Copper Alloy Market

Copper Alloy Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700345 | Last Updated : July 24, 2025 |

Format : ![]()

![]()

![]()

![]()

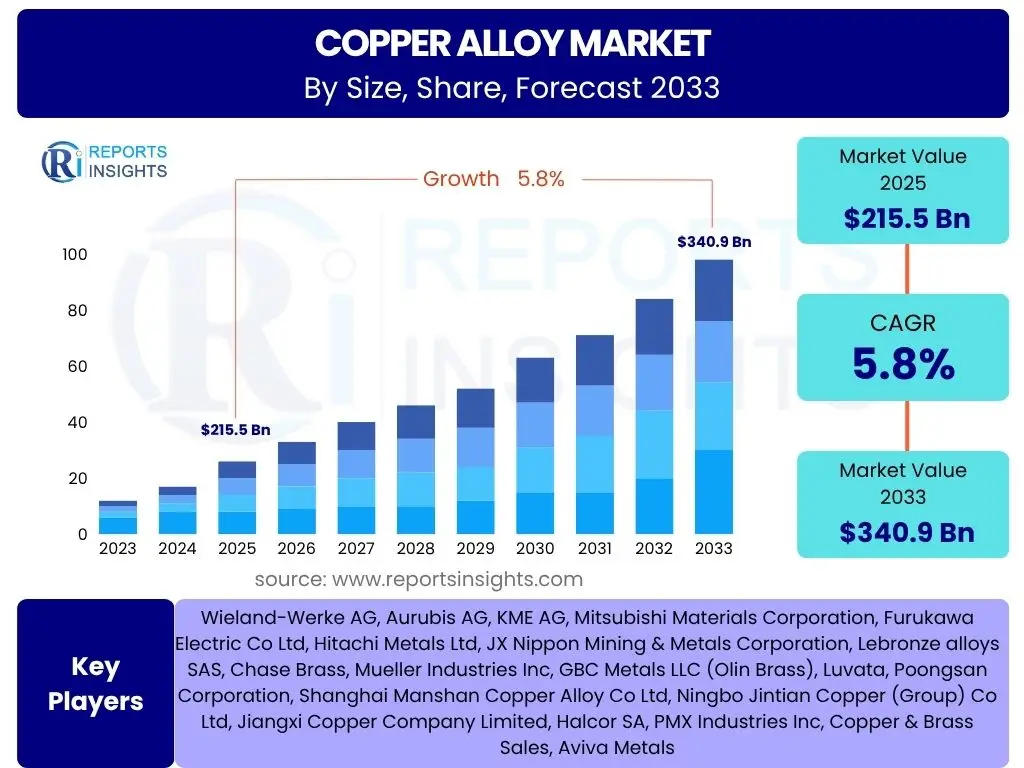

Copper Alloy Market Size

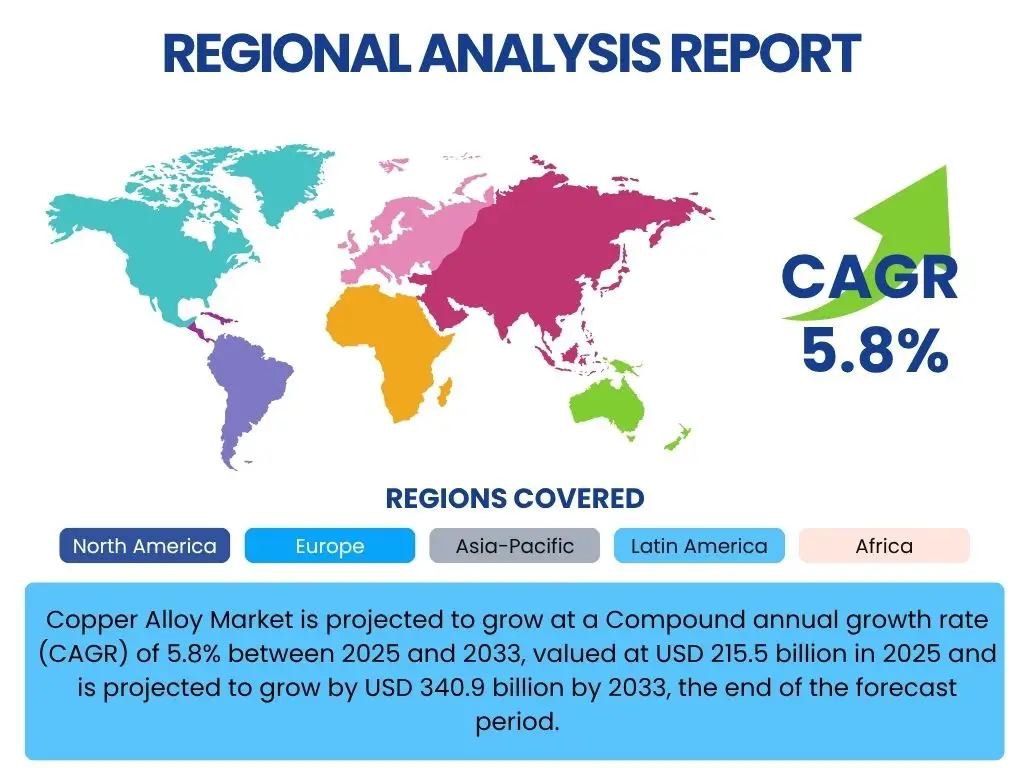

Copper Alloy Market is projected to grow at a Compound annual growth rate (CAGR) of 5.8% between 2025 and 2033, valued at USD 215.5 billion in 2025 and is projected to grow by USD 340.9 billion by 2033, the end of the forecast period.

Key Copper Alloy Market Trends & Insights

The copper alloy market is currently experiencing dynamic shifts driven by several pivotal trends, including the accelerating global transition towards electric vehicles and renewable energy infrastructure, which inherently boosts demand for highly conductive and durable materials. Concurrently, there is a significant emphasis on developing advanced copper alloys with enhanced properties such as superior strength, corrosion resistance, and thermal conductivity, catering to high-performance applications across various industries. Furthermore, the growing adoption of smart manufacturing processes, including automation and additive manufacturing techniques, is transforming production efficiencies and enabling the creation of intricate copper alloy components. Sustainability initiatives, including stringent regulations on material sourcing and increased focus on recycling and circular economy principles, are also profoundly influencing market practices and product development. Additionally, the expansion of smart cities and digital infrastructure projects globally is fueling the need for reliable electrical and communication components made from copper alloys, supporting the broader digital transformation.

AI Impact Analysis on Copper Alloy

Artificial Intelligence (AI) is set to significantly revolutionize the copper alloy industry by optimizing various stages of the value chain. AI-driven predictive analytics can enhance demand forecasting, leading to more efficient production planning and inventory management, thereby reducing waste and operational costs. In material science, AI algorithms are accelerating the discovery and development of novel copper alloys with tailored properties, predicting material performance, and optimizing compositional variations for specific applications, significantly cutting down research and development timelines. Furthermore, AI-powered quality control systems, utilizing computer vision and machine learning, can detect defects with unparalleled precision during manufacturing, ensuring higher product quality and reducing scrap rates. The integration of AI into supply chain logistics will enable real-time tracking, optimize transportation routes, and predict potential disruptions, enhancing overall supply chain resilience and efficiency for copper alloy raw materials and finished products. AI is also poised to play a crucial role in optimizing energy consumption in smelting and refining processes, contributing to more sustainable and cost-effective production methods within the copper alloy manufacturing landscape.

Key Takeaways Copper Alloy Market Size & Forecast

- The global copper alloy market is poised for robust expansion, driven by increasing industrialization and urbanization across emerging economies.

- Significant growth is anticipated from the electrical and electronics sector, fueled by advancements in connectivity and smart device proliferation.

- The automotive industry, particularly the electric vehicle segment, will be a major catalyst for demand dueating to copper alloys' thermal and electrical conductivity.

- Sustainable practices and recycling initiatives are gaining traction, influencing raw material sourcing and manufacturing processes in the industry.

- Technological advancements in alloy composition and manufacturing techniques are leading to high-performance materials for specialized applications.

- Asia Pacific is expected to maintain its dominance in market share, owing to robust manufacturing bases and infrastructural development.

- Volatility in raw material prices and environmental regulations pose persistent challenges to market stability and growth.

- Opportunities lie in the development of lightweight and high-strength alloys for aerospace and defense applications.

- The market will likely witness increased mergers, acquisitions, and strategic collaborations to consolidate market position and expand product portfolios.

- Innovations in additive manufacturing are opening new avenues for complex copper alloy component fabrication.

Copper Alloy Market Drivers Analysis

The copper alloy market's expansion is fundamentally propelled by a confluence of macroeconomic trends and industry-specific demands that underscore the material's indispensable qualities. Copper alloys, renowned for their excellent electrical and thermal conductivity, corrosion resistance, and malleability, are critical components across diverse sectors. The global push for sustainable energy solutions and the rapid evolution of electric vehicles are generating unprecedented demand, as these applications heavily rely on efficient power transmission and thermal management. Simultaneously, the continuous growth in telecommunications infrastructure, including 5G deployment and data centers, necessitates high-performance conductive materials. Urbanization and industrial development in emerging economies further amplify demand for copper alloys in construction, plumbing, and various industrial machinery. These drivers collectively paint a picture of sustained growth, with each factor contributing significantly to the market's positive trajectory over the forecast period by creating new avenues for application and increasing consumption in established sectors.| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rising Demand from Electrical & Electronics Industry: The pervasive integration of electronics into daily life, coupled with the rapid expansion of communication networks (e.g., 5G infrastructure), data centers, and consumer electronics, significantly drives the demand for copper alloys. Their superior electrical conductivity and heat dissipation properties make them indispensable for wires, cables, connectors, and circuit components, ensuring efficient power transmission and signal integrity. | +1.5% | Asia Pacific (China, South Korea, Japan), North America, Europe | Long-term (2025-2033) |

| Growth in Automotive Sector, especially Electric Vehicles (EVs): The global shift towards electric and hybrid vehicles is a major growth impetus. Copper alloys are critical for EV components such as battery packs, charging infrastructure, electric motors, and power electronics, owing to their high electrical conductivity, thermal management capabilities, and corrosion resistance. The increasing production targets for EVs worldwide directly translate to higher copper alloy consumption. | +1.2% | Asia Pacific (China), Europe (Germany), North America (USA) | Medium to Long-term (2025-2033) |

| Expanding Construction and Infrastructure Development: Massive infrastructure projects globally, including smart cities, commercial buildings, residential complexes, and transportation networks, require vast quantities of copper alloys for plumbing, roofing, wiring, and architectural elements. The durability, aesthetic appeal, and corrosion resistance of copper alloys make them preferred materials in modern construction. | +0.9% | Asia Pacific (India, China), Middle East & Africa, Latin America | Long-term (2025-2033) |

| Increasing Adoption in Renewable Energy Systems: The global energy transition towards renewable sources such as solar, wind, and geothermal power generation relies heavily on copper alloys. They are essential in solar panels (wiring, inverters), wind turbines (generators, cabling), and power transmission lines due to their efficiency in conducting electricity and resilience in varied environmental conditions, supporting the sustainability agenda. | +0.8% | Europe, North America, Asia Pacific (China, India) | Medium to Long-term (2025-2033) |

| Technological Advancements and Material Innovation: Continuous research and development in metallurgy are leading to the creation of new copper alloys with enhanced properties, such as improved strength-to-weight ratio, higher corrosion resistance, and better thermal conductivity. These innovations open up new application areas in aerospace, defense, and specialized industrial machinery, further stimulating market demand. | +0.5% | North America, Europe, Japan | Long-term (2025-2033) |

Copper Alloy Market Restraints Analysis

Despite the robust growth drivers, the copper alloy market faces significant restraints that could impede its overall expansion. The primary challenge remains the inherent volatility in raw material prices, particularly copper, which directly impacts production costs and pricing strategies for manufacturers. This fluctuation makes long-term planning and stable profit margins difficult. Furthermore, the increasing availability and adoption of substitute materials, such as aluminum and various plastics, especially in applications where weight reduction or cost efficiency is prioritized over copper's specific properties, pose a competitive threat. Environmental regulations pertaining to mining, processing, and waste disposal of copper alloys are becoming increasingly stringent, leading to higher operational costs for compliance and potentially limiting production capacity. Additionally, the capital-intensive nature of copper alloy manufacturing, requiring substantial investment in infrastructure and technology, can be a barrier to entry for new players and limit expansion for existing ones. Addressing these restraints will be crucial for sustained growth in the copper alloy market.| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in Raw Material Prices: The price of copper, the primary raw material, is highly susceptible to global economic conditions, geopolitical events, and supply-demand imbalances. Significant fluctuations in copper prices directly impact the production costs of copper alloys, leading to unpredictable profit margins for manufacturers and potentially higher prices for end-users, which can curb demand. | -0.8% | Global, particularly major consuming regions (Asia Pacific, Europe) | Short to Medium-term (Ongoing) |

| Availability and Competition from Substitute Materials: In various applications, especially where weight reduction or lower cost is a priority, alternative materials such as aluminum, stainless steel, and certain plastics are increasingly being adopted. For instance, aluminum is a cheaper and lighter alternative in automotive wiring and heat sinks, directly competing with copper alloys in specific segments. | -0.6% | Global, especially automotive and construction sectors | Medium to Long-term (Evolving) |

| Stringent Environmental Regulations and Sustainability Concerns: The copper mining and processing industries face increasing scrutiny and stringent regulations regarding environmental impact, energy consumption, and waste management. Compliance with these regulations often leads to higher operational costs, limits production expansions, and necessitates significant investments in cleaner technologies, affecting overall market growth. | -0.5% | Europe, North America, parts of Asia Pacific (China) | Long-term (Continuous) |

| High Capital Investment and Production Costs: Setting up and operating copper alloy manufacturing facilities requires substantial capital investment for machinery, technology, and adherence to quality standards. The energy-intensive nature of smelting and refining processes further adds to the overall production costs, making it challenging for new entrants and potentially limiting scaling capabilities for smaller players. | -0.3% | Global, especially emerging economies needing infrastructure | Long-term (Structural) |

Copper Alloy Market Opportunities Analysis

The copper alloy market is presented with several promising opportunities that can significantly contribute to its long-term growth and expansion. The burgeoning electric vehicle (EV) market, alongside the global push for renewable energy infrastructure, creates a substantial and sustained demand for high-performance copper alloys essential for efficient energy transmission and storage. Furthermore, continuous advancements in material science and manufacturing technologies, such as additive manufacturing and smart factory concepts, are enabling the development of novel alloys with superior properties and more complex geometries, opening doors to new high-value applications. The increasing focus on circular economy principles and efficient recycling of copper alloys not only addresses sustainability concerns but also provides a cost-effective and environmentally friendly source of raw materials, reducing reliance on virgin mining. Moreover, the expanding urbanization and industrialization in developing economies, particularly in Asia Pacific, offer vast untapped potential for market penetration in construction, infrastructure, and consumer goods sectors. These opportunities highlight strategic areas for innovation, investment, and market expansion.| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand for Electric Vehicles and Charging Infrastructure: The rapid global adoption of EVs presents a significant opportunity. Copper alloys are vital for battery components, electric motors, power electronics, and high-speed charging stations due to their unmatched electrical and thermal conductivity. As EV production scales, so too will the demand for specialized copper alloys. | +1.3% | Global, particularly China, Europe, North America | Long-term (2025-2033) |

| Expansion of Renewable Energy and Energy Storage Systems: Investment in solar, wind, and geothermal energy, along with grid modernization and large-scale energy storage solutions, offers immense growth potential. Copper alloys are crucial for efficient power generation, transmission, and storage, making them indispensable in the green energy transition. | +1.0% | Europe, North America, Asia Pacific (China, India) | Long-term (2025-2033) |

| Advancements in Additive Manufacturing (3D Printing): The emergence of additive manufacturing for metals allows for the creation of complex, high-performance copper alloy components with reduced waste and faster prototyping. This technology opens up new avenues for customized parts in aerospace, medical, and specialized industrial applications, driving demand for specific alloy powders. | +0.7% | North America, Europe, Japan | Medium to Long-term (Emerging) |

| Increasing Focus on Recycling and Circular Economy: The growing emphasis on sustainability drives the market for recycled copper alloys. This not only reduces reliance on virgin copper mining but also offers a more environmentally friendly and often cost-effective source of material. Investment in advanced recycling technologies creates significant business opportunities. | +0.6% | Global, especially Europe and North America with strong recycling infrastructure | Long-term (Continuous) |

Copper Alloy Market Challenges Impact Analysis

The copper alloy market, despite its promising outlook, is not without its share of formidable challenges that could constrain its growth trajectory. Beyond the previously discussed price volatility and material substitution, issues related to supply chain disruptions, particularly in raw material sourcing and logistics, pose significant hurdles. Geopolitical tensions, trade disputes, and unforeseen global events can quickly impact the availability and cost of primary copper and alloy components. Furthermore, the industry faces the challenge of continually meeting increasingly stringent performance requirements for specialized applications, demanding significant investment in research and development and advanced manufacturing capabilities. Managing the energy-intensive nature of copper alloy production while adhering to evolving environmental standards also presents a substantial operational and financial burden. Lastly, the skilled labor shortage in metallurgy and advanced manufacturing fields could hinder production capacity and innovation. Successfully navigating these challenges will be crucial for the market's sustained growth and competitiveness.| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Supply Chain Disruptions and Geopolitical Instability: The global copper alloy supply chain is vulnerable to disruptions arising from geopolitical conflicts, trade policies, natural disasters, and pandemics. These events can restrict the supply of raw materials, increase transportation costs, and delay product delivery, causing production bottlenecks and impacting market stability. | -0.7% | Global, especially regions reliant on imports/exports | Short to Medium-term (Unpredictable) |

| High Energy Consumption and Carbon Footprint: The production of copper alloys, particularly smelting and refining, is highly energy-intensive and contributes significantly to carbon emissions. Increasing pressure for decarbonization and higher energy costs necessitate substantial investments in energy-efficient technologies and renewable energy sources, adding to operational expenses. | -0.4% | Global, particularly in regions with strict emission targets (Europe, North America) | Long-term (Continuous pressure) |

| Technological Obsolescence and Need for Continuous R&D: The rapid pace of technological change in end-use industries (e.g., electronics, automotive) constantly demands higher performance, lighter weight, and more specialized copper alloys. Manufacturers must continuously invest in R&D to innovate and develop new alloys and manufacturing processes, or risk market irrelevance, requiring significant capital. | -0.3% | Global, especially technologically advanced economies | Long-term (Continuous) |

| Skilled Labor Shortage and Workforce Development: The copper alloy industry, particularly in manufacturing and metallurgy, requires specialized skills. A growing shortage of skilled engineers, metallurgists, and technicians can hamper production efficiency, delay technological adoption, and increase labor costs, posing a long-term challenge to the industry's growth capacity. | -0.2% | North America, Europe, Japan | Long-term (Structural) |

Copper Alloy Market - Updated Report Scope

This updated market research report provides a comprehensive analysis of the global copper alloy market, offering detailed insights into its size, growth trajectory, key trends, and future projections. The scope encompasses a thorough examination of market drivers, restraints, opportunities, and challenges influencing the industry, along with a granular segmentation analysis across various product types, forms, end-use industries, and geographical regions. The report is designed to equip stakeholders with actionable intelligence for strategic decision-making, covering historical performance and future forecasts with a focus on market dynamics from 2025 to 2033, and an in-depth profiling of leading market participants.| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 215.5 billion |

| Market Forecast in 2033 | USD 340.9 billion |

| Growth Rate | 5.8% CAGR from 2025 to 2033 |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Wieland-Werke AG, Aurubis AG, KME AG, Mitsubishi Materials Corporation, Furukawa Electric Co Ltd, Hitachi Metals Ltd, JX Nippon Mining & Metals Corporation, Lebronze alloys SAS, Chase Brass, Mueller Industries Inc, GBC Metals LLC (Olin Brass), Luvata, Poongsan Corporation, Shanghai Manshan Copper Alloy Co Ltd, Ningbo Jintian Copper (Group) Co Ltd, Jiangxi Copper Company Limited, Halcor SA, PMX Industries Inc, Copper & Brass Sales, Aviva Metals |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The copper alloy market is meticulously analyzed across several key segments to provide a granular understanding of its composition and growth dynamics. These segmentations allow for a detailed examination of market performance based on specific product characteristics, manufacturing forms, and diverse end-use applications, offering valuable insights for strategic planning and resource allocation.- By Product Type: This segment categorizes copper alloys based on their elemental composition and resultant properties. It includes Brass, an alloy of copper and zinc known for its workability and aesthetic appeal; Bronze, an alloy primarily of copper and tin, valued for its strength and corrosion resistance; Copper-Nickel alloys, which offer excellent corrosion resistance, especially in marine environments; Beryllium Copper, renowned for its high strength, hardness, and electrical conductivity; and Other Alloys, encompassing specialized compositions like Cupro-nickel and Silicon Bronze, tailored for specific high-performance applications.

- By Form: This segmentation classifies copper alloys by their manufactured physical state, crucial for understanding their application across industries. It comprises Rods, used for machining and electrical components; Wires, essential for electrical conductivity and cabling; Tubes, critical for plumbing, HVAC, and heat exchangers; Sheets and Plates, widely used in construction, automotive, and industrial fabrication; Strips, common in electrical connectors and automotive applications; Castings, for intricate and robust components; Forgings, for high-strength parts; and Others, including powders for additive manufacturing and billets for further processing.

- By End-Use Industry: This segment analyzes the market based on the major industries consuming copper alloys, reflecting their diverse applications. It encompasses the Electrical & Electronics sector, where copper alloys are vital for wires, cables, connectors, and heat sinks; the Automotive industry, heavily reliant on copper alloys for EV components, radiators, and braking systems; Construction, utilizing copper alloys for plumbing, roofing, architectural elements, and wiring; Industrial Machinery, where they are used in bearings, gears, valves, and heat exchangers; Marine applications, leveraging their corrosion resistance for propellers, valves, and fittings; Defense & Aerospace, requiring high-strength and conductive alloys; Consumer Goods, for appliances and decorative items; and Other sectors, including medical devices and coinage.

Regional Highlights

The global copper alloy market exhibits diverse dynamics across key geographical regions, with certain areas standing out as primary contributors to market growth due to their robust industrial bases, evolving infrastructure, and technological advancements.- Asia Pacific (APAC): This region dominates the global copper alloy market in terms of both production and consumption. Countries like China, India, Japan, and South Korea are at the forefront, driven by rapid industrialization, extensive urban development, and significant manufacturing capabilities in the electrical and electronics, automotive (including a booming EV sector), and construction industries. China's massive infrastructure projects and status as a global manufacturing hub make it a pivotal market. The increasing demand for consumer electronics and continued investment in smart city initiatives further bolster growth in this region.

- Europe: Europe represents a mature yet continually innovating market for copper alloys. Countries such as Germany, Italy, and the UK are key players, driven by a strong automotive sector (especially EV manufacturing), advanced industrial machinery production, and substantial investments in renewable energy infrastructure. Strict environmental regulations also push for high-quality, sustainable copper alloy solutions and promote recycling initiatives within the region, fostering innovation in material science and production processes.

- North America: The market in North America, led by the United States and Canada, is characterized by high demand from the electrical and electronics, aerospace and defense, and automotive sectors. Significant investments in smart grid modernization, telecommunication infrastructure (5G rollout), and a growing emphasis on electric vehicle production are key growth drivers. The region also benefits from robust research and development activities, leading to the adoption of advanced copper alloys in high-performance applications.

- Latin America: This region is an emerging market for copper alloys, primarily driven by increasing urbanization, developing infrastructure, and growth in the automotive and industrial sectors in countries like Brazil and Mexico. While smaller in market share compared to APAC, Latin America presents significant long-term growth potential as industrialization continues and demand for modern infrastructure expands.

- Middle East & Africa (MEA): The MEA region is witnessing growth in the copper alloy market due to large-scale construction projects, diversification of economies away from oil, and growing investments in industrial and energy infrastructure. Countries like UAE, Saudi Arabia, and South Africa are key contributors. The demand for electrical components and pipes for water infrastructure projects also plays a crucial role in market expansion here.

Top Key Players:

The market research report covers the analysis of key stake holders of the Copper Alloy Market. Some of the leading players profiled in the report include -- Wieland-Werke AG

- Aurubis AG

- KME AG

- Mitsubishi Materials Corporation

- Furukawa Electric Co Ltd

- Hitachi Metals Ltd

- JX Nippon Mining & Metals Corporation

- Lebronze alloys SAS

- Chase Brass

- Mueller Industries Inc

- GBC Metals LLC (Olin Brass)

- Luvata

- Poongsan Corporation

- Shanghai Manshan Copper Alloy Co Ltd

- Ningbo Jintian Copper (Group) Co Ltd

- Jiangxi Copper Company Limited

- Halcor SA

- PMX Industries Inc

- Copper & Brass Sales

- Aviva Metals

Frequently Asked Questions:

What is the current market size of the Copper Alloy Market?

The global Copper Alloy Market was valued at USD 215.5 billion in 2025.

What is the projected growth rate for the Copper Alloy Market?

The Copper Alloy Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033.

Which end-use industries are primarily driving the demand for copper alloys?

The primary drivers for copper alloy demand include the electrical and electronics industry, the rapidly expanding automotive sector (especially electric vehicles), and the global construction and infrastructure development sectors.

What are the key types of copper alloys available in the market?

Key types of copper alloys commonly found in the market include Brass (copper-zinc), Bronze (copper-tin), Copper-Nickel, and Beryllium Copper, each offering distinct properties suited for various applications.

Which region is expected to dominate the Copper Alloy Market during the forecast period?

Asia Pacific is expected to maintain its dominance in the Copper Alloy Market throughout the forecast period, driven by significant industrial growth, urbanization, and manufacturing activities in countries like China and India.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted