Commercial Refrigeration Compressor Market

Commercial Refrigeration Compressor Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706735 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

Commercial Refrigeration Compressor Market Size

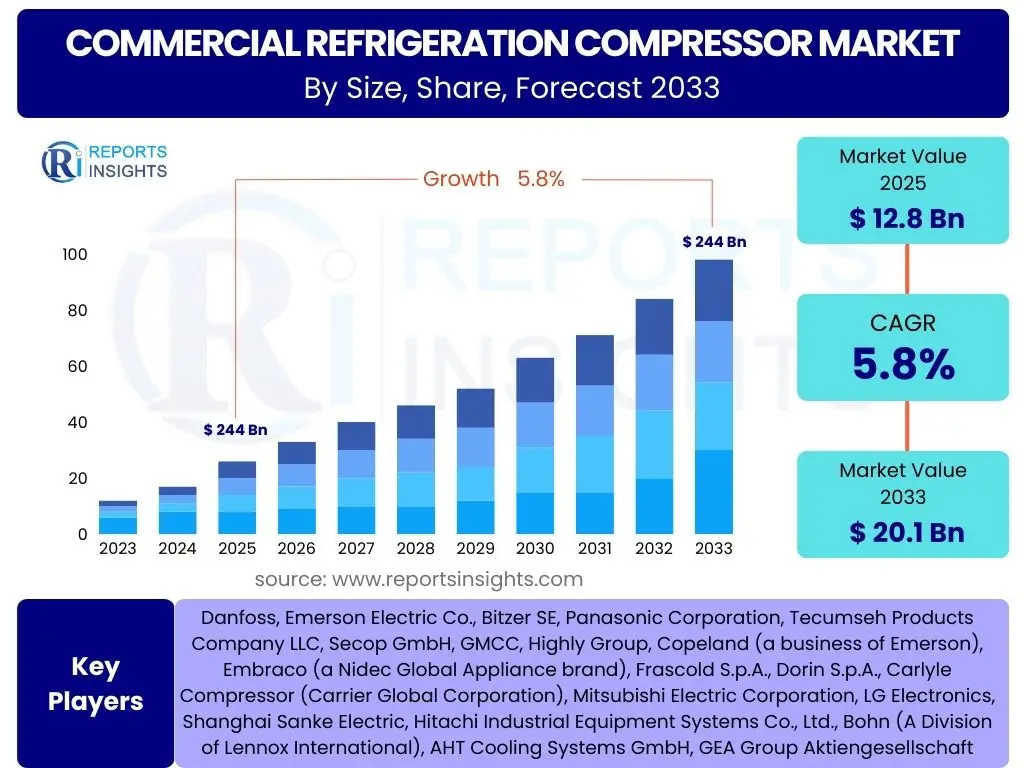

According to Reports Insights Consulting Pvt Ltd, The Commercial Refrigeration Compressor Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 12.8 Billion in 2025 and is projected to reach USD 20.1 Billion by the end of the forecast period in 2033.

Key Commercial Refrigeration Compressor Market Trends & Insights

The Commercial Refrigeration Compressor market is currently experiencing a transformative phase, driven by a confluence of technological advancements, stringent environmental regulations, and shifting consumer preferences. A major trend involves the accelerating adoption of natural refrigerants, such as CO2, ammonia, and hydrocarbons, as industries globally pivot away from hydrofluorocarbons (HFCs) due to their high global warming potential. This shift necessitates the development of new compressor technologies optimized for these environmentally friendly alternatives, leading to increased research and development investments in transcritical and subcritical CO2 systems.

Another significant insight is the growing emphasis on energy efficiency and connectivity. With rising energy costs and a global push towards sustainability, there is a strong demand for compressors that consume less power while maintaining optimal performance. This has spurred innovation in variable speed drive (VSD) compressors, digital scroll technology, and integrated smart controls that allow for real-time monitoring and optimization. The integration of IoT capabilities enables predictive maintenance, remote diagnostics, and improved system reliability, reducing operational downtime and costs for end-users. Furthermore, the expansion of the cold chain infrastructure, particularly in emerging economies, is driving demand for robust and efficient refrigeration solutions across various sectors, including food and beverage, pharmaceuticals, and retail.

- Accelerated adoption of natural refrigerants (CO2, ammonia, hydrocarbons).

- Rising demand for energy-efficient compressors, including Variable Speed Drive (VSD) and digital scroll technologies.

- Increasing integration of IoT and smart connectivity for real-time monitoring and predictive maintenance.

- Expansion of global cold chain infrastructure, particularly in developing regions.

- Focus on compact, lightweight, and quieter compressor designs for diverse applications.

AI Impact Analysis on Commercial Refrigeration Compressor

Artificial Intelligence (AI) is poised to significantly transform the commercial refrigeration compressor market by enhancing operational efficiency, predictive capabilities, and sustainable practices. Users are increasingly interested in how AI can optimize energy consumption, reduce maintenance costs, and improve system reliability. AI-powered algorithms can analyze vast amounts of data from compressor sensors, including temperature, pressure, vibration, and energy usage, to identify patterns and anomalies that indicate potential failures before they occur. This enables the transition from reactive to predictive maintenance, minimizing unexpected downtime and extending the lifespan of refrigeration units.

Beyond predictive maintenance, AI also plays a crucial role in optimizing the performance of refrigeration systems. Through machine learning, AI can dynamically adjust compressor speeds, refrigerant flow, and defrost cycles based on real-time environmental conditions, load demands, and even energy tariffs. This intelligent control leads to substantial energy savings and reduced operational expenditures. Furthermore, AI can aid in designing more efficient compressor components and systems by simulating various operating conditions and material properties, accelerating innovation in the sector. The integration of AI in refrigeration management platforms is expected to create a more responsive, efficient, and sustainable cold chain ecosystem.

- Predictive maintenance and anomaly detection, reducing downtime.

- Optimized energy consumption through dynamic control and load balancing.

- Enhanced system diagnostics and automated troubleshooting.

- Improved supply chain efficiency for refrigerated goods through data analytics.

- Accelerated R&D for more efficient compressor designs and materials.

Key Takeaways Commercial Refrigeration Compressor Market Size & Forecast

The commercial refrigeration compressor market is on a robust growth trajectory, driven primarily by an expanding global cold chain, stringent energy efficiency regulations, and the rising adoption of natural refrigerants. A key takeaway from the market forecast is the significant investment in research and development aimed at producing more sustainable and energy-efficient compressor technologies. This includes innovations in variable speed drives, digital scroll technology, and the development of compressors specifically designed for low global warming potential (GWP) refrigerants, which are becoming mandatory in many regions.

Another crucial insight is the increasing demand from emerging economies, particularly in the Asia Pacific region, fueled by rapid urbanization, growth in the organized retail sector, and increasing disposable incomes leading to higher consumption of perishable goods. The market is also being shaped by the integration of smart technologies, such as IoT and AI, which are enhancing system performance, enabling predictive maintenance, and offering greater control and monitoring capabilities to end-users. These technological advancements, coupled with an escalating focus on environmental sustainability, are critical factors underpinning the projected market expansion and shaping future investment opportunities.

- Strong growth fueled by cold chain expansion and regulatory push for efficiency.

- Significant shift towards natural refrigerant-compatible compressors.

- Emerging markets, especially in Asia Pacific, are major growth hubs.

- Technological advancements in smart controls and IoT integration are pivotal.

- Increased focus on sustainable and energy-efficient solutions drives innovation.

Commercial Refrigeration Compressor Market Drivers Analysis

The expansion of the global cold chain infrastructure stands as a primary driver for the commercial refrigeration compressor market. As populations grow and urbanization accelerates, particularly in developing regions, the demand for perishable goods such as fresh food, pharmaceuticals, and floriculture products intensifies. This necessitates a robust and efficient cold chain, from production to retail, creating a continuous demand for commercial refrigeration units and, by extension, their core component: compressors. The growth of organized retail, including supermarkets, hypermarkets, and convenience stores, further amplifies this demand by requiring extensive refrigeration capacities for product display and storage.

Additionally, stringent environmental regulations aimed at phasing out high global warming potential (GWP) refrigerants are compelling manufacturers and end-users to adopt more eco-friendly and energy-efficient compressor technologies. Regulations like the F-Gas Regulation in Europe and the SNAP program in the U.S. are accelerating the shift towards natural refrigerants such as CO2, propane, and ammonia, which often require specialized compressor designs. This regulatory pressure not only drives innovation but also encourages the replacement of older, less efficient systems with new, compliant ones, thereby creating a continuous market for advanced compressors. The increasing awareness among consumers and businesses regarding energy conservation and sustainability further supports the adoption of high-efficiency compressors that reduce operational costs and environmental impact.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion of Cold Chain & Organized Retail | +1.8% | Global, particularly APAC & Latin America | Mid to Long-term (2025-2033) |

| Increasing Demand for Processed & Perishable Foods | +1.5% | Globally, including Developed & Emerging Markets | Mid to Long-term (2025-2033) |

| Stringent Energy Efficiency & Environmental Regulations | +1.3% | Europe, North America, parts of Asia | Short to Mid-term (2025-2029) |

| Technological Advancements in Compressor Design (e.g., VSD, Digital Scroll) | +1.2% | Global | Mid to Long-term (2025-2033) |

Commercial Refrigeration Compressor Market Restraints Analysis

The high initial investment costs associated with advanced commercial refrigeration compressor systems, especially those designed for natural refrigerants, pose a significant restraint on market growth. While these systems offer long-term energy savings and environmental benefits, their upfront price can be prohibitive for small and medium-sized enterprises (SMEs) or businesses operating on tight budgets. The complexity of installing and maintaining these sophisticated systems, often requiring specialized technicians, also adds to the overall cost burden, deterring some potential adopters. This cost barrier can slow down the adoption rate, particularly in regions where economic stability is a concern or where capital expenditure budgets are constrained.

Furthermore, the fluctuating prices of raw materials, such as copper, steel, and aluminum, which are essential for compressor manufacturing, introduce an element of unpredictability to production costs. These volatilities can impact profit margins for manufacturers and lead to price increases for end-products, potentially dampening demand. Additionally, the existing large installed base of conventional HFC-based refrigeration systems presents a challenge. While regulations encourage their replacement, the sheer scale of these legacy systems means that the transition to newer, more compliant technologies will be gradual, creating a lag in the complete market overhaul and maintaining a certain level of demand for replacement parts for older systems.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment & Installation Costs | -0.8% | Global, particularly SMEs | Mid-term (2025-2030) |

| Volatile Raw Material Prices | -0.5% | Global (Manufacturing regions) | Short to Mid-term (2025-2028) |

| Technological Complexity & Skilled Labor Shortage | -0.4% | Global, particularly developing markets | Mid to Long-term (2025-2033) |

| Competition from Alternative Cooling Technologies | -0.3% | Specific Niche Applications | Long-term (2028-2033) |

Commercial Refrigeration Compressor Market Opportunities Analysis

The burgeoning trend towards the adoption of natural refrigerants presents a significant opportunity for market players in the commercial refrigeration compressor sector. As global environmental regulations become increasingly stringent regarding high GWP refrigerants, there is a growing demand for compressors optimized for natural alternatives like CO2 (R744), propane (R290), and ammonia (R717). This shift opens avenues for innovation in compressor design, material science, and system integration, allowing manufacturers to develop and market new product lines that comply with future environmental standards and cater to a sustainability-conscious market. Early movers in this segment can establish strong market positions and capture a substantial share of the growing demand for eco-friendly solutions.

Furthermore, the increasing integration of smart technologies, including the Internet of Things (IoT), artificial intelligence (AI), and advanced analytics, offers vast opportunities for enhancing compressor performance and market value. Compressors equipped with IoT sensors can provide real-time operational data, enabling predictive maintenance, energy optimization, and remote diagnostics, which significantly reduce operational costs and improve system reliability for end-users. This technological convergence allows for the creation of value-added services, such as energy management platforms and smart refrigeration solutions, transforming the traditional hardware business into a more comprehensive service-oriented model. The untapped potential in emerging markets, particularly for expanding cold chain infrastructure and modernizing existing retail formats, also represents a substantial growth opportunity, driving demand for both new installations and system upgrades.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Adoption of Natural Refrigerants | +1.5% | Europe, North America, parts of Asia | Mid to Long-term (2025-2033) |

| Integration of IoT, AI, & Smart Controls | +1.2% | Global, particularly developed markets | Mid to Long-term (2025-2033) |

| Expansion in Emerging Markets & Untapped Regions | +1.0% | APAC, Latin America, MEA | Long-term (2028-2033) |

| Retrofitting & Replacement of Aging Infrastructure | +0.8% | Developed Markets (Europe, North America) | Mid-term (2025-2030) |

Commercial Refrigeration Compressor Market Challenges Impact Analysis

Navigating the complex and evolving landscape of environmental regulations poses a significant challenge for manufacturers and users in the commercial refrigeration compressor market. While regulations promote sustainability, their varying implementation across different regions and countries, along with frequent updates, can create compliance complexities. For instance, the phase-down schedules and permitted GWP limits for refrigerants differ globally, requiring manufacturers to develop region-specific products or invest heavily in flexible designs. This fragmentation can increase R&D costs, complicate supply chain management, and potentially limit market access for non-compliant products, slowing down market penetration of new technologies.

Another prominent challenge is the increasing need for highly skilled technicians capable of installing, maintaining, and repairing advanced refrigeration systems, especially those using natural refrigerants like CO2, which operate at higher pressures. The current shortage of such specialized labor, particularly in emerging markets, can lead to higher service costs, extended downtime, and compromise the efficiency and longevity of sophisticated refrigeration equipment. Furthermore, the constant pressure to innovate while keeping costs competitive and ensuring product reliability represents a perpetual challenge. Balancing the development of cutting-edge, energy-efficient, and eco-friendly compressors with cost-effective manufacturing and market pricing requires significant strategic planning and investment, especially in a price-sensitive market environment.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complexity of Evolving Environmental Regulations | -0.7% | Global, particularly Europe & North America | Short to Mid-term (2025-2029) |

| Shortage of Skilled Technicians for New Technologies | -0.6% | Global, more pronounced in emerging markets | Mid to Long-term (2025-2033) |

| Intense Price Competition & Cost Sensitivity | -0.5% | Global | Mid-term (2025-2030) |

| Managing Supply Chain Disruptions & Component Shortages | -0.4% | Global | Short-term (2025-2027) |

Commercial Refrigeration Compressor Market - Updated Report Scope

This report provides a detailed and extensive analysis of the global Commercial Refrigeration Compressor Market, offering comprehensive insights into its current size, historical performance, and future growth projections from 2025 to 2033. It examines the key market drivers, restraints, opportunities, and challenges that influence market dynamics, along with an in-depth assessment of AI's transformative impact. The study segments the market by various types, applications, and end-use sectors across major geographical regions, identifying growth hotspots and competitive landscapes to deliver actionable intelligence for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 12.8 Billion |

| Market Forecast in 2033 | USD 20.1 Billion |

| Growth Rate | 5.8% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Danfoss, Emerson Electric Co., Bitzer SE, Panasonic Corporation, Tecumseh Products Company LLC, Secop GmbH, GMCC, Highly Group, Copeland (a business of Emerson), Embraco (a Nidec Global Appliance brand), Frascold S.p.A., Dorin S.p.A., Carlyle Compressor (Carrier Global Corporation), Mitsubishi Electric Corporation, LG Electronics, Shanghai Sanke Electric, Hitachi Industrial Equipment Systems Co., Ltd., Bohn (A Division of Lennox International), AHT Cooling Systems GmbH, GEA Group Aktiengesellschaft |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The commercial refrigeration compressor market is extensively segmented to provide a granular understanding of its diverse components and evolving dynamics. These segmentations allow for a detailed analysis of market performance across different compressor technologies, refrigerant types, application areas, and end-use industries. The "By Type" segmentation captures the various mechanical designs of compressors, each suited for specific performance requirements and efficiency levels, from the ubiquitous reciprocating and rotary types to the more advanced scroll and screw compressors favored for larger applications. Understanding the market share and growth trends within each type is crucial for manufacturers to align their product development with market demand.

The "By Refrigerant Type" segment highlights the ongoing industry transition towards environmentally sustainable solutions, differentiating between traditional HFCs and HCFCs, newer HFOs, and the rapidly growing natural refrigerants such as CO2, ammonia, and propane. This segmentation underscores the impact of environmental regulations and consumer preferences on product innovation. Furthermore, segmenting by "Application" and "End-Use" provides insights into the primary sectors driving demand, from food and beverage retail and foodservice to healthcare and cold storage warehouses. This multi-faceted segmentation helps stakeholders pinpoint high-growth areas, develop targeted strategies, and optimize resource allocation across the value chain.

- By Type: Rotary, Reciprocating, Scroll, Screw, Centrifugal

- By Refrigerant Type: HFC, HCFC, HFO, Natural Refrigerants (CO2, Ammonia, Propane, Others)

- By Application: Refrigerators & Freezers, Vending Machines, Display Cases, Ice Machines, Transport Refrigeration, Others

- By End-Use: Food & Beverage Retail, Food Service, Hospitality, Healthcare, Cold Storage Warehouses, Chemical, Logistics & Transport, Others

- By Capacity: Up to 1 HP, 1 HP to 5 HP, Above 5 HP

Regional Highlights

- North America: This region is characterized by early adoption of advanced refrigeration technologies and a strong emphasis on energy efficiency and environmental compliance. The presence of major cold chain logistics providers, a developed retail food sector, and a growing pharmaceutical industry drives consistent demand for commercial refrigeration compressors. Regulatory frameworks, such as those promoting the phase-down of HFCs, also stimulate the adoption of natural refrigerant-based systems and high-efficiency units.

- Europe: Europe is a frontrunner in the adoption of natural refrigerants, largely due to stringent environmental regulations like the F-Gas Regulation. This has spurred significant innovation in CO2 and hydrocarbon-based compressor technologies. The mature food and beverage market, alongside a strong focus on sustainability and energy conservation, ensures a robust demand for highly efficient and eco-friendly commercial refrigeration solutions across the continent.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region in the commercial refrigeration compressor market. This growth is propelled by rapid urbanization, increasing disposable incomes, and the burgeoning organized retail sector in countries like China, India, and Southeast Asian nations. The expansion of cold chain infrastructure to support growing food and pharmaceutical industries, coupled with rising awareness of food safety, significantly contributes to market expansion in this region.

- Latin America: The market in Latin America is witnessing steady growth, driven by expanding retail and foodservice industries, particularly in countries like Brazil and Mexico. Investments in modernizing food processing and storage facilities, along with increasing international trade in perishable goods, fuel the demand for commercial refrigeration compressors. While natural refrigerant adoption is slower than in Europe, there is a gradual shift towards more energy-efficient solutions.

- Middle East and Africa (MEA): This region presents emerging opportunities due to significant investments in infrastructure development, particularly in the cold chain and hospitality sectors. The hot climatic conditions necessitate efficient cooling solutions, contributing to the demand for commercial refrigeration. While the market is still developing, a growing awareness of food security and the expansion of tourism and retail are expected to drive future growth.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Commercial Refrigeration Compressor Market.- Danfoss

- Emerson Electric Co.

- Bitzer SE

- Panasonic Corporation

- Tecumseh Products Company LLC

- Secop GmbH

- GMCC

- Highly Group

- Copeland (a business of Emerson)

- Embraco (a Nidec Global Appliance brand)

- Frascold S.p.A.

- Dorin S.p.A.

- Carlyle Compressor (Carrier Global Corporation)

- Mitsubishi Electric Corporation

- LG Electronics

- Shanghai Sanke Electric

- Hitachi Industrial Equipment Systems Co., Ltd.

- Bohn (A Division of Lennox International)

- AHT Cooling Systems GmbH

- GEA Group Aktiengesellschaft

Frequently Asked Questions

What is the projected growth rate for the Commercial Refrigeration Compressor market?

The Commercial Refrigeration Compressor market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033, driven by expanding cold chain infrastructure and increasing demand for energy-efficient solutions.

What are the key technological trends influencing the market?

Key technological trends include the accelerated adoption of natural refrigerants, advancements in energy-efficient compressor designs like Variable Speed Drive (VSD) and digital scroll, and the increasing integration of IoT and smart controls for enhanced monitoring and predictive maintenance.

How do environmental regulations impact the Commercial Refrigeration Compressor market?

Environmental regulations, particularly those phasing down high global warming potential (GWP) refrigerants, significantly drive market innovation by compelling manufacturers and end-users to adopt compressors optimized for natural refrigerants, thereby accelerating the transition to more sustainable solutions.

Which region is expected to lead market growth and why?

The Asia Pacific (APAC) region is expected to lead market growth due to rapid urbanization, increasing disposable incomes, the expansion of organized retail, and significant investments in developing robust cold chain infrastructure to meet the rising demand for perishable goods.

What are the main challenges faced by the Commercial Refrigeration Compressor market?

Major challenges include high initial investment costs for advanced systems, the complexity of navigating diverse and evolving environmental regulations, and a shortage of skilled technicians capable of handling sophisticated refrigeration technologies, particularly those utilizing natural refrigerants.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted