Cyber Defense Market

Cyber Defense Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705641 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

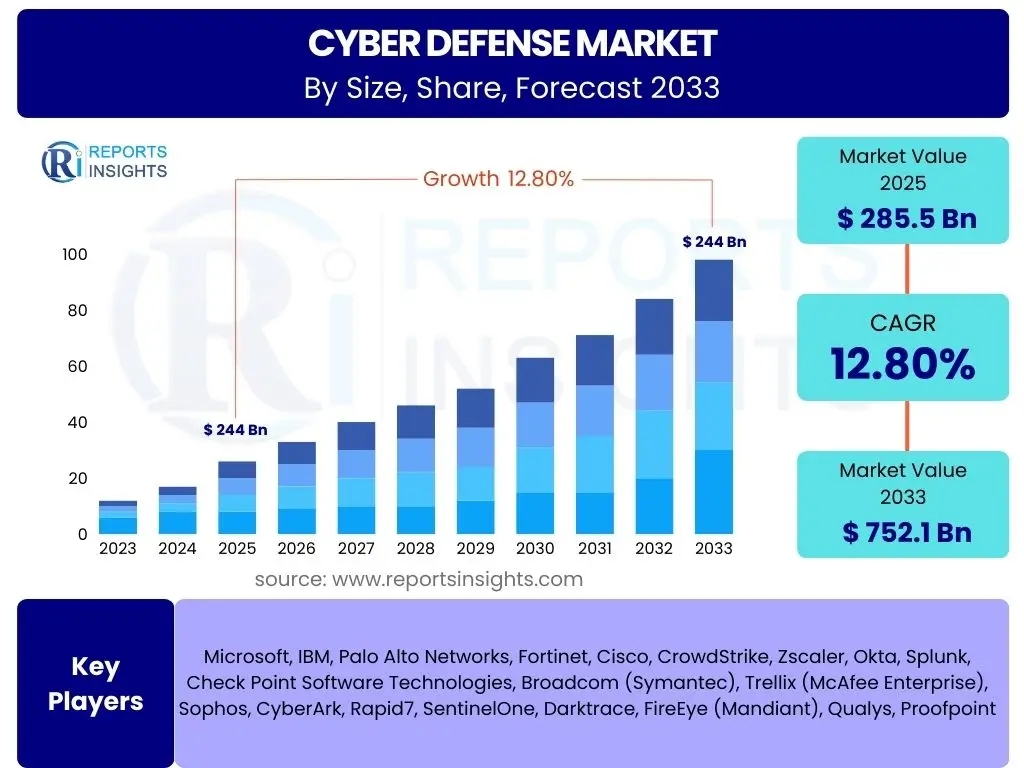

Cyber Defense Market Size

According to Reports Insights Consulting Pvt Ltd, The Cyber Defense Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.8% between 2025 and 2033. The market is estimated at USD 285.5 billion in 2025 and is projected to reach USD 752.1 billion by the end of the forecast period in 2033.

Key Cyber Defense Market Trends & Insights

The Cyber Defense market is experiencing rapid evolution driven by an escalating threat landscape and pervasive digital transformation across industries. User queries frequently revolve around the adoption of proactive security measures, the shift towards cloud-native solutions, and the increasing sophistication of cyberattacks. Organizations are prioritizing resilience and integrated security architectures to combat advanced persistent threats, ransomware, and supply chain vulnerabilities. The convergence of IT and OT security is also a prominent concern, reflecting the expanding attack surface in critical infrastructure and industrial environments.

Another key area of interest concerns the impact of regulatory frameworks and compliance requirements, which are compelling businesses to invest more heavily in robust cyber defense capabilities. There is a strong emphasis on data privacy and protection, leading to increased demand for data security and identity management solutions. Furthermore, the persistent cybersecurity talent gap continues to drive interest in automated solutions and managed security services, as organizations seek to augment their internal capabilities and reduce operational burdens.

- Zero Trust Architecture adoption accelerating across enterprises.

- Increased focus on supply chain security and third-party risk management.

- Expansion of cloud security solutions to protect hybrid and multi-cloud environments.

- Growing demand for advanced threat intelligence and predictive analytics.

- Convergence of IT, OT, and IoT security for comprehensive protection.

- Emphasis on human-centric security awareness training to mitigate insider threats.

- Rise of security orchestration, automation, and response (SOAR) platforms.

- Evolution of ransomware and nation-state sponsored cyberattacks.

AI Impact Analysis on Cyber Defense

User inquiries concerning the influence of Artificial Intelligence (AI) on cyber defense frequently highlight its dual nature: a powerful tool for enhanced security and a potential enabler for more sophisticated attacks. Key themes include AI's role in automating threat detection, accelerating incident response, and performing predictive analytics to identify vulnerabilities before exploitation. There is a strong expectation that AI will significantly improve the efficiency and effectiveness of security operations centers (SOCs) by reducing alert fatigue and enabling faster triage of critical incidents. However, concerns also exist regarding the potential for AI to be weaponized by malicious actors, leading to polymorphic malware, automated phishing campaigns, and more evasive attack techniques.

Furthermore, users are keen to understand the ethical implications and potential biases within AI-driven security systems, as well as the need for explainable AI to ensure transparency and accountability. The balance between leveraging AI for defensive purposes and preparing for AI-powered offensive strategies is a critical discussion point. Organizations are increasingly looking for AI-powered security solutions that can adapt to evolving threats, learn from past incidents, and provide real-time insights to minimize the window of vulnerability. The integration of machine learning into existing security frameworks is viewed as essential for future-proofing cyber defenses.

- Enhanced threat detection through AI-powered anomaly recognition and behavioral analysis.

- Automated incident response and remediation capabilities, reducing response times.

- Predictive threat intelligence and risk assessment based on vast data sets.

- Improved phishing and malware detection by analyzing complex patterns.

- Potential for AI to generate highly convincing deepfake-based social engineering attacks.

- Emergence of AI-driven polymorphic malware that can evade traditional defenses.

- Increased demand for AI ethics and transparency in cybersecurity applications.

- Optimization of security operations center (SOC) efficiency and resource allocation.

Key Takeaways Cyber Defense Market Size & Forecast

Common user questions regarding the Cyber Defense market size and forecast often focus on understanding the primary drivers behind its robust growth and identifying the most promising areas for investment. The market's consistent expansion is largely attributable to the escalating volume and sophistication of cyber threats, coupled with the accelerating digital transformation initiatives across all sectors. Organizations are realizing that robust cyber defense is not merely a cost center but a fundamental enabler of business continuity, innovation, and trust, leading to sustained budget allocations.

A significant takeaway is the shift towards a more proactive and resilient security posture, moving beyond reactive defense mechanisms. The integration of advanced technologies like AI, machine learning, and automation is critical in managing the ever-expanding attack surface and the complexity of modern IT environments. Moreover, the increasing regulatory pressure for data protection and privacy compliance globally is a strong underlying factor driving market demand. The forecast indicates that the market will continue its upward trajectory, with substantial opportunities emerging in specialized areas such as cloud security, identity management, and managed security services, as organizations seek comprehensive and outsourced expertise.

- Market growth driven by increasing cyberattack sophistication and digital transformation.

- Significant investment surge in proactive and resilient cyber defense strategies.

- AI and automation are becoming indispensable for effective threat management.

- Regulatory compliance and data privacy concerns are major market accelerators.

- Cloud security and managed security services represent high-growth segments.

Cyber Defense Market Drivers Analysis

The Cyber Defense market is propelled by a confluence of critical factors that necessitate enhanced security postures across all organizational sizes and sectors. The pervasive digitalization of global economies, coupled with the rapid adoption of cloud computing, IoT devices, and remote work models, has dramatically expanded the attack surface, creating more entry points for malicious actors. This expansion inherently drives the demand for comprehensive cyber defense solutions capable of protecting diverse and distributed environments. The increasing frequency, volume, and sophistication of cyberattacks, including ransomware, phishing, and supply chain attacks, force organizations to continuously upgrade their defenses to prevent significant financial losses, data breaches, and reputational damage.

Furthermore, stringent regulatory frameworks and data privacy mandates globally, such as GDPR, CCPA, and various industry-specific regulations, compel businesses to invest heavily in compliance-driven security measures. Non-compliance often results in severe penalties, legal repercussions, and erosion of customer trust. The growing awareness among businesses and individuals about the economic and social consequences of cyber incidents also contributes to the heightened demand for robust cyber defense. Lastly, the persistent cybersecurity skills gap incentivizes organizations to adopt advanced automated solutions and rely on managed security service providers (MSSPs) to bridge their internal resource deficits, further fueling market growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Escalating Volume and Sophistication of Cyberattacks | +4.5% | Global | 2025-2033 (Long-term) |

| Rapid Digital Transformation and Cloud Adoption | +3.8% | North America, Europe, APAC | 2025-2033 (Ongoing) |

| Stringent Regulatory Compliance and Data Privacy Mandates | +2.9% | Europe, North America, Asia Pacific | 2025-2030 (Medium-term) |

| Increasing Geopolitical Tensions and Nation-State Attacks | +1.5% | Global | 2025-2033 (Long-term) |

| Expansion of IoT and OT Environments | +1.2% | North America, Europe, Asia Pacific | 2027-2033 (Mid- to Long-term) |

Cyber Defense Market Restraints Analysis

Despite the robust growth of the Cyber Defense market, several significant restraints impede its full potential. One primary challenge is the high cost associated with implementing and maintaining sophisticated cyber defense solutions, particularly for small and medium-sized enterprises (SMEs) with limited budgets. These costs include not only software and hardware but also ongoing maintenance, training, and specialized personnel, which can be prohibitive. The sheer complexity of integrating disparate security tools and managing a fragmented security infrastructure also poses a considerable hurdle, leading to operational inefficiencies and potential security gaps.

Another significant restraint is the persistent shortage of skilled cybersecurity professionals globally. This talent gap makes it difficult for organizations to effectively deploy, manage, and optimize their cyber defense systems, often leading to underutilized tools and increased reliance on outsourced services, which can further inflate costs. Additionally, the rapid pace of technological change means that security solutions can become obsolete quickly, requiring continuous investment in upgrades and new technologies. The reluctance of some organizations to fully embrace new security paradigms or to allocate sufficient resources due to a perceived lower priority compared to other business functions also acts as a restraint, leaving them vulnerable to evolving threats.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of Implementation and Maintenance | -2.1% | Global, particularly SMEs | 2025-2033 (Ongoing) |

| Shortage of Skilled Cybersecurity Professionals | -1.8% | North America, Europe, APAC | 2025-2033 (Long-term) |

| Complexity of Integrating Disparate Security Solutions | -1.5% | Global | 2025-2030 (Medium-term) |

| Rapid Technological Obsolescence of Security Tools | -1.0% | Global | 2025-2033 (Ongoing) |

Cyber Defense Market Opportunities Analysis

The Cyber Defense market presents numerous opportunities driven by technological advancements and evolving enterprise needs. The increasing adoption of Artificial Intelligence and Machine Learning (AI/ML) within security solutions offers a significant avenue for growth, enabling more predictive, proactive, and automated threat detection and response. This shift reduces reliance on manual processes and enhances the overall efficiency of security operations, creating demand for AI/ML-driven platforms that can adapt to sophisticated and dynamic threat landscapes. Furthermore, the expansion of managed security services (MSSP) and security-as-a-service (SaaS) models provides significant opportunities. Organizations, particularly SMEs and those facing talent shortages, are increasingly outsourcing their security needs, leading to a surge in demand for comprehensive, scalable, and cost-effective managed offerings that provide 24/7 monitoring and expertise without the need for extensive in-house resources.

Another key opportunity lies in the growing focus on industry-specific security solutions tailored to the unique compliance and operational requirements of sectors like healthcare, finance, and critical infrastructure. As digital transformation permeates these industries, specialized cyber defense solutions addressing sector-specific vulnerabilities and regulatory mandates will see increased adoption. The rising importance of identity and access management (IAM) and privileged access management (PAM) to secure hybrid workforces and multi-cloud environments also represents a substantial growth area. Moreover, the emergence of quantum computing poses both a threat and an opportunity, driving research and development into post-quantum cryptography, which will open new markets for future-proof security solutions. Collaboration and threat intelligence sharing platforms also represent an opportunity for collective defense mechanisms against sophisticated adversaries, fostering a more resilient global cybersecurity ecosystem.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration of AI and Machine Learning in Security Solutions | +3.2% | Global | 2025-2033 (Long-term) |

| Growing Demand for Managed Security Services (MSSP) and SaaS | +2.8% | North America, Europe, Asia Pacific | 2025-2033 (Ongoing) |

| Expansion of Identity and Access Management (IAM) Solutions | +2.5% | Global | 2025-2030 (Medium-term) |

| Development of Industry-Specific and Verticalized Security Solutions | +1.9% | Global | 2026-2033 (Mid- to Long-term) |

| Emergence of Post-Quantum Cryptography | +0.8% | North America, Europe | 2028-2033 (Long-term, nascent) |

Cyber Defense Market Challenges Impact Analysis

The Cyber Defense market faces several significant challenges that can impede its growth and the effectiveness of deployed solutions. The primary challenge is the perpetually evolving and increasingly sophisticated threat landscape, where cybercriminals and nation-state actors constantly develop new attack techniques, making it difficult for defense mechanisms to keep pace. This requires continuous investment in research and development and agile adaptation from security vendors, creating a race against time. Another critical challenge is the sheer volume of security alerts generated by various systems, leading to "alert fatigue" among security analysts. This can cause legitimate threats to be overlooked amidst the noise, making efficient incident response more difficult and increasing the risk of breaches.

Furthermore, the integration of diverse and often incompatible security solutions from multiple vendors presents a significant challenge. Organizations frequently suffer from "vendor sprawl," leading to complex, fragmented security architectures that are difficult to manage, operate, and optimize. This lack of interoperability can create blind spots and inefficiencies, undermining the overall security posture. Additionally, geopolitical tensions and cyber warfare contribute to market volatility, as organizations and critical infrastructure become targets in broader conflicts. Balancing comprehensive security with budget constraints and ensuring return on investment for cybersecurity expenditures also remains a persistent challenge for many organizations, particularly given the intangible nature of prevented attacks.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapidly Evolving and Sophisticated Threat Landscape | -2.0% | Global | 2025-2033 (Ongoing) |

| Alert Fatigue and Overwhelm for Security Analysts | -1.7% | Global | 2025-2030 (Medium-term) |

| Complexity of Security Integrations and Vendor Sprawl | -1.4% | Global, particularly large enterprises | 2025-2033 (Ongoing) |

| Budget Constraints and Proving ROI for Security Investments | -1.1% | Global, particularly SMEs | 2025-2033 (Ongoing) |

| Geopolitical Instability and Increased State-Sponsored Cyberattacks | -0.9% | Global | 2025-2030 (Medium-term) |

Cyber Defense Market - Updated Report Scope

This report provides an in-depth analysis of the global Cyber Defense Market, offering comprehensive insights into market size, growth trends, key drivers, restraints, opportunities, and challenges across various segments and regions. It meticulously examines the competitive landscape, profiling leading companies and their strategic initiatives, alongside an extensive segmentation analysis covering solution types, deployment models, organization sizes, and end-use verticals. The report leverages extensive primary and secondary research to deliver a robust forecast from 2025 to 2033, serving as a critical resource for stakeholders, investors, and industry participants seeking to make informed decisions within this dynamic sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 285.5 Billion |

| Market Forecast in 2033 | USD 752.1 Billion |

| Growth Rate | 12.8% CAGR |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Microsoft, IBM, Palo Alto Networks, Fortinet, Cisco, CrowdStrike, Zscaler, Okta, Splunk, Check Point Software Technologies, Broadcom (Symantec), Trellix (McAfee Enterprise), Sophos, CyberArk, Rapid7, SentinelOne, Darktrace, FireEye (Mandiant), Qualys, Proofpoint |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Cyber Defense market is extensively segmented to provide a granular understanding of its diverse components and evolving demand patterns. This segmentation encompasses various dimensions, including solution types, services, deployment models, organization sizes, and end-use verticals, reflecting the multifaceted nature of modern cybersecurity requirements. The solution segment analyzes the demand for specific defense technologies such as network security, endpoint security, cloud security, application security, data security, and identity and access management, each addressing distinct aspects of an organization's digital perimeter. Services, including professional and managed security services, highlight the growing trend towards outsourcing security operations and expertise to specialized providers.

Furthermore, the market is differentiated by deployment models, distinguishing between on-premise, cloud, and hybrid solutions, reflecting varied infrastructure preferences and scalability needs. Organization size segmentation, separating small & medium enterprises from large enterprises, reveals differences in budget allocation, complexity of security needs, and adoption rates of advanced solutions. Finally, the end-use vertical analysis provides insights into the unique security challenges and regulatory compliance requirements across critical sectors such as BFSI, IT & Telecom, Government, Healthcare, Manufacturing, and Retail, enabling targeted market strategies and specialized product development.

- By Solution:

- Network Security (Firewalls, IDS/IPS, VPN, DDoS Protection)

- Endpoint Security (Antivirus/Anti-Malware, EDR, EPP)

- Cloud Security (CASB, CWPP, CSPM)

- Application Security (SAST, DAST, WAF)

- Data Security (Encryption, DLP, Database Security)

- Identity and Access Management (IAM, PAM, MFA)

- Security Information and Event Management (SIEM)

- Threat Intelligence

- Security Orchestration, Automation, and Response (SOAR)

- Other Solutions

- By Service:

- Professional Services (Consulting, Implementation, Support)

- Managed Security Services (MSSP)

- By Deployment:

- On-Premise

- Cloud

- Hybrid

- By Organization Size:

- Small & Medium Enterprises (SMEs)

- Large Enterprises

- By End Use Vertical:

- BFSI (Banking, Financial Services, and Insurance)

- IT and Telecom

- Government and Defense

- Healthcare

- Retail and E-commerce

- Manufacturing

- Energy and Utilities

- Other Verticals

Regional Highlights

- North America: This region is a dominant force in the Cyber Defense market, characterized by early adoption of advanced security technologies, stringent regulatory compliance, and a high concentration of cybersecurity solution providers. The presence of major technology hubs, significant R&D investments, and a robust awareness of evolving cyber threats contribute to its market leadership. The United States, in particular, drives substantial demand across government, defense, and critical infrastructure sectors.

- Europe: Europe represents a significant market, fueled by comprehensive data protection regulations like GDPR and increasing investments in digital transformation initiatives. Countries such as the UK, Germany, and France are at the forefront of adopting advanced cyber defense solutions, driven by a growing awareness of cyber risks and the need to protect sensitive data and critical national infrastructure. The region also sees a strong focus on cybersecurity talent development and cross-border threat intelligence sharing.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region, driven by rapid digitalization, increasing internet penetration, and a surge in cyberattacks targeting emerging economies. Countries like China, India, Japan, and Australia are witnessing substantial investments in cybersecurity infrastructure, particularly in BFSI, IT & Telecom, and manufacturing sectors. Government initiatives to promote cybersecurity and digital sovereignty further accelerate market growth in this region.

- Latin America: This region is experiencing steady growth in the cyber defense market, primarily driven by increasing digital adoption, cloud migration, and a rising awareness of cybercrime. Brazil and Mexico are leading the charge, with growing investments in cybersecurity solutions to protect financial institutions, government data, and critical national infrastructure. The demand for managed security services is also notably increasing due to budget constraints and skills shortages.

- Middle East and Africa (MEA): The MEA region is witnessing significant investments in cybersecurity, particularly in the Gulf Cooperation Council (GCC) countries, driven by ambitious digitalization agendas, smart city initiatives, and the need to secure critical oil and gas infrastructure. Governments in this region are actively promoting cybersecurity frameworks and national defense strategies, contributing to a robust demand for advanced cyber defense solutions. Challenges persist, but opportunities are expanding due to economic diversification efforts and increased foreign investment.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Cyber Defense Market.- Microsoft

- IBM

- Palo Alto Networks

- Fortinet

- Cisco

- CrowdStrike

- Zscaler

- Okta

- Splunk

- Check Point Software Technologies

- Broadcom (Symantec)

- Trellix (McAfee Enterprise)

- Sophos

- CyberArk

- Rapid7

- SentinelOne

- Darktrace

- FireEye (Mandiant)

- Qualys

- Proofpoint

Frequently Asked Questions

What is Cyber Defense?

Cyber Defense refers to the collective measures, strategies, and technologies designed to protect computer systems, networks, programs, and data from cyberattacks, damage, or unauthorized access. It encompasses various security disciplines aimed at preventing, detecting, responding to, and recovering from cyber threats to ensure data integrity, confidentiality, and availability.

Why is Cyber Defense important for businesses?

Cyber Defense is crucial for businesses to protect sensitive data, maintain operational continuity, safeguard intellectual property, and preserve customer trust. It helps mitigate financial losses from breaches, avoids reputational damage, ensures compliance with data protection regulations, and provides a secure foundation for digital transformation and innovation.

What are the primary drivers of the Cyber Defense market growth?

The primary drivers include the escalating volume and sophistication of cyberattacks, the pervasive digital transformation across industries, stringent regulatory compliance mandates, the widespread adoption of cloud computing and IoT devices, and the increasing geopolitical tensions contributing to nation-state sponsored cyber threats.

How is AI impacting Cyber Defense?

AI significantly impacts Cyber Defense by enhancing threat detection through anomaly recognition, automating incident response, improving predictive analytics for vulnerabilities, and optimizing security operations. However, it also presents challenges as malicious actors can leverage AI for more sophisticated and evasive attacks.

What are the key trends shaping the future of Cyber Defense?

Key trends include the widespread adoption of Zero Trust architectures, a heightened focus on supply chain security, the continuous expansion of cloud-native security solutions, growing demand for advanced threat intelligence and security orchestration automation and response (SOAR) platforms, and the increasing convergence of IT, OT, and IoT security.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted