Connector Market

Connector Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702731 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

Connector Market Size

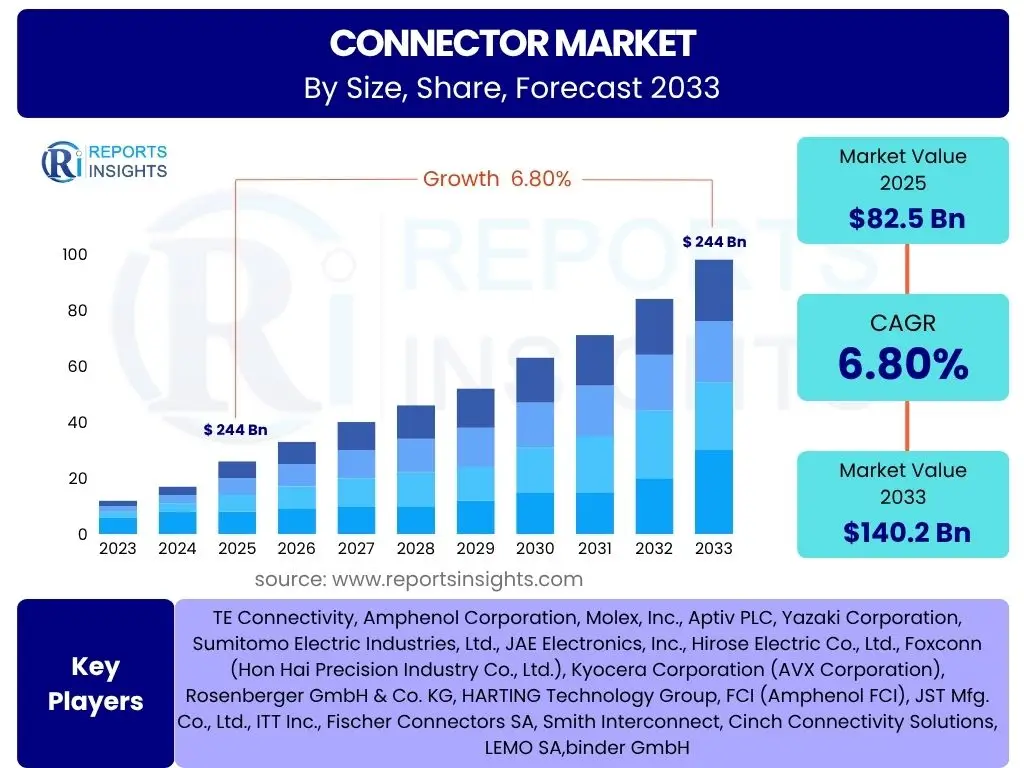

According to Reports Insights Consulting Pvt Ltd, The Connector Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 82.5 billion in 2025 and is projected to reach USD 140.2 billion by the end of the forecast period in 2033.

The growth trajectory of the connector market is underpinned by increasing digitalization across various industries, coupled with the rapid expansion of data centers and the proliferation of IoT devices. Miniaturization trends and the demand for high-speed data transmission capabilities are also significant contributors to this market expansion. Furthermore, the automotive sector's shift towards electric vehicles (EVs) and advanced driver-assistance systems (ADAS) is creating substantial demand for robust and high-performance connectors, driving the market forward.

Geographically, Asia Pacific is expected to remain the dominant region, fueled by its robust manufacturing base, burgeoning consumer electronics industry, and widespread adoption of 5G infrastructure. North America and Europe are also anticipated to exhibit steady growth due to ongoing investments in industrial automation, aerospace, and medical technologies, all of which heavily rely on advanced connector solutions. The global supply chain dynamics and raw material availability will continue to influence market pricing and production capacities.

Key Connector Market Trends & Insights

User inquiries frequently highlight the evolving landscape of connectivity solutions, focusing on how technological advancements are shaping product development and application. Common questions revolve around the push for smaller, more efficient connectors, the integration of smart functionalities, and the imperative for reliability in harsh operating environments. There is significant interest in understanding the impact of high-speed data requirements, power density demands, and the adoption of new materials and manufacturing processes within the connector industry.

These inquiries underscore a collective industry interest in next-generation connectivity, emphasizing the move towards hyper-converged solutions and the ability of connectors to support complex ecosystems. The trend towards modularity and interoperability is also a recurring theme, reflecting the need for flexible and scalable solutions that can adapt to diverse technological infrastructures. Furthermore, sustainability in manufacturing and the lifecycle of connectors are gaining prominence as a key concern for end-users and manufacturers alike, driving innovation in eco-friendly materials and production techniques.

- Miniaturization and high-density packaging for space-constrained applications.

- Increased demand for high-speed data transmission (e.g., PCIe Gen 5/6, USB4, Thunderbolt).

- Growth in power connectors for EV, industrial, and data center applications.

- Development of smart connectors with integrated sensors and diagnostic capabilities.

- Enhanced ruggedization for harsh environments (temperature, vibration, moisture).

- Adoption of optical fiber connectors for superior bandwidth and EMI immunity.

- Focus on modularity and customization for diverse application requirements.

- Integration of advanced materials for improved performance and durability.

- Emphasis on sustainability and eco-friendly manufacturing processes.

AI Impact Analysis on Connector

User queries regarding the impact of Artificial Intelligence (AI) on the connector market frequently explore how AI influences design, manufacturing processes, and the performance requirements of connectors themselves. Common questions include how AI tools are used for optimizing connector layouts, predicting failure points, or enhancing quality control in production. There is also significant interest in understanding the demand for specialized connectors to support AI-driven hardware, such as GPUs, FPGAs, and high-bandwidth memory modules, which require extremely high data rates and power delivery capabilities.

Furthermore, discussions often center on how AI-powered predictive maintenance can extend the lifespan of connectors in critical infrastructure by monitoring performance and detecting anomalies. Users also inquire about the role of AI in supply chain optimization for connector manufacturing, including demand forecasting and inventory management. The overarching theme is how AI transforms both the production and the end-use applications of connectors, pushing the boundaries of what is possible in terms of speed, reliability, and efficiency for data and power transmission in AI-centric systems.

- AI-driven design optimization for miniaturization and performance enhancement.

- AI in manufacturing for improved quality control, predictive maintenance, and efficiency.

- Increased demand for high-performance connectors for AI accelerators and servers.

- AI enabling smart connectors with self-monitoring and diagnostic features.

- Supply chain optimization in connector production through AI-powered analytics.

- Enhanced thermal management requirements due to high-power AI components.

- Development of new testing methodologies leveraging AI for rapid validation.

Key Takeaways Connector Market Size & Forecast

Analysis of common user questions regarding the connector market size and forecast reveals a keen interest in identifying the primary drivers of growth, understanding the impact of technological shifts, and recognizing key geographical opportunities. Users frequently inquire about the segments expected to experience the most significant expansion, particularly those related to emerging technologies like 5G, IoT, and electric vehicles. There is also considerable focus on the resilience of the market against economic fluctuations and supply chain challenges, seeking clarity on long-term stability and investment potential.

These inquiries collectively highlight a desire for strategic insights into market sustainability and future direction. Stakeholders are keen to understand which product types and end-use applications will present the most lucrative prospects, as well as the competitive dynamics that will shape the industry. The discussions often touch upon the importance of innovation in maintaining market leadership and the potential for new entrants or disruptive technologies to alter the existing landscape, reinforcing the need for continuous market monitoring and adaptive business strategies.

- Robust growth driven by digitalization, IoT, 5G, and electric vehicle adoption.

- Asia Pacific maintains market dominance due to manufacturing and consumer electronics.

- High-speed and high-power connectors are key growth segments.

- Miniaturization remains a critical design imperative across applications.

- Supply chain resilience and material innovations are central to market stability.

Connector Market Drivers Analysis

The global connector market is experiencing significant tailwinds from several macro and microeconomic factors that are collectively driving demand and innovation. A primary driver is the accelerating pace of digital transformation across all industries, leading to an increased need for reliable and efficient data and power connectivity. The proliferation of IoT devices, from smart homes to industrial sensors, necessitates a vast array of specialized connectors capable of functioning in diverse environments and transmitting varying data volumes.

Furthermore, the automotive industry's paradigm shift towards electric vehicles (EVs) and autonomous driving systems is creating unprecedented demand for high-voltage, high-current, and high-speed data connectors. The continuous expansion of data centers and cloud infrastructure, essential for supporting AI, big data, and cloud computing, requires sophisticated and robust connectivity solutions. Additionally, advancements in consumer electronics, industrial automation (Industry 4.0), and the global rollout of 5G networks are propelling the demand for high-performance and miniaturized connectors, underpinning sustained market growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Adoption of IoT Devices | +1.5% | Global, particularly APAC & North America | 2025-2033 |

| Growth in Electric Vehicles (EVs) & ADAS | +1.8% | Europe, North America, China | 2025-2033 |

| Expansion of Data Centers & Cloud Computing | +1.2% | North America, Europe, China, India | 2025-2033 |

| Global 5G Network Deployments | +1.0% | Global, especially APAC, North America | 2025-2030 |

| Increasing Automation in Industries (Industry 4.0) | +0.8% | Germany, Japan, North America, China | 2025-2033 |

Connector Market Restraints Analysis

Despite the robust growth prospects, the connector market faces several significant restraints that could impede its full potential. One major challenge is the volatility in raw material prices, particularly for metals like copper, gold, and palladium, which are essential components in connector manufacturing. These price fluctuations directly impact production costs and profit margins, making long-term planning more complex for manufacturers. Furthermore, complex and fragmented supply chains, exacerbated by geopolitical tensions and trade disputes, can lead to disruptions in the availability of components and delays in product delivery.

Another crucial restraint is the intense price competition prevalent in the market, driven by a large number of established players and the entry of new manufacturers, particularly from Asian markets. This competitive pressure often forces companies to lower prices, affecting profitability and limiting investment in research and development for innovative solutions. Additionally, the rapid pace of technological change and standardization challenges across different industries can lead to product obsolescence, requiring continuous adaptation and significant R&D investment to remain competitive, which can be a strain, especially for smaller market participants.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile Raw Material Prices | -0.7% | Global | 2025-2033 |

| Intense Price Competition | -0.5% | Global | 2025-2033 |

| Complex & Fragile Supply Chains | -0.6% | Global | 2025-2028 |

| High R&D Costs & Short Product Lifecycles | -0.4% | Global | 2025-2033 |

Connector Market Opportunities Analysis

The connector market is poised for significant growth through various emerging opportunities that can be strategically leveraged by market players. The continued development of smart cities and smart infrastructure projects worldwide presents a vast untapped potential for advanced connectivity solutions, ranging from smart streetlights to intelligent transportation systems. These initiatives require robust, reliable, and often ruggedized connectors capable of operating in diverse urban environments, creating a new segment for specialized products.

Furthermore, the increasing adoption of sustainable practices and green technologies across industries offers a compelling opportunity for innovation in connector design and manufacturing. This includes the development of connectors made from recycled materials, energy-efficient production processes, and solutions for renewable energy systems like solar and wind power. The expansion into niche and high-growth application areas such as medical devices, aerospace and defense, and industrial robots, which demand highly specialized and performance-critical connectors, also represents a lucrative avenue for market expansion and premium product development.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Smart Cities & Infrastructure | +0.9% | Global, particularly APAC & Europe | 2025-2033 |

| Development of Sustainable & Green Connectors | +0.7% | Europe, North America | 2025-2033 |

| Expansion into Niche High-Growth Applications (Medical, Aerospace) | +1.1% | North America, Europe, Japan | 2025-2033 |

| Increasing Demand for Custom & Application-Specific Connectors | +0.8% | Global | 2025-2033 |

Connector Market Challenges Impact Analysis

The connector market faces several inherent challenges that require strategic navigation for sustained success. One significant hurdle is the rapid pace of technological advancements across end-use industries, which necessitates constant innovation and adaptation in connector design and functionality. This rapid evolution can lead to a shorter product lifecycle for certain connectors, requiring significant and continuous investment in research and development to keep pace with changing industry standards and user expectations. Moreover, ensuring interoperability and standardization across diverse platforms and systems remains a persistent challenge, particularly as new communication protocols and power delivery methods emerge.

Another critical challenge is managing the complexities of a global supply chain, which is often susceptible to geopolitical instability, natural disasters, and pandemics, leading to potential disruptions in manufacturing and distribution. Maintaining a skilled workforce capable of designing, manufacturing, and testing advanced connector solutions is also becoming increasingly difficult amidst a global talent shortage in engineering and technical fields. These challenges collectively demand agile business models, robust risk management strategies, and a strong emphasis on collaboration within the industry to ensure resilient operations and continuous innovation.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Technological Obsolescence | -0.5% | Global | 2025-2033 |

| Lack of Standardization & Interoperability Issues | -0.4% | Global | 2025-2033 |

| Geopolitical Risks & Trade Barriers | -0.6% | Global | 2025-2030 |

| Skilled Labor Shortage | -0.3% | North America, Europe, Japan | 2025-2033 |

Connector Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global connector market, offering detailed insights into market dynamics, segmentation, and regional trends. It covers the market's historical performance, current landscape, and future projections, aiming to provide stakeholders with actionable intelligence for strategic decision-making. The scope includes a thorough examination of market drivers, restraints, opportunities, and challenges, complemented by an impact analysis of AI on the industry and a profile of key market players.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 82.5 Billion |

| Market Forecast in 2033 | USD 140.2 Billion |

| Growth Rate | 6.8% CAGR |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | TE Connectivity, Amphenol Corporation, Molex, Inc., Aptiv PLC, Yazaki Corporation, Sumitomo Electric Industries, Ltd., JAE Electronics, Inc., Hirose Electric Co., Ltd., Foxconn (Hon Hai Precision Industry Co., Ltd.), Kyocera Corporation (AVX Corporation), Rosenberger GmbH & Co. KG, HARTING Technology Group, FCI (Amphenol FCI), JST Mfg. Co., Ltd., ITT Inc., Fischer Connectors SA, Smith Interconnect, Cinch Connectivity Solutions, LEMO SA,binder GmbH |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The connector market is extensively segmented based on product type, application, and end-use industry, reflecting the diverse and specialized nature of its demand. The product type segment includes various connector designs, each optimized for specific electrical, mechanical, and environmental requirements, such as PCB connectors vital for internal device connections, and robust circular connectors used in industrial and harsh environments. Rectangular and fiber optic connectors address specific needs for data and power transmission, while specialized automotive connectors are designed to withstand the unique demands of vehicle systems.

Application-wise, the market is driven by sectors like automotive, consumer electronics, and telecommunications, which are major consumers of high-volume and high-performance connectors. Industrial applications, data centers, and the burgeoning medical and aerospace sectors also represent critical segments requiring highly reliable and specialized solutions. This multi-faceted segmentation allows for a granular understanding of market dynamics, enabling targeted product development and strategic market penetration based on specific industry needs and technological requirements.

- By Product Type: PCB Connectors (Board-to-Board, Wire-to-Board, FFC/FPC, etc.), Rectangular Connectors, Circular Connectors, Fiber Optic Connectors, RF Connectors, Heavy Duty Connectors, Automotive Connectors, IO Connectors, Power Connectors, Other Connectors.

- By Application: Automotive, Consumer Electronics, Telecommunications, Industrial, Data Communications, Aerospace & Defense, Medical, Energy & Power, Others.

- By End-Use Industry: Automotive & Transportation, IT & Telecom, Industrial Automation, Consumer Electronics, Healthcare, Aerospace & Defense, Energy & Utilities, Commercial, Others.

Regional Highlights

- Asia Pacific (APAC): Dominates the global connector market due to its robust electronics manufacturing base, rapid industrialization, and high adoption rates of consumer electronics, 5G technology, and electric vehicles, particularly in China, Japan, South Korea, and Taiwan.

- North America: A significant market driven by technological innovation, strong defense and aerospace sectors, increasing investments in data centers, and the growing automotive industry transitioning towards EVs and autonomous driving. The United States is a key contributor to regional growth.

- Europe: Characterized by advanced industrial automation (Industry 4.0), a strong automotive sector, and substantial investments in renewable energy. Germany, France, and the UK are leading countries, emphasizing high-reliability and specialized connector solutions for various applications.

- Latin America: An emerging market with growing industrialization and increasing demand for consumer electronics. Brazil and Mexico are key countries, benefiting from manufacturing growth and infrastructure development.

- Middle East and Africa (MEA): Shows promising growth fueled by investments in telecommunications infrastructure, smart city initiatives, and diversification of economies away from oil, particularly in countries like UAE and Saudi Arabia.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Connector Market.- TE Connectivity

- Amphenol Corporation

- Molex, Inc.

- Aptiv PLC

- Yazaki Corporation

- Sumitomo Electric Industries, Ltd.

- JAE Electronics, Inc.

- Hirose Electric Co., Ltd.

- Foxconn (Hon Hai Precision Industry Co., Ltd.)

- Kyocera Corporation (AVX Corporation)

- Rosenberger GmbH & Co. KG

- HARTING Technology Group

- FCI (Amphenol FCI)

- JST Mfg. Co., Ltd.

- ITT Inc.

- Fischer Connectors SA

- Smith Interconnect

- Cinch Connectivity Solutions

- LEMO SA

- binder GmbH

Frequently Asked Questions

What is the projected growth rate for the Connector Market?

The Connector Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033.

Which factors are primarily driving the growth of the Connector Market?

Key drivers include the rapid adoption of IoT devices, the expansion of electric vehicles (EVs) and advanced driver-assistance systems (ADAS), the growth of data centers and cloud computing, global 5G network deployments, and increasing industrial automation.

What is the estimated market size for connectors in 2025 and 2033?

The connector market is estimated at USD 82.5 billion in 2025 and is projected to reach USD 140.2 billion by the end of the forecast period in 2033.

How is AI impacting the Connector Market?

AI is influencing connector design optimization, improving manufacturing quality control and efficiency, increasing demand for high-performance connectors for AI hardware, and enabling smart connectors with self-monitoring capabilities.

Which region is expected to dominate the Connector Market?

Asia Pacific (APAC) is expected to remain the dominant region due to its robust manufacturing base, high consumer electronics adoption, and significant investments in 5G and EV infrastructure.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted