Containerboard Market

Containerboard Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702977 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

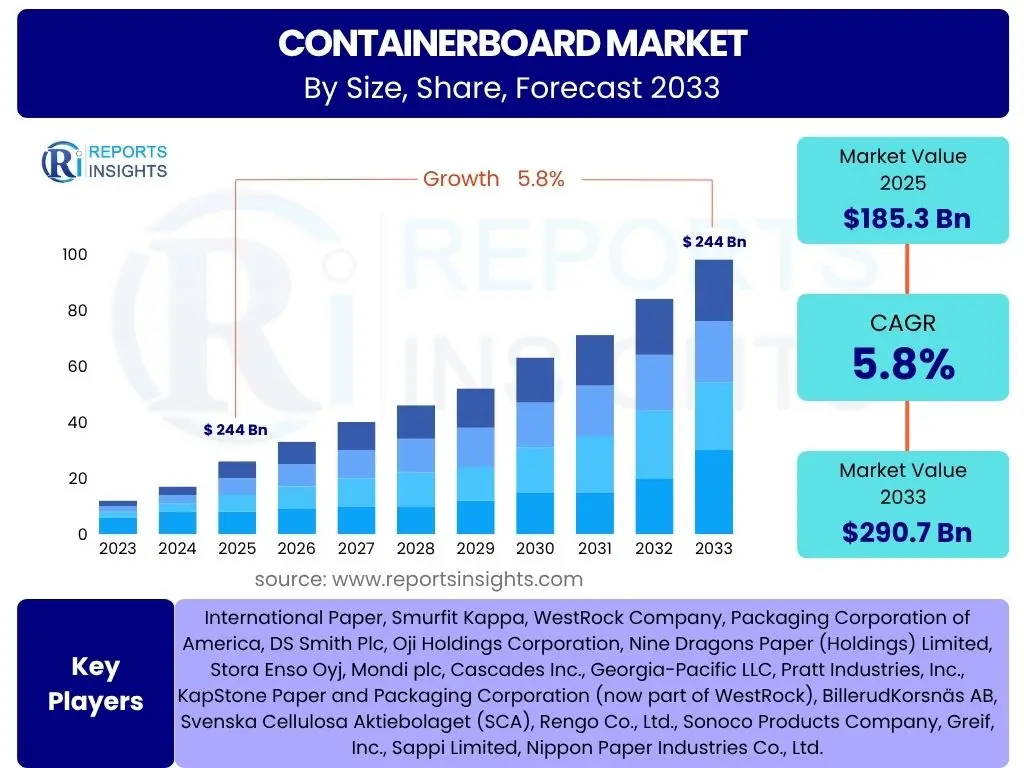

Containerboard Market Size

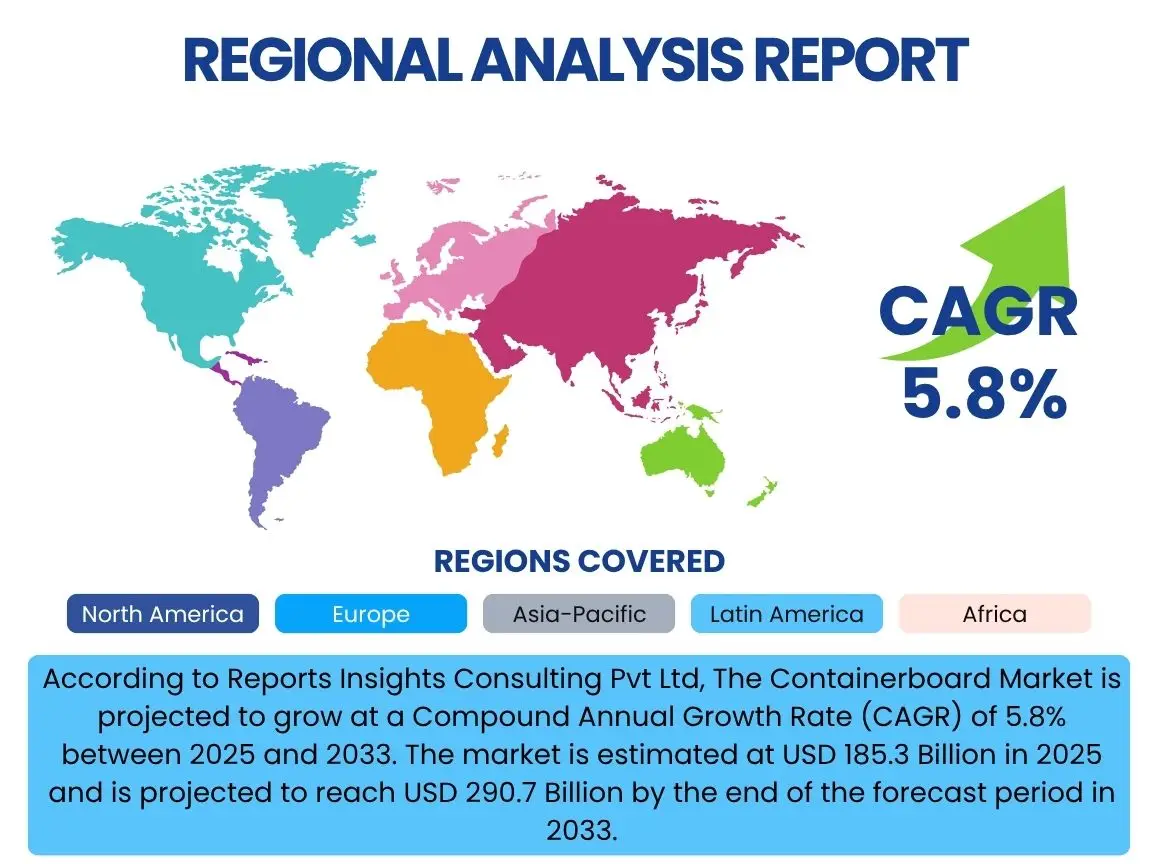

According to Reports Insights Consulting Pvt Ltd, The Containerboard Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 185.3 Billion in 2025 and is projected to reach USD 290.7 Billion by the end of the forecast period in 2033.

Key Containerboard Market Trends & Insights

The containerboard market is experiencing significant shifts driven by evolving consumer behaviors, sustainability imperatives, and technological advancements. Key inquiries from users often center on the impact of e-commerce expansion, the increasing demand for eco-friendly packaging solutions, and the ongoing innovations in material science aimed at enhancing product performance while reducing environmental footprint. These trends collectively shape the strategic direction for manufacturers and influence investment decisions across the value chain, pushing the industry towards more resilient and responsible practices.

Furthermore, the focus on supply chain efficiency and the adoption of advanced manufacturing processes are frequently highlighted by market participants. Users are keen to understand how global logistics networks influence containerboard demand and how automation in packaging lines is impacting material specifications. The interplay between these operational efficiencies and the broader market trends indicates a move towards integrated solutions that deliver both economic and environmental benefits.

- Exponential growth of e-commerce necessitating robust and sustainable packaging.

- Rising consumer and regulatory demand for recycled content and recyclable packaging solutions.

- Innovation in lightweighting and high-performance containerboard for optimized logistics.

- Shift towards digital printing on corrugated packaging for customization and branding.

- Increased focus on circular economy principles in raw material sourcing and end-of-life management.

AI Impact Analysis on Containerboard

Common user questions regarding AI's impact on the containerboard sector frequently revolve around its potential to revolutionize manufacturing processes, enhance supply chain efficiency, and improve product quality. There is significant interest in how artificial intelligence can optimize resource allocation, predict maintenance needs for machinery, and streamline inventory management, thereby reducing operational costs and waste. Users are particularly keen on understanding AI's role in creating more agile and responsive production environments that can adapt quickly to market fluctuations and consumer demands.

Beyond manufacturing, inquiries often extend to AI's influence on demand forecasting and customer relationship management within the containerboard industry. The ability of AI to analyze vast datasets for more accurate demand predictions allows companies to optimize production schedules and minimize overstocking or shortages. Additionally, users are exploring how AI-driven insights can lead to more personalized packaging solutions and improved customer service, fostering stronger client relationships and unlocking new revenue streams for containerboard manufacturers and converters.

- Optimized production scheduling and predictive maintenance reducing downtime and costs.

- Enhanced quality control through AI-powered vision systems for defect detection.

- Improved demand forecasting and inventory management via advanced analytics.

- Streamlined supply chain logistics and route optimization for reduced transportation costs.

- Development of AI-driven tools for designing and prototyping more efficient and sustainable packaging solutions.

Key Takeaways Containerboard Market Size & Forecast

Analysis of user inquiries about the containerboard market size and forecast reveals a strong interest in understanding the underlying drivers of growth and the long-term sustainability of this expansion. Users are particularly focused on how the sustained rise in e-commerce activity is translating into tangible demand for corrugated packaging, and whether the industry is adequately prepared to meet this escalating requirement. The emphasis is on identifying the most impactful factors contributing to the market's projected growth trajectory through 2033, alongside potential headwinds.

Furthermore, a significant portion of user questions pertains to the regional dynamics and the role of innovation in shaping future market opportunities. Stakeholders are keen to discern which geographical areas are poised for the most robust growth and how advancements in material science, such as lightweighting and enhanced barrier properties, will influence market segmentation and competitive landscapes. These insights are crucial for strategic planning and investment decisions within the global containerboard ecosystem.

- The containerboard market is poised for robust expansion, primarily fueled by global e-commerce proliferation and heightened demand for sustainable packaging.

- Technological advancements in manufacturing and supply chain management are critical for maintaining competitive edge and operational efficiency.

- Asia Pacific continues to be a pivotal region, offering significant growth avenues due to rapid industrialization and urbanization.

- Sustainability initiatives, including increased use of recycled content, are not just regulatory mandates but also key drivers for market innovation and consumer preference.

- Strategic investments in automation and AI integration are essential for future scalability and responsiveness to dynamic market needs.

Containerboard Market Drivers Analysis

The burgeoning e-commerce sector stands as a primary catalyst for the containerboard market's expansion. As online retail continues its exponential growth globally, the demand for robust, protective, and cost-effective packaging solutions to ensure safe product delivery has surged. Containerboard, due to its versatility, strength, and recyclability, is the material of choice for shipping everything from electronics to groceries, making its growth intrinsically linked to the digital commerce revolution.

Moreover, the increasing global emphasis on sustainable packaging solutions is significantly driving the adoption of containerboard. Consumers and corporations alike are prioritizing environmentally friendly materials, moving away from plastics towards renewable and recyclable alternatives. Containerboard, being derived from wood fibers and highly recyclable, perfectly aligns with these sustainability goals, positioning it as a preferred material in the circular economy framework.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| E-commerce Growth | +1.8% | Global, particularly North America, Asia Pacific | Short to Long-Term |

| Increased Demand for Sustainable Packaging | +1.5% | Europe, North America, developing Asia Pacific economies | Mid to Long-Term |

| Urbanization and Rise in Disposable Income | +0.9% | Asia Pacific (China, India), Latin America | Mid to Long-Term |

| Growth of Food & Beverage Industry | +0.8% | Global, particularly emerging markets | Short to Mid-Term |

| Industrial Production Expansion | +0.5% | Asia Pacific, North America, Europe | Short to Mid-Term |

Containerboard Market Restraints Analysis

The containerboard market faces significant restraints, notably the volatility of raw material prices. The cost of virgin pulp and recycled fiber, the primary inputs for containerboard production, is subject to fluctuations influenced by global supply-demand dynamics, energy costs, and geopolitical factors. Such price instability directly impacts manufacturing costs and profit margins for producers, leading to potential market instability and reduced investment in capacity expansion or innovation.

Furthermore, increasing stringent environmental regulations, while promoting sustainability, can also act as a restraint. Compliance with evolving waste management directives, forestry certifications, and emissions standards often necessitates significant capital expenditure on new equipment and processes. This can burden manufacturers, particularly smaller players, and potentially lead to higher production costs which may be passed on to consumers, impacting the competitiveness of containerboard against alternative packaging materials.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Raw Material Price Volatility | -1.2% | Global | Short to Mid-Term |

| Stringent Environmental Regulations | -0.8% | Europe, North America, developed Asia Pacific | Mid to Long-Term |

| Competition from Alternative Packaging Materials | -0.7% | Global | Mid to Long-Term |

| High Energy Costs | -0.5% | Global | Short to Mid-Term |

Containerboard Market Opportunities Analysis

The containerboard market is presented with significant opportunities driven by ongoing innovation in product development, particularly in the realm of lightweighting and enhanced barrier properties. Developing lighter yet equally strong containerboard reduces transportation costs and carbon footprint, aligning with both economic and environmental objectives. Furthermore, improving moisture and grease barrier properties expands the application scope of containerboard into new segments like fresh food packaging, traditionally dominated by plastic, thereby opening up new revenue streams.

Another substantial opportunity lies in the burgeoning demand for sustainable and recyclable packaging solutions, especially in emerging economies. As these regions experience rapid urbanization and increased consumer awareness regarding environmental issues, the preference for eco-friendly packaging is growing. Containerboard, being inherently sustainable and widely recyclable, is well-positioned to capitalize on this shift, offering a viable alternative to less sustainable materials and fostering market penetration in previously underserved areas.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Innovation in Lightweighting and Barrier Properties | +1.0% | Global | Mid to Long-Term |

| Expansion in Emerging Economies and E-commerce Adoption | +1.5% | Asia Pacific, Latin America, Africa | Short to Long-Term |

| Increased Adoption of Recycled Content | +0.8% | Europe, North America, developed Asia Pacific | Mid to Long-Term |

| Development of Smart Packaging Solutions | +0.6% | Global, particularly developed markets | Long-Term |

Containerboard Market Challenges Impact Analysis

The containerboard market faces notable challenges, including global supply chain disruptions that have become more prevalent in recent years. Events such as pandemics, geopolitical conflicts, and natural disasters can severely impact the availability of raw materials, disrupt logistics, and lead to significant production delays. These disruptions not only escalate operational costs but also make it difficult for manufacturers to consistently meet demand, leading to market volatility and potential loss of competitive edge.

Another significant challenge is the rising cost of energy and transportation, which directly affects the profitability of containerboard production and distribution. Manufacturing containerboard is an energy-intensive process, and fluctuating energy prices can erode profit margins. Similarly, the increasing cost of fuel and logistical bottlenecks impact the entire supply chain, from raw material procurement to product delivery, adding to the overall cost burden for industry players and influencing market pricing strategies.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Supply Chain Disruptions | -1.0% | Global | Short to Mid-Term |

| Volatile Energy & Transportation Costs | -0.9% | Global | Short to Mid-Term |

| Availability and Quality of Recycled Fiber | -0.6% | Global | Mid to Long-Term |

| Intense Competition and Pricing Pressures | -0.4% | Global | Short to Mid-Term |

Containerboard Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global containerboard market, offering a detailed assessment of its current status and future growth trajectory. The scope includes a thorough examination of market size, trends, drivers, restraints, opportunities, and challenges influencing the industry from 2019 to 2033. Emphasis is placed on market segmentation, regional dynamics, and the competitive landscape, providing stakeholders with critical insights for strategic decision-making and market positioning.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 185.3 Billion |

| Market Forecast in 2033 | USD 290.7 Billion |

| Growth Rate | 5.8% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | International Paper, Smurfit Kappa, WestRock Company, Packaging Corporation of America, DS Smith Plc, Oji Holdings Corporation, Nine Dragons Paper (Holdings) Limited, Stora Enso Oyj, Mondi plc, Cascades Inc., Georgia-Pacific LLC, Pratt Industries, Inc., KapStone Paper and Packaging Corporation (now part of WestRock), BillerudKorsnäs AB, Svenska Cellulosa Aktiebolaget (SCA), Rengo Co., Ltd., Sonoco Products Company, Greif, Inc., Sappi Limited, Nippon Paper Industries Co., Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The containerboard market is meticulously segmented to provide a granular understanding of its diverse applications and material compositions. This segmentation offers valuable insights into specific market dynamics, allowing stakeholders to identify niche opportunities and tailor strategies effectively. The primary categories for analysis include product type, raw material composition, basis weight, and the wide array of end-use industries that rely on containerboard for packaging and protection.

Each segment exhibits unique growth patterns and demand drivers. For instance, the distinction between virgin and recycled containerboard highlights the industry's commitment to sustainability and resource efficiency, while the various end-use sectors underscore the ubiquitous nature of corrugated packaging across consumer and industrial goods. Understanding these segments is paramount for forecasting future demand and innovation trajectories within the market.

- By Product Type:

- Linerboard

- Corrugating Medium

- By Material:

- Recycled Containerboard

- Virgin Containerboard

- By Basis Weight:

- Less than 125 gsm

- 125-200 gsm

- More than 200 gsm

- By End Use Industry:

- Food & Beverage

- Industrial

- Consumer Durables

- Building & Construction

- E-commerce

- Others (e.g., Pharmaceuticals, Apparel, Cosmetics)

Regional Highlights

- North America: A mature market with strong demand driven by established e-commerce infrastructure, robust manufacturing, and increasing focus on sustainable packaging solutions. The region is a key adopter of advanced packaging technologies and high-strength containerboard.

- Europe: Characterized by stringent environmental regulations and a strong emphasis on circular economy principles, leading to high demand for recycled content containerboard. Innovation in lightweighting and specialized packaging for fresh produce and e-commerce is prominent.

- Asia Pacific (APAC): The fastest-growing market, propelled by rapid industrialization, burgeoning e-commerce penetration, expanding manufacturing bases, and rising disposable incomes in countries like China, India, and Southeast Asia. Significant opportunities exist for capacity expansion and technological adoption.

- Latin America: Experiencing steady growth fueled by increasing industrial activity, expanding retail sectors, and developing e-commerce markets. Economic stability and foreign investments are key factors influencing market demand.

- Middle East and Africa (MEA): Emerging market with growing demand from the food & beverage sector, ongoing infrastructure projects, and developing e-commerce platforms. Market growth is influenced by economic diversification efforts and urbanization trends.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Containerboard Market.- International Paper

- Smurfit Kappa

- WestRock Company

- Packaging Corporation of America

- DS Smith Plc

- Oji Holdings Corporation

- Nine Dragons Paper (Holdings) Limited

- Stora Enso Oyj

- Mondi plc

- Cascades Inc.

- Georgia-Pacific LLC

- Pratt Industries, Inc.

- BillerudKorsnäs AB

- Svenska Cellulosa Aktiebolaget (SCA)

- Rengo Co., Ltd.

- Sonoco Products Company

- Greif, Inc.

- Sappi Limited

- Nippon Paper Industries Co., Ltd.

- Klabin S.A.

Frequently Asked Questions

Analyze common user questions about the Containerboard market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is containerboard and how is it different from other paper products?

Containerboard is a specialized paper product primarily used to manufacture corrugated cardboard. Unlike regular paper, it is engineered for strength, durability, and resistance to compression, essential properties for protective packaging. It typically comes in two forms: linerboard, which forms the outer layers, and corrugating medium, which is fluted and sandwiched between the linerboards.

What are the primary drivers of growth in the containerboard market?

The key drivers for containerboard market growth include the exponential rise of e-commerce, increasing demand for sustainable and recyclable packaging solutions, and the expansion of industrial production and the food and beverage industry globally. Urbanization and rising disposable incomes also contribute to sustained demand.

How is sustainability impacting the containerboard industry?

Sustainability is profoundly impacting the containerboard industry by driving demand for recycled content, promoting circular economy practices, and fostering innovations in lightweighting and responsible forestry. Consumers and regulations increasingly favor containerboard due to its renewability and recyclability, pushing manufacturers to enhance their environmental performance.

What are the main challenges faced by containerboard manufacturers?

Key challenges for containerboard manufacturers include volatility in raw material prices (pulp and recycled fiber), fluctuating energy and transportation costs, increasing stringency of environmental regulations, and managing global supply chain disruptions. Intense competition and the availability of quality recycled fiber also pose significant hurdles.

Which regions are leading the growth in the containerboard market?

The Asia Pacific region, particularly countries like China and India, is leading growth in the containerboard market due to rapid industrialization, booming e-commerce, and expanding consumer markets. North America and Europe also maintain significant market shares, driven by established industries and strong sustainable packaging initiatives.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted