Copper Anode Market

Copper Anode Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705119 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

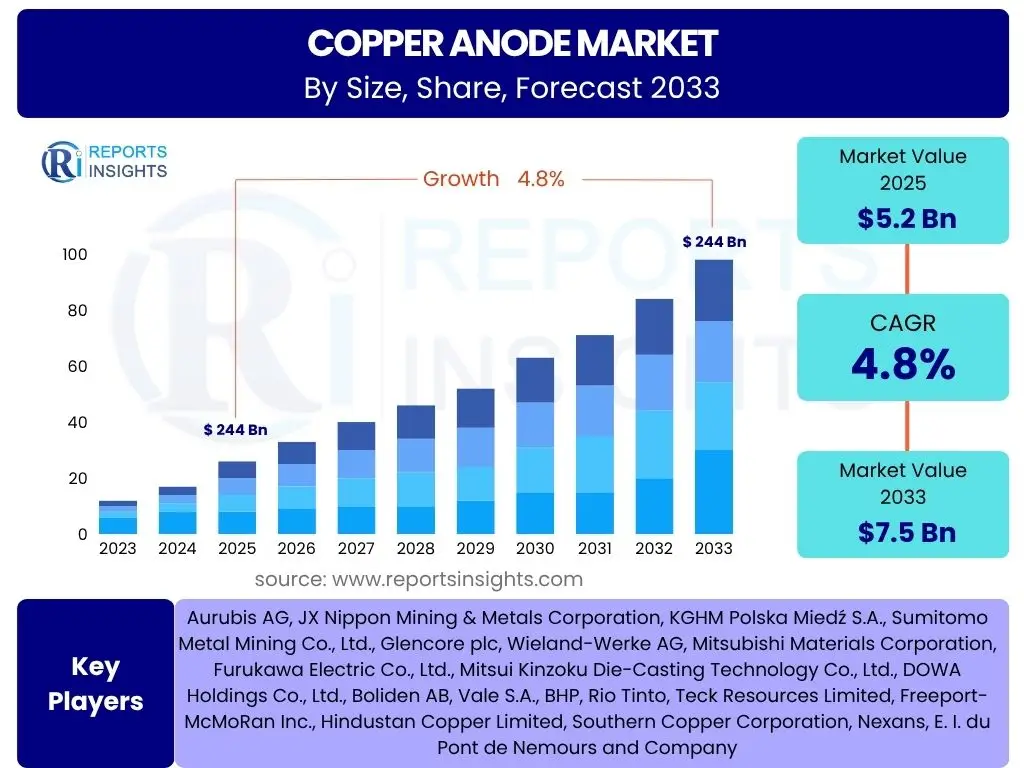

Copper Anode Market Size

According to Reports Insights Consulting Pvt Ltd, The Copper Anode Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.8% between 2025 and 2033. The market is estimated at USD 5.2 billion in 2025 and is projected to reach USD 7.5 billion by the end of the forecast period in 2033. This growth is underpinned by escalating demand across various industrial applications, including electronics, automotive, and general manufacturing, where copper anodes are essential for electroplating, electrowinning, and electroforming processes. The increasing global focus on electric vehicles (EVs) and renewable energy infrastructure further contributes to the robust demand for copper, thereby driving the anode market.

Key Copper Anode Market Trends & Insights

User queries regarding the Copper Anode market frequently focus on the evolving technological landscape, the influence of sustainability initiatives, and the impact of global economic shifts. Stakeholders are keen to understand how advancements in manufacturing processes, such as additive manufacturing, are shaping the demand for specific anode types. There is also significant interest in the role of recycled copper in anode production and the implications of stricter environmental regulations on sourcing and processing practices. Furthermore, regional market dynamics, particularly in rapidly industrializing economies, are a common area of inquiry, reflecting the market's sensitivity to macroeconomic factors and industrial expansion.

Another prevalent theme in user questions revolves around the integration of advanced materials and surface treatment technologies that enhance anode performance and lifespan. Manufacturers are constantly seeking methods to improve current efficiency, reduce impurity levels, and optimize deposition rates in electroplating operations. The increasing complexity of electronic components and the need for high-precision finishes drive innovation in anode purity and composition. Additionally, the shift towards digitalization and automation in industrial processes is influencing how copper anodes are manufactured, quality-controlled, and utilized, prompting questions about the future of traditional production methods versus automated, data-driven approaches.

- Growing demand from electric vehicle (EV) battery manufacturing and charging infrastructure.

- Increasing adoption of advanced electroplating techniques for high-performance electronics.

- Rising emphasis on sustainable sourcing and recycling of copper materials for anode production.

- Technological advancements in anode purity and composition to meet stringent industry standards.

- Expansion of renewable energy projects driving demand for copper in grid infrastructure.

AI Impact Analysis on Copper Anode

Common user questions regarding AI's impact on the Copper Anode sector primarily revolve around efficiency gains, predictive capabilities, and the potential for process optimization. Users frequently ask how Artificial intelligence (AI) can enhance the manufacturing of copper anodes, particularly concerning quality control, impurity detection, and energy consumption. There is considerable interest in AI's role in predictive maintenance for electroplating and electrowinning cells, aiming to minimize downtime and improve operational continuity. Furthermore, inquiries often touch upon AI's application in supply chain management, enabling better forecasting of raw material prices and demand fluctuations, thus optimizing inventory and procurement strategies for anode producers.

Another key area of user inquiry pertains to the integration of AI in research and development for new anode materials and compositions. Stakeholders are curious about AI's capacity to simulate material behaviors, predict performance under various conditions, and accelerate the discovery of novel alloys or surface treatments that could enhance anode efficiency and durability. Concerns are also raised regarding the initial investment costs associated with AI implementation, the need for specialized data analytics expertise, and the potential for job displacement due to increased automation. However, the overarching expectation is that AI will drive significant improvements in consistency, cost-efficiency, and innovation across the copper anode value chain.

- AI-driven optimization of manufacturing processes for improved anode purity and consistency.

- Predictive maintenance analytics for electroplating and electrowinning equipment reducing downtime.

- Enhanced supply chain management through AI-powered demand forecasting and raw material price prediction.

- Accelerated R&D for novel copper anode compositions and performance enhancements.

- Automated quality inspection systems for detecting defects and ensuring product integrity.

Key Takeaways Copper Anode Market Size & Forecast

User inquiries about key takeaways from the Copper Anode market size and forecast frequently highlight the primary drivers of growth, such as the burgeoning electronics and automotive industries, particularly the electric vehicle segment. There is a keen interest in understanding the long-term sustainability of demand given global economic volatility and geopolitical factors. Users often seek confirmation on the most impactful regional markets and the specific application areas that are projected to experience the most significant expansion, providing insights for strategic investment and market entry decisions. The persistent demand for high-purity copper anodes in advanced technological applications remains a central point of interest.

Another critical takeaway that users consistently seek relates to the interplay between raw material availability, pricing stability, and the overall market forecast. The copper market's inherent volatility poses challenges for anode manufacturers, leading to questions about hedging strategies and the development of more resilient supply chains. The market's future trajectory is also heavily influenced by technological shifts, such as advancements in battery technology and the push towards miniaturization in electronics, which necessitate high-quality and reliable copper anodes. Understanding these interconnected factors is crucial for stakeholders to accurately gauge market potential and mitigate risks over the forecast period.

- Robust growth driven by electronics, automotive (especially EV), and renewable energy sectors.

- Asia Pacific to remain the dominant market due to extensive industrial bases and manufacturing hubs.

- Technological advancements in anode purity and composition are critical for meeting evolving industry demands.

- Sustainability initiatives, including recycling, are increasingly influencing production methods and supply chains.

- Market resilience linked to global economic stability and continued industrialization efforts.

Copper Anode Market Drivers Analysis

The Copper Anode market is experiencing significant growth propelled by several key drivers. The burgeoning electronics industry, characterized by the miniaturization of components and the increasing demand for high-performance devices, necessitates precise electroplating processes that rely heavily on high-purity copper anodes. This includes everything from printed circuit boards to semiconductor manufacturing. Additionally, the automotive sector's rapid transition towards electric vehicles (EVs) and hybrid electric vehicles (HEVs) is a major catalyst, as copper anodes are integral to battery manufacturing, charging infrastructure, and various electronic systems within modern vehicles. This sustained demand from critical end-use industries forms the bedrock of market expansion.

Furthermore, the global push towards renewable energy solutions, particularly solar and wind power, contributes substantially to the demand for copper anodes. Copper is a vital material in the construction of energy grids, transformers, and cabling systems required for renewable energy integration. The expansion of urban infrastructure and continued industrialization in developing economies also fuels the market, as general manufacturing, construction, and plumbing applications consistently require copper and related products. These broad industrial applications, coupled with technological advancements demanding higher purity and performance, underscore the robust growth trajectory of the copper anode market.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Electric Vehicle (EV) Production | +1.5% | North America, Europe, Asia Pacific (China, Japan) | Short to Mid-Term (2025-2030) |

| Expansion of Electronics & Semiconductor Industry | +1.2% | Asia Pacific (South Korea, Taiwan, China), North America | Mid to Long-Term (2027-2033) |

| Increasing Demand for Renewable Energy Infrastructure | +0.8% | Europe, North America, Asia Pacific (India, China) | Mid to Long-Term (2028-2033) |

| Infrastructure Development & Urbanization | +0.7% | Asia Pacific (China, India), Latin America, MEA | Mid to Long-Term (2027-2033) |

| Technological Advancements in Electroplating | +0.6% | Global, particularly developed economies | Short to Mid-Term (2025-2030) |

Copper Anode Market Restraints Analysis

Despite the positive growth trajectory, the Copper Anode market faces several significant restraints. One primary challenge is the volatility of copper prices in the global commodity markets. Fluctuations in raw material costs directly impact the production expenses of copper anodes, making it difficult for manufacturers to maintain stable pricing and profit margins. This unpredictability can deter investment and create uncertainty across the value chain. Geopolitical instabilities and trade tensions further exacerbate this issue by disrupting supply chains and imposing tariffs, which can increase the cost of imported raw copper or finished anodes, thereby constraining market expansion.

Another notable restraint is the high energy consumption associated with the production of copper anodes, particularly in the electrowinning and refining processes. Rising energy costs, coupled with increasing environmental regulations aimed at reducing carbon footprints, place significant pressure on manufacturers to adopt more energy-efficient and sustainable production methods. The capital expenditure required for upgrading existing facilities or building new, greener plants can be substantial, limiting the growth potential for smaller players. Additionally, the availability of substitutes for certain copper applications or the development of alternative plating technologies, though currently limited, poses a potential long-term restraint if technological breakthroughs reduce reliance on traditional copper anodes.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility of Copper Raw Material Prices | -1.0% | Global | Short to Mid-Term (2025-2030) |

| Stringent Environmental Regulations | -0.7% | Europe, North America, Asia Pacific (China) | Mid to Long-Term (2027-2033) |

| High Energy Consumption in Production | -0.5% | Global | Mid-Term (2026-2031) |

| Trade Barriers & Geopolitical Tensions | -0.4% | Global, particularly US-China, EU-Asia | Short-Term (2025-2027) |

| Scarcity of High-Purity Copper Ore | -0.3% | Global, affects specific mining regions | Long-Term (2030-2033) |

Copper Anode Market Opportunities Analysis

The Copper Anode market is poised for significant opportunities driven by emerging technological shifts and increasing global sustainability initiatives. One major opportunity lies in the growing adoption of electric vehicles (EVs) and the associated expansion of charging infrastructure. As EV production scales up globally, the demand for copper in batteries, motors, and charging stations will surge, creating a direct need for high-quality copper anodes for electrodeposition and related manufacturing processes. This presents a sustained growth avenue, particularly for manufacturers capable of producing anodes with precise specifications for advanced battery technologies.

Furthermore, the increasing focus on the circular economy and sustainable manufacturing practices offers substantial opportunities for market participants. The development of advanced recycling technologies for copper waste and end-of-life products can provide a more stable and environmentally friendly source of raw material for anode production, reducing reliance on virgin copper mining. This trend aligns with corporate sustainability goals and government regulations, potentially leading to preferential market positioning for companies investing in circular supply chains. Additionally, the exploration of novel applications in niche markets, such as additive manufacturing (3D printing) of copper components, and the continuous innovation in surface finishing technologies, open new avenues for specialized copper anode products and services, fostering long-term market expansion.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Investment in Copper Recycling & Circular Economy | +1.3% | Europe, North America, Asia Pacific | Mid to Long-Term (2027-2033) |

| Emergence of Niche Applications (e.g., Additive Manufacturing) | +0.9% | Global, R&D focused regions | Long-Term (2029-2033) |

| Expansion in Data Center & 5G Infrastructure | +0.8% | North America, Asia Pacific, Europe | Mid-Term (2026-2031) |

| Government Initiatives for Green Energy & Infrastructure | +0.7% | Global, particularly developing economies | Mid to Long-Term (2027-2033) |

| Technological Collaboration & Partnerships | +0.6% | Global | Short to Mid-Term (2025-2030) |

Copper Anode Market Challenges Impact Analysis

The Copper Anode market faces several critical challenges that could impede its growth trajectory. One significant hurdle is the increasing scarcity and declining quality of high-grade copper ore. As easily accessible deposits are depleted, mining operations must delve deeper or process lower-grade ores, leading to higher extraction costs and greater environmental impact. This affects the overall supply and cost structure for raw copper, directly influencing the pricing and availability of copper anodes. Furthermore, the complexities of international trade and geopolitical tensions, such as sanctions or trade disputes, can disrupt the global supply chain, causing delays and increasing logistical costs for manufacturers reliant on cross-border material flows.

Another substantial challenge is the intense competition within the market, which often leads to price wars and compressed profit margins for manufacturers. This competitive pressure necessitates continuous investment in R&D to improve anode performance, reduce production costs, and differentiate products, which can be a heavy burden, especially for smaller market players. Additionally, the labor-intensive nature of some copper anode manufacturing processes, coupled with a potential shortage of skilled labor specializing in metallurgy and electrochemistry, poses operational challenges. Ensuring consistent quality and purity, especially for demanding applications like semiconductors, remains a persistent challenge that requires meticulous process control and advanced analytical capabilities.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rising Production Costs due to Energy & Labor | -0.9% | Global | Short to Mid-Term (2025-2030) |

| Intense Market Competition & Price Pressure | -0.8% | Global | Short to Mid-Term (2025-2030) |

| Supply Chain Disruptions & Logistical Issues | -0.6% | Global | Short-Term (2025-2027) |

| Need for High Capital Investment in Technology Upgrades | -0.5% | Global | Mid to Long-Term (2027-2033) |

| Management of Hazardous Waste from Processes | -0.4% | Global, particularly developed regions | Mid-Term (2026-2031) |

Copper Anode Market - Updated Report Scope

This report provides an in-depth analysis of the global Copper Anode market, encompassing historical data from 2019 to 2023, current market estimates for 2025, and projections through to 2033. The study delves into market sizing, growth rates, key trends, and the impact of various drivers, restraints, opportunities, and challenges affecting the industry. It offers a comprehensive segmentation analysis by type, application, and end-use industry, alongside a detailed regional outlook covering major geographies. The report also profiles leading market players, offering strategic insights into the competitive landscape, aiming to equip stakeholders with actionable intelligence for informed decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 5.2 Billion |

| Market Forecast in 2033 | USD 7.5 Billion |

| Growth Rate | 4.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Aurubis AG, JX Nippon Mining & Metals Corporation, KGHM Polska Miedź S.A., Sumitomo Metal Mining Co., Ltd., Glencore plc, Wieland-Werke AG, Mitsubishi Materials Corporation, Furukawa Electric Co., Ltd., Mitsui Kinzoku Die-Casting Technology Co., Ltd., DOWA Holdings Co., Ltd., Boliden AB, Vale S.A., BHP, Rio Tinto, Teck Resources Limited, Freeport-McMoRan Inc., Hindustan Copper Limited, Southern Copper Corporation, Nexans, E. I. du Pont de Nemours and Company |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Copper Anode market is broadly segmented by type, application, and end-use industry, reflecting the diverse requirements and uses of copper anodes across various sectors. The segmentation by type primarily distinguishes between Phosphorized Copper Anodes and Non-Phosphorized Copper Anodes, with phosphorized anodes being widely preferred in many electroplating applications due to their ability to dissolve uniformly and minimize sludge formation. Understanding these distinctions is crucial for manufacturers to tailor their production and for end-users to select the most appropriate anode for their specific operational needs, influencing performance and cost efficiency.

Further granularity is achieved through segmentation by application, which includes key areas such as electroplating, electrowinning, printed circuit boards (PCBs), and electroforming, among others. Each application demands specific characteristics from the copper anodes, driving product innovation and specialization. For instance, the electronics industry requires exceptionally high-purity anodes for precise PCB manufacturing, while electrowinning operations may prioritize anodes optimized for large-scale copper extraction. Finally, the end-use industry segmentation provides insight into the primary sectors driving demand, including Electronics & Electrical, Automotive, Building & Construction, and General Manufacturing, highlighting the market's reliance on industrial growth and technological advancement in these sectors.

- By Type:

- Phosphorized Copper Anodes

- Non-Phosphorized Copper Anodes

- Other Copper Anodes

- By Application:

- Electroplating

- Electrowinning

- Printed Circuit Boards (PCBs)

- Electroforming

- Cathode Ray Tubes (CRTs)

- Decorative Coatings

- Others

- By End-Use Industry:

- Electronics & Electrical

- Automotive

- Building & Construction

- General Manufacturing

- Aerospace & Defense

- Jewelry

- Others

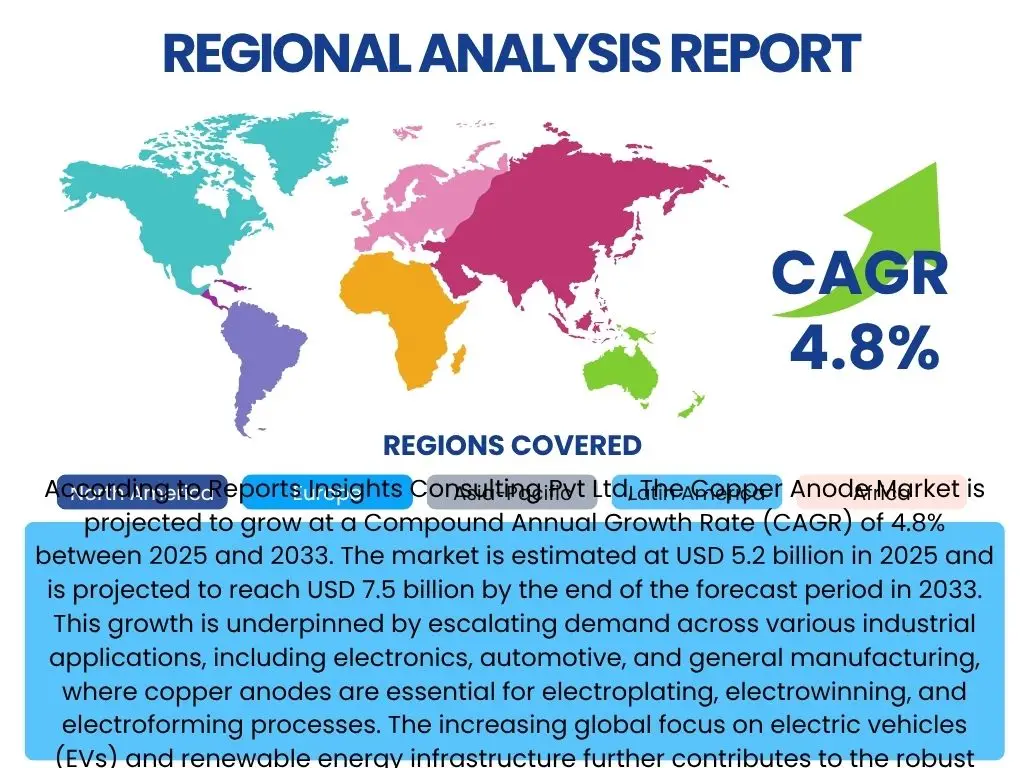

Regional Highlights

Asia Pacific (APAC) stands as the dominant region in the Copper Anode market, primarily driven by the presence of major manufacturing hubs in countries like China, Japan, South Korea, and Taiwan. These nations are global leaders in electronics, automotive, and general manufacturing, creating robust demand for copper anodes for various applications, including printed circuit boards, automotive components, and consumer electronics. Rapid industrialization, increasing disposable incomes, and substantial government investments in infrastructure and technological development further bolster the market growth in this region. The sheer scale of industrial output and ongoing expansion of manufacturing capacities across diverse sectors solidify APAC's leading position, with countries like India also emerging as significant contributors to regional demand.

North America and Europe represent mature but steadily growing markets for Copper Anodes. In North America, demand is fueled by the robust automotive sector, particularly the surge in electric vehicle production, coupled with the thriving aerospace and defense industries which require high-precision electroplating. Innovation in semiconductor manufacturing and advanced electronics also contributes significantly to market expansion. Europe's market is characterized by stringent environmental regulations driving demand for more efficient and sustainable production processes. The region's strong automotive industry, coupled with investments in renewable energy infrastructure and advanced manufacturing technologies, ensures consistent demand for high-quality copper anodes. Both regions are also at the forefront of adopting advanced manufacturing techniques and sustainable practices, which influences the types of anodes and processes preferred.

Latin America, the Middle East, and Africa (MEA) are emerging markets for Copper Anodes, showing promising growth potential. Latin America, particularly countries like Chile and Peru, are major copper producers, which provides a natural advantage in raw material sourcing for anode production. Increased industrialization, infrastructure development, and growing automotive and electronics sectors in countries such as Brazil and Mexico are driving demand. The Middle East and Africa regions are witnessing significant investments in infrastructure, industrial diversification, and renewable energy projects. While currently smaller in market share compared to APAC, North America, and Europe, these regions are projected to experience accelerated growth rates due to their ongoing economic development and increasing adoption of industrial processes that require copper anodes.

- Asia Pacific: Dominant market share due to extensive electronics, automotive, and general manufacturing industries in China, Japan, South Korea, and Taiwan. Strong demand driven by industrialization and infrastructure development.

- North America: Significant growth propelled by the electric vehicle boom, robust aerospace and defense sectors, and continuous advancements in semiconductor technology. Emphasis on high-purity and performance anodes.

- Europe: Mature market with steady growth, supported by a strong automotive industry, increasing renewable energy projects, and a focus on sustainable manufacturing processes. Strict environmental regulations influence product development.

- Latin America: Emerging market with potential due to rich copper resources and growing industrial activities, particularly in Brazil and Mexico. Infrastructure development projects are driving demand.

- Middle East & Africa: Developing market with increasing industrialization, diversification efforts in non-oil sectors, and investment in infrastructure and renewable energy, leading to rising demand for copper anodes.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Copper Anode Market.- Aurubis AG

- JX Nippon Mining & Metals Corporation

- KGHM Polska Miedź S.A.

- Sumitomo Metal Mining Co., Ltd.

- Glencore plc

- Wieland-Werke AG

- Mitsubishi Materials Corporation

- Furukawa Electric Co., Ltd.

- Mitsui Kinzoku Die-Casting Technology Co., Ltd.

- DOWA Holdings Co., Ltd.

- Boliden AB

- Vale S.A.

- BHP

- Rio Tinto

- Teck Resources Limited

- Freeport-McMoRan Inc.

- Hindustan Copper Limited

- Southern Copper Corporation

- Nexans

- E. I. du Pont de Nemours and Company

Frequently Asked Questions

What are the primary applications of copper anodes?

Copper anodes are primarily used in electroplating for surface finishing, electrowinning for copper extraction, and in the manufacturing of printed circuit boards (PCBs) and other electronic components. They are essential for depositing uniform and high-quality copper layers onto various substrates.

How do phosphorized copper anodes differ from non-phosphorized anodes?

Phosphorized copper anodes contain a small percentage of phosphorus, typically 0.03% to 0.06%, which promotes uniform dissolution, reduces the formation of sludge, and improves the efficiency of acid copper plating baths. Non-phosphorized anodes, while also used, tend to dissolve less uniformly and may produce more sludge.

Which region holds the largest market share for copper anodes?

The Asia Pacific region currently holds the largest market share for copper anodes, driven by its extensive manufacturing capabilities in electronics, automotive, and general industrial sectors, particularly in countries like China, Japan, and South Korea.

What key factors are driving the growth of the copper anode market?

Key growth drivers include the booming electric vehicle (EV) industry, increasing demand from the electronics and semiconductor sectors, expanding renewable energy infrastructure, and ongoing global urbanization and industrial development.

What challenges does the copper anode market face?

The market faces challenges such as volatility in raw copper prices, stringent environmental regulations increasing production costs, intense market competition leading to price pressures, and potential supply chain disruptions due to geopolitical factors.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted