Commercial Radome Market

Commercial Radome Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702576 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

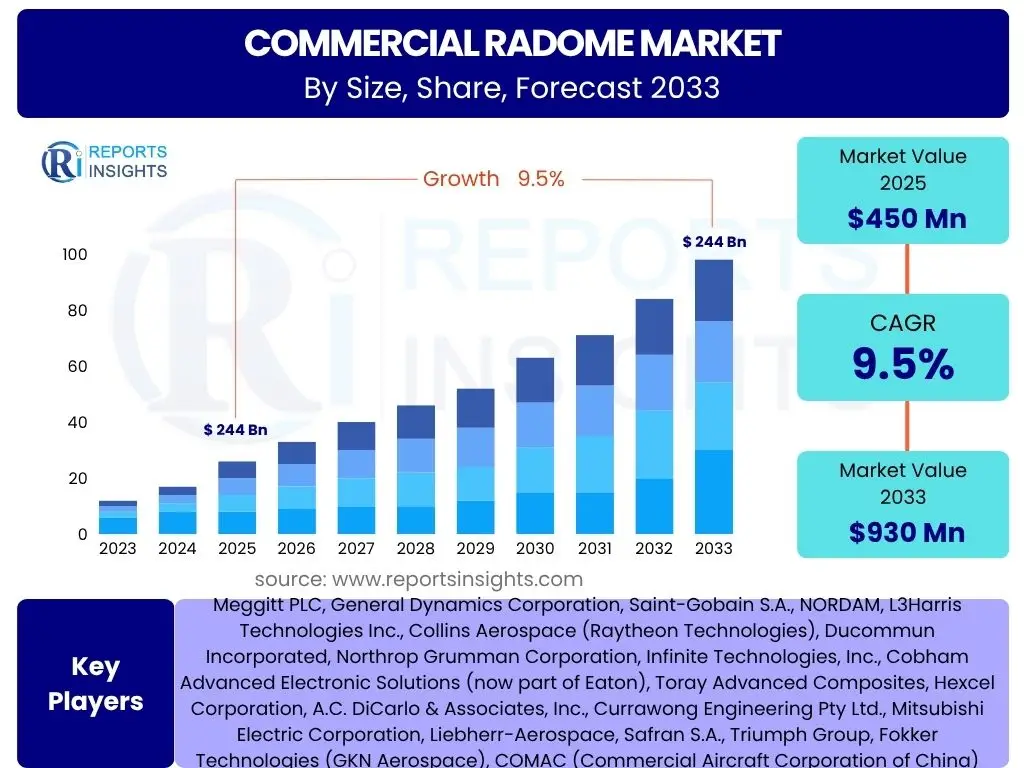

Commercial Radome Market Size

According to Reports Insights Consulting Pvt Ltd, The Commercial Radome Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2025 and 2033. The market is estimated at USD 450 Million in 2025 and is projected to reach USD 930 Million by the end of the forecast period in 2033.

Key Commercial Radome Market Trends & Insights

User inquiries frequently highlight an intense focus on the evolution of materials science and advanced manufacturing techniques as central to commercial radome development. The industry is witnessing a significant shift towards lighter, stronger, and more electromagnetically transparent materials that can withstand increasingly harsh environmental conditions while maintaining optimal signal integrity. This includes research into novel composites, thermoplastic structures, and even metamaterials designed to offer superior performance characteristics across broader frequency ranges, addressing the demand for multi-functional capabilities in contemporary airborne and ground-based systems.

Another prominent area of interest revolves around the integration of advanced communication technologies, specifically the pervasive influence of 5G and the expanding role of satellite communication systems. Commercial radomes are increasingly required to support higher bandwidths, multiple frequency bands simultaneously, and enhanced data transmission rates without compromising aerodynamic efficiency or structural durability. This trend necessitates sophisticated design methodologies that can minimize signal loss and interference, paving the way for more integrated and intelligent radome systems that are seamlessly incorporated into the overall aircraft or platform architecture.

Furthermore, the diversification of applications beyond traditional commercial aircraft is a key trend. The burgeoning Urban Air Mobility (UAM) sector, the proliferation of commercial Unmanned Aerial Vehicles (UAVs) for logistics and surveillance, and the expansion of ground-based commercial satellite communication networks are creating new and distinct requirements for radome design. These varied applications demand customizable solutions regarding size, weight, shape, and specific performance profiles, driving innovation in miniaturization, modularity, and rapid prototyping to meet specialized operational needs while adhering to stringent industry standards.

- Advanced materials (e.g., thermoset composites, thermoplastics, metamaterials) for enhanced performance.

- Lightweighting and aerodynamic optimization for fuel efficiency and reduced drag.

- Increased demand for multi-band and broadband compatibility to support diverse communication systems (e.g., 5G, SATCOM Ku/Ka/V-band).

- Integration of smart features and sensor capabilities within radome structures.

- Miniaturization and modular design for diverse applications, including UAVs and UAM.

- Focus on improved stealth and electromagnetic signature management for specialized commercial applications.

- Growing adoption of predictive maintenance and structural health monitoring for radome integrity.

AI Impact Analysis on Commercial Radome

User questions regarding the impact of Artificial intelligence (AI) on commercial radomes frequently center on its potential to revolutionize the design, manufacturing, and maintenance phases. There is considerable interest in how AI, particularly through machine learning and generative design algorithms, can significantly accelerate the iterative design process. By simulating various material combinations, structural configurations, and electromagnetic properties, AI can optimize radome performance for specific operational parameters, leading to superior structural integrity, electromagnetic transparency, and aerodynamic efficiency far more rapidly than traditional methods. This capability enables designers to explore a vast array of possibilities, identifying optimal solutions that balance conflicting performance requirements.

Moreover, AI is anticipated to play a crucial role in enhancing the manufacturing precision and quality control of commercial radomes. AI-powered vision systems and data analytics can monitor production lines in real-time, detecting even minuscule defects in materials or manufacturing processes that might otherwise compromise the radome’s performance or lifespan. This predictive quality assurance can drastically reduce waste, improve yield rates, and ensure that each radome meets stringent aerospace standards. Furthermore, AI can optimize complex composite layup procedures and automated assembly processes, leading to greater consistency and efficiency in large-scale production environments.

In the operational and maintenance phases, AI offers transformative potential for predictive maintenance and anomaly detection. By continuously analyzing sensor data from in-service radomes, AI algorithms can predict potential failures due to environmental stress, fatigue, or impact, allowing for proactive maintenance before issues escalate. This shifts maintenance strategies from reactive to predictive, significantly reducing downtime, enhancing safety, and lowering operational costs for airlines and other commercial operators. The ability of AI to interpret vast datasets from flight operations, weather conditions, and performance metrics will ensure the longevity and reliability of radome systems throughout their lifecycle.

- Generative design and simulation for optimized radome shape, material composition, and electromagnetic performance.

- AI-powered predictive maintenance for early detection of structural damage or material degradation.

- Enhanced quality control in manufacturing through AI-driven visual inspection and anomaly detection.

- Optimization of manufacturing processes, including automated composite layup and curing cycles.

- Real-time performance monitoring and adaptive signal processing to compensate for environmental factors.

- Data analytics for lifecycle management, improving design iterations based on in-service performance.

Key Takeaways Commercial Radome Market Size & Forecast

Insights derived from user queries about the Commercial Radome market's size and forecast underscore the critical role of technological advancement as the primary growth catalyst. The market's expansion is not merely volume-driven but fundamentally propelled by innovations in material science, manufacturing processes, and communication technologies. The transition towards high-performance radomes that can accommodate multi-band frequencies, withstand extreme conditions, and contribute to overall aircraft efficiency is a significant underlying driver, positioning the market for sustained expansion as aviation and satellite communication sectors continue their upward trajectory.

Another key takeaway is the increasing diversification of demand, moving beyond traditional commercial airliners to encompass emerging aviation segments. The rapid growth in business jets, the accelerating development of Unmanned Aerial Vehicles (UAVs) for commercial applications, and the nascent Urban Air Mobility (UAM) sector are all creating new and distinct market niches for specialized radome solutions. This diversification mandates greater flexibility in design, manufacturing, and material selection, ensuring that radomes can be tailored to specific platform requirements, whether for high-altitude endurance, urban operational density, or payload-specific communication needs.

Furthermore, the global nature of the aviation and communication industries means that regional dynamics significantly influence market development. While North America and Europe remain mature markets with established players and ongoing upgrade cycles, the Asia Pacific region is rapidly emerging as a central hub for growth, driven by increasing air passenger traffic, new aircraft deliveries, and expanding satellite communication infrastructure. This regional shift, coupled with continued investment in research and development for next-generation aerospace technologies, indicates a robust and evolving market landscape where innovation and adaptability will be paramount for market participants to capture growth opportunities.

- The market is poised for significant growth, primarily driven by advancements in materials and communication technologies.

- Expanding commercial aviation fleet, including new aircraft deliveries and retrofits, is a major demand generator.

- Emerging applications like commercial UAVs, Urban Air Mobility (UAM), and advanced satellite communication systems are creating new market avenues.

- Material innovation, focusing on lightweight, electromagnetically transparent, and durable solutions, is central to future development.

- Asia Pacific is expected to exhibit the fastest growth due to increasing air traffic and investment in aerospace infrastructure.

- Integration of AI and smart features into radome design and maintenance will enhance performance and efficiency.

Commercial Radome Market Drivers Analysis

The Commercial Radome Market is significantly propelled by several key drivers stemming from the global aerospace and telecommunications sectors. The continuous expansion of commercial aviation, marked by increasing air passenger traffic and the subsequent demand for new aircraft deliveries and fleet modernizations, necessitates a steady supply of advanced radomes. Concurrently, the burgeoning satellite communication industry, with its drive for higher bandwidths and ubiquitous connectivity, particularly for in-flight entertainment and broadband services, directly fuels the demand for sophisticated radome solutions capable of managing complex frequency requirements. This dual demand from traditional aviation and advanced communication applications underpins much of the market’s current growth trajectory, emphasizing the radome’s indispensable role in modern air transport and connectivity.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in commercial aviation (new aircraft deliveries, fleet modernization) | +2.5% | Global, particularly Asia Pacific, North America, Europe | 2025-2033 |

| Increasing demand for satellite communication (in-flight connectivity, broadband services) | +2.0% | Global, high impact in North America, Europe, Middle East | 2025-2033 |

| Technological advancements in materials (composites, thermoplastics, metamaterials) | +1.8% | Global, strong R&D in North America, Europe, parts of Asia | 2025-2033 |

| Expanding commercial UAV and Urban Air Mobility (UAM) markets | +1.5% | North America, Europe, Asia Pacific | 2027-2033 |

| Need for enhanced radar and communication system performance (multi-band, higher data rates) | +1.2% | Global | 2025-2033 |

Commercial Radome Market Restraints Analysis

Despite robust growth drivers, the Commercial Radome Market faces several significant restraints that could temper its expansion. The inherent complexity of radome design and manufacturing, involving specialized materials, intricate aerodynamic shapes, and rigorous electromagnetic performance requirements, translates into high production costs. This elevated cost can be a barrier for new entrants and may limit adoption rates, especially for smaller operators or in cost-sensitive segments. Furthermore, the stringent regulatory environment governing aerospace components, including lengthy and expensive certification processes, can significantly delay product introduction and innovation, posing a substantial hurdle for market players seeking to bring novel radome technologies to commercial deployment. These factors collectively contribute to a challenging operating landscape for radome manufacturers.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High manufacturing and material costs for advanced radomes | -1.8% | Global | 2025-2033 |

| Stringent regulatory approvals and lengthy certification processes | -1.5% | Global, particularly North America, Europe | 2025-2033 |

| Material limitations at extreme frequencies or environmental conditions | -1.0% | Global | 2025-2033 |

| Complexity of design and testing for multi-functionality and broad bandwidths | -0.8% | Global | 2025-2033 |

| Potential for supply chain disruptions in specialized materials | -0.7% | Global, due to concentrated supply sources | 2025-2030 |

Commercial Radome Market Opportunities Analysis

The Commercial Radome Market is ripe with opportunities driven by technological innovation and evolving aerospace needs. The ongoing development of next-generation materials, such as advanced composites, smart materials, and even emerging metamaterials, presents a significant avenue for creating radomes with unparalleled performance characteristics, including superior electromagnetic transparency, enhanced durability, and reduced weight. These material breakthroughs can unlock new design possibilities and improve the efficiency of communication and radar systems. Concurrently, the burgeoning Urban Air Mobility (UAM) sector and the rapid expansion of commercial drone operations are creating entirely new application areas for compact, lightweight, and highly performant radomes, catering to distinct size and operational requirements not previously seen in traditional aviation.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development and integration of next-generation materials (e.g., smart materials, metamaterials) | +2.2% | Global, R&D focused in North America, Europe, select Asian countries | 2026-2033 |

| Demand from emerging aviation sectors (Urban Air Mobility, advanced commercial UAVs) | +2.0% | North America, Europe, Asia Pacific | 2027-2033 |

| Increasing need for retrofitting existing aircraft with advanced communication systems | +1.5% | Global, particularly mature aviation markets | 2025-2033 |

| Advancements in 5G and IoT integration for air-to-ground and air-to-air connectivity | +1.3% | Global | 2026-2033 |

| Expansion into new geographical markets, particularly developing economies | +1.0% | Asia Pacific, Latin America, Middle East & Africa | 2025-2033 |

Commercial Radome Market Challenges Impact Analysis

The Commercial Radome Market faces distinct challenges that can impede its growth and technological progression. A primary challenge involves maintaining optimal structural integrity and electromagnetic performance across an increasingly wide range of operating frequencies and harsh environmental conditions. Balancing the need for high signal transparency with robust mechanical strength and resistance to factors like ice, rain erosion, and UV degradation requires sophisticated material science and engineering. Furthermore, managing Electromagnetic Interference (EMI) within increasingly crowded spectrum environments, especially with the proliferation of onboard electronic systems and diverse communication frequencies, presents a complex hurdle, demanding innovative shielding and design solutions to prevent signal distortion or degradation. These technical complexities necessitate continuous research and development, adding to product development costs and timelines.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Maintaining structural integrity and electromagnetic performance across wide frequency ranges and harsh environments | -1.7% | Global | 2025-2033 |

| Balancing lightweighting with mechanical strength and durability | -1.4% | Global | 2025-2033 |

| Managing electromagnetic interference (EMI) in complex onboard electronic systems | -1.2% | Global | 2025-2033 |

| High research and development investments required for new materials and designs | -1.0% | Global, concentrated in leading R&D nations | 2025-2033 |

| Addressing cybersecurity risks for connected radome systems and data integrity | -0.8% | Global | 2027-2033 |

Commercial Radome Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Commercial Radome Market, offering a detailed segmentation of the market by material type, application, end-use, and frequency band. It includes historical data from 2019 to 2023, current market estimates for 2025, and projections through 2033. The report meticulously examines market trends, drivers, restraints, opportunities, and challenges, providing a holistic view of the industry landscape. Furthermore, it incorporates an AI impact analysis and regional insights, identifying key growth areas and competitive dynamics among leading market players.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 450 Million |

| Market Forecast in 2033 | USD 930 Million |

| Growth Rate | 9.5% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Meggitt PLC, General Dynamics Corporation, Saint-Gobain S.A., NORDAM, L3Harris Technologies Inc., Collins Aerospace (Raytheon Technologies), Ducommun Incorporated, Northrop Grumman Corporation, Infinite Technologies, Inc., Cobham Advanced Electronic Solutions (now part of Eaton), Toray Advanced Composites, Hexcel Corporation, A.C. DiCarlo & Associates, Inc., Currawong Engineering Pty Ltd., Mitsubishi Electric Corporation, Liebherr-Aerospace, Safran S.A., Triumph Group, Fokker Technologies (GKN Aerospace), COMAC (Commercial Aircraft Corporation of China) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Commercial Radome Market is broadly segmented across several key dimensions to provide a nuanced understanding of its intricate dynamics and diverse application landscape. This segmentation allows for precise analysis of demand patterns, technological preferences, and regional contributions across different product types and end-use sectors. Understanding these segments is crucial for stakeholders to identify specific growth opportunities and tailor product development strategies to meet the evolving needs of various commercial aviation and communication applications. Each segment represents distinct requirements regarding material properties, design complexities, and operational environments, necessitating specialized radome solutions.

- By Material: Includes Composite (Fiberglass, Quartz, Carbon Fiber, Hybrid Composites), Thermoplastics, and Other Advanced Materials like Metamaterials, emphasizing the shift towards high-performance, lightweight, and electromagnetically optimized structures.

- By Application: Covers Commercial Aircraft (Narrow-body, Wide-body, Regional Jets), Business Jets, Unmanned Aerial Vehicles (UAVs), Commercial Ground Stations, and Commercial Marine Vessels, reflecting the expanding range of platforms requiring protective enclosures for their communication and radar systems.

- By End-Use: Differentiates demand from Airlines, Satellite Communication Providers, Commercial UAV Operators, Air Traffic Control & Navigation, and Other entities such as private owners or freight carriers, illustrating the diverse user base for commercial radomes.

- By Frequency Band: Details market activity across X-band, Ku-band, Ka-band, C-band, L-band, S-band, and Other Bands (e.g., V-band, Q-band), highlighting the increasing need for radomes capable of supporting multiple and higher frequency communications critical for modern data-intensive applications.

Regional Highlights

- North America: This region maintains a significant market share, driven by a mature aerospace industry, robust defense spending, and substantial investments in advanced communication technologies. The presence of major aircraft manufacturers, satellite operators, and leading radome solution providers contributes to continuous innovation and demand for high-performance radomes. Focus areas include next-generation aircraft programs, modernization of existing fleets, and expansion of in-flight connectivity services.

- Europe: Characterized by a strong aerospace manufacturing base and a focus on research and development in composite materials, Europe represents a key market. Demand is fueled by major aircraft OEM production, regional aviation growth, and the deployment of advanced air traffic management systems. Strict regulatory standards also drive innovation in safety and performance for radome technology across the region.

- Asia Pacific (APAC): Expected to be the fastest-growing region, propelled by surging air passenger traffic, substantial investments in new airport infrastructure, and an increasing number of commercial aircraft deliveries. Countries like China and India are experiencing rapid expansion in their aviation sectors, alongside growing satellite communication needs, creating immense opportunities for radome manufacturers. The region is also becoming a hub for UAV development and deployment, further stimulating market growth.

- Latin America: This region presents emerging opportunities due to the expansion of regional aviation networks and increasing demand for improved air connectivity. While smaller in market size compared to North America or Europe, ongoing fleet upgrades and a focus on enhancing communication infrastructure are expected to contribute to steady growth in the commercial radome market.

- Middle East & Africa (MEA): Marked by significant investments in aviation infrastructure and the development of major international air hubs, the MEA region is experiencing notable growth. The demand is driven by fleet expansion of national carriers, ambitious tourism development plans, and strategic geographical positioning for global air routes, all requiring state-of-the-art communication and radar systems that rely on advanced radomes.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Commercial Radome Market.- Meggitt PLC

- General Dynamics Corporation

- Saint-Gobain S.A.

- NORDAM

- L3Harris Technologies Inc.

- Collins Aerospace (Raytheon Technologies)

- Ducommun Incorporated

- Northrop Grumman Corporation

- Infinite Technologies, Inc.

- Cobham Advanced Electronic Solutions (now part of Eaton)

- Toray Advanced Composites

- Hexcel Corporation

- A.C. DiCarlo & Associates, Inc.

- Currawong Engineering Pty Ltd.

- Mitsubishi Electric Corporation

- Liebherr-Aerospace

- Safran S.A.

- Triumph Group

- Fokker Technologies (GKN Aerospace)

- COMAC (Commercial Aircraft Corporation of China)

Frequently Asked Questions

Analyze common user questions about the Commercial Radome market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is a commercial radome and its primary function?

A commercial radome is a structural enclosure that protects a radar or antenna from environmental elements (e.g., wind, rain, ice, UV radiation) without significantly attenuating or distorting the electromagnetic signals. Its primary function is to ensure optimal performance and longevity of onboard communication, navigation, and weather radar systems in commercial aircraft, UAVs, and ground stations.

Why are advanced materials crucial for modern commercial radomes?

Advanced materials, such as composites, thermoplastics, and metamaterials, are crucial for modern commercial radomes because they offer superior electromagnetic transparency, lighter weight, enhanced structural integrity, and better resistance to extreme environmental conditions. These properties are vital for accommodating multi-band frequencies, improving fuel efficiency, and extending the lifespan of sensitive electronic equipment.

How does 5G technology influence commercial radome design and demand?

5G technology significantly influences commercial radome design by demanding increased bandwidth capabilities and compatibility with higher frequency bands. Radomes must be engineered to minimize signal loss and interference at these new frequencies, supporting faster in-flight connectivity, real-time data transfer, and advanced air-to-ground communication, thereby driving demand for more sophisticated and electromagnetically efficient designs.

What are the key applications driving the growth of the commercial radome market?

The key applications driving growth in the commercial radome market include the expanding fleets of commercial aircraft (both new deliveries and retrofits), the rapid proliferation of commercial Unmanned Aerial Vehicles (UAVs) for various tasks, the development of Urban Air Mobility (UAM) vehicles, and the increasing global demand for high-bandwidth satellite communication services for in-flight entertainment and broadband connectivity.

Which geographical regions are expected to lead market growth in commercial radomes?

The Asia Pacific (APAC) region is expected to lead market growth in commercial radomes due to surging air passenger traffic, significant investments in new aircraft and airport infrastructure, and an expanding satellite communication ecosystem. North America and Europe will continue to be strong markets, driven by technological advancements and fleet modernization efforts, while emerging opportunities are noted in Latin America and the Middle East & Africa.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted