Cable and Connector Market

Cable and Connector Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701217 | Last Updated : July 29, 2025 |

Format : ![]()

![]()

![]()

![]()

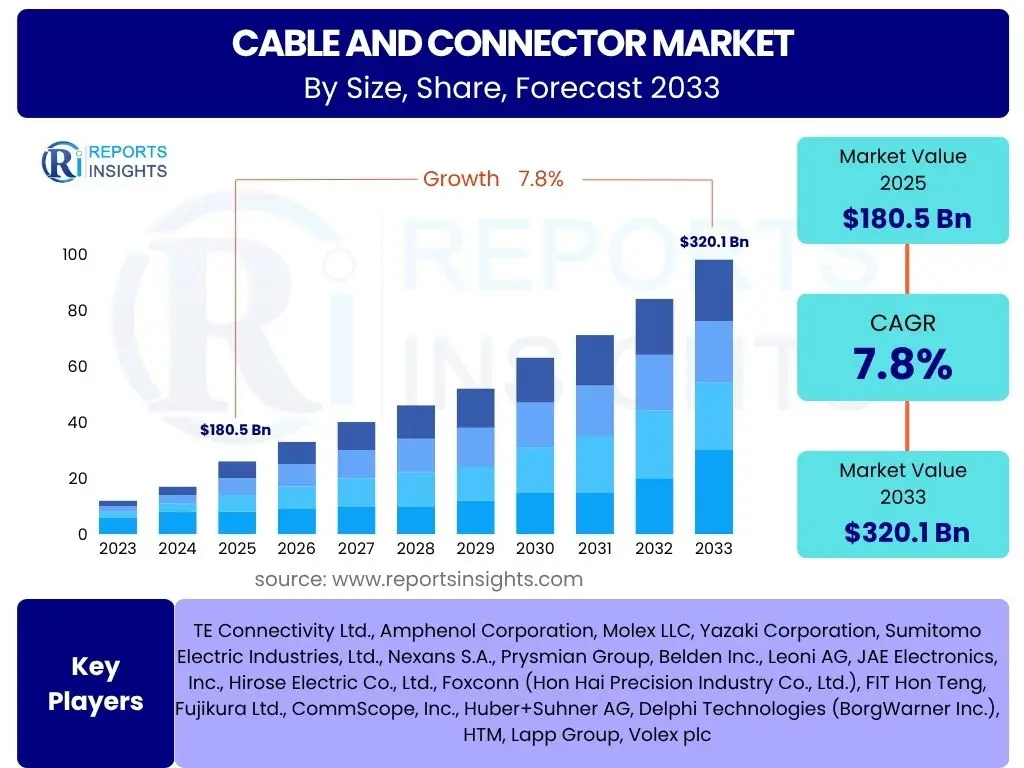

Cable and Connector Market Size

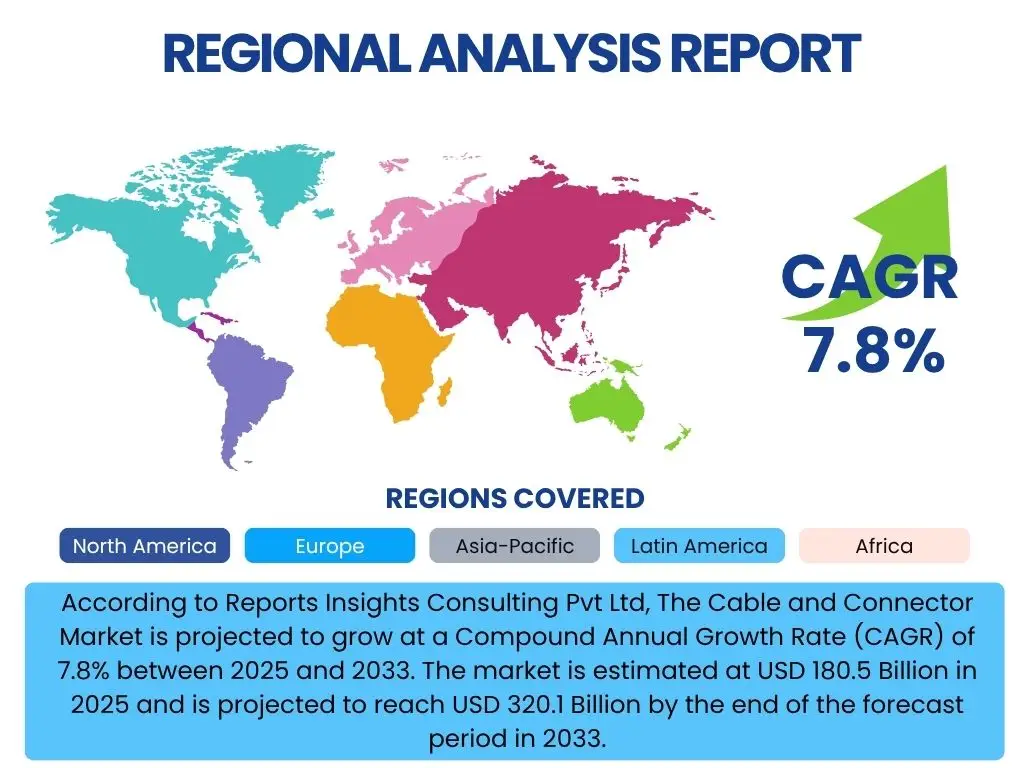

According to Reports Insights Consulting Pvt Ltd, The Cable and Connector Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033. The market is estimated at USD 180.5 Billion in 2025 and is projected to reach USD 320.1 Billion by the end of the forecast period in 2033.

Key Cable and Connector Market Trends & Insights

The Cable and Connector market is experiencing rapid evolution driven by the proliferation of advanced technologies and growing demand across diverse industries. Key trends revolve around the escalating need for high-speed data transmission, miniaturization of components, and enhanced reliability in harsh environments. Users frequently inquire about the impact of emerging standards like 5G and Wi-Fi 6, the increasing adoption of electric vehicles, and the expansion of data center infrastructure, all of which are significantly shaping product development and market dynamics. Furthermore, the focus on sustainable manufacturing practices and the integration of smart functionalities into connectors are gaining prominence, addressing both environmental concerns and the demand for more intelligent systems.

- Miniaturization and High-Density Connectivity

- Increased Demand for High-Speed Data Transmission (5G, Fiber Optics)

- Growing Adoption of USB-C and other Universal Connectors

- Emphasis on Robustness and Reliability for Industrial and Automotive Applications

- Integration of Smart Features (e.g., IoT-enabled connectors, sensors)

AI Impact Analysis on Cable and Connector

The integration of Artificial Intelligence (AI) is set to profoundly transform the Cable and Connector market by optimizing design, manufacturing, and application processes. User questions frequently focus on how AI can enhance efficiency in production lines, enable predictive maintenance for critical infrastructure, and facilitate the development of smarter, self-configuring connectivity solutions. AI algorithms are increasingly being employed for advanced material science research, identifying optimal compositions for cables that offer superior conductivity and durability, while also streamlining quality control through automated inspection systems. This shift enables manufacturers to produce more reliable, higher-performing products with reduced waste and increased precision.

- AI-driven Predictive Maintenance for Cable Infrastructure

- Optimized Design and Simulation of Connectors using AI Algorithms

- Automated Quality Inspection in Cable and Connector Manufacturing

- Enhanced Supply Chain Efficiency and Demand Forecasting via AI

- Development of Self-Configuring and Adaptive Smart Connectors

Key Takeaways Cable and Connector Market Size & Forecast

The projected growth of the Cable and Connector market underscores its critical role as the foundational infrastructure for global digital transformation and industrial advancement. Key takeaways from the market size and forecast analysis reveal significant investment opportunities in segments catering to high-growth areas such as 5G network deployment, electric vehicle infrastructure, and the continuous expansion of data centers and cloud computing. The sustained demand for reliable, high-performance connectivity solutions across consumer electronics, industrial automation, and healthcare further solidifies the market's robust trajectory. Strategic focus on innovation in materials, miniaturization, and intelligent connectivity will be crucial for companies aiming to capitalize on these trends and secure a competitive edge within this expanding landscape.

- Significant Growth Driven by Digital Transformation and Electrification

- High Investment Potential in 5G, EV, and Data Center Connectivity

- Continued Demand for High-Performance and Miniaturized Solutions

- Emerging Opportunities in Smart Infrastructure and IoT Applications

- Strategic Importance of Material Innovation and Manufacturing Efficiency

Cable and Connector Market Drivers Analysis

The Cable and Connector market is propelled by a confluence of technological advancements and increasing global connectivity demands. The pervasive rollout of 5G networks, requiring extensive fiber optic and high-speed copper cabling, alongside the accelerating adoption of Electric Vehicles (EVs) which demand specialized high-power and data connectors, are primary growth catalysts. Furthermore, the relentless expansion of data centers and cloud computing infrastructure necessitates robust, high-bandwidth connectivity solutions, while the burgeoning industrial automation sector drives demand for durable and intelligent industrial-grade cables and connectors. These macro trends create a fertile ground for market expansion, driving innovation in product design and material science to meet evolving performance requirements.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Rollout of 5G Technology | +1.5% | Global, particularly North America, Asia Pacific | Short-term to Mid-term (2025-2029) |

| Rapid Adoption of Electric Vehicles (EVs) | +1.2% | Europe, Asia Pacific (China), North America | Mid-term to Long-term (2026-2033) |

| Expansion of Data Centers and Cloud Computing | +1.0% | Global, particularly US, Ireland, Singapore | Short-term to Long-term (2025-2033) |

| Growth in Industrial Automation and IoT Devices | +0.8% | Germany, Japan, China, US | Mid-term (2027-2031) |

| Increasing Demand for Consumer Electronics | +0.7% | Asia Pacific, North America | Short-term (2025-2028) |

Cable and Connector Market Restraints Analysis

Despite robust growth prospects, the Cable and Connector market faces several significant restraints that could impede its trajectory. Volatility in raw material prices, particularly for copper, aluminum, and plastics, directly impacts manufacturing costs and profit margins across the industry. Furthermore, complex global supply chain disruptions, exacerbated by geopolitical tensions and logistics challenges, can lead to production delays and increased operational expenses. The ongoing challenge of achieving universal standardization across diverse applications and regions also poses a barrier, hindering interoperability and driving up development costs. Addressing these issues requires strategic procurement, diversified supply chains, and collaborative industry efforts towards global norms.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in Raw Material Prices | -0.9% | Global | Short-term to Mid-term (2025-2029) |

| Complex Global Supply Chain Disruptions | -0.7% | Global | Short-term (2025-2027) |

| Lack of Universal Standardization | -0.5% | Global, particularly across emerging technologies | Mid-term (2027-2030) |

| Intense Competition and Price Pressure | -0.4% | Global | Short-term to Long-term (2025-2033) |

| Environmental Regulations and Compliance Costs | -0.3% | Europe, North America | Mid-term to Long-term (2026-2033) |

Cable and Connector Market Opportunities Analysis

Significant opportunities are emerging within the Cable and Connector market, driven by evolving technological landscapes and increased demand for specialized solutions. The burgeoning need for high-speed, high-bandwidth connectivity in next-generation data centers, alongside the expansion of smart city infrastructure and the integration of IoT devices, presents substantial avenues for growth. Moreover, the increasing electrification of various sectors, including automotive and industrial machinery, creates demand for advanced power and data transmission solutions. Opportunities also lie in the development of custom and application-specific connectors for niche markets such as medical devices and aerospace, where stringent performance and reliability standards are paramount. Innovating in areas like modularity, easy installation, and enhanced durability will be key for market players to capitalize on these trends.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Advanced Data Center Connectivity | +1.3% | North America, Asia Pacific, Europe | Mid-term to Long-term (2026-2033) |

| Growth in Smart City and IoT Infrastructure | +1.0% | Asia Pacific, Europe | Mid-term (2027-2031) |

| Rising Demand for Hybrid and Custom Connectors | +0.9% | Global | Short-term to Mid-term (2025-2029) |

| Expansion into Renewable Energy Sector | +0.8% | Europe, North America, China | Mid-term to Long-term (2026-2033) |

| Integration of Circular Economy Principles | +0.6% | Europe, North America | Long-term (2028-2033) |

Cable and Connector Market Challenges Impact Analysis

The Cable and Connector market is confronted by several formidable challenges that necessitate innovative solutions and strategic adaptation. The persistent threat of counterfeit products, particularly in emerging markets, undermines legitimate businesses by diluting market share and potentially compromising system integrity due to substandard quality. Cybersecurity risks associated with increasingly smart and connected cables and connectors pose a growing concern, as vulnerabilities in these components could be exploited for data breaches or system disruptions. Rapid technological obsolescence, driven by fast-paced innovation in industries like consumer electronics and telecommunications, demands continuous investment in research and development to remain competitive. Furthermore, securing intellectual property rights in a globally interconnected market remains a complex task, requiring robust legal frameworks and enforcement to protect proprietary designs and technologies. Addressing these challenges is vital for sustained growth and maintaining market integrity.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Prevalence of Counterfeit Products | -0.8% | Asia Pacific, Africa, Latin America | Short-term to Long-term (2025-2033) |

| Cybersecurity Risks for Connected Systems | -0.7% | Global | Mid-term to Long-term (2026-2033) |

| Rapid Technological Obsolescence | -0.6% | Global, particularly in high-tech sectors | Short-term to Mid-term (2025-2029) |

| Skilled Labor Shortage in Manufacturing | -0.5% | North America, Europe, Japan | Mid-term to Long-term (2027-2033) |

| Intellectual Property Infringement | -0.4% | Global, particularly Asia Pacific | Short-term to Long-term (2025-2033) |

Cable and Connector Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global Cable and Connector market, offering a detailed understanding of its current landscape, historical performance, and future growth trajectory. The scope covers key market dynamics including drivers, restraints, opportunities, and challenges that are shaping the industry. It further dissects the market by various segments and sub-segments, providing granular insights into product types, applications, and regional contributions. The report also profiles leading market players, offering strategic intelligence on their competitive positioning and recent developments, serving as a vital resource for stakeholders seeking to make informed business decisions in this evolving sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 180.5 Billion |

| Market Forecast in 2033 | USD 320.1 Billion |

| Growth Rate | 7.8% CAGR |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | TE Connectivity Ltd., Amphenol Corporation, Molex LLC, Yazaki Corporation, Sumitomo Electric Industries, Ltd., Nexans S.A., Prysmian Group, Belden Inc., Leoni AG, JAE Electronics, Inc., Hirose Electric Co., Ltd., Foxconn (Hon Hai Precision Industry Co., Ltd.), FIT Hon Teng, Fujikura Ltd., CommScope, Inc., Huber+Suhner AG, Delphi Technologies (BorgWarner Inc.), HTM, Lapp Group, Volex plc |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Cable and Connector market is extensively segmented to reflect the diverse range of products and their applications across various industries. This detailed segmentation allows for a granular understanding of market dynamics, identifying specific growth pockets and evolving demand patterns. Key segments include categorization by cable type such as copper, fiber optic, and coaxial cables, each serving distinct performance requirements for data and power transmission. Connectors are segmented by product type, encompassing PCB, circular, rectangular, and specialized fiber optic and RF coaxial connectors, crucial for varied connection needs from circuit boards to high-frequency communication systems. Further segmentation by application and end-use industry highlights the market's penetration into critical sectors like automotive, telecommunication, industrial automation, healthcare, and consumer electronics, underscoring the universal reliance on robust connectivity solutions for modern infrastructure.

- By Type: Copper Cables, Fiber Optic Cables, Coaxial Cables, Power Cables, Others (e.g., Hybrid Cables)

- By Product Type (Connectors): PCB Connectors, Circular Connectors, Rectangular Connectors, Fiber Optic Connectors, RF Coaxial Connectors, I/O Connectors, Heavy Duty Connectors, Others

- By Application: Automotive, Telecommunication, Consumer Electronics, Industrial, Energy & Power, Healthcare, Aerospace & Defense, Building & Construction, Data Communication, Others

- By End-Use Industry: Information Technology & Telecommunications, Automotive & Transportation, Industrial Automation, Aerospace & Defense, Energy & Utilities, Medical & Healthcare, Consumer Electronics, Other Manufacturing

Regional Highlights

North America: The North American Cable and Connector market is characterized by significant demand from the telecommunications sector, driven by aggressive 5G infrastructure deployment and expanding data center footprints. The region's robust automotive industry, particularly with the surging investments in electric vehicles, also fuels the demand for high-performance and robust connectivity solutions. Furthermore, advancements in industrial automation and smart manufacturing across the United States and Canada contribute to the market's growth, with a strong emphasis on reliability and compliance with stringent industry standards. Innovation in advanced materials and high-speed data transmission technologies remains a key focus for regional market players.

Europe: Europe stands as a pivotal market for cables and connectors, largely influenced by stringent regulatory frameworks promoting sustainability and energy efficiency, particularly within the automotive and renewable energy sectors. The region's commitment to industrial automation, evidenced by initiatives like Industry 4.0, drives the adoption of advanced industrial connectors and heavy-duty cables. Countries such as Germany, with its strong manufacturing base, and the Nordic countries, focusing on green data centers, are at the forefront of adopting cutting-edge connectivity solutions. The ongoing upgrade of telecommunications infrastructure to support higher bandwidths and lower latency also contributes significantly to market expansion.

Asia Pacific (APAC): The Asia Pacific region dominates the global Cable and Connector market, propelled by rapid industrialization, urbanization, and massive investments in digital infrastructure, particularly in China, India, Japan, and South Korea. This region is the manufacturing hub for a vast array of consumer electronics, telecommunication equipment, and automotive components, generating immense demand for diverse cable and connector solutions. The widespread deployment of 5G networks, coupled with significant growth in data center construction and electric vehicle manufacturing, positions APAC as the fastest-growing market. Local players are increasingly focusing on scaling production and innovating to meet the evolving demands of a technologically advanced and cost-sensitive market.

Latin America: The Latin American Cable and Connector market is experiencing steady growth, primarily driven by investments in telecommunications infrastructure, including the expansion of broadband networks and nascent 5G rollouts in countries like Brazil and Mexico. The automotive sector, particularly in Mexico as a manufacturing hub, and the developing industrial automation segment contribute to the demand for specialized connectors. While still maturing compared to other regions, increasing foreign direct investment and government initiatives aimed at digital inclusion are expected to further stimulate market expansion. Infrastructure development projects in energy and transportation also create opportunities for cable and connector manufacturers.

Middle East and Africa (MEA): The MEA region's Cable and Connector market is characterized by significant infrastructure development projects, especially in the Gulf Cooperation Council (GCC) countries, focusing on smart cities, renewable energy, and telecommunication network upgrades. Investments in large-scale construction projects and diversification away from oil economies are creating new avenues for market growth. South Africa and Saudi Arabia are leading the adoption of advanced connectivity solutions for data centers and industrial applications. While the market faces challenges related to economic diversification and political stability in some areas, the long-term outlook remains positive due to ambitious national development visions and increasing digital transformation efforts.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Cable and Connector Market.

- TE Connectivity Ltd.

- Amphenol Corporation

- Molex LLC

- Yazaki Corporation

- Sumitomo Electric Industries, Ltd.

- Nexans S.A.

- Prysmian Group

- Belden Inc.

- Leoni AG

- JAE Electronics, Inc.

- Hirose Electric Co., Ltd.

- Foxconn (Hon Hai Precision Industry Co., Ltd.)

- FIT Hon Teng

- Fujikura Ltd.

- CommScope, Inc.

- Huber+Suhner AG

- Delphi Technologies (BorgWarner Inc.)

- HTM

- Lapp Group

- Volex plc

Frequently Asked Questions

What is the current market size of the Cable and Connector market?

The Cable and Connector market is estimated at USD 180.5 Billion in 2025, demonstrating substantial value within the global industrial landscape.

What is the projected growth rate for the Cable and Connector market?

The market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033, indicating robust expansion.

Which factors are primarily driving the growth of this market?

Key drivers include the global rollout of 5G technology, rapid adoption of Electric Vehicles (EVs), expansion of data centers, and increasing industrial automation.

What are the main challenges faced by the Cable and Connector market?

Challenges include volatility in raw material prices, global supply chain disruptions, the prevalence of counterfeit products, and rapid technological obsolescence.

Which regions are key contributors to the Cable and Connector market?

Asia Pacific (APAC) is a dominant contributor, with significant growth also observed in North America and Europe, driven by technology adoption and infrastructure development.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted