Continuou Silicon Carbide Fiber Market

Continuou Silicon Carbide Fiber Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701168 | Last Updated : July 29, 2025 |

Format : ![]()

![]()

![]()

![]()

Continuou Silicon Carbide Fiber Market Size

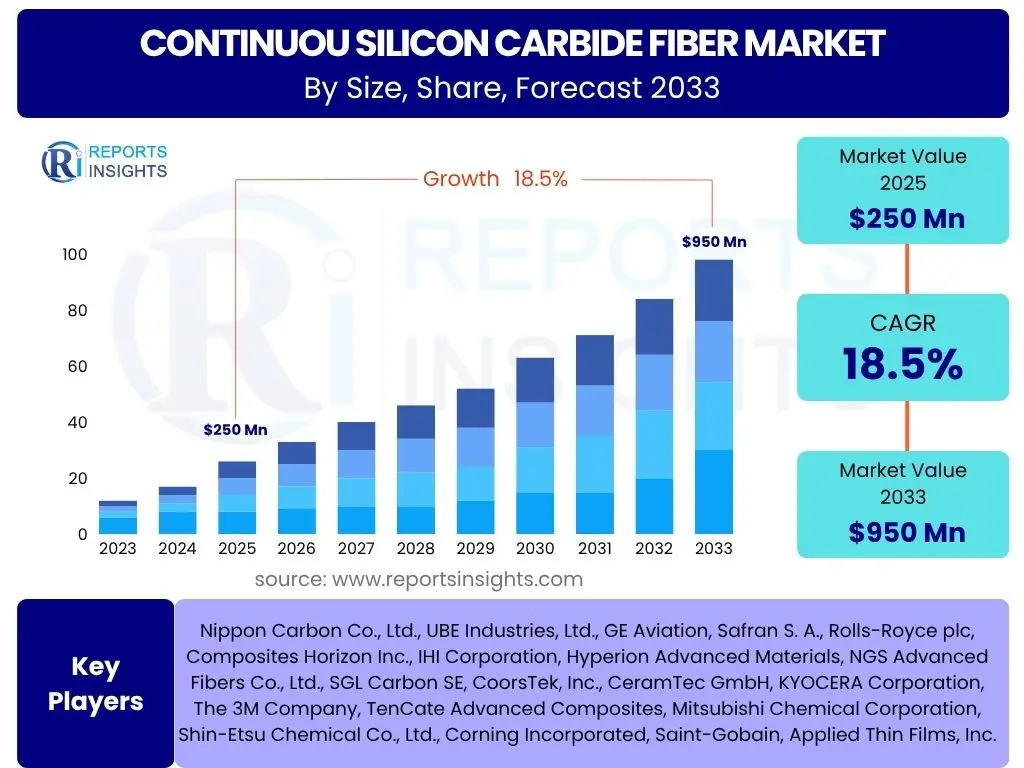

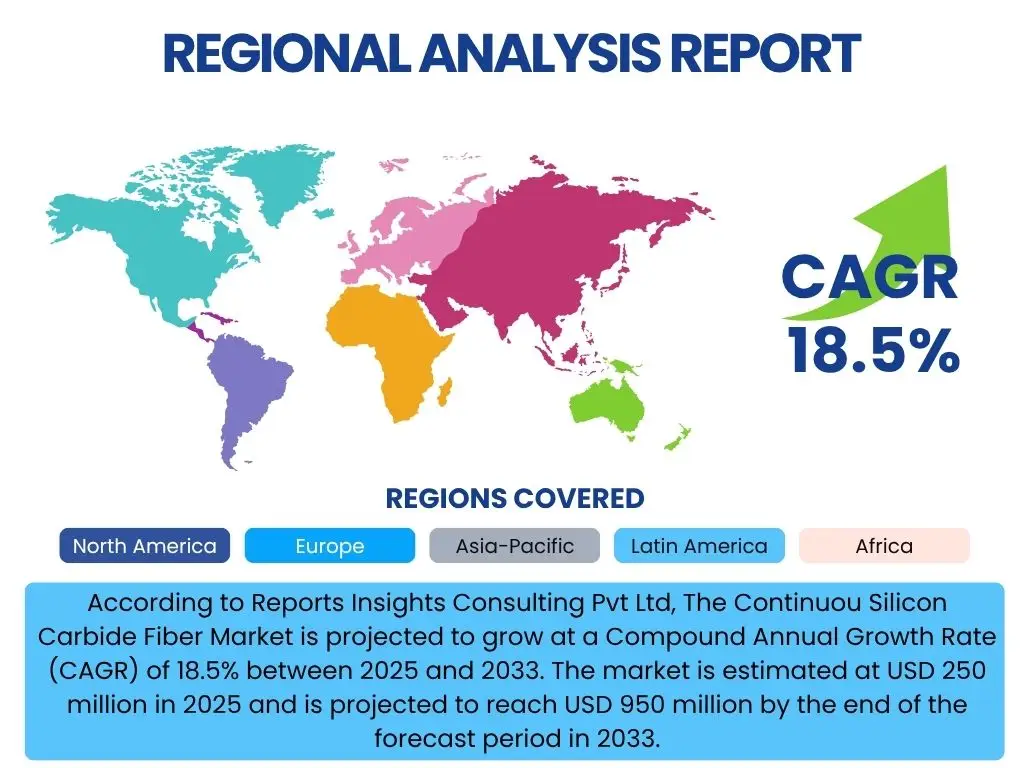

According to Reports Insights Consulting Pvt Ltd, The Continuou Silicon Carbide Fiber Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.5% between 2025 and 2033. The market is estimated at USD 250 million in 2025 and is projected to reach USD 950 million by the end of the forecast period in 2033.

Key Continuou Silicon Carbide Fiber Market Trends & Insights

Common user inquiries about continuous silicon carbide (SiC) fiber market trends frequently revolve around material performance advancements, application diversification, and manufacturing process innovations. Users are keen to understand how SiC fibers are evolving to meet more stringent requirements in extreme environments and whether their adoption is expanding beyond traditional aerospace and defense sectors. There is also significant interest in sustainable production methods and cost reduction strategies, reflecting a broader market shift towards both high performance and economic viability.

Further insights reveal a growing emphasis on optimizing the mechanical properties of SiC fibers, such as tensile strength, creep resistance, and oxidation resistance at ultra-high temperatures, which are critical for next-generation engine components and nuclear applications. The trend also indicates increasing collaboration across the value chain, from raw material suppliers to end-product manufacturers, aiming to standardize production processes and accelerate market penetration. This collaborative approach is essential for overcoming existing barriers related to scalability and material consistency, ensuring SiC fibers meet diverse industrial needs.

- Growing demand for lightweight, high-temperature resistant materials in aerospace and defense.

- Increased R&D in nuclear fusion and fission energy applications requiring extreme environment materials.

- Advancements in manufacturing techniques, including chemical vapor deposition (CVD) and polymer infiltration and pyrolysis (PIP), for enhanced fiber properties and cost efficiency.

- Expanding application scope in industrial furnaces, high-performance brakes, and automotive exhaust systems.

- Emphasis on developing more cost-effective production methods to broaden commercial adoption.

- Development of SiC fiber-reinforced ceramic matrix composites (CMCs) for superior performance in harsh conditions.

- Focus on sustainability and reduced environmental footprint in SiC fiber production.

AI Impact Analysis on Continuou Silicon Carbide Fiber

User questions regarding the impact of AI on continuous silicon carbide (SiC) fiber largely center on its potential to accelerate material discovery, optimize manufacturing processes, and enhance quality control. There is significant curiosity about how AI-driven simulations can predict material behavior under extreme conditions, thereby reducing the need for extensive physical testing and speeding up product development cycles. Users also express interest in AI's role in improving the efficiency and consistency of SiC fiber production, which traditionally faces challenges related to complex processing parameters and high costs.

The key themes emerging from these inquiries highlight expectations that AI will revolutionize the SiC fiber industry by enabling more precise control over synthesis and processing, leading to superior material properties and reduced defects. Users anticipate that AI algorithms can analyze vast datasets from manufacturing operations to identify optimal parameters for fiber spinning, pyrolysis, and coating, thereby improving yield and reducing waste. Furthermore, AI's capability in predictive maintenance for manufacturing equipment is seen as a crucial factor for ensuring continuous, high-quality production and minimizing downtime, directly contributing to the economic viability of SiC fiber manufacturing.

- AI-driven material design and discovery accelerating the development of novel SiC fiber compositions with enhanced properties.

- Optimization of manufacturing parameters (e.g., temperature, pressure, flow rates) using machine learning algorithms for improved yield and consistency.

- Enhanced quality control through AI-powered anomaly detection in fiber production, identifying defects in real-time.

- Predictive maintenance for manufacturing equipment, reducing downtime and operational costs in SiC fiber plants.

- Simulation and modeling of SiC fiber performance under various stress conditions, reducing physical prototyping and testing cycles.

- Supply chain optimization using AI for demand forecasting and inventory management, ensuring timely delivery of raw materials and finished products.

- Robotics and automation integrated with AI for precise handling and processing of delicate SiC fibers during manufacturing.

Key Takeaways Continuou Silicon Carbide Fiber Market Size & Forecast

Analysis of common user questions about the Continuous Silicon Carbide Fiber market size and forecast consistently points to an interest in the significant growth potential, driven by critical applications in high-performance sectors. Users are eager to understand the primary forces propelling this growth, such as increasing demand from aerospace, defense, and advanced energy industries, which require materials capable of withstanding extreme temperatures and harsh environments. The forecast also suggests a strong correlation between sustained investment in R&D and the market's expansion, particularly in developing more cost-effective and scalable manufacturing processes.

Furthermore, inquiries often highlight the importance of technological advancements in overcoming current limitations, such as high production costs and processing complexities, which are perceived as key barriers to broader market adoption. The market's future trajectory is seen as heavily dependent on breakthroughs that can make SiC fibers more accessible and competitive against traditional materials. Overall, the key takeaways underscore a market poised for substantial expansion, underpinned by its unique material properties and the critical need for next-generation composite solutions across a diverse range of high-tech industries.

- The Continuous Silicon Carbide Fiber market is projected for substantial growth, driven by unique high-temperature and lightweight properties.

- Aerospace and defense remain primary drivers, with increasing adoption in advanced engine components and structural applications.

- Emerging applications in nuclear energy, industrial furnaces, and high-performance automotive parts represent significant growth opportunities.

- Technological advancements aimed at reducing manufacturing costs and improving scalability are critical for market expansion.

- Strategic collaborations and R&D investments are fostering innovation in fiber composition and composite integration.

- The market is transitioning towards more widespread commercial use as performance benefits increasingly outweigh initial production challenges.

Continuou Silicon Carbide Fiber Market Drivers Analysis

The market for continuous silicon carbide fibers is significantly driven by the escalating demand for materials capable of performing reliably in extreme conditions. Industries such as aerospace, defense, and energy are continuously seeking materials that offer exceptional high-temperature strength, stiffness, and oxidation resistance, along with lightweight properties. SiC fibers, particularly in the form of ceramic matrix composites (CMCs), are uniquely positioned to meet these stringent requirements, enabling the development of more fuel-efficient aircraft engines, high-performance rocket components, and durable nuclear reactor parts. This imperative for enhanced performance and efficiency across critical sectors forms the foundational demand for SiC fibers.

Another major driver is the ongoing global push for energy efficiency and reduced emissions, especially in the transportation sector. Lightweight materials contribute directly to lower fuel consumption and greenhouse gas emissions, making SiC fibers an attractive option for advanced automotive and aircraft designs. Furthermore, the increasing investment in advanced nuclear power generation, including fusion and Generation IV fission reactors, necessitates materials that can withstand severe radiation environments and extremely high temperatures, thereby creating a long-term growth trajectory for SiC fibers. These factors collectively underscore the vital role of SiC fibers in supporting technological advancements and environmental sustainability goals.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand from Aerospace & Defense | +4.2% | North America, Europe, Asia Pacific | 2025-2033 |

| Growing Focus on Energy Efficiency & Lightweighting | +3.5% | Global | 2025-2033 |

| Advancements in Nuclear Energy & Power Generation | +2.8% | Asia Pacific, North America, Europe | 2028-2033 |

| Superior High-Temperature Performance of SiC Fibers | +3.0% | Global | 2025-2033 |

| Expansion of Ceramic Matrix Composites (CMCs) Market | +2.5% | Global | 2025-2033 |

Continuou Silicon Carbide Fiber Market Restraints Analysis

Despite the compelling advantages, the continuous silicon carbide fiber market faces significant restraints, primarily revolving around the high manufacturing cost. The production of SiC fibers is a complex, energy-intensive process involving specialized raw materials and precise synthesis techniques, such as chemical vapor deposition (CVD) or polymer infiltration and pyrolysis (PIP). These sophisticated methods inherently lead to high production expenses, which translate into a high price per unit for the end product. This elevated cost makes SiC fibers less competitive for applications where traditional materials or other advanced composites offer sufficient performance at a lower price point, thus limiting their broader commercial adoption.

Furthermore, the relatively limited production capacity and the technical complexities associated with processing SiC fibers and integrating them into composites also pose considerable challenges. Scaling up production to meet potential future demand requires substantial capital investment and highly skilled labor, which are not readily available. The brittle nature of ceramic fibers and the specific handling requirements during composite fabrication add another layer of complexity, requiring specialized equipment and expertise. These factors contribute to a constrained supply chain and slower market penetration, acting as key impediments to the otherwise strong growth potential of continuous SiC fibers.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Manufacturing Cost | -3.5% | Global | 2025-2033 |

| Limited Production Capacity & Scalability Issues | -2.0% | Global | 2025-2030 |

| Complex Processing & Fabrication Challenges | -1.5% | Global | 2025-2033 |

| Competition from Alternative High-Performance Materials | -1.0% | Global | 2025-2033 |

Continuou Silicon Carbide Fiber Market Opportunities Analysis

Significant opportunities for the continuous silicon carbide fiber market lie in the expansion into new application areas beyond traditional aerospace and defense. As industries increasingly demand materials that offer extreme temperature resistance, lightweight properties, and corrosion resistance, SiC fibers are finding potential in automotive exhaust systems, high-performance brake discs, and industrial furnace components. The ongoing research and development into more cost-effective production methods, such as alternative precursor materials and advanced spinning techniques, also present a substantial opportunity. Success in reducing manufacturing costs would significantly broaden the addressable market for SiC fibers, making them viable for a wider range of commercial and industrial applications where current costs are prohibitive.

Furthermore, the global push towards advanced nuclear energy technologies, including modular reactors and fusion power, represents a long-term, high-value opportunity. SiC fibers and their composites are crucial for these next-generation reactors due to their exceptional radiation resistance and thermal stability, properties vital for safety and operational longevity. Collaborative efforts between material scientists, manufacturers, and end-users to standardize SiC fiber properties and develop robust design methodologies for SiC/SiC composites will also unlock new market segments. These collaborations can accelerate adoption by ensuring material reliability and promoting confidence in new applications, paving the way for increased market penetration and sustained growth.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into New Application Sectors (Automotive, Industrial) | +3.8% | Asia Pacific, Europe, North America | 2027-2033 |

| Development of Cost-Effective Manufacturing Processes | +3.0% | Global | 2026-2033 |

| Increased Investment in Advanced Nuclear Energy Technologies | +2.5% | North America, Asia Pacific, Europe | 2028-2033 |

| Government Initiatives and Funding for Advanced Materials Research | +1.5% | North America, Europe, China | 2025-2033 |

Continuou Silicon Carbide Fiber Market Challenges Impact Analysis

The continuous silicon carbide fiber market faces several significant challenges, primarily related to the high initial investment required for production facilities and the complexities of achieving large-scale manufacturing. Establishing a SiC fiber production line demands substantial capital for specialized equipment, high-purity raw materials, and advanced processing technologies. This high barrier to entry limits the number of market participants and restricts immediate supply chain flexibility. Furthermore, scaling up production from laboratory or pilot stages to commercial volumes without compromising fiber quality and consistency remains a major technical hurdle, directly impacting market accessibility and cost-effectiveness for broader applications.

Another critical challenge is the inherent brittleness of ceramic fibers, which necessitates careful handling during manufacturing and integration into composite structures. This characteristic complicates composite fabrication processes, making them more labor-intensive and susceptible to defects, which can affect the final component's performance and reliability. Additionally, the nascent stage of standardization for SiC fiber properties and SiC/SiC composite design limits widespread adoption. Without universally accepted standards, potential end-users face uncertainties regarding material performance guarantees and interchangeability, hindering confidence and slowing market growth outside of niche, high-value applications. Addressing these challenges through innovation and industry-wide collaboration is crucial for the market's long-term success.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment & Scalability Challenges | -2.8% | Global | 2025-2030 |

| Brittleness of Ceramic Fibers & Complex Handling | -1.5% | Global | 2025-2033 |

| Lack of Standardized Testing & Characterization Methods | -1.0% | Global | 2025-2029 |

| Intellectual Property Landscape & Licensing Costs | -0.8% | Global | 2025-2033 |

Continuou Silicon Carbide Fiber Market - Updated Report Scope

This report provides a comprehensive analysis of the continuous silicon carbide (SiC) fiber market, detailing its historical performance, current size, and future projections from 2025 to 2033. It examines key market trends, growth drivers, restraints, opportunities, and challenges influencing market dynamics. The scope includes an in-depth segmentation analysis by fiber type, application, and end-use industry, alongside a thorough regional assessment to highlight market variations and opportunities across major geographies. Furthermore, the report offers insights into the competitive landscape, profiling key market players and their strategies, with a specific focus on the impact of artificial intelligence on the industry's evolution.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 250 Million |

| Market Forecast in 2033 | USD 950 Million |

| Growth Rate | 18.5% |

| Number of Pages | 267 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Nippon Carbon Co., Ltd., UBE Industries, Ltd., GE Aviation, Safran S. A., Rolls-Royce plc, Composites Horizon Inc., IHI Corporation, Hyperion Advanced Materials, NGS Advanced Fibers Co., Ltd., SGL Carbon SE, CoorsTek, Inc., CeramTec GmbH, KYOCERA Corporation, The 3M Company, TenCate Advanced Composites, Mitsubishi Chemical Corporation, Shin-Etsu Chemical Co., Ltd., Corning Incorporated, Saint-Gobain, Applied Thin Films, Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The continuous silicon carbide fiber market is comprehensively segmented to provide granular insights into its diverse applications and technological variations. This segmentation helps in understanding the specific drivers and opportunities within each sub-segment, allowing for targeted strategic planning. The primary categories for segmentation include fiber type, which differentiates between stoichiometric and non-stoichiometric compositions based on their atomic ratios and resultant properties; application, which details how these fibers are integrated into various composite structures like ceramic matrix composites (CMCs), metal matrix composites (MMCs), and polymer matrix composites (PMCs); and end-use industry, which identifies the major sectors benefiting from SiC fiber adoption such as aerospace & defense, energy, and industrial manufacturing.

Further analysis within these segments reveals that stoichiometric SiC fibers, known for their superior high-temperature stability and strength retention, dominate critical aerospace and nuclear applications, while non-stoichiometric fibers offer a balance of performance and cost, making them suitable for broader industrial uses. The CMCs segment holds the largest share due to their exceptional performance in extreme environments, but growing interest in MMCs and PMCs for specific lightweighting and structural applications is also evident. Understanding these detailed segmentations is crucial for market participants to identify lucrative niches, anticipate demand shifts, and tailor their product offerings to specific industry needs.

- By Fiber Type: This segment analyzes the market based on the chemical composition of the SiC fibers.

- Stoichiometric SiC Fiber: Characterized by a near 1:1 ratio of silicon to carbon, offering excellent high-temperature properties and creep resistance. Primarily used in demanding aerospace and nuclear applications.

- Non-stoichiometric SiC Fiber: Contains excess carbon or oxygen, leading to variations in properties. Often more cost-effective to produce and suitable for a wider range of industrial applications.

- Others (e.g., Oxycarbide Fibers): Includes other variations with specific property profiles.

- By Application: This segment categorizes the market based on how SiC fibers are utilized in various composite structures and materials.

- Ceramic Matrix Composites (CMCs): The largest and most critical application, where SiC fibers reinforce ceramic matrices for extreme temperature and environmental resistance in aerospace engines, nuclear reactors, and industrial furnaces.

- Metal Matrix Composites (MMCs): SiC fibers reinforcing metal matrices, offering enhanced strength, stiffness, and wear resistance at elevated temperatures, used in automotive and specific industrial components.

- Polymer Matrix Composites (PMCs): SiC fibers providing superior mechanical properties to polymer matrices, particularly in high-performance structural parts where stiffness and heat resistance are crucial.

- Filtration Media: Utilized in high-temperature gas filtration due to chemical inertness and thermal stability.

- Others: Includes applications in heating elements, cutting tools, and specialized sports equipment.

- By End-Use Industry: This segment examines the demand for SiC fibers across different industrial sectors.

- Aerospace & Defense: Dominant sector, utilizing SiC/SiC CMCs for turbine engine components, exhaust nozzles, and missile parts due to high-temperature capabilities and lightweighting.

- Energy (Nuclear, Power Generation): Crucial for next-generation nuclear reactors (fusion and fission) requiring radiation-resistant and high-temperature tolerant materials; also used in power generation systems.

- Industrial (Furnaces, Heat Exchangers): Applications in high-temperature industrial processes, including furnace linings, heat exchangers, and chemical processing equipment due to thermal and chemical stability.

- Automotive: Emerging applications in lightweight structural components, high-performance brake systems, and hot section parts for improved fuel efficiency and durability.

- Others (e.g., Sports & Leisure, Medical): Niche applications in high-performance sporting goods, specialized medical devices, and research equipment.

Regional Highlights

- North America: This region holds a significant share in the continuous silicon carbide fiber market, primarily driven by robust investments in the aerospace and defense sectors, particularly in the United States. The presence of major aircraft engine manufacturers, defense contractors, and strong government funding for advanced materials research positions North America as a leading consumer and innovator. The focus on developing next-generation fighter jets, advanced propulsion systems, and space exploration technologies continues to fuel the demand for high-performance SiC fiber composites, contributing substantially to regional market growth.

- Europe: Europe represents another key market, propelled by its strong aerospace industry, particularly in countries like France, the UK, and Germany, alongside significant investments in industrial manufacturing and energy sectors. The region's emphasis on fuel efficiency standards and emission reductions in aviation and automotive industries drives the adoption of lightweight, high-temperature resistant materials. Additionally, European research initiatives and collaborations in advanced ceramics and composites support market expansion, fostering innovation in SiC fiber production and application development across diverse industrial verticals.

- Asia Pacific (APAC): The Asia Pacific region is projected to be the fastest-growing market for continuous SiC fibers, driven by rapid industrialization, increasing defense expenditures, and a burgeoning aerospace sector, especially in China, Japan, and India. Significant government support for advanced materials development and a growing focus on energy security, including nuclear power expansion, are key accelerators. The region's expanding manufacturing capabilities and the establishment of new production facilities contribute to both demand and supply-side growth, making APAC a critical hub for future market opportunities.

- Latin America: While currently a smaller market, Latin America is expected to witness steady growth, primarily influenced by increasing investments in its emerging aerospace and defense sectors. Countries like Brazil are focusing on modernizing their aviation industries and enhancing defense capabilities, leading to a gradual increase in demand for advanced materials. As industrial development progresses and technological adoption accelerates, the market for continuous SiC fibers is anticipated to expand, driven by requirements for enhanced performance and efficiency in various industrial applications.

- Middle East and Africa (MEA): The MEA region is at an nascent stage but holds potential for the continuous silicon carbide fiber market, largely driven by strategic investments in defense modernization and emerging energy projects. Countries within the Middle East are expanding their defense capabilities and investing in new energy infrastructure, including some nuclear ambitions, which will incrementally increase the demand for high-performance materials. While market penetration is currently limited, long-term growth is expected as industrial diversification efforts mature and the need for durable, high-temperature materials becomes more prevalent across various sectors.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Continuou Silicon Carbide Fiber Market.- Nippon Carbon Co., Ltd.

- UBE Industries, Ltd.

- GE Aviation

- Safran S. A.

- Rolls-Royce plc

- Composites Horizon Inc.

- IHI Corporation

- Hyperion Advanced Materials

- NGS Advanced Fibers Co., Ltd.

- SGL Carbon SE

- CoorsTek, Inc.

- CeramTec GmbH

- KYOCERA Corporation

- The 3M Company

- TenCate Advanced Composites

- Mitsubishi Chemical Corporation

- Shin-Etsu Chemical Co., Ltd.

- Corning Incorporated

- Saint-Gobain

- Applied Thin Films, Inc.

Frequently Asked Questions

Analyze common user questions about the Continuou Silicon Carbide Fiber market and generate a concise list of summarized FAQs reflecting key topics and concerns.What are Continuous Silicon Carbide Fibers used for?

Continuous Silicon Carbide (SiC) fibers are primarily used as reinforcement in advanced composites, especially Ceramic Matrix Composites (CMCs), Metal Matrix Composites (MMCs), and Polymer Matrix Composites (PMCs). Their unique properties make them ideal for applications requiring exceptional high-temperature strength, stiffness, lightweighting, and chemical resistance, particularly in aerospace engine components, nuclear reactors, and industrial furnaces.

Why is the Continuous SiC Fiber market experiencing growth?

The market is growing due to increasing demand from high-performance industries like aerospace, defense, and energy, which require materials capable of operating in extreme conditions. The push for lightweighting for fuel efficiency, advancements in nuclear power generation, and the superior thermal and mechanical properties of SiC fibers compared to traditional materials are key growth drivers.

What are the main challenges in the Continuous SiC Fiber market?

Key challenges include the high manufacturing cost of SiC fibers due to complex production processes, limited production capacity and scalability issues, and the inherent brittleness of ceramic fibers requiring specialized handling. The lack of fully standardized testing and characterization methods also presents a hurdle for broader commercial adoption.

How does AI impact the Continuous SiC Fiber industry?

AI impacts the SiC fiber industry by accelerating material design and discovery, optimizing manufacturing parameters for improved yield and consistency, enhancing quality control through real-time defect detection, and enabling predictive maintenance for production equipment. AI-driven simulations also reduce the need for extensive physical testing, speeding up development.

Which regions are leading the Continuous SiC Fiber market?

North America and Europe are currently leading the market due to strong aerospace, defense, and industrial sectors, coupled with significant R&D investments. However, the Asia Pacific region, particularly China, Japan, and India, is projected to be the fastest-growing market, driven by rapid industrialization, increasing defense spending, and expanding energy infrastructure.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted