growth of Server-as-a-Service (SaaS) and Infrastructure-as-a-Service (IaaS) Models | +0.9% | Global, particularly attractive for smaller businesses | Throughout forecast period |

Data Centre Server Market Challenges Impact Analysis

The data centre server market, while experiencing substantial growth, is not without its significant challenges that could impede progress. One primary concern is the escalating cost of advanced server components and the continuous need for upgrading infrastructure to keep pace with technological advancements, leading to high capital expenditure. Maintaining robust cybersecurity measures in an increasingly complex and interconnected server environment is another persistent challenge, as data breaches can have severe financial and reputational consequences. Furthermore, the scarcity of skilled professionals capable of designing, deploying, and managing sophisticated data centre server architectures poses a significant operational hurdle. These challenges demand proactive strategies from market participants to ensure sustainable growth and innovation within the industry.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Power Density and Cooling Requirements | -0.8% | Global, more pronounced in high-density data centres | Throughout forecast period |

| Rapid Technological Obsolescence | -0.7% | Global, impacts investment cycles for enterprises | Short to Medium-term |

| Shortage of Skilled Workforce | -0.6% | Global, particularly in specialized fields like AI/HPC server management | Throughout forecast period |

| Regulatory Compliance and Data Sovereignty | -0.5% | Europe, Asia Pacific, and countries with strict data laws | Medium to Long-term |

Data Centre Server Market - Updated Report Scope

This comprehensive market research report delves into the intricate dynamics of the global Data Centre Server Market, offering a detailed analysis of its current landscape and future growth prospects. It provides an in-depth assessment of market size, trends, drivers, restraints, opportunities, and challenges across various segments and regions. The report is meticulously crafted to equip stakeholders with actionable insights, enabling informed strategic decisions in this rapidly evolving technological domain.

| Report Attributes | Report Details |

|---|---|

| Report Name | Data Centre Server Market |

| Market Size in 2025 | USD 95.5 Billion |

| Market Forecast in 2033 | USD 245.0 Billion |

| Growth Rate | CAGR of 2025 to 2033 12.5% |

| Number of Pages | 250 |

| Key Companies Covered | HP, Dell, IBM Corporation, Fujitsu, Cisco Systems, Lenovo Group, Oracle Corporation, Huawei Technologies., Inspur Group, Bull (Atos SE), Hitachi Systems, NEC Corporation, Super Micro Computer, Silicon Graphics International ( Rackable Systems) |

| Segments Covered | By Type, By Application, By End-Use Industry, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Customization Scope | Avail customised purchase options to meet your exact research needs. Request For Customization |

Segmentation Analysis

Market by Order Type Segmentation:-- Rack Server

- Blade Server

- Tower Server

- Microserver

- Open Compute Project Server

- Healthcare

- Financial Institutions

- IT

- Retail

- Government Sectors

Regional Highlights

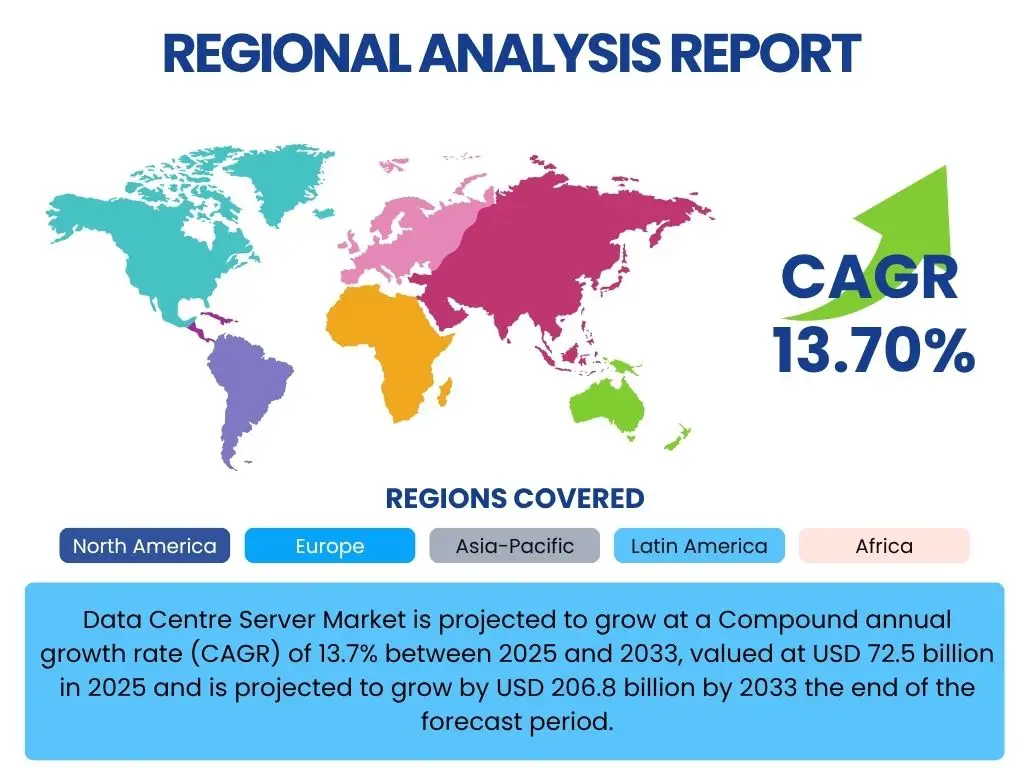

- North America: This region is anticipated to maintain its dominance in the data centre server market, driven by the presence of major technology innovators, hyperscale cloud providers, and early adoption of advanced technologies like AI and edge computing. The strong digital infrastructure, high investment in R&D, and the increasing demand for data processing from various industries, including IT, finance, and healthcare, contribute significantly to its market share. The United States, in particular, leads in data centre buildouts and technological advancements.

- Europe: Europe represents a mature market with significant growth driven by increasing digital transformation initiatives, stringent data privacy regulations (like GDPR) necessitating local data centres, and a rising focus on green data centre solutions. Countries like Germany, the UK, and France are investing heavily in cloud infrastructure and smart city initiatives, further fueling the demand for energy-efficient and secure server solutions. The region's emphasis on sustainability also drives innovation in server technology.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region due to rapid urbanization, widespread digital adoption, and significant investments in data centre infrastructure by both local and international players. Emerging economies like China, India, and Southeast Asian countries are experiencing explosive growth in internet penetration, e-commerce, and mobile data usage, creating immense demand for scalable server solutions. Government initiatives supporting digital economies and the expansion of cloud services are key contributors to this region's expansion.

- Latin America: The Latin American market is experiencing steady growth, propelled by increasing internet penetration, adoption of cloud services by enterprises, and a growing digital economy. Countries such as Brazil and Mexico are leading the charge, with expanding investments in data centres and IT infrastructure to support local businesses and international operations. The region's focus on improving connectivity and digital literacy is fostering demand for data centre servers.

- Middle East and Africa (MEA): This region is witnessing substantial growth in data centre server adoption, primarily driven by government-led digital transformation agendas, diversification of economies away from oil, and increasing cloud service penetration. Countries like UAE, Saudi Arabia, and South Africa are investing heavily in building modern data centre facilities to support smart initiatives, FinTech, and e-governance, thereby creating robust demand for server hardware.

Top Key Players:

The market research report covers the analysis of key stake holders of the Data Centre Server Market. Some of the leading players profiled in the report include -:- HP

- Dell

- IBM Corporation

- Fujitsu

- Cisco Systems

- Lenovo Group

- Oracle Corporation

- Huawei Technologies.

- Inspur Group

- Bull (Atos SE)

- Hitachi Systems

- NEC Corporation

- Super Micro Computer

- Silicon Graphics International ( Rackable Systems)

Frequently Asked Questions:

What is a data centre server?

A data centre server is a powerful computer designed to process, store, and manage data and applications within a data centre environment. These servers are typically optimized for high performance, reliability, and scalability, supporting critical business operations, cloud services, and complex computations.

What are the primary drivers of growth in the Data Centre Server Market?

Key drivers include rapid digital transformation, the exponential growth of cloud computing and hybrid cloud models, increasing demand for AI, Machine Learning, and Big Data analytics, the expansion of hyperscale data centres, and the proliferation of edge computing and 5G technology.

How is Artificial Intelligence impacting the demand for data centre servers?

AI significantly impacts server demand by necessitating specialized, high-performance servers equipped with GPUs and other accelerators to handle intensive computational workloads. This drives innovation in server architecture, power management, and cooling solutions to support AI model training and inference.

What are the main types of servers used in data centres?

The main types include rack servers, which are designed for high-density configurations; blade servers, known for their modularity and space efficiency; tower servers, suitable for smaller environments; microservers, ideal for low-power, distributed workloads; and Open Compute Project servers, focusing on open hardware designs for efficiency.

Which regions are leading in the adoption and growth of the Data Centre Server Market?

North America and Asia Pacific are currently the leading regions. North America benefits from technological innovation and hyperscale cloud providers, while Asia Pacific exhibits the fastest growth due to rapid digital transformation, increasing internet penetration, and significant investments in data centre infrastructure by emerging economies.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted