Concrete Pipe Market

Concrete Pipe Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702395 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

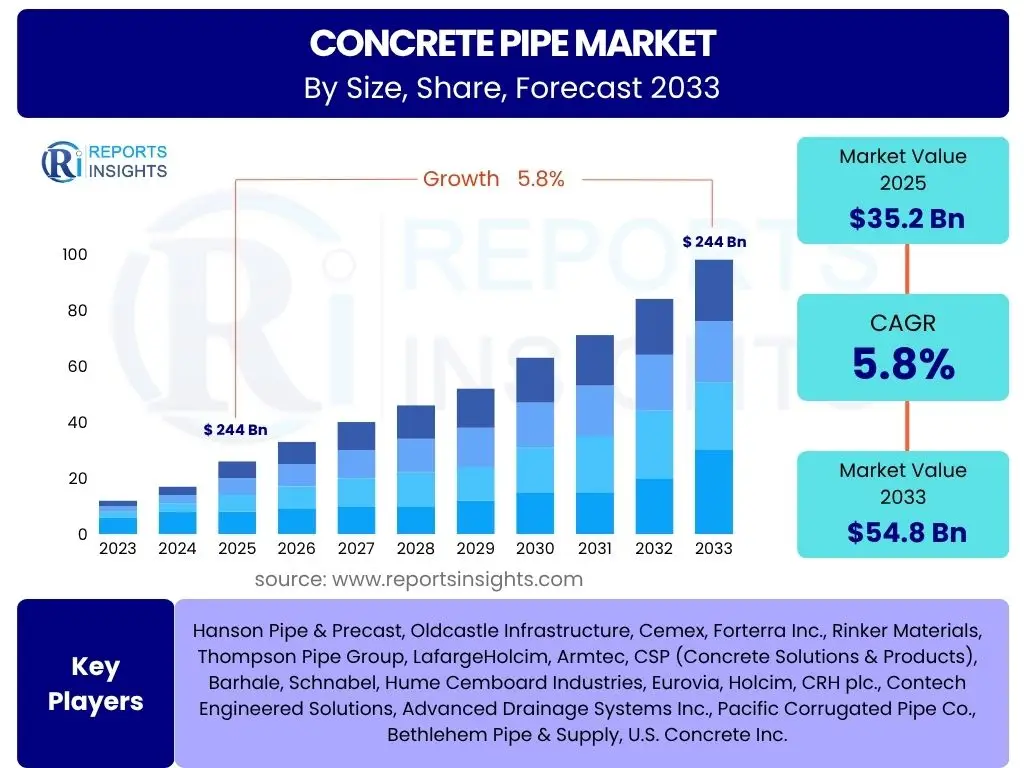

Concrete Pipe Market Size

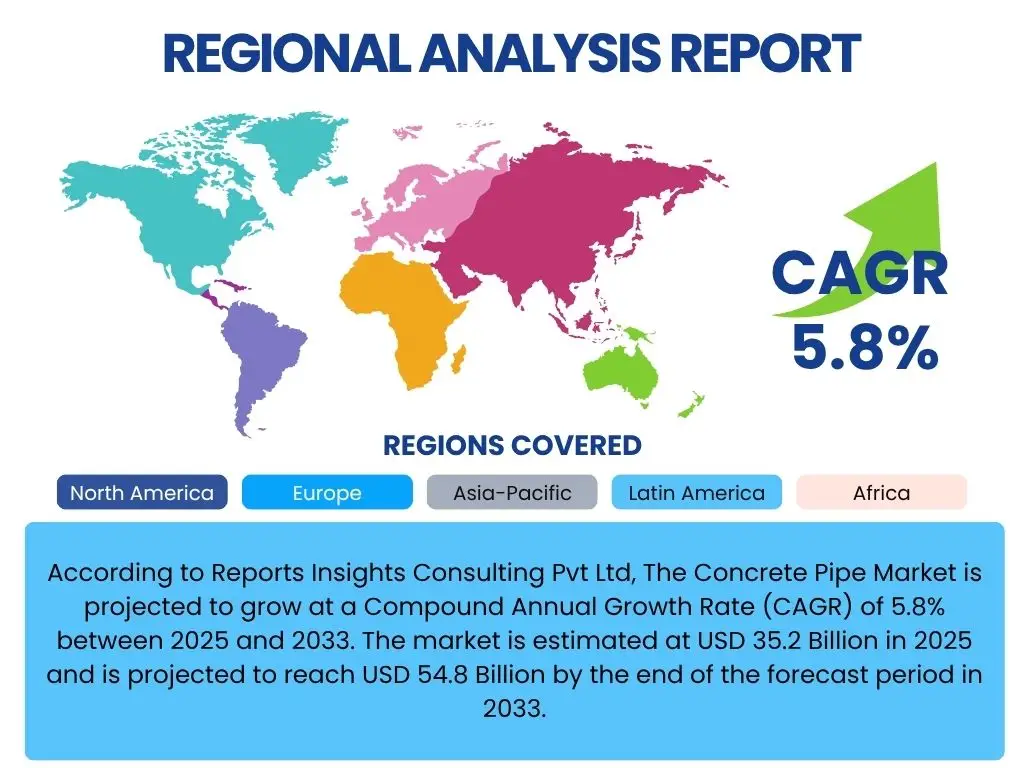

According to Reports Insights Consulting Pvt Ltd, The Concrete Pipe Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 35.2 Billion in 2025 and is projected to reach USD 54.8 Billion by the end of the forecast period in 2033.

Key Concrete Pipe Market Trends & Insights

The concrete pipe market is currently experiencing significant shifts driven by evolving infrastructure needs, technological advancements, and a heightened focus on sustainability. Users frequently inquire about the integration of new manufacturing processes, the push for more environmentally friendly materials, and the impact of large-scale urban development projects. These inquiries highlight a collective interest in understanding how the industry is adapting to modern demands while addressing long-standing challenges.

A notable trend is the increasing adoption of smart infrastructure solutions, where concrete pipes are designed to incorporate sensors for real-time monitoring of flow, pressure, and structural integrity. This allows for predictive maintenance and more efficient water management systems. Furthermore, there is a growing demand for large-diameter concrete pipes, particularly for major storm drain and wastewater collection projects in rapidly expanding urban centers. The emphasis on resilience against extreme weather events also influences design and material choices, driving innovation in pipe durability.

Additionally, the market is seeing a stronger push towards sustainable concrete mixes and manufacturing processes. This includes the use of supplementary cementitious materials (SCMs), recycled aggregates, and less energy-intensive curing methods to reduce the carbon footprint of concrete pipe production. The integration of prefabrication and modular construction techniques is also gaining traction, enhancing installation efficiency and reducing on-site labor requirements, thereby improving overall project timelines and cost-effectiveness.

- Increased demand for large-diameter concrete pipes for major infrastructure.

- Growing integration of smart sensing technologies for pipe monitoring.

- Focus on sustainable concrete mixes and eco-friendly manufacturing processes.

- Rising adoption of prefabrication and modular construction techniques.

- Enhanced emphasis on pipe resilience against severe weather conditions.

AI Impact Analysis on Concrete Pipe

User queries regarding the impact of Artificial intelligence (AI) on the concrete pipe industry often revolve around its potential to optimize manufacturing processes, enhance quality control, and streamline supply chain logistics. Stakeholders are keen to understand how AI can improve efficiency in a traditionally labor-intensive sector, reduce waste, and provide predictive insights for better operational management. The anticipation is that AI will introduce precision and intelligence, transforming various stages from design to deployment.

AI's influence is primarily observed in advanced manufacturing, where machine learning algorithms are employed for predictive maintenance of machinery, optimizing production schedules, and ensuring consistent product quality through real-time defect detection. This minimizes downtime, reduces operational costs, and enhances the reliability of the pipes. Furthermore, AI can analyze complex design parameters and material properties to suggest optimal concrete mixes, improving the strength and longevity of the pipes while potentially reducing material consumption.

Beyond manufacturing, AI is also making inroads into logistics and supply chain management within the concrete pipe sector. AI-powered systems can optimize delivery routes, manage inventory levels more effectively, and predict demand fluctuations, leading to reduced transportation costs and improved responsiveness to market needs. While the adoption rate is gradual compared to other industries, the potential for significant efficiency gains and cost reductions is driving increasing interest in AI-driven solutions within the concrete pipe market.

- Optimized manufacturing processes through AI-driven predictive maintenance.

- Enhanced quality control with AI for real-time defect detection and material optimization.

- Streamlined supply chain and logistics via AI for route optimization and inventory management.

- Improved concrete mix design and material efficiency using AI algorithms.

- Potential for reduced operational costs and increased production reliability.

Key Takeaways Concrete Pipe Market Size & Forecast

User inquiries about key takeaways from the concrete pipe market size and forecast consistently point to an interest in understanding the underlying growth drivers, the resilience of demand, and the long-term outlook for the industry. There is a clear focus on identifying stable investment opportunities and recognizing the critical role concrete pipes play in global infrastructure development, particularly in urban expansion and water management initiatives. Insights often highlight the market's stability despite economic fluctuations.

The market is poised for steady growth, primarily fueled by significant investments in municipal infrastructure projects, including upgrades to aging water and wastewater systems, and the development of new urban infrastructure. This sustained demand is a fundamental takeaway, indicating the essential nature of concrete pipes in modern society. Furthermore, the market's trajectory is influenced by population growth and increasing urbanization, which necessitate robust and reliable drainage and sewerage networks.

Another crucial insight is the increasing emphasis on sustainable and resilient infrastructure, which is driving innovation in concrete pipe manufacturing. Manufacturers are focusing on durable products that can withstand environmental stressors and contribute to long-term infrastructure stability. The forecast suggests that while challenges exist, the fundamental need for water management and civil infrastructure will continue to provide a solid foundation for the concrete pipe market's expansion.

- Consistent growth projected, driven by global infrastructure development.

- Robust demand from municipal projects, especially water and wastewater systems.

- Market resilience linked to essential infrastructure needs.

- Growing focus on sustainable and durable concrete pipe solutions.

- Long-term stability influenced by urbanization and population growth.

Concrete Pipe Market Drivers Analysis

The concrete pipe market is propelled by several robust drivers, primarily rooted in the global imperative for infrastructure development and maintenance. The increasing pace of urbanization worldwide, particularly in developing economies, creates an immense demand for new and upgraded water management systems, including storm drains and sanitary sewers. This demographic shift necessitates extensive civil engineering projects, with concrete pipes forming a fundamental component of these essential networks.

Furthermore, significant governmental investments in infrastructure upgrades and rehabilitation projects, especially in developed nations, are consistently driving market growth. Many regions possess aging water and wastewater infrastructure that requires urgent replacement to prevent system failures and ensure public health. Concrete pipes, known for their durability and longevity, are frequently the material of choice for such critical replacements and expansions.

Beyond urban development and infrastructure renewal, the agricultural sector's demand for efficient irrigation systems and the industrial sector's need for robust culverts and utility conduits also contribute significantly to market expansion. Population growth further compounds these needs, as more people require access to reliable sanitation and water services, translating directly into increased demand for concrete pipe solutions.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Urbanization and Population Growth | +1.5% | Asia Pacific, Africa, Latin America | Medium-Long Term (2025-2033) |

| Increasing Government Spending on Infrastructure | +1.2% | North America, Europe, China, India | Medium Term (2025-2030) |

| Aging Water and Wastewater Infrastructure Replacement | +1.0% | North America, Western Europe | Long Term (2025-2033) |

| Growth in Agricultural and Industrial Sectors | +0.8% | Global, particularly Emerging Economies | Medium Term (2025-2030) |

| Resilience and Durability of Concrete Pipes | +0.7% | Global | Long Term (2025-2033) |

Concrete Pipe Market Restraints Analysis

Despite its inherent advantages and critical role in infrastructure, the concrete pipe market faces several significant restraints that can impede its growth trajectory. One primary concern is the volatility in raw material prices, particularly cement, aggregates, and steel reinforcement. Fluctuations in the cost of these essential components can directly impact production expenses, leading to higher manufacturing costs and potentially reducing profit margins for pipe manufacturers, which can then be passed on to consumers or lead to reduced investment in new production capabilities.

Another considerable restraint is the intense competition from alternative pipe materials, such as plastic (PVC, HDPE), ductile iron, and fiberglass-reinforced pipes. These materials often offer advantages like lighter weight, easier installation, and perceived lower initial costs in certain applications. While concrete pipes excel in strength and durability for specific uses, the growing preference for lighter alternatives in less demanding applications or where specific chemical resistance is required poses a continuous challenge to market share.

Furthermore, stringent environmental regulations regarding cement production's carbon footprint and the energy intensity of concrete manufacturing can act as a restraint. While the industry is actively pursuing more sustainable practices, complying with increasingly strict emissions standards and waste management protocols can add to operational complexities and costs. Lastly, labor shortages, particularly for skilled workers in manufacturing and installation, present a persistent challenge, impacting project timelines and overall market efficiency.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in Raw Material Prices | -0.8% | Global | Short-Medium Term (2025-2028) |

| Competition from Alternative Pipe Materials | -0.7% | Global, particularly Developed Markets | Medium-Long Term (2025-2033) |

| Environmental Regulations and Carbon Footprint Concerns | -0.5% | Europe, North America | Medium-Long Term (2025-2033) |

| Skilled Labor Shortages and Rising Labor Costs | -0.4% | North America, Europe, Australia | Medium Term (2025-2030) |

Concrete Pipe Market Opportunities Analysis

The concrete pipe market is presented with several promising opportunities that can foster significant growth and innovation. The increasing global focus on developing smart cities offers a substantial avenue for market expansion. Smart city initiatives prioritize sustainable, efficient, and resilient infrastructure, where concrete pipes, particularly those integrated with monitoring technologies, can play a crucial role in advanced water management, storm water runoff control, and utility conduit systems.

Another key opportunity lies in the expanding investment in wastewater treatment infrastructure. As populations grow and environmental regulations become stricter, the need for robust and reliable wastewater collection and treatment systems intensifies. Concrete pipes, renowned for their structural integrity and resistance to corrosive environments, are ideally suited for these demanding applications, promising sustained demand in this sector. Furthermore, the development and adoption of trenchless technology for pipe installation present a significant opportunity to reduce disruption and costs, making concrete pipes more competitive in urban renewal projects where traditional open-cut methods are impractical.

Moreover, the continuous innovation in concrete mixes, including the development of self-healing concrete, ultra-high-performance concrete, and greener concrete formulations utilizing recycled materials, presents an opportunity for manufacturers to offer enhanced products. These innovations can lead to more durable, sustainable, and cost-effective pipe solutions, meeting evolving environmental standards and customer preferences. The increasing number of public-private partnerships (PPPs) in infrastructure development also provides opportunities for larger-scale projects and more stable long-term contracts for concrete pipe suppliers.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Smart City Initiatives and Infrastructure | +1.0% | Global, particularly Asia Pacific, Europe | Long Term (2025-2033) |

| Increased Investment in Wastewater Treatment Infrastructure | +0.9% | Global | Medium-Long Term (2025-2033) |

| Advancements in Concrete Mixes and Sustainable Production | +0.8% | Global | Medium-Long Term (2025-2033) |

| Adoption of Trenchless Technology for Installation | +0.7% | Developed Markets (North America, Europe) | Medium Term (2025-2030) |

| Expansion of Public-Private Partnerships (PPPs) | +0.6% | Global | Medium-Long Term (2025-2033) |

Concrete Pipe Market Challenges Impact Analysis

The concrete pipe market, while robust, must navigate several critical challenges that can impact its operational efficiency and growth prospects. One significant challenge is the complexity of managing an extensive and often fragmented supply chain. The sourcing of raw materials, particularly aggregates, can be geographically constrained, leading to logistical complexities and increased transportation costs. Disruptions in the supply chain, such as those caused by geopolitical events or natural disasters, can severely impede production and delivery schedules.

Another persistent challenge is the variability in regulatory compliance across different regions and countries. Concrete pipe manufacturers must adhere to a myriad of local and national standards concerning material specifications, manufacturing processes, and environmental impact. Navigating these diverse and often evolving regulations requires substantial resources for compliance testing, certification, and process adjustments, adding to the operational burden and potentially slowing market entry into new regions.

Furthermore, the high initial investment required for establishing or upgrading concrete pipe manufacturing facilities can be a significant barrier to entry for new players and a challenge for existing ones seeking to expand. The capital-intensive nature of machinery, molds, and specialized curing equipment necessitates substantial financial commitment. Lastly, competition from lower-cost alternatives, especially in less critical applications, continues to pressure pricing and profitability, requiring concrete pipe manufacturers to continuously emphasize the long-term value and durability of their products to maintain market share.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complex Supply Chain Management and Raw Material Sourcing | -0.6% | Global | Short-Medium Term (2025-2028) |

| Variability and Stringency of Regulatory Compliance | -0.5% | Europe, North America | Medium-Long Term (2025-2033) |

| High Initial Capital Investment for Manufacturing Facilities | -0.4% | Global | Long Term (2025-2033) |

| Intense Price Competition from Alternative Materials | -0.3% | Global | Medium Term (2025-2030) |

Concrete Pipe Market - Updated Report Scope

This report offers a comprehensive analysis of the global Concrete Pipe Market, providing a detailed understanding of its current landscape and future growth trajectory. It covers critical market aspects from 2019 to 2033, encompassing historical performance, current market size, and a robust forecast period. The study delves into key market trends, segmentations by type, application, and end-use, and highlights regional dynamics. It also profiles leading companies, offering insights into their market strategies and competitive positioning.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 35.2 Billion |

| Market Forecast in 2033 | USD 54.8 Billion |

| Growth Rate | 5.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Hanson Pipe & Precast, Oldcastle Infrastructure, Cemex, Forterra Inc., Rinker Materials, Thompson Pipe Group, LafargeHolcim, Armtec, CSP (Concrete Solutions & Products), Barhale, Schnabel, Hume Cemboard Industries, Eurovia, Holcim, CRH plc., Contech Engineered Solutions, Advanced Drainage Systems Inc., Pacific Corrugated Pipe Co., Bethlehem Pipe & Supply, U.S. Concrete Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The concrete pipe market is comprehensively segmented to provide a granular understanding of its diverse components and drivers. These segmentations allow for a detailed analysis of market dynamics based on pipe characteristics, intended use, and ultimate end-users, providing valuable insights for manufacturers, investors, and policymakers. Each segment exhibits unique growth patterns and demand influences, reflecting the varied applications of concrete pipes across the globe.

The segmentation by type distinguishes between Reinforced Concrete Pipe (RCP), Non-Reinforced Concrete Pipe, and Prestressed Concrete Pipe. RCPs are dominant due to their superior strength and durability, making them suitable for high-stress applications like large-diameter storm drains and culverts. Non-reinforced pipes are typically used in less demanding scenarios, while prestressed pipes offer enhanced load-bearing capacity and crack resistance, ideal for very large infrastructure projects.

Application-based segmentation includes storm drains, sanitary sewers, irrigation systems, culverts, and other specialized uses like utility conduits. Storm drains and sanitary sewers represent the largest application segments, driven by extensive urban development and the constant need for efficient wastewater and stormwater management. The end-use segmentation covers municipal, industrial, agricultural, commercial, and residential sectors, with municipal applications being the primary consumer, reflecting public infrastructure investments.

- By Type:

- Reinforced Concrete Pipe (RCP): Widely used for strength and durability in major infrastructure.

- Non-Reinforced Concrete Pipe: Suitable for less demanding applications.

- Prestressed Concrete Pipe: Offers high load-bearing capacity for large-scale projects.

- By Application:

- Storm Drains: Critical for urban flood control and stormwater management.

- Sanitary Sewers: Essential for wastewater collection and transport.

- Irrigation: Used in agricultural contexts for water distribution.

- Culverts: Enables water flow under roads, railways, and embankments.

- Others: Includes utility conduits, tunnels, and specialized industrial piping.

- By End-Use:

- Municipal: Dominant segment driven by public infrastructure projects.

- Industrial: Used for various industrial processes and waste management.

- Agricultural: Primarily for drainage and irrigation systems.

- Commercial: Applied in commercial development drainage and utility networks.

- Residential: Used in residential drainage and sewage systems.

Regional Highlights

The concrete pipe market exhibits diverse dynamics across different geographic regions, influenced by varying levels of urbanization, infrastructure development, and regulatory environments. Each region presents unique growth opportunities and challenges that shape market demand and supply. Understanding these regional nuances is crucial for strategic market positioning and investment decisions, as infrastructure priorities differ significantly from one part of the world to another.

North America is characterized by significant investments in the rehabilitation and replacement of aging infrastructure. Many municipal water and wastewater systems are decades old, creating a consistent demand for concrete pipes. Environmental regulations and the need for resilient infrastructure capable of withstanding extreme weather events further drive market growth in this region. Europe also focuses on upgrading existing infrastructure and is increasingly emphasizing sustainable and eco-friendly manufacturing practices for concrete pipes.

Asia Pacific is projected to be the fastest-growing region, fueled by rapid urbanization, substantial population growth, and massive infrastructure development projects, particularly in countries like China, India, and Southeast Asian nations. The demand for new residential, commercial, and industrial infrastructure, along with expanding water and sanitation networks, is a major catalyst. Latin America and the Middle East & Africa (MEA) are also expected to witness considerable growth due to ongoing urbanization, industrialization, and increased focus on water management and resource development projects.

- North America: Driven by extensive aging infrastructure replacement and rehabilitation projects; strong emphasis on resilience and durability.

- Europe: Focus on modernizing existing infrastructure and strict environmental regulations promoting sustainable concrete solutions.

- Asia Pacific (APAC): Experiencing the highest growth due to rapid urbanization, population expansion, and large-scale new infrastructure development, particularly in emerging economies.

- Latin America: Growing demand from developing urban centers and increasing investments in water and sanitation infrastructure.

- Middle East and Africa (MEA): Significant investments in new city development, industrialization, and critical water resource management projects.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Concrete Pipe Market.

- Hanson Pipe & Precast

- Oldcastle Infrastructure

- Cemex

- Forterra Inc.

- Rinker Materials

- Thompson Pipe Group

- LafargeHolcim

- Armtec

- CSP (Concrete Solutions & Products)

- Barhale

- Schnabel

- Hume Cemboard Industries

- Eurovia

- Holcim

- CRH plc.

- Contech Engineered Solutions

- Advanced Drainage Systems Inc.

- Pacific Corrugated Pipe Co.

- Bethlehem Pipe & Supply

- U.S. Concrete Inc.

Frequently Asked Questions

What is the primary use of concrete pipes?

Concrete pipes are primarily used in critical civil infrastructure for conveying water, wastewater, and stormwater. Their strength and durability make them ideal for storm drains, sanitary sewers, culverts under roads, and large-scale irrigation systems, ensuring efficient fluid management and ground stability.

What factors are driving the growth of the concrete pipe market?

The concrete pipe market's growth is driven by increasing global urbanization, substantial government investments in infrastructure development and rehabilitation, and the necessity to replace aging water and wastewater systems. The inherent durability and long lifespan of concrete pipes also contribute to their sustained demand.

What are the different types of concrete pipes available?

Concrete pipes are generally categorized into Reinforced Concrete Pipe (RCP), which contains steel reinforcement for enhanced strength; Non-Reinforced Concrete Pipe, used for less demanding applications; and Prestressed Concrete Pipe, offering superior load-bearing capacity for very large diameters and high-pressure applications.

What challenges does the concrete pipe market face?

Key challenges include volatility in raw material prices, intense competition from alternative pipe materials like plastic and ductile iron, stringent environmental regulations regarding manufacturing processes, and shortages of skilled labor in both production and installation, which can impact project timelines and costs.

How is sustainability impacting the concrete pipe industry?

Sustainability is increasingly influencing the concrete pipe industry through a focus on greener concrete mixes, using recycled aggregates and supplementary cementitious materials to reduce carbon footprint. Manufacturers are also exploring energy-efficient production methods and promoting the long-term environmental benefits of concrete's durability and minimal maintenance needs.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted