Data Center Physical Security Market

Data Center Physical Security Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708539 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

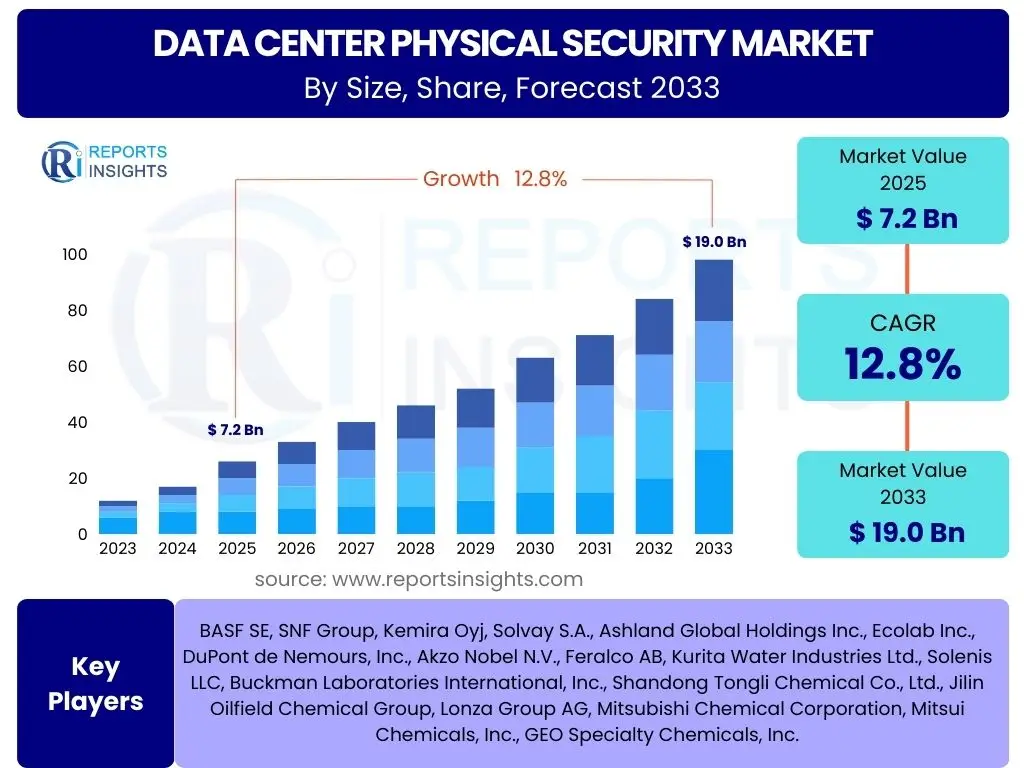

Data Center Physical Security Market Size

According to Reports Insights Consulting Pvt Ltd, The Data Center Physical Security Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.8% between 2025 and 2033. The market is estimated at USD 7.2 Billion in 2025 and is projected to reach USD 19.0 Billion by the end of the forecast period in 2033. This robust growth is primarily driven by the escalating demand for digital infrastructure, coupled with an increasing awareness and necessity for safeguarding critical data assets against a backdrop of sophisticated cyber and physical threats.

The market’s expansion is further supported by the global proliferation of hyperscale and edge data centers, which require advanced physical security solutions to ensure uninterrupted operations and data integrity. As organizations continue their digital transformation journeys, the reliance on secure and resilient data center environments intensifies, thereby boosting investments in comprehensive physical security measures, including advanced access control, video surveillance, and intrusion detection systems. The focus on meeting stringent regulatory compliance standards across various industries also significantly contributes to this upward trajectory.

Key Data Center Physical Security Market Trends & Insights

The Data Center Physical Security market is undergoing a significant transformation, driven by technological advancements and an evolving threat landscape. Users are primarily concerned with how new technologies like artificial intelligence and machine learning are being integrated, the growing emphasis on converged security solutions, and the impact of regulatory compliance on security strategies. There is also a keen interest in understanding how to secure increasingly distributed data center environments, including edge and hyperscale facilities, and the role of automation in enhancing security operations. These insights reveal a shift towards more proactive, intelligent, and integrated security frameworks.

The market is rapidly moving beyond traditional perimeter defense to embrace holistic security architectures that blend physical and digital protection. This convergence allows for a more unified command and control, enabling quicker response times and more efficient threat mitigation. Furthermore, the increasing complexity of data center environments necessitates solutions that can adapt and scale, making modular and flexible security systems particularly appealing to operators. The demand for solutions that not only detect but also predict and prevent security incidents is at an all-time high, pushing manufacturers to innovate constantly.

- Convergence of physical and cybersecurity frameworks for holistic protection.

- Increased adoption of AI and machine learning for predictive analytics, anomaly detection, and automation in surveillance and access control.

- Growing demand for integrated security platforms that offer unified management of various security components.

- Emphasis on advanced biometric authentication and multi-factor access control systems.

- Expansion of edge data centers driving the need for distributed yet centrally managed security solutions.

- Stringent regulatory compliance and data governance requirements (e.g., GDPR, HIPAA) influencing security investments.

AI Impact Analysis on Data Center Physical Security

User inquiries regarding AI's impact on data center physical security predominantly focus on its potential to enhance detection capabilities, automate routine tasks, and provide predictive insights, thereby improving overall security posture. Concerns often revolve around the accuracy of AI systems, the ethical implications of advanced surveillance, and the integration challenges with existing infrastructure. Users seek to understand how AI can move physical security from a reactive to a proactive paradigm, reducing human error and optimizing resource allocation. The consensus is that AI represents a transformative force, offering both significant opportunities and new considerations for data center operators.

Artificial intelligence is revolutionizing data center physical security by enabling more intelligent surveillance systems, predictive maintenance for security hardware, and automated, granular access control. AI-powered video analytics can process vast amounts of footage to identify suspicious activities, recognize faces or objects, and alert security personnel in real-time, drastically reducing response times and minimizing false alarms. Furthermore, machine learning algorithms can analyze historical data to predict potential security breaches or equipment failures, allowing for proactive interventions. This shift empowers data center operators to implement more robust, efficient, and resilient security protocols that adapt to dynamic threat landscapes.

- Enhanced surveillance with AI-powered video analytics for real-time anomaly detection, facial recognition, and object tracking.

- Predictive maintenance for security infrastructure, anticipating failures in cameras, sensors, or access control systems.

- Automated and intelligent access control systems, leveraging biometrics and behavioral analytics for more secure and efficient entry management.

- Real-time threat assessment and improved situational awareness through AI-driven correlation of data from various security systems.

- Reduction of false positives in security alerts, allowing security teams to focus on genuine threats.

- Optimization of security personnel deployment and resource allocation based on AI-generated insights and threat patterns.

Key Takeaways Data Center Physical Security Market Size & Forecast

The Data Center Physical Security market is on a path of substantial and sustained growth, driven primarily by the escalating demand for robust digital infrastructure and the imperative to protect highly sensitive data assets. Users frequently inquire about the primary factors fueling this expansion, the role of technological innovation, and the strategic implications for businesses investing in data center operations. The core takeaway is the market's resilience and its critical importance in the broader digital economy, underscoring the necessity for continuous investment in advanced security measures to mitigate an ever-evolving spectrum of threats.

The forecast highlights that physical security is no longer a peripheral concern but a fundamental component of data center design and operation, integral to business continuity and regulatory compliance. The integration of cutting-edge technologies like AI, IoT, and advanced biometrics is not merely an enhancement but a strategic necessity, enabling data centers to withstand increasingly sophisticated physical and cyber-physical attacks. This market trajectory suggests significant opportunities for innovation and specialization, particularly in areas like managed security services and solutions tailored for hybrid and edge computing environments.

- The Data Center Physical Security Market is projected for robust double-digit CAGR growth, reflecting its critical role in the expanding digital economy.

- Significant market expansion is fueled by the rapid proliferation of data centers globally, coupled with a heightened awareness of physical and cyber-physical security risks.

- Technological advancements, particularly in AI, machine learning, and advanced biometrics, are key enablers for next-generation security solutions.

- Stringent regulatory frameworks and compliance mandates are compelling organizations across all sectors to elevate their physical security investments.

- The market is shifting towards comprehensive, integrated security platforms that offer converged protection, moving away from siloed security systems.

- Opportunities abound in managed security services and specialized solutions catering to the unique requirements of hyperscale, colocation, and edge data centers.

Data Center Physical Security Market Drivers Analysis

The Data Center Physical Security market is significantly propelled by several interconnected factors, all pointing towards an increased need for robust protective measures. A primary driver is the accelerating pace of digital transformation and the resultant explosion of data, requiring more data centers that inherently demand advanced security. Concurrently, the sophistication and frequency of both cyber and physical threats are on the rise, forcing organizations to invest heavily in preventative and responsive security systems. The regulatory landscape is also tightening, with mandates like GDPR and HIPAA imposing strict requirements on data protection, making robust physical security a compliance imperative.

Moreover, the global expansion of hyperscale and edge computing infrastructure further fuels market growth. Hyperscale data centers represent massive investments requiring comprehensive security, while edge data centers, often distributed and less supervised, present unique challenges that drive demand for specialized, often automated, physical security solutions. The desire for operational efficiency and reduced human intervention through automation also acts as a driver, as data center operators seek intelligent systems that can monitor, detect, and respond to threats with minimal human input, thereby reducing operational costs and human error.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Escalating Cyber and Physical Threats | +2.5% | Global | Short-to-Mid Term |

| Strict Regulatory Compliance & Data Governance | +2.0% | North America, Europe | Mid-to-Long Term |

| Proliferation of Data Centers (Hyperscale, Edge, Colocation) | +1.8% | APAC, North America | Mid-to-Long Term |

| Rising Adoption of IoT and Connected Devices in Data Centers | +1.5% | Global | Mid-to-Long Term |

| Demand for Operational Efficiency and Automation in Security | +1.0% | Global | Short-to-Mid Term |

Data Center Physical Security Market Restraints Analysis

Despite the strong growth drivers, the Data Center Physical Security market faces several notable restraints that can impede its full potential. One significant barrier is the high initial investment cost associated with deploying advanced physical security systems. This includes not only the capital expenditure for hardware and software but also the costs related to infrastructure upgrades, installation, and integration, which can be prohibitive for smaller and medium-sized enterprises (SMEs) or data centers with limited budgets. The complexity involved in integrating new, sophisticated security technologies with legacy systems also poses a significant challenge, often leading to extended deployment times and unexpected costs.

Another key restraint is the persistent shortage of skilled personnel capable of designing, implementing, and managing these increasingly complex security solutions. The specialized knowledge required for AI-powered surveillance, biometric access controls, and converged security platforms is not readily available, leading to operational inefficiencies and potential security gaps. Furthermore, growing concerns around data privacy and compliance with various data protection laws can act as a restraint, as organizations grapple with the ethical implications and legal requirements associated with advanced surveillance and identity management systems. Budgetary constraints, particularly in highly competitive or nascent markets, also limit the adoption of premium security solutions.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment Costs for Advanced Systems | -1.5% | Emerging Markets, SMEs | Short-to-Mid Term |

| Complexity of Integration with Existing Infrastructure | -1.2% | Global | Mid-Term |

| Lack of Skilled Personnel and Expertise | -1.0% | Global | Long Term |

| Concerns Over Data Privacy and Ethical Use of Surveillance | -0.8% | Europe, North America | Mid-to-Long Term |

| Budgetary Constraints in Smaller Organizations | -0.7% | Global | Short-to-Mid Term |

Data Center Physical Security Market Opportunities Analysis

The Data Center Physical Security market is ripe with opportunities for innovation and growth, particularly as technological capabilities advance and the digital landscape evolves. A significant opportunity lies in the continued development and deployment of AI-powered predictive security solutions. These systems move beyond reactive threat detection to proactive threat prediction and prevention, offering a substantial leap in security efficacy. The burgeoning market for managed security services (MSS) also presents a strong opportunity, as many organizations lack the internal expertise or resources to manage complex security infrastructures, preferring to outsource these functions to specialized providers.

Furthermore, the rapid expansion of edge computing necessitates novel security approaches, creating a distinct market segment for purpose-built edge data center security solutions. These solutions must be robust yet compact, capable of remote management, and resilient in diverse environmental conditions. The substantial installed base of older data center infrastructure worldwide also offers a significant opportunity for retrofitting and upgrading existing security systems with modern, more efficient technologies. Additionally, the increasing focus on advanced authentication methods, such as biometrics and multi-factor authentication, across all data center types opens avenues for specialized product development and market penetration.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of AI-Powered Predictive Security Solutions | +3.0% | Global | Mid-to-Long Term |

| Growth in Demand for Managed Security Services (MSS) | +2.5% | Global | Short-to-Mid Term |

| Development of Specialized Edge Data Center Security Solutions | +2.0% | Global | Mid-to-Long Term |

| Retrofitting and Upgrading Existing Data Center Infrastructure | +1.5% | Developed Regions | Short-to-Mid Term |

| Increasing Adoption of Biometric and Multi-Factor Authentication | +1.0% | Global | Short-to-Mid Term |

Data Center Physical Security Market Challenges Impact Analysis

The Data Center Physical Security market, while growing, is also confronted by a series of significant challenges that necessitate constant innovation and adaptation. A primary concern is the continuously evolving threat landscape, where attackers are becoming increasingly sophisticated, developing new methods to bypass traditional security measures. This constant arms race demands continuous investment in research and development, as well as rapid deployment of updated solutions, which can be resource-intensive. Interoperability issues between diverse security systems from different vendors also present a major challenge, hindering the creation of a truly integrated and seamless security posture.

Another critical challenge involves striking the right balance between robust security measures and the operational accessibility required for data center staff and authorized personnel. Overly restrictive security protocols can impede legitimate operations, leading to inefficiencies, while lax security creates vulnerabilities. Additionally, the increasing complexity of global supply chains for hardware and software components introduces significant supply chain vulnerabilities, making it difficult for data center operators to ensure the integrity of their security systems from origin to deployment. The escalating cost of continuous upgrades and maintenance for advanced security solutions further compounds these challenges, particularly for organizations operating on tight budgets.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Evolving and Sophisticated Threat Landscape | -1.5% | Global | Continuous |

| Interoperability Issues Between Disparate Security Systems | -1.2% | Global | Mid-to-Long Term |

| Balancing Enhanced Security with Operational Accessibility | -1.0% | Global | Continuous |

| Supply Chain Vulnerabilities for Security Hardware & Software | -0.8% | Global | Short-to-Mid Term |

| Cost of Continuous Upgrades and Maintenance | -0.7% | Global | Long Term |

Data Center Physical Security Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Data Center Physical Security market, examining its current landscape, key growth drivers, emerging trends, significant restraints, and promising opportunities. It offers a detailed forecast from 2025 to 2033, segmenting the market by solution, service, deployment type, and end-user, while also providing regional insights. The report aims to equip stakeholders with critical market intelligence to make informed strategic decisions, identify lucrative investment avenues, and understand the competitive dynamics shaping the industry. Special emphasis is placed on the impact of artificial intelligence and the importance of converged security solutions in future market growth.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 7.2 Billion |

| Market Forecast in 2033 | USD 19.0 Billion |

| Growth Rate | 12.8% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Axis Communications, Cisco Systems, Honeywell International Inc., Johnson Controls International plc, HID Global Corporation, Siemens AG, Schneider Electric SE, Bosch Security Systems GmbH, Dahua Technology Co. Ltd., Hikvision Digital Technology Co. Ltd., Genetec Inc., Pelco, Avigilon Corporation, Hanwha Techwin Co. Ltd., NEC Corporation, Securitas AB, Allegion plc, Aiphone Co. Ltd., Identiv Inc., Salto Systems S.L. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Data Center Physical Security market is comprehensively segmented to provide a granular view of its various components and their respective contributions to the overall market dynamics. This segmentation helps in understanding the specific technologies, services, and deployment models that are driving growth, as well as the diverse needs of different end-user industries. By breaking down the market into these core segments, the report offers detailed insights into areas of high growth potential and specific market niches, allowing for targeted strategic planning and investment decisions across the value chain.

Each segment is analyzed for its current market size, projected growth rate, and key influencing factors. For instance, the solution segment highlights the prevalence and evolution of access control and video surveillance technologies, while the service segment underscores the increasing reliance on expert support and managed security offerings. The deployment type and end-user segments further delineate how various organizations are adopting and implementing these security measures, from large cloud providers to government entities. This structured approach ensures a thorough understanding of the market's intricate ecosystem.

- By Solution: This segment includes the core technological components of physical security.

- Access Control: Encompasses various methods like Biometric (fingerprint, iris, facial recognition), Card-Based (proximity cards, smart cards), PIN (keypads), and Mobile (smartphone-based access).

- Video Surveillance: Involves IP Cameras, Analog Cameras, Video Analytics software for pattern detection, and Video Management Systems (VMS).

- Intrusion Detection: Covers Perimeter Security systems, Motion Sensors, and Door/Window Sensors.

- Alarm Systems: For immediate notification of security breaches.

- Environmental Monitoring: Monitors temperature, humidity, and water leakage.

- Power Monitoring: Tracks power usage and anomalies.

- Fire Protection: Includes fire suppression and detection systems.

- By Service: This segment focuses on the support and operational aspects of physical security.

- Installation & Integration: Services for setting up and integrating diverse security systems.

- Maintenance & Support: Ongoing services for system upkeep and troubleshooting.

- Consulting: Expert advice on security strategy, risk assessment, and compliance.

- Managed Security Services: Outsourcing of security operations to third-party specialists.

- By Deployment Type: This segment categorizes solutions based on their hosting model.

- On-Premise: Security systems hosted and managed within the data center facility.

- Cloud-Based: Security solutions delivered and managed via cloud infrastructure.

- Hybrid: A combination of on-premise and cloud-based security components.

- By End User: This segment details the various types of organizations utilizing data center physical security.

- Colocation Data Centers: Facilities that lease space and resources to multiple tenants.

- Enterprise Data Centers: Private data centers owned and operated by a single organization.

- Cloud Providers: Companies offering cloud computing services, requiring robust security for their vast infrastructure.

- Telecom & IT: Companies in the telecommunications and information technology sectors.

- Government & Defense: Public sector entities with stringent security requirements.

- Healthcare: Organizations handling sensitive patient data (e.g., HIPAA compliance).

- BFSI (Banking, Financial Services, and Insurance): Financial institutions with critical data protection needs.

- Others: Includes retail, manufacturing, energy, and utility sectors.

Regional Highlights

The Data Center Physical Security market exhibits distinct growth patterns and maturity levels across different geographical regions, influenced by economic development, regulatory environments, technological adoption rates, and the density of data center infrastructure. Each region presents a unique set of drivers and challenges, contributing to the global market's overall trajectory. Understanding these regional nuances is crucial for companies seeking to expand their market reach and for investors evaluating opportunities within specific geographies.

North America, for instance, leads the market due to its advanced digital infrastructure, early adoption of cutting-edge technologies, and stringent regulatory compliance standards. The Asia Pacific region is expected to demonstrate the highest growth rate, driven by rapid industrialization, burgeoning digital economies, and significant investments in new data center construction, particularly in countries like China, India, and Japan. Europe is characterized by a strong emphasis on data privacy and security regulations (e.g., GDPR), which compels robust security investments, while Latin America and the Middle East & Africa are emerging markets showing increasing potential as their digital infrastructures mature and expand.

- North America: Dominates the market due to the presence of a large number of hyperscale data centers, early adoption of advanced security technologies, and strict regulatory frameworks, particularly in the United States and Canada. High investment in R&D and cybersecurity infrastructure further solidifies its leading position.

- Europe: Characterized by strong regulatory mandates such as GDPR, driving significant investments in physical security to ensure data protection and privacy. Countries like Germany, the UK, and France are key contributors, focusing on integrated and compliant security solutions.

- Asia Pacific (APAC): Expected to be the fastest-growing region, fueled by rapid digital transformation, increasing internet penetration, massive data generation, and significant investments in data center expansion in countries like China, India, Japan, and Australia. The proliferation of smart cities and IoT devices also drives demand.

- Latin America: An emerging market experiencing steady growth, driven by increasing digital adoption, cloud service expansion, and the establishment of new data center facilities, particularly in Brazil and Mexico. Economic development and foreign investments are key factors.

- Middle East & Africa (MEA): Shows promising growth potential due to government initiatives for digital transformation, diversification of economies away from oil, and growing investments in smart infrastructure projects in countries like UAE, Saudi Arabia, and South Africa.

Top Key Players

The marketresearch report includes a detailed profile of leading stakeholders in the Data Center Physical Security Market.- Axis Communications AB

- Cisco Systems, Inc.

- Honeywell International Inc.

- Johnson Controls International plc

- HID Global Corporation

- Siemens AG

- Schneider Electric SE

- Bosch Security Systems GmbH

- Dahua Technology Co. Ltd.

- Hikvision Digital Technology Co. Ltd.

- Genetec Inc.

- Pelco (Motorola Solutions)

- Avigilon Corporation (Motorola Solutions)

- Hanwha Techwin Co. Ltd.

- NEC Corporation

- Securitas AB

- Allegion plc

- Aiphone Co. Ltd.

- Identiv Inc.

- Salto Systems S.L.

Frequently Asked Questions

What is the projected growth for the Data Center Physical Security market?

The Data Center Physical Security market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.8% from USD 7.2 Billion in 2025 to USD 19.0 Billion by 2033, driven by increasing data center expansion and heightened security threats.

How is AI transforming data center physical security?

AI is revolutionizing data center physical security by enabling enhanced surveillance with intelligent video analytics, predictive maintenance for security infrastructure, automated access control, and real-time threat assessment to provide more proactive and efficient protection.

What are the main drivers for the Data Center Physical Security market?

Key drivers include escalating cyber and physical threats, stringent regulatory compliance requirements (e.g., GDPR), the rapid proliferation of data centers globally (hyperscale, edge), and the growing demand for operational efficiency through security automation.

What are the key challenges in implementing data center physical security?

Major challenges include the continuously evolving threat landscape, interoperability issues between disparate security systems, balancing robust security with operational accessibility, supply chain vulnerabilities, and the high cost of continuous upgrades and maintenance.

Which regions are leading the Data Center Physical Security market?

North America currently leads the market due to its advanced infrastructure and stringent regulations, while the Asia Pacific region is anticipated to exhibit the fastest growth, driven by massive data center investments and rapid digital transformation across its economies.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted