Composite Material in the Wind Energy Market

Composite Material in the Wind Energy Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_710356 | Last Updated : January 05, 2026 |

Format : ![]()

![]()

![]()

![]()

Composite Material in the Wind Energy Market Size

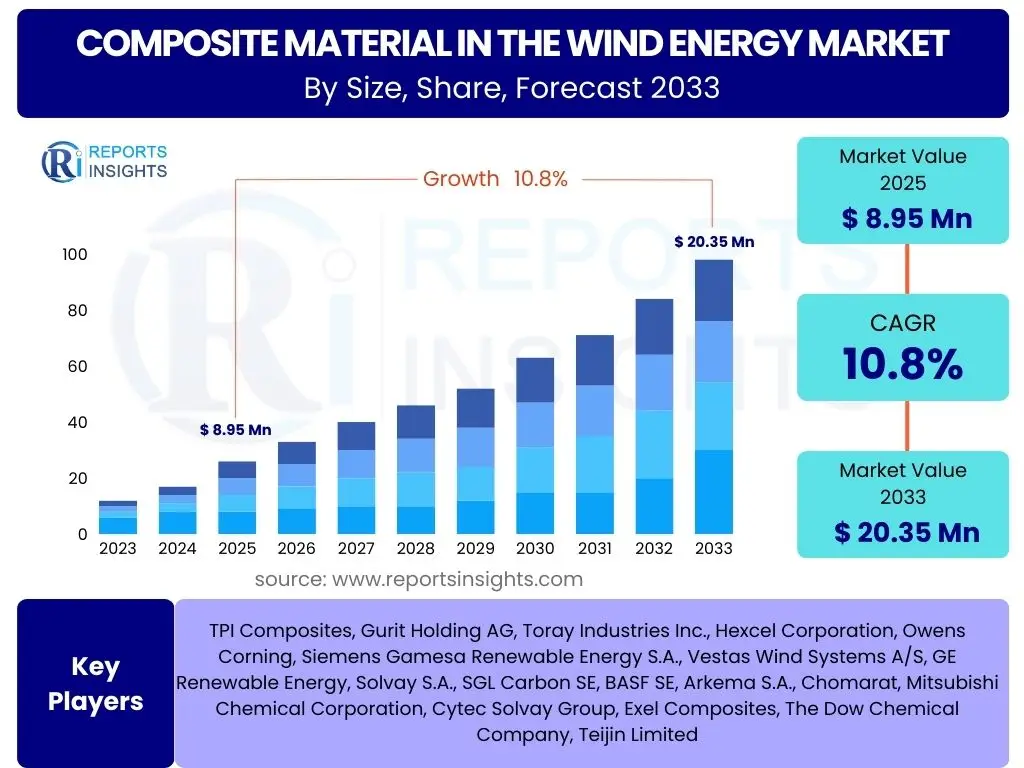

According to Reports Insights Consulting Pvt Ltd, The Composite Material in the Wind Energy Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 10.8% between 2025 and 2033. The market is estimated at USD 8.95 Billion in 2025 and is projected to reach USD 20.35 Billion by the end of the forecast period in 2033.

Key Composite Material in the Wind Energy Market Trends & Insights

The wind energy sector is undergoing significant transformation, driving demand for advanced composite materials. A predominant trend involves the increasing size of wind turbine blades, necessitating materials that offer superior strength-to-weight ratios and enhanced durability. This shift is crucial for optimizing energy capture and improving the overall efficiency of wind farms, particularly in offshore environments where larger turbines are increasingly deployed. Furthermore, there is a strong emphasis on developing more sustainable composite solutions, including recyclable materials and bio-composites, to address environmental concerns associated with the end-of-life management of turbine components. These innovations are critical for reducing the carbon footprint of wind energy production and aligning with global sustainability goals.

Another significant trend is the continuous innovation in manufacturing processes for composite materials, focusing on automation and digitalization. Advanced manufacturing techniques, such as automated fiber placement (AFP) and robotic processing, are being adopted to enhance production efficiency, reduce labor costs, and improve the consistency and quality of composite components. These methods allow for the creation of more complex geometries and larger structures with greater precision, which is essential for the next generation of wind turbines. The integration of smart sensors into composite structures for real-time monitoring and predictive maintenance is also gaining traction, offering the potential to extend operational lifespans and minimize downtime. This holistic approach to material development and manufacturing underpins the industry's drive towards greater performance and cost-effectiveness.

- Increasing adoption of longer, lighter, and more aerodynamic turbine blades to enhance energy capture.

- Growing demand for advanced composite materials such as carbon fiber to improve structural integrity and reduce weight.

- Rising investment in offshore wind energy projects driving the need for robust and durable composites capable of withstanding harsh marine environments.

- Development of sustainable and recyclable composite materials to address environmental concerns and end-of-life challenges.

- Integration of advanced manufacturing techniques, including automation and digitalization, for enhanced production efficiency and quality control.

AI Impact Analysis on Composite Material in the Wind Energy

Artificial intelligence is poised to revolutionize various aspects of the composite material lifecycle within the wind energy sector. Users are keenly interested in how AI can optimize the design and manufacturing of wind turbine components, particularly blades. AI-driven simulation tools can rapidly evaluate countless design iterations, allowing engineers to identify optimal material compositions and structural configurations that maximize aerodynamic performance and minimize material usage. This capability not only accelerates the R&D process but also leads to the creation of more efficient and cost-effective turbine designs. Furthermore, AI's role in predictive analytics for material behavior and defect detection during manufacturing is a significant area of focus, promising to enhance quality control and reduce waste.

The operational phase of wind turbines also stands to benefit immensely from AI integration. Users anticipate AI will play a critical role in predictive maintenance, analyzing sensor data from composite components to forecast potential failures and recommend proactive interventions. This shift from reactive to predictive maintenance can significantly extend the lifespan of turbine blades, reduce unscheduled downtime, and lower operational costs. Moreover, AI can optimize the entire supply chain for composite materials, from raw material sourcing to delivery, by predicting demand fluctuations and identifying potential bottlenecks. The overarching expectation is that AI will enhance efficiency, improve reliability, and drive innovation across the entire value chain of composite materials in wind energy, making wind power even more competitive.

- Optimized design of composite wind turbine blades using AI-driven simulation and generative design tools.

- Enhanced material selection and composition through AI analysis of performance data and environmental factors.

- Improved manufacturing processes for composites via AI-powered quality control, defect detection, and robotic automation.

- Predictive maintenance for composite components, reducing downtime and extending the operational life of wind turbines.

- Supply chain optimization for composite raw materials and finished components, ensuring efficiency and reducing lead times.

Key Takeaways Composite Material in the Wind Energy Market Size & Forecast

The Composite Material in the Wind Energy Market is experiencing robust growth, driven by the global energy transition and the increasing adoption of wind power. A key takeaway is the substantial expansion anticipated, with the market projected to more than double in value by 2033. This growth is fundamentally underpinned by the continuous innovation in composite material technology, which enables the production of larger, more efficient, and structurally resilient wind turbines. The forecast indicates a sustained upward trajectory, reflecting the critical role of composites in enhancing the performance and reducing the Levelized Cost of Energy (LCOE) of wind power projects worldwide, making them increasingly competitive with traditional energy sources. The market's resilience is further supported by proactive governmental policies and significant investments in renewable energy infrastructure.

Another crucial insight is the dynamic interplay between material science advancements and the evolving demands of the wind energy sector. The industry's push towards deeper offshore installations and higher capacity turbines places unprecedented demands on material properties, such as fatigue resistance, stiffness, and durability in harsh environments. Consequently, the market is witnessing an accelerated development of high-performance composites, including hybrids of glass and carbon fibers, as well as the exploration of smart materials. The emphasis on sustainability and circular economy principles is also a defining feature, influencing material choices and manufacturing processes to ensure the long-term viability of wind energy as a clean power source. These factors collectively highlight a market characterized by innovation, strategic investment, and a strong commitment to addressing global energy challenges.

- The market for composite materials in wind energy is poised for significant expansion, demonstrating a high Compound Annual Growth Rate (CAGR).

- Technological advancements in composite materials are critical for developing next-generation, higher-capacity wind turbines.

- Increased investment in offshore wind energy projects is a major catalyst for market growth and material innovation.

- Sustainability and recyclability of composite materials are becoming central to industry development and future material selection.

- Global government initiatives and renewable energy targets continue to be strong drivers for market progression.

Composite Material in the Wind Energy Market Drivers Analysis

The growth of the Composite Material in the Wind Energy Market is significantly propelled by several key factors. The global imperative to transition towards renewable energy sources to combat climate change and reduce reliance on fossil fuels stands as a primary driver. Governments worldwide are implementing ambitious renewable energy targets and offering various incentives, subsidies, and favorable regulatory frameworks for wind power projects. This supportive policy environment directly stimulates investment in new wind farms and the expansion of existing ones, consequently escalating the demand for high-performance composite materials essential for turbine components. The increasing competitiveness of wind energy, driven by falling Levelized Cost of Energy (LCOE), also encourages broader adoption.

Technological advancements in composite materials themselves, coupled with an increasing demand for larger and more efficient wind turbines, represent another powerful driver. Modern wind turbines require lighter, stronger, and more durable components to maximize energy capture and withstand extreme environmental conditions, especially in offshore applications. Composites, with their superior strength-to-weight ratio, fatigue resistance, and design flexibility, are indispensable for manufacturing increasingly longer rotor blades, robust nacelle covers, and structural elements. Innovations in manufacturing processes, such as vacuum infusion and automated fiber placement, further enhance the efficiency and cost-effectiveness of producing these large-scale composite structures, making them the material of choice for the wind energy industry.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Renewable Energy Targets and Policies | +3.5% | Europe, North America, Asia Pacific | Long-term (2025-2033) |

| Advancements in Wind Turbine Technology (Larger Blades) | +2.8% | Global | Mid to Long-term |

| Decreasing Levelized Cost of Energy (LCOE) for Wind Power | +2.1% | Global | Mid to Long-term |

| Growth in Offshore Wind Energy Installations | +1.5% | Europe, Asia Pacific, North America | Long-term |

| Material Innovation (e.g., higher performance fibers) | +0.9% | Global | Mid-term |

Composite Material in the Wind Energy Market Restraints Analysis

Despite the robust growth, the Composite Material in the Wind Energy Market faces several significant restraints that could impede its full potential. One primary challenge is the relatively high initial cost of advanced composite materials, particularly carbon fiber, compared to traditional materials. While composites offer long-term benefits in terms of performance and efficiency, the upfront investment in raw materials and specialized manufacturing processes can be substantial, potentially increasing the overall project cost for wind farm developers. This cost factor can be a barrier, especially in price-sensitive markets or for projects with limited capital. The economic viability of projects often depends on balancing initial costs against long-term operational savings, and high material costs can tip this balance.

Another critical restraint is the complexity and environmental impact associated with the recycling and end-of-life management of composite components. Current recycling methods for thermoset composites, predominantly used in wind turbine blades, are often energy-intensive, costly, and do not always yield high-value recovered materials. This creates a significant waste management challenge as thousands of turbine blades reach the end of their operational life, leading to landfill issues. The lack of a robust, economically viable, and scalable recycling infrastructure for composite materials poses a sustainability dilemma for the wind energy industry, which prides itself on being environmentally friendly. Furthermore, potential disruptions in the global supply chain for raw materials like glass and carbon fibers, and various resins, can also lead to price volatility and production delays, impacting market stability.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Cost of Advanced Composites | -1.8% | Global | Mid to Long-term |

| Challenges in Recycling and End-of-Life Management | -2.2% | Europe, North America | Long-term |

| Supply Chain Volatility of Raw Materials | -1.3% | Global | Short to Mid-term |

| Complex Manufacturing Processes for Large Components | -0.9% | Global | Mid-term |

| Competition from Alternative Materials (e.g., metals) | -0.7% | Specific Applications | Mid-term |

Composite Material in the Wind Energy Market Opportunities Analysis

Significant opportunities exist for expansion within the Composite Material in the Wind Energy Market, particularly driven by emerging technological developments and geographical expansion. The burgeoning offshore wind energy sector presents a substantial opportunity, demanding larger, more robust, and durable composite components capable of withstanding harsh marine environments. As countries worldwide invest heavily in offshore wind farms, the need for specialized composites that offer superior fatigue resistance, corrosion resistance, and structural integrity will intensify. This creates avenues for innovation in material science, focusing on advanced resin systems, tougher fibers, and smart materials that can self-monitor their structural health. The transition towards floating offshore wind turbines further amplifies this demand, requiring lighter yet incredibly strong materials for innovative substructure designs.

Furthermore, the focus on sustainability within the wind energy industry opens up significant opportunities for recyclable and circular economy solutions in composite materials. The development of thermoplastic composites, which can be melted and reshaped, offers a promising alternative to traditional thermosets, addressing the end-of-life challenges of turbine blades. Investments in chemical recycling processes and the creation of infrastructure for material recovery and reuse represent substantial growth areas. Beyond material innovation, the digitalization of manufacturing processes and the integration of artificial intelligence for design optimization, predictive maintenance, and supply chain management can unlock new efficiencies and cost reductions. Emerging markets in Asia Pacific, Latin America, and Africa, with their vast untapped wind resources and increasing energy demands, also present lucrative opportunities for market penetration and technological transfer.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion of Offshore Wind Energy Projects | +3.2% | Europe, Asia Pacific, North America | Long-term |

| Development of Recyclable and Sustainable Composites | +2.5% | Global | Mid to Long-term |

| Growth in Emerging Markets (e.g., Asia Pacific) | +1.9% | Asia Pacific, Latin America | Long-term |

| Technological Advancements in Thermoplastic Composites | +1.3% | Global | Mid to Long-term |

| Integration of AI and Digitalization in Manufacturing | +0.8% | Global | Mid-term |

Composite Material in the Wind Energy Market Challenges Impact Analysis

The Composite Material in the Wind Energy Market is not without its challenges, which can impact growth and stability. A significant hurdle is the inherent variability in raw material quality and availability, which can affect the consistency and performance of large composite structures like wind turbine blades. Ensuring uniform material properties across vast production volumes, especially with globalized supply chains, requires stringent quality control and robust material characterization techniques. Fluctuations in the prices of key raw materials, such as petroleum-derived resins and energy-intensive fibers, can also lead to unpredictable manufacturing costs, thereby impacting profitability and making long-term project planning more difficult for manufacturers and developers.

Another critical challenge revolves around processing efficiency and scalability for increasingly larger composite components. Manufacturing processes for multi-megawatt turbine blades, which can exceed 100 meters in length, demand extensive infrastructure, specialized equipment, and highly skilled labor. Scaling up production while maintaining high quality, reducing cycle times, and minimizing waste presents a complex engineering and logistical problem. Furthermore, navigating diverse and stringent regulatory landscapes, particularly concerning environmental standards and recycling mandates across different regions, adds another layer of complexity. The long lifespan of wind turbines means that end-of-life management, including decommissioning and disposal, remains a long-term environmental and economic challenge that the industry is actively seeking to address through innovation and policy development.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Raw Material Price Volatility and Supply Chain Risks | -1.5% | Global | Short to Mid-term |

| Technical Complexity of Manufacturing Large Blades | -1.2% | Global | Mid-term |

| Need for Skilled Workforce and Specialized Training | -1.0% | Global | Long-term |

| Evolving Regulatory Landscape and Environmental Standards | -0.8% | Europe, North America | Long-term |

| Competition from Non-Composite Materials in Specific Applications | -0.6% | Specific Applications | Mid-term |

Composite Material in the Wind Energy Market - Updated Report Scope

This report provides a comprehensive analysis of the Composite Material in the Wind Energy Market, offering in-depth insights into market size, growth drivers, restraints, opportunities, and challenges across various segments and key regions. It covers historical data from 2019 to 2023, along with market forecasts from 2025 to 2033. The study also includes an impact analysis of artificial intelligence on the market, a detailed examination of the competitive landscape, and profiles of leading industry players. The objective is to provide stakeholders with actionable intelligence to make informed strategic decisions.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 8.95 Billion |

| Market Forecast in 2033 | USD 20.35 Billion |

| Growth Rate | 10.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | TPI Composites, Gurit Holding AG, Toray Industries Inc., Hexcel Corporation, Owens Corning, Siemens Gamesa Renewable Energy S.A., Vestas Wind Systems A/S, GE Renewable Energy, Solvay S.A., SGL Carbon SE, BASF SE, Arkema S.A., Chomarat, Mitsubishi Chemical Corporation, Cytec Solvay Group, Exel Composites, The Dow Chemical Company, Teijin Limited |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Composite Material in the Wind Energy Market is meticulously segmented to provide a granular view of its various facets, allowing for a detailed understanding of market dynamics across different material types, applications, and manufacturing processes. These segmentations are critical for identifying key growth areas, competitive landscapes, and technological advancements within the industry. By breaking down the market into its constituent components, the analysis reveals how specific material choices or manufacturing methods contribute to the overall market expansion and where future innovations are likely to emerge. This comprehensive approach enables stakeholders to pinpoint lucrative opportunities and develop targeted strategies.

- By Fiber Type: This segment includes Glass Fiber, Carbon Fiber, Aramid Fiber, and other specialized fibers. Glass fiber composites currently dominate due to their cost-effectiveness and good performance, particularly for rotor blades. Carbon fiber is gaining traction for its superior stiffness and lightweight properties, enabling longer blades and enhanced efficiency, especially in larger turbines. Aramid fiber and other high-performance fibers are used in niche applications requiring exceptional impact resistance or specific mechanical properties.

- By Resin Type: This segment covers Epoxy, Polyester, Vinyl Ester, Polyurethane, and other resin systems. Epoxy resins are widely used for their excellent mechanical properties, adhesion, and fatigue resistance, making them ideal for high-performance blade manufacturing. Polyester resins offer a cost-effective solution for less demanding applications. Vinyl ester resins provide enhanced chemical resistance, while polyurethane resins are emerging for their potential in reducing manufacturing time and improving recyclability.

- By Application: This segment categorizes the market by the specific components where composites are utilized, primarily Rotor Blades, Nacelles, Towers, and Other Components (such as spinners, structural frames, and internal supports). Rotor blades represent the largest application segment due to their critical role in energy capture and the demanding performance requirements. Nacelles house vital operational components and require protective, lightweight, and durable composite enclosures. Composites are increasingly being explored for tower structures to reduce weight and enable taller designs, while other components benefit from composite properties for enhanced functionality and lifespan.

- By Manufacturing Process: This segment includes Hand Lay-up, Vacuum Infusion, Prepreg Lay-up, Pultrusion, Resin Transfer Molding (RTM), and other advanced processes. Vacuum infusion is a dominant process for large wind turbine blades, offering excellent material consolidation and reduced volatile organic compound (VOC) emissions. Hand lay-up is used for smaller components or specialized repairs. Prepreg lay-up offers high precision and material control but can be more costly. Pultrusion and RTM are increasingly adopted for producing standardized, high-volume components with consistent quality.

Regional Highlights

- Asia Pacific: The Asia Pacific region is anticipated to be a dominant and rapidly growing market for composite materials in wind energy, primarily driven by massive investments in renewable energy infrastructure, particularly in China and India. China's ambitious wind energy targets, coupled with its robust manufacturing capabilities and extensive coastlines for offshore wind development, make it a key growth engine. India's expanding energy needs and governmental support for wind power also contribute significantly. The region benefits from increasing industrialization, urbanization, and the imperative to reduce carbon emissions.

- Europe: Europe maintains a leading position in the Composite Material in the Wind Energy Market, characterized by early adoption of wind energy, strong regulatory support for renewables, and significant investments in offshore wind projects. Countries such as Germany, the UK, Denmark, and the Netherlands are at the forefront of technological innovation and have established robust supply chains for wind turbine components. The focus on sustainability and circular economy principles also drives research and development into advanced and recyclable composite solutions within the region.

- North America: North America, particularly the United States, demonstrates substantial growth in the wind energy sector, fueled by favorable government policies like tax credits and renewable portfolio standards. The region possesses vast onshore wind resources and is increasingly exploring offshore wind potential on its East and West coasts. Technological advancements, coupled with the drive for energy independence and decarbonization, are propelling the demand for high-performance composite materials for larger and more efficient turbines.

- Latin America: The Latin American market for composite materials in wind energy is experiencing steady growth, with countries like Brazil, Mexico, and Chile leading the charge. Abundant wind resources, coupled with growing energy demand and governmental efforts to diversify energy matrices, are attracting investments in wind power projects. While still developing compared to other regions, increasing infrastructure development and local manufacturing capabilities present significant long-term opportunities.

- Middle East and Africa (MEA): The MEA region is an emerging market for wind energy, with several countries initiating large-scale renewable energy projects to meet growing power demands and reduce reliance on fossil fuels. Investments in wind farms in countries like South Africa, Morocco, and Saudi Arabia are creating a nascent but expanding demand for composite materials. While currently a smaller share, the region's vast undeveloped wind resources offer considerable potential for future growth.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Composite Material in the Wind Energy Market.- TPI Composites

- Gurit Holding AG

- Toray Industries Inc.

- Hexcel Corporation

- Owens Corning

- Siemens Gamesa Renewable Energy S.A.

- Vestas Wind Systems A/S

- GE Renewable Energy

- Solvay S.A.

- SGL Carbon SE

- BASF SE

- Arkema S.A.

- Chomarat

- Mitsubishi Chemical Corporation

- Cytec Solvay Group

- Exel Composites

- The Dow Chemical Company

- Teijin Limited

- Saertex GmbH & Co. KG

- 3M Company

Frequently Asked Questions

Analyze common user questions about the Composite Material in the Wind Energy market and generate a concise list of summarized FAQs reflecting key topics and concerns.What are the primary composite materials used in wind turbines?

The primary composite materials used in wind turbines are glass fiber reinforced polymers (GFRP) and carbon fiber reinforced polymers (CFRP), utilizing resins such as epoxy, polyester, and vinyl ester. Glass fibers offer cost-effectiveness and good performance, while carbon fibers provide superior stiffness and strength-to-weight ratios for larger, more efficient blades.

How do composite materials contribute to the efficiency of wind energy?

Composite materials significantly enhance wind energy efficiency by enabling the construction of lighter, longer, and more aerodynamic turbine blades. Their high strength-to-weight ratio allows for larger rotor diameters, increasing energy capture. Additionally, their durability and fatigue resistance extend the operational lifespan of components, reducing maintenance and downtime.

What are the key challenges associated with composite materials in wind energy?

Key challenges include the high initial cost of advanced composites, particularly carbon fiber, and the complexities surrounding the recycling and end-of-life management of thermoset composite wind turbine blades. Supply chain volatility for raw materials and the need for specialized manufacturing processes for large components also pose significant hurdles.

What role does AI play in the future of composite materials for wind energy?

AI is expected to optimize the design and manufacturing of composite components, enhance material quality control, and enable predictive maintenance for wind turbines. AI-driven simulations can accelerate development of lighter and stronger blades, while real-time data analysis improves operational efficiency and extends component lifespan.

Which regions are leading in the adoption and innovation of composite materials for wind energy?

Europe and Asia Pacific are leading regions in the adoption and innovation of composite materials for wind energy. Europe benefits from early market development and strong offshore wind investment, while Asia Pacific, particularly China, drives demand through extensive wind farm development and robust manufacturing capabilities. North America also shows significant growth.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted