Cyanoacrylate Adhesive Market

Cyanoacrylate Adhesive Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709028 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

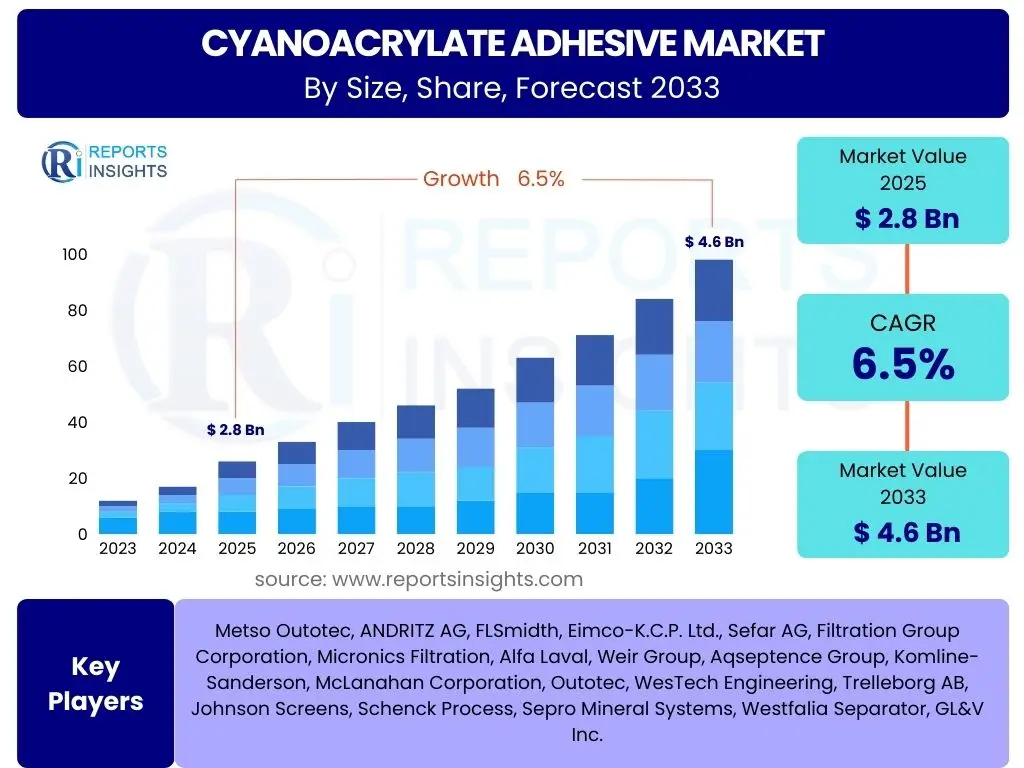

Cyanoacrylate Adhesive Market Size

According to Reports Insights Consulting Pvt Ltd, The Cyanoacrylate Adhesive Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2025 and 2033. The market is estimated at USD 2.8 Billion in 2025 and is projected to reach USD 4.6 Billion by the end of the forecast period in 2033.

Key Cyanoacrylate Adhesive Market Trends & Insights

The cyanoacrylate adhesive market is currently experiencing significant transformative trends driven by advancements in material science, increasing demand from high-growth industrial sectors, and a strong emphasis on sustainability. Users frequently inquire about how these market dynamics are shaping product development, application areas, and the competitive landscape. Key insights reveal a persistent push towards specialized formulations tailored for specific, high-performance applications, moving beyond general-purpose super glues to highly engineered solutions.

Another prominent trend involves the growing adoption of cyanoacrylates in medical and wearable electronics, where their rapid curing and strong bonding properties are highly advantageous. The market is also witnessing a surge in demand for low-odor, low-bloom, and non-toxic formulations, addressing environmental concerns and user comfort, especially in consumer and medical applications. Furthermore, the integration of automation in manufacturing processes is increasing the need for adhesives that can facilitate faster assembly lines and improve production efficiency.

- Growing demand for specialized formulations in medical and electronics.

- Increased focus on sustainable, low-odor, and low-bloom cyanoacrylates.

- Advancements in rapid-curing and high-performance variants.

- Integration of cyanoacrylates in automated assembly processes.

- Expansion into new application areas such as wearable technology and advanced composites.

AI Impact Analysis on Cyanoacrylate Adhesive

Artificial intelligence (AI) is poised to exert a substantial influence across the cyanoacrylate adhesive value chain, from research and development to manufacturing and quality control. Common user questions revolve around how AI can accelerate new product discovery, optimize formulation, enhance process efficiency, and predict adhesive performance. AI’s capacity to analyze vast datasets of chemical compounds and their properties can significantly reduce the time and cost associated with developing novel adhesive materials, leading to customized solutions for complex bonding challenges.

In manufacturing, AI-powered predictive maintenance can optimize equipment uptime and improve consistency in production, while machine learning algorithms can analyze real-time production data to adjust parameters for optimal yield and quality. Moreover, AI can revolutionize quality assurance by detecting microscopic defects or inconsistencies that human inspection might miss, ensuring higher product reliability. The ability of AI to simulate various environmental conditions and predict adhesive longevity also offers immense value in product development and application engineering, providing deeper insights into material behavior under stress.

- Accelerated R&D through AI-driven material discovery and formulation optimization.

- Enhanced manufacturing efficiency via AI-powered process control and predictive maintenance.

- Improved quality assurance and defect detection using machine learning algorithms.

- Predictive performance modeling for adhesive behavior under various conditions.

- Supply chain optimization through AI-driven demand forecasting and inventory management.

Key Takeaways Cyanoacrylate Adhesive Market Size & Forecast

The cyanoacrylate adhesive market is positioned for robust growth over the forecast period, driven by its versatile applications and continuous innovation. Users frequently seek concise summaries of the market's trajectory, key growth drivers, and factors influencing its expansion. A primary takeaway is the escalating demand from specialized industries, particularly healthcare and electronics, where the unique properties of cyanoacrylates provide indispensable solutions for complex bonding requirements. The market's resilience is also attributed to ongoing advancements in product formulations that address specific industry needs, such as improved temperature resistance or flexibility.

Furthermore, the increasing adoption of automation in manufacturing across various sectors underpins the consistent demand for fast-curing and high-strength adhesives like cyanoacrylates. The global market is expected to expand significantly, reflecting both volume growth in traditional applications and value growth from high-performance, custom-formulated products. Regional market dynamics, with strong growth in Asia Pacific and North America, also represent a crucial element of the overall market forecast, highlighting regional opportunities and competitive landscapes.

- Sustained growth projected with a CAGR of 6.5% reaching USD 4.6 Billion by 2033.

- Strong demand stemming from medical, electronics, and automotive industries.

- Continuous innovation in product formulation to meet specialized application needs.

- Increasing integration into automated manufacturing processes globally.

- Asia Pacific and North America identified as key growth regions.

Cyanoacrylate Adhesive Market Drivers Analysis

The expansion of the cyanoacrylate adhesive market is fundamentally propelled by several critical factors that underscore its indispensability across various industries. These drivers primarily relate to technological advancements, evolving industrial requirements, and increasing product versatility. The rapid cure time and high bond strength of cyanoacrylates make them ideal for high-speed assembly lines, which are becoming standard in modern manufacturing, thereby boosting their adoption in automated processes.

Furthermore, the miniaturization of electronic components and the increasing complexity of medical devices necessitate adhesives that can provide precision bonding in extremely small or sensitive applications without compromising performance. Cyanoacrylates excel in these environments, offering reliable adhesion with minimal material usage. The continuous development of specialized formulations, such as those with improved flexibility, impact resistance, or thermal stability, also broadens their application scope, catering to more demanding industrial requirements and fostering market growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing demand from medical and electronics industries | +1.8% | North America, Europe, Asia Pacific | Medium-term (3-5 years) |

| Growing adoption in automotive and transportation sectors | +1.5% | Asia Pacific, Europe, North America | Medium-term (3-5 years) |

| Technological advancements in product formulation | +1.2% | Global | Long-term (5+ years) |

| Shift towards automation in manufacturing processes | +1.0% | Global | Short-term (1-3 years) |

| Miniaturization of electronic devices | +0.8% | Asia Pacific, North America | Medium-term (3-5 years) |

Cyanoacrylate Adhesive Market Restraints Analysis

Despite its significant growth prospects, the cyanoacrylate adhesive market faces several notable restraints that could temper its expansion. A primary concern is the relatively low heat resistance of standard cyanoacrylate formulations, which limits their applicability in high-temperature environments. This characteristic often necessitates the use of more specialized, and consequently more expensive, variants or alternative adhesive technologies in certain demanding industrial applications.

Another significant restraint is the regulatory scrutiny surrounding the use of certain chemical components in cyanoacrylates, particularly regarding health and safety. Strict environmental regulations and concerns about volatile organic compound (VOC) emissions can lead to compliance challenges and higher development costs for manufacturers. Furthermore, the brittleness of some cyanoacrylate bonds, especially under impact or peel stress, restricts their use in applications requiring high flexibility or dynamic load-bearing, driving users towards more robust, albeit slower-curing, alternatives.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Limited temperature resistance of standard formulations | -0.9% | Global | Long-term (5+ years) |

| Regulatory scrutiny and environmental concerns | -0.7% | Europe, North America | Medium-term (3-5 years) |

| Brittleness of certain cyanoacrylate bonds | -0.6% | Global | Medium-term (3-5 years) |

| Competition from alternative adhesive technologies | -0.5% | Global | Short-term (1-3 years) |

| Skin and eye irritation associated with uncured adhesive | -0.4% | Global | Short-term (1-3 years) |

Cyanoacrylate Adhesive Market Opportunities Analysis

The cyanoacrylate adhesive market is replete with significant opportunities stemming from evolving technological landscapes, emerging applications, and a growing emphasis on product innovation. A key opportunity lies in the development of advanced formulations that overcome existing limitations, such as those offering enhanced flexibility, improved heat resistance, or specialized bonding for difficult-to-bond substrates like certain plastics and composites. Such innovations will unlock new markets and expand penetration in existing ones where conventional cyanoacrylates fall short.

Moreover, the burgeoning markets for wearable electronics, electric vehicles, and advanced medical implants present substantial growth avenues. These sectors demand high-performance, fast-curing, and often biocompatible adhesives, which cyanoacrylates are uniquely positioned to provide with further development. The shift towards sustainable and eco-friendly products also creates opportunities for manufacturers to invest in bio-based or low-VOC cyanoacrylate formulations, catering to environmentally conscious consumers and stringent regulatory frameworks, thereby gaining a competitive edge and fostering long-term market expansion.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of advanced, high-performance formulations | +1.3% | Global | Long-term (5+ years) |

| Expansion into emerging applications (wearables, EVs, medical implants) | +1.1% | Asia Pacific, North America, Europe | Medium-term (3-5 years) |

| Growing demand for sustainable and eco-friendly products | +0.9% | Europe, North America | Long-term (5+ years) |

| Increased penetration in Asia Pacific's manufacturing sector | +0.8% | Asia Pacific | Short-term (1-3 years) |

| Customization for niche industrial bonding requirements | +0.6% | Global | Medium-term (3-5 years) |

Cyanoacrylate Adhesive Market Challenges Impact Analysis

The cyanoacrylate adhesive market faces a set of intrinsic and external challenges that necessitate strategic responses from industry players. One significant challenge is managing the short shelf life and sensitive storage requirements of many cyanoacrylate formulations, which can lead to product degradation if not handled correctly. This impacts logistics, inventory management, and ultimately product efficacy for end-users, requiring careful supply chain management and consumer education.

Furthermore, intense competition from other adhesive technologies, such as epoxies, silicones, and UV-curable adhesives, poses a continuous challenge, especially in applications where cyanoacrylates' limitations (e.g., impact strength, gap filling) become prominent. The need to balance performance with cost-effectiveness is also a constant struggle, particularly in price-sensitive markets. Navigating the complex global regulatory landscape for chemical substances and ensuring compliance across diverse regions also presents a significant hurdle for manufacturers operating on an international scale, requiring substantial investment in research and regulatory affairs.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Short shelf life and sensitive storage conditions | -0.8% | Global | Short-term (1-3 years) |

| Competition from alternative adhesive technologies | -0.7% | Global | Medium-term (3-5 years) |

| Price sensitivity and cost pressures in various applications | -0.6% | Asia Pacific, Latin America | Medium-term (3-5 years) |

| Regulatory compliance and chemical management complexities | -0.5% | Europe, North America | Long-term (5+ years) |

| Need for specialized dispensing equipment in industrial settings | -0.4% | Global | Short-term (1-3 years) |

Cyanoacrylate Adhesive Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global cyanoacrylate adhesive market, offering critical insights into its current landscape, historical performance, and future growth trajectories. The scope encompasses detailed market sizing, segmentation analysis by type, application, and end-use industry, alongside a thorough examination of regional dynamics. It also delves into the competitive environment, profiling key market participants and assessing their strategic initiatives.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.8 Billion |

| Market Forecast in 2033 | USD 4.6 Billion |

| Growth Rate | 6.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Henkel AG & Co. KGaA, 3M Company, H.B. Fuller Company, Sika AG, Arkema S.A., Dymax Corporation, Master Bond Inc., Permabond LLC, Huntsman Corporation, Ashland Global Holdings Inc., Bostik (an Arkema company), Illinois Tool Works Inc. (ITW), WEICON GmbH & Co. KG, Toagosei Co., Ltd., Avery Dennison Corporation, Dow Inc., Lord Corporation, Showa Denko K.K., Parson Adhesives Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The cyanoacrylate adhesive market is meticulously segmented to provide a granular understanding of its diverse applications and product types, facilitating targeted market strategies and investment decisions. These segmentations are crucial for identifying specific growth pockets and understanding user preferences across various industries. By categorizing the market based on chemical composition, application, and end-use, a clear picture emerges of where demand is strongest and where future opportunities lie for specific formulations.

The segmentation by type, such as Ethyl, Methyl, and Butyl cyanoacrylates, highlights the chemical diversity and their inherent properties that dictate suitability for different substrates and environments. Application-based segmentation, encompassing medical, electronics, and automotive, among others, illustrates the broad utility of these adhesives across critical industrial sectors. Finally, end-use industry segmentation provides insight into the ultimate consumer of these adhesives, offering a macro view of market demand from sectors like healthcare, transportation, and construction.

- By Type:

- Ethyl Cyanoacrylate

- Methyl Cyanoacrylate

- Butyl Cyanoacrylate

- Allyl Cyanoacrylate

- Methoxyethyl Cyanoacrylate

- Other Types

- By Application:

- Medical & Dental

- Electronics

- Automotive

- Industrial

- Construction

- Consumer Goods

- Other Applications

- By End-Use Industry:

- Healthcare

- Transportation

- Electrical & Electronics

- Packaging

- Building & Construction

- Others

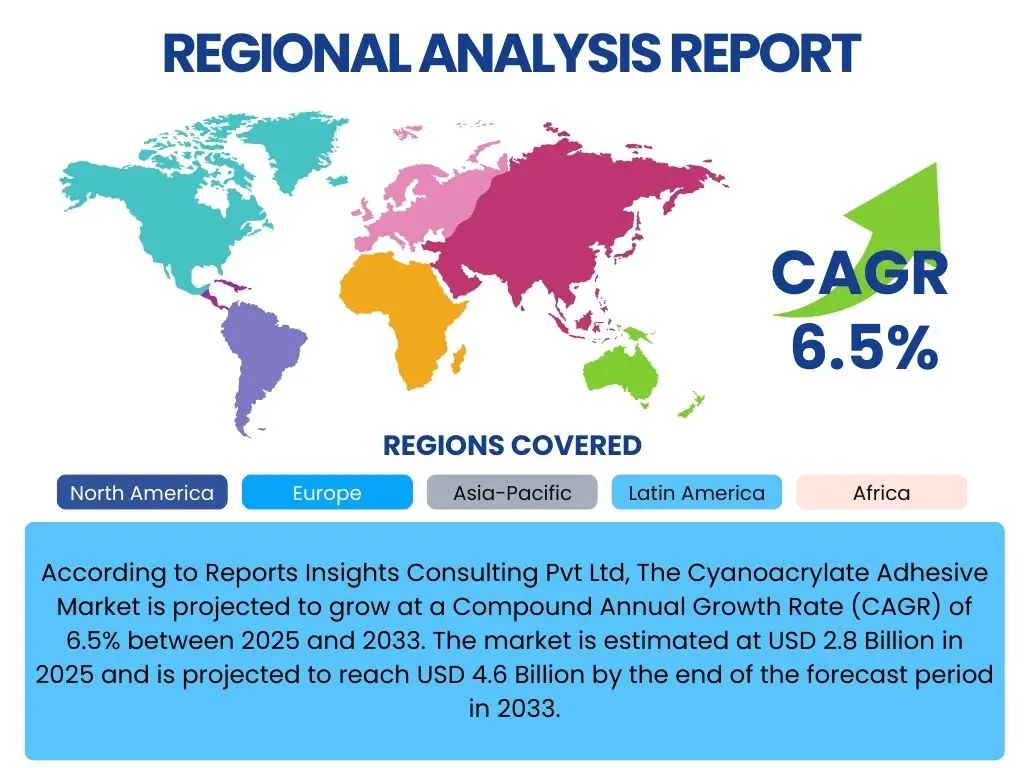

Regional Highlights

Geographical analysis reveals significant disparities in the adoption and growth of cyanoacrylate adhesives across the globe, influenced by varying industrialization levels, regulatory frameworks, and technological advancements. Asia Pacific currently dominates the market, driven by its robust manufacturing sector, expanding electronics production, and increasing automotive industry. Countries like China, India, Japan, and South Korea are key contributors to this regional growth, experiencing rapid industrial development and technological innovation that fuel demand for high-performance adhesives.

North America and Europe represent mature markets for cyanoacrylate adhesives, characterized by a strong emphasis on specialized applications in healthcare, aerospace, and advanced electronics. These regions are also at the forefront of developing sustainable and high-performance formulations, driven by stringent environmental regulations and a demand for innovative solutions. Latin America, the Middle East, and Africa are emerging markets, showing considerable potential for growth as industrialization accelerates and demand for construction, automotive, and consumer goods manufacturing increases.

- Asia Pacific: Dominant market share due to strong manufacturing bases in electronics, automotive, and general industrial sectors, particularly in China, India, and Japan.

- North America: Significant demand from medical devices, aerospace, and high-tech electronics industries, with a focus on specialized and high-performance formulations.

- Europe: Mature market with a strong emphasis on automotive, construction, and precision engineering, alongside a growing focus on sustainable and compliant adhesive solutions.

- Latin America: Emerging market with increasing industrialization and growing demand from automotive, construction, and consumer goods sectors.

- Middle East and Africa: Growing market driven by infrastructure development, automotive assembly, and expansion of local manufacturing capabilities.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Cyanoacrylate Adhesive Market.- Henkel AG & Co. KGaA

- 3M Company

- H.B. Fuller Company

- Sika AG

- Arkema S.A.

- Dymax Corporation

- Master Bond Inc.

- Permabond LLC

- Huntsman Corporation

- Ashland Global Holdings Inc.

- Bostik (an Arkema company)

- Illinois Tool Works Inc. (ITW)

- WEICON GmbH & Co. KG

- Toagosei Co., Ltd.

- Avery Dennison Corporation

- Dow Inc.

- Lord Corporation (a Parker Hannifin company)

- Showa Denko K.K.

- Parson Adhesives Inc.

- Royal Adhesives & Sealants (an H.B. Fuller Company)

- DELO Industrial Adhesives

Frequently Asked Questions

Analyze common user questions about the Cyanoacrylate Adhesive market and generate a concise list of summarized FAQs reflecting key topics and concerns.What are the primary types of cyanoacrylate adhesives?

The primary types of cyanoacrylate adhesives include Ethyl Cyanoacrylate, Methyl Cyanoacrylate, and Butyl Cyanoacrylate, each offering distinct properties suited for various applications. Ethyl Cyanoacrylates are common for general use, Methyl for metals, and Butyl for medical applications due to their lower toxicity.

Which industries are the biggest consumers of cyanoacrylate adhesives?

The largest consuming industries for cyanoacrylate adhesives are electronics, medical & dental, automotive, and general industrial applications. Their rapid curing and strong bonding capabilities make them ideal for these sectors requiring precision and efficiency.

What are the key benefits of using cyanoacrylate adhesives?

Key benefits include extremely rapid curing at room temperature, high bond strength on a variety of substrates, solvent-free formulations, and suitability for automated assembly lines. They offer excellent adhesion for small bond areas and quick repairs.

What are the main challenges facing the cyanoacrylate adhesive market?

Major challenges include limited temperature resistance of standard formulations, brittleness under impact or peel stress, short shelf life, and increasing regulatory scrutiny regarding certain chemical components. Competition from other adhesive technologies also presents a significant hurdle.

How is Asia Pacific contributing to the cyanoacrylate adhesive market growth?

Asia Pacific is a leading growth region due to its expansive manufacturing base, particularly in electronics, automotive, and general industrial sectors. Rapid industrialization and a growing demand for advanced bonding solutions across countries like China, India, and Japan are driving significant market expansion.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted