Cut and Stack Label Market

Cut and Stack Label Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709005 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

Cut and Stack Label Market Size

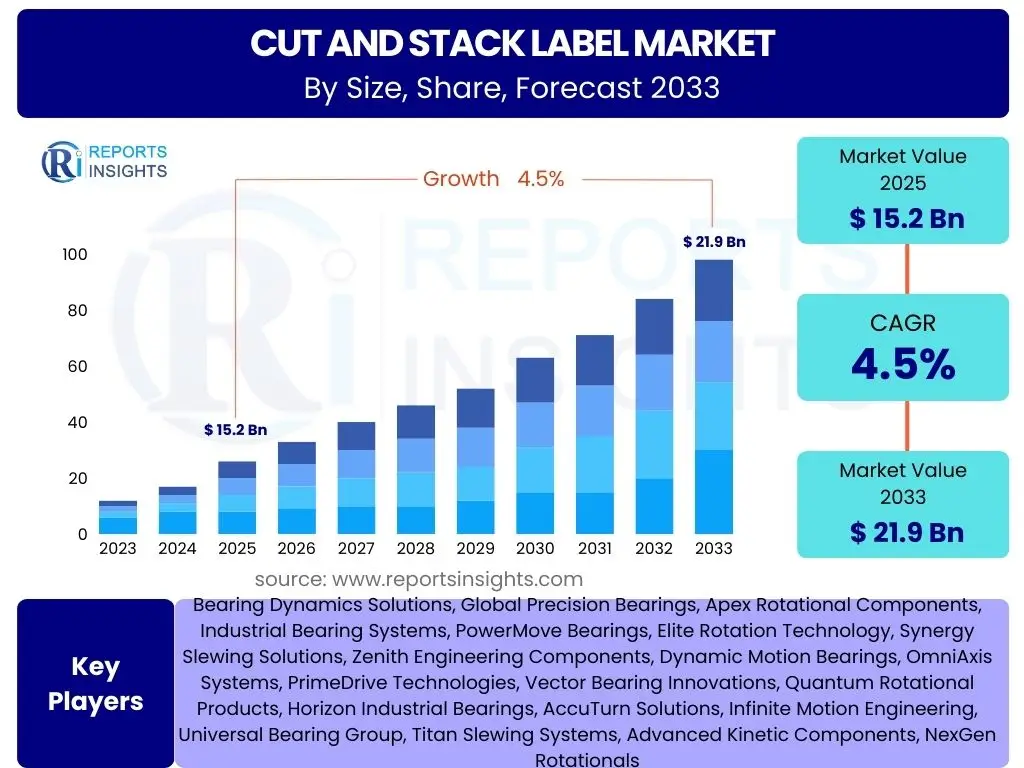

According to Reports Insights Consulting Pvt Ltd, The Cut and Stack Label Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.5% between 2025 and 2033. The market is estimated at USD 15.2 billion in 2025 and is projected to reach USD 21.9 billion by the end of the forecast period in 2033.

Key Cut and Stack Label Market Trends & Insights

The Cut and Stack Label market is experiencing dynamic shifts driven by consumer preferences, technological advancements, and a growing emphasis on sustainability. Users frequently inquire about the impact of eco-friendly practices on label production and the integration of digital printing solutions. The market is increasingly characterized by a demand for visually appealing and durable labels that also adhere to environmental standards, pushing manufacturers to innovate in materials and processes.

Another significant area of interest revolves around the adoption of smart packaging features and enhanced label functionalities. Brands are seeking labels that can offer more than just product information, incorporating elements like QR codes, NFC tags, and augmented reality (AR) capabilities to engage consumers and provide traceability. This trend is particularly prominent in sectors such as food and beverage, personal care, and pharmaceuticals, where consumer interaction and product transparency are paramount.

Furthermore, the market is witnessing a move towards greater customization and shorter print runs, fueled by the proliferation of diverse product SKUs and targeted marketing campaigns. This necessitates flexible and efficient printing technologies, making digital and hybrid presses more attractive. The evolving regulatory landscape, particularly concerning food contact materials and recyclability, also significantly shapes product development and market strategies, compelling companies to invest in compliant and future-proof labeling solutions.

- Growing demand for sustainable and recyclable label materials.

- Increased adoption of digital printing technologies for customization and efficiency.

- Integration of smart label features for enhanced consumer engagement and traceability.

- Focus on high-quality graphics and premium aesthetics to differentiate products.

- Expansion in emerging markets driven by rising disposable incomes and consumerism.

AI Impact Analysis on Cut and Stack Label

Artificial Intelligence (AI) is poised to significantly transform the Cut and Stack Label market by enhancing operational efficiency, optimizing design processes, and improving quality control. Users are keen to understand how AI can automate repetitive tasks, reduce material waste, and streamline the entire label production workflow. AI-powered systems can analyze vast datasets to predict equipment maintenance needs, manage inventory more effectively, and even optimize printing parameters for superior output, leading to substantial cost savings and increased productivity for label manufacturers.

The application of AI extends to the design and pre-press stages, where it can assist in generating innovative label designs, ensuring brand consistency, and adapting layouts for different package types and sizes. AI algorithms can evaluate design effectiveness based on consumer preferences and market trends, providing valuable insights to accelerate product development. This capability allows brands to respond more quickly to market demands with visually compelling and functionally optimized labels.

Moreover, AI is expected to revolutionize quality inspection processes, moving beyond traditional manual checks to highly accurate, automated defect detection systems. AI-driven vision systems can identify printing errors, color inconsistencies, and material flaws at high speeds, significantly reducing the chances of defective products reaching the market. This not only upholds brand reputation but also minimizes rework and waste, contributing to a more sustainable and efficient manufacturing paradigm in the Cut and Stack Label sector.

- Automated quality control and defect detection through AI-powered vision systems.

- Optimization of production schedules and inventory management with predictive analytics.

- Enhanced design capabilities and rapid prototyping facilitated by generative AI.

- Reduced material waste and energy consumption through AI-driven process optimization.

- Improved supply chain visibility and traceability using AI to analyze data.

Key Takeaways Cut and Stack Label Market Size & Forecast

The Cut and Stack Label market is on a robust growth trajectory, primarily fueled by the expanding packaging industry and the increasing demand for high-quality, cost-effective labeling solutions across various end-use sectors. A key takeaway is the consistent growth in the food and beverage industry, which remains the largest application segment, alongside the burgeoning pharmaceutical and personal care sectors. The market's resilience is also attributed to its adaptability in incorporating advanced printing technologies and sustainable materials to meet evolving consumer and regulatory demands.

Furthermore, the forecast indicates a significant shift towards greater product differentiation through innovative label designs and enhanced functionalities. Manufacturers are strategically investing in machinery that offers greater flexibility and efficiency, such as advanced rotogravure and offset presses, while also exploring hybrid digital solutions. This investment strategy aims to cater to the growing trend of customized packaging and shorter production runs, ensuring competitiveness in a dynamic market landscape.

Geographically, emerging economies are poised to become major growth engines, driven by rapid industrialization, urbanization, and increasing consumer disposable incomes. These regions present substantial opportunities for market players to expand their footprint. Overall, the market's future will be shaped by a balance between cost-efficiency, aesthetic appeal, and environmental responsibility, with technological innovation serving as a critical enabler for sustained expansion and value creation.

- Consistent growth driven by expanding food, beverage, and personal care sectors.

- Emphasis on premiumization and customization necessitating advanced printing solutions.

- Significant opportunities in emerging economies due to rising consumer spending.

- Strategic investments in sustainable materials and production processes are crucial for market leadership.

- Technological advancements, including digital printing and smart labels, will redefine market offerings.

Cut and Stack Label Market Drivers Analysis

The proliferation of the packaged food and beverage industry globally stands as a primary catalyst for the Cut and Stack Label market. As consumer lifestyles become more convenience-oriented, the demand for packaged goods, ranging from dairy products to snacks and beverages, continues to surge. Cut and stack labels, known for their cost-effectiveness and versatility in various printing techniques, offer an ideal solution for branding these high-volume products, directly translating into increased market demand.

Beyond the food and beverage sector, the personal care and pharmaceutical industries also significantly contribute to market expansion. These sectors require labels that convey brand identity, product information, and regulatory compliance with high clarity and aesthetic appeal. Cut and stack labels provide the durability and print quality necessary for such applications, capable of withstanding various environmental conditions while maintaining their visual integrity.

Technological advancements in printing machinery and materials further propel market growth. Innovations in high-speed presses, improved ink technologies, and the development of new substrates allow for more efficient production, enhanced visual effects, and greater sustainability. These advancements enable manufacturers to produce complex and visually appealing labels at competitive prices, meeting the evolving demands of brand owners for distinctive and environmentally responsible packaging.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Packaged Food & Beverage Industry | +1.5% | Global, particularly Asia Pacific & Latin America | Short to Mid-term (2025-2030) |

| Demand for Cost-Effective & High-Quality Labels | +1.0% | North America, Europe, Asia Pacific | Mid to Long-term (2027-2033) |

| Advancements in Printing Technology | +0.8% | Global, driven by developed economies | Mid to Long-term (2028-2033) |

| Expansion of Personal Care & Pharmaceutical Industries | +0.7% | North America, Europe, China, India | Short to Mid-term (2026-2031) |

Cut and Stack Label Market Restraints Analysis

The volatility of raw material prices, particularly for paper and film substrates, poses a significant restraint on the Cut and Stack Label market. Fluctuations in pulp prices, petrochemical derivatives, and energy costs directly impact production expenses, leading to increased operational costs for label manufacturers. These cost instabilities can compel manufacturers to absorb higher expenses or pass them onto consumers, potentially affecting market competitiveness and profit margins, especially for smaller players.

Intense competition from alternative labeling technologies, such as pressure-sensitive labels, in-mold labels (IML), and shrink sleeves, also acts as a considerable restraint. While cut and stack labels offer cost advantages, other technologies provide benefits like enhanced aesthetics, higher durability, or specific application characteristics that may be preferred by certain brands. The continuous innovation and cost reductions in these alternative segments create pressure on the Cut and Stack Label market to maintain its competitive edge.

Furthermore, stringent environmental regulations regarding packaging waste and material recyclability present challenges. Manufacturers are increasingly required to comply with stricter guidelines on material sourcing, production processes, and end-of-life disposal. Adapting to these regulations often involves significant investment in new materials and technologies, which can slow down innovation cycles and increase product development costs, particularly in regions with advanced environmental policies.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Raw Material Price Volatility | -0.9% | Global | Short-term to Mid-term (2025-2029) |

| Competition from Alternative Label Technologies | -0.7% | Global, particularly developed markets | Mid-term (2027-2032) |

| Stringent Environmental Regulations | -0.5% | Europe, North America | Mid-term to Long-term (2028-2033) |

Cut and Stack Label Market Opportunities Analysis

The burgeoning growth in emerging economies, particularly in Asia Pacific and Latin America, presents significant opportunities for the Cut and Stack Label market. Rapid urbanization, increasing disposable incomes, and the expansion of organized retail in these regions are driving a surge in the consumption of packaged goods. This demographic shift creates a substantial demand for cost-effective and high-volume labeling solutions, which cut and stack labels are well-suited to provide, allowing market players to expand their geographical reach and customer base.

Innovation in sustainable and eco-friendly label materials offers another critical avenue for growth. As consumer awareness about environmental issues rises, there is a growing preference for packaging solutions that are recyclable, compostable, or made from renewable resources. Companies investing in the research and development of such materials, including recycled content paper and biodegradable films, can capture a growing segment of environmentally conscious brands and consumers, differentiating themselves in a competitive market.

Furthermore, the increasing demand for customized and visually appealing packaging provides an opportunity for manufacturers to offer value-added services. Brands are constantly seeking unique ways to capture consumer attention and enhance their product's shelf appeal. By leveraging advanced printing techniques, specialty finishes, and intricate designs, cut and stack label providers can cater to these premiumization trends, offering bespoke solutions that command higher margins and strengthen client relationships.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Emerging Economies | +1.2% | Asia Pacific, Latin America, MEA | Short to Mid-term (2025-2030) |

| Innovation in Sustainable Label Materials | +0.9% | Global, particularly Europe & North America | Mid to Long-term (2027-2033) |

| Increasing Demand for Customization & Premiumization | +0.8% | Global, driven by developed markets | Mid-term (2026-2031) |

| Technological Advancements in Digital Printing | +0.6% | Global | Mid to Long-term (2028-2033) |

Cut and Stack Label Market Challenges Impact Analysis

The primary challenge confronting the Cut and Stack Label market is the rising operational costs associated with labor, energy, and logistics. As manufacturing processes become more complex and supply chains extend globally, the expense of skilled labor, particularly in specialized printing and finishing roles, increases. Concurrently, escalating energy prices and intricate logistics networks for material procurement and product distribution add significant financial burdens, eroding profit margins and limiting investment in innovation for many players.

Maintaining consistent quality and ensuring rapid turnaround times in a highly competitive and demand-driven market also presents a substantial challenge. Brand owners require labels that are not only aesthetically perfect but also delivered promptly to meet tight production schedules. Any deviation in print quality or delays in delivery can result in significant financial penalties and damage to reputation, forcing manufacturers to invest heavily in robust quality assurance systems and efficient production planning.

Furthermore, adapting to rapid technological evolution, such as the rise of digital printing and smart packaging solutions, poses a challenge for traditional cut and stack label manufacturers. Integrating these new technologies requires significant capital investment in equipment, software, and employee training. Companies that fail to embrace or integrate these advancements risk falling behind competitors that offer more agile and innovative labeling solutions, potentially losing market share to more forward-thinking players.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rising Operational Costs (Labor, Energy, Logistics) | -0.8% | Global | Short to Mid-term (2025-2029) |

| Ensuring Quality & Fast Turnaround Times | -0.6% | Global, especially developed markets | Mid-term (2026-2031) |

| Adoption of New Printing Technologies (e.g., Digital) | -0.5% | Global | Mid to Long-term (2027-2033) |

| Managing Supply Chain Disruptions | -0.4% | Global | Short to Mid-term (2025-2028) |

Cut and Stack Label Market - Updated Report Scope

This report offers an in-depth analysis of the Cut and Stack Label market, providing a comprehensive overview of its current landscape, growth trajectory, and future outlook. It meticulously dissects market trends, drivers, restraints, opportunities, and challenges, offering actionable insights for stakeholders. The scope includes a thorough examination of various market segments by material, application, and end-use industry, alongside a detailed regional analysis, to present a holistic view of market dynamics and potential for expansion.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 15.2 Billion |

| Market Forecast in 2033 | USD 21.9 Billion |

| Growth Rate | 4.5% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Avery Dennison Corporation, CCL Industries Inc., Constantia Flexibles Group GmbH, Huhtamaki Oyj, Mondi plc, Multi-Color Corporation, UPM Raflatac, WestRock Company, Amcor plc, Bemis Company Inc. (now part of Amcor), Essel Propack Limited (now Esselunga), Coveris Holdings S.A., Fuji Seal International, Inc., Interflex Group, Smyth Companies, P.E. Labellers S.p.A., Heidelberg Druckmaschinen AG, KHS GmbH, Sidel S.A., Sacmi Imola S.C. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Cut and Stack Label market is intricately segmented across various dimensions to provide a granular understanding of its dynamics and growth prospects. These segmentations by material, printing technology, and application allow for a detailed examination of market performance within distinct categories, revealing key trends and demand patterns. Each segment's growth is influenced by unique drivers and faces specific challenges, necessitating tailored strategies for market penetration and expansion.

- By Material:

- Paper: Coated Paper, Uncoated Paper, Metallized Paper

- Film: Polypropylene (PP), Polyethylene (PE), Polyvinyl Chloride (PVC), Others

- By Printing Technology:

- Offset Printing

- Rotogravure Printing

- Flexographic Printing

- Digital Printing

- Others

- By Application:

- Food & Beverages: Dairy & Frozen Products, Baked Goods & Confectionery, Beverages, Processed Food, Others

- Personal Care: Cosmetics, Toiletries, Hair Care

- Pharmaceutical

- Home Care

- Industrial

- Others

- By Region:

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Regional Highlights

- Asia Pacific (APAC) is projected to exhibit the highest growth rate due to rapid industrialization, increasing population, rising disposable incomes, and the booming packaged food and beverage sector in countries like China, India, and Southeast Asian nations. The region is becoming a manufacturing hub, leading to high demand for cost-effective labeling solutions.

- North America holds a significant market share, driven by strong demand from the food and beverage, personal care, and pharmaceutical industries, coupled with a high adoption rate of advanced printing technologies and a focus on premium packaging.

- Europe is characterized by stringent environmental regulations and a strong emphasis on sustainable packaging, leading to innovation in eco-friendly label materials and production processes. Countries such as Germany, the UK, and France are key contributors to market value.

- Latin America is experiencing steady growth, fueled by urbanization, increasing consumer spending, and the expansion of the organized retail sector. Brazil and Mexico are leading markets within the region for packaged goods.

- Middle East and Africa (MEA) present emerging opportunities, particularly in the Gulf Cooperation Council (GCC) countries and South Africa, driven by economic diversification, infrastructure development, and growing consumer markets for packaged products.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Cut and Stack Label Market.- Avery Dennison Corporation

- CCL Industries Inc.

- Constantia Flexibles Group GmbH

- Huhtamaki Oyj

- Mondi plc

- Multi-Color Corporation

- UPM Raflatac

- WestRock Company

- Amcor plc

- Esselunga (formerly Essel Propack Limited)

- Coveris Holdings S.A.

- Fuji Seal International, Inc.

- Interflex Group

- Smyth Companies

- P.E. Labellers S.p.A.

- Heidelberg Druckmaschinen AG

- KHS GmbH

- Sidel S.A.

- Sacmi Imola S.C.

- ProAmpac LLC

Frequently Asked Questions

What is the projected growth rate of the Cut and Stack Label Market?

The Cut and Stack Label Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.5% between 2025 and 2033, driven by increasing demand for packaged goods and advancements in labeling technology.

Which factors are primarily driving the Cut and Stack Label Market?

Key drivers include the expanding packaged food and beverage industry, the demand for cost-effective and high-quality labels, and advancements in printing technologies that enhance efficiency and aesthetic appeal.

How is sustainability impacting the Cut and Stack Label Market?

Sustainability is a major trend, driving demand for recyclable, compostable, and renewable label materials. Manufacturers are innovating to meet stricter environmental regulations and consumer preferences for eco-friendly packaging solutions.

What role does AI play in the Cut and Stack Label industry?

AI is improving operational efficiency through automated quality control, predictive maintenance, and optimized production scheduling. It also assists in design generation and enhances overall supply chain visibility, leading to cost savings and improved product quality.

Which regions offer the most significant growth opportunities for Cut and Stack Labels?

Asia Pacific is expected to be a key growth region due to rapid economic development, urbanization, and rising disposable incomes, leading to increased consumption of packaged goods and demand for labeling solutions.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted