Commercial Jet Engine Market

Commercial Jet Engine Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709065 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

Commercial Jet Engine Market Size

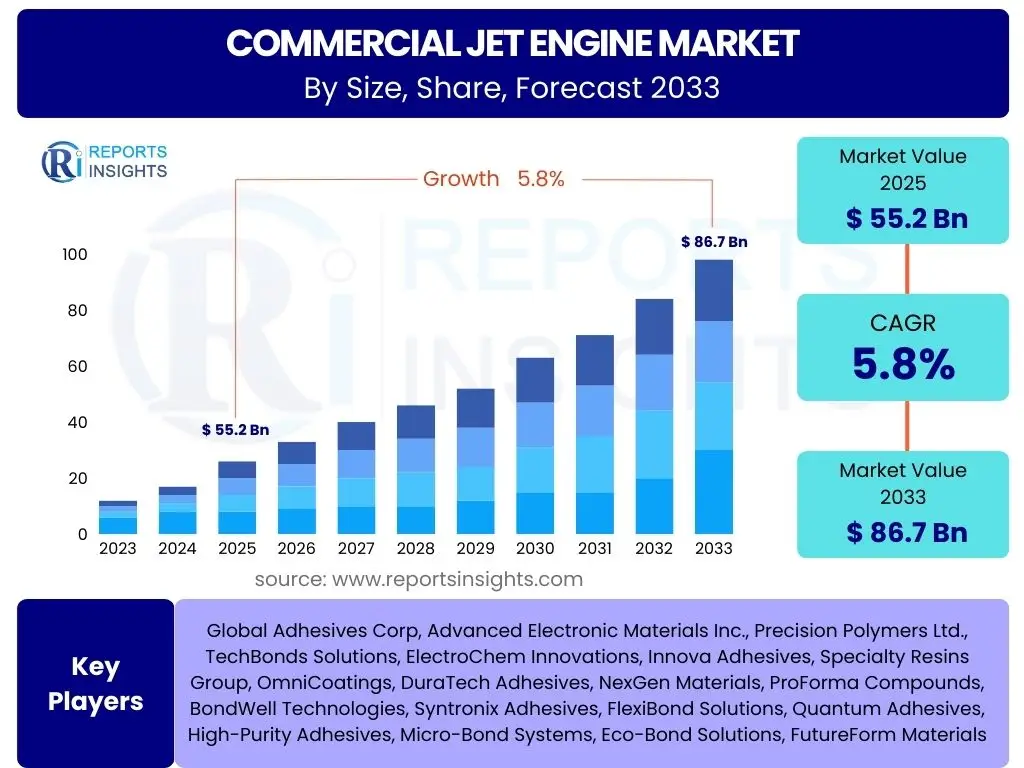

According to Reports Insights Consulting Pvt Ltd, The Commercial Jet Engine Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 55.2 Billion in 2025 and is projected to reach USD 86.7 Billion by the end of the forecast period in 2033. This growth trajectory is underpinned by an anticipated resurgence in global air travel, coupled with ongoing fleet modernization initiatives across major airlines worldwide. The demand for more fuel-efficient and environmentally compliant propulsion systems remains a primary driver, fostering innovation and investment in advanced engine technologies.

Key Commercial Jet Engine Market Trends & Insights

The commercial jet engine market is significantly influenced by global air travel demand, which drives the need for new aircraft and efficient propulsion systems. Key trends reflect an industry-wide push towards sustainability, operational efficiency, and advanced technological integration. Users frequently inquire about the trajectory of engine design in response to climate concerns and the evolving operational requirements of airlines.

Airlines and manufacturers are increasingly focusing on reducing fuel consumption and emissions, leading to the adoption of next-generation engine architectures and materials. This focus is complemented by the ongoing development of maintenance and repair services that leverage predictive analytics to minimize downtime. The shift towards cleaner aviation is not merely a regulatory compliance issue but a fundamental repositioning of market strategy, impacting every stage from conceptual design to end-of-life management.

- Increased adoption of sustainable aviation fuels (SAFs) compatible engines and readiness for future alternative fuels.

- Development of ultra-high bypass ratio turbofan engines for enhanced fuel efficiency and reduced noise.

- Growing emphasis on predictive maintenance, digital twins, and condition-based monitoring systems.

- Advancements in additive manufacturing (3D printing) for complex, lightweight engine components.

- Focus on lightweight materials such as composites and advanced alloys to improve power-to-weight ratio.

- Rise in demand for efficient engines specifically designed for narrow-body aircraft, dominating new aircraft orders.

- Strategic partnerships and collaborations among original equipment manufacturers (OEMs) for technology development and production sharing.

- Integration of advanced data analytics and artificial intelligence for performance optimization and fault detection.

AI Impact Analysis on Commercial Jet Engine

The integration of Artificial Intelligence (AI) across the commercial jet engine lifecycle is fundamentally transforming design, manufacturing, operations, and maintenance. Users frequently inquire about how AI can enhance engine performance, optimize maintenance schedules, and improve fuel efficiency, alongside concerns regarding data security and the complexity of implementation.

AI-driven solutions are expected to significantly reduce operational costs and increase safety margins by enabling proactive issue detection and more precise control systems. This technological shift is also poised to accelerate research and development cycles for next-generation engines, allowing for rapid prototyping and simulation. From smart manufacturing processes that identify defects in real-time to sophisticated algorithms that predict component wear, AI is becoming an indispensable tool for efficiency and reliability in the aviation sector.

- Predictive maintenance and anomaly detection through machine learning algorithms processing sensor data.

- Optimized engine performance and fuel efficiency via real-time data analysis and adaptive control systems.

- Enhanced design and simulation capabilities using AI for faster iteration and material optimization.

- Automated quality control and inspection processes in manufacturing, reducing human error.

- Supply chain optimization for engine parts and logistics management, improving efficiency and reducing lead times.

- Improved troubleshooting and fault isolation with AI-powered diagnostic tools.

- Development of digital twin models for comprehensive lifecycle management and performance monitoring.

- AI-driven optimization of flight paths and engine thrust settings to minimize fuel burn during operation.

Key Takeaways Commercial Jet Engine Market Size & Forecast

Key takeaways from the Commercial Jet Engine market forecast highlight a robust growth trajectory, primarily driven by increasing global passenger traffic and modernization efforts within airline fleets. Stakeholders are particularly interested in the long-term sustainability goals and the financial implications of investing in new engine technologies that meet evolving environmental standards. The market's expansion is intrinsically linked to advancements in fuel efficiency and reduced emissions, positioning these factors as critical determinants of future success and competitive advantage.

The forecast period indicates a sustained demand for propulsion systems that offer operational cost savings alongside superior environmental performance. This necessitates continued significant investment in research and development, particularly in areas such as sustainable aviation fuels compatibility and hybrid-electric technologies. Market participants who can effectively innovate and scale these solutions are expected to capture substantial market share, influencing the competitive landscape. The market remains dynamic, requiring adaptability to global economic shifts and regulatory changes.

- The market is projected for strong growth, largely fueled by the recovery and expansion of global air travel demand.

- Significant capital investment is flowing into research and development of fuel-efficient and environmentally sustainable engine technologies.

- Emerging economies, particularly in the Asia Pacific region, are expected to contribute substantially to new engine demand due to increasing air connectivity.

- There is a long-term strategic focus across the industry on reducing the carbon footprint of aviation through advanced propulsion.

- Technological innovation, particularly in materials science, aerodynamics, and digital integration, is a primary competitive differentiator.

- Increasing demand for aftermarket services, including maintenance, repair, and overhaul (MRO), is a critical revenue stream.

- Strategic alliances and joint ventures are becoming increasingly crucial for sharing development costs and accelerating market penetration for complex technologies.

- Regulatory pressures and government incentives for greener aviation will continue to shape market evolution.

Commercial Jet Engine Market Drivers Analysis

Market drivers for commercial jet engines are primarily influenced by the expanding aviation sector, driven by a surge in passenger and cargo air traffic globally. The worldwide trend towards fleet modernization and replacement of aging aircraft with more fuel-efficient, quieter, and environmentally compliant models significantly propels demand for new engines. This imperative is often dictated by both operational economics and increasingly stringent regulatory frameworks.

Furthermore, the increasing focus on reducing the environmental impact of aviation necessitates the development and adoption of advanced, greener propulsion systems, which stimulates market growth. Airlines are actively seeking engines that can integrate sustainable aviation fuels (SAFs) or are designed for future hybrid-electric or hydrogen power. These factors collectively create a strong impetus for innovation, production, and long-term investment in the jet engine industry, fostering a competitive environment focused on performance and sustainability.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Air Passenger Traffic and Cargo Demand | +1.5-2.0% | Global, especially Asia Pacific, North America | Short to Mid-Term (2025-2030) |

| Fleet Modernization and Replacement Cycles | +1.0-1.5% | North America, Europe, China | Mid-Term (2027-2033) |

| Growing Demand for Fuel-Efficient and Environmentally Friendly Aircraft | +1.2-1.8% | Global, with strong regulatory push in Europe | Long-Term (2028-2033) |

| Advancements in Aviation Technology and Materials Science | +0.8-1.2% | North America, Europe, Japan | Long-Term (2029-2033) |

| Expansion of Low-Cost Carriers (LCCs) and Regional Connectivity | +0.7-1.0% | Emerging Markets, South East Asia, Latin America | Mid-Term (2026-2032) |

Commercial Jet Engine Market Restraints Analysis

The commercial jet engine market faces several significant restraints, including the substantial capital investment required for research, development, and advanced manufacturing of new, more efficient engines. The immense costs associated with developing breakthrough technologies, coupled with the extended certification processes, often pose a barrier to entry and slow down innovation cycles for smaller players. Furthermore, the inherently long lifecycle of aircraft means that fleet replacement is a gradual process, limiting immediate demand spikes.

Strict environmental regulations and emissions standards, while driving innovation, also pose significant challenges by necessitating costly technological upgrades and complex certification processes, which can increase the overall cost of engines. Economic uncertainties, such as inflation, high interest rates, and geopolitical instabilities, can impact airline profitability and, consequently, their aircraft procurement plans, leading to fluctuations in engine demand. Supply chain disruptions, intensified by global events, further compound these issues by affecting production schedules and material availability, contributing to market volatility.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Research, Development, and Certification Costs | -0.8-1.2% | Global | Long-Term (2025-2033) |

| Stringent Environmental Regulations and Emissions Standards | -0.7-1.0% | Europe, North America | Mid to Long-Term (2026-2033) |

| Geopolitical Instability and Economic Uncertainties | -0.5-0.8% | Global, specific conflict zones | Short to Mid-Term (2025-2028) |

| Global Supply Chain Disruptions and Raw Material Price Volatility | -0.4-0.6% | Global | Short to Mid-Term (2025-2029) |

| Long Lifecycle of Aircraft and Slow Fleet Replacement | -0.3-0.5% | Global | Long-Term (2025-2033) |

Commercial Jet Engine Market Opportunities Analysis

Significant opportunities within the commercial jet engine market are emerging from the ongoing development of sustainable aviation fuels (SAFs) and the exploratory phases of hybrid-electric and hydrogen propulsion systems, which promise to redefine future flight. The push towards decarbonization is opening new market segments for innovative engine designs and retrofitting solutions that can meet ambitious net-zero targets. This creates a compelling need for significant investments in new fuel types and engine architectures that can operate efficiently with these alternatives.

The expansion of air travel in emerging economies, particularly in Asia Pacific, Africa, and Latin America, presents new markets for both new engine sales and aftermarket services. As these regions develop their aviation infrastructure and increase connectivity, demand for various aircraft types, from regional jets to wide-body aircraft, is expected to surge. Additionally, the increasing focus on digital integration and data analytics for engine maintenance and performance optimization offers avenues for service innovation, creating recurring revenue streams and enhancing operational efficiency for airlines.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development and Adoption of Sustainable Aviation Fuels (SAFs) | +1.0-1.5% | Global, strong in Europe, North America | Long-Term (2027-2033) |

| Emergence of Hybrid-Electric and Hydrogen Propulsion Technologies | +0.7-1.0% | Europe, North America, Japan | Long-Term (2030-2033) |

| Growth in Emerging Aviation Markets (Asia Pacific, Africa, Latin America) | +0.9-1.3% | Asia Pacific, Africa, Latin America | Mid to Long-Term (2026-2033) |

| Expansion and Digitalization of Maintenance, Repair, and Overhaul (MRO) Services | +0.6-0.9% | Global | Mid-Term (2025-2030) |

| Integration of AI and Data Analytics for Engine Optimization | +0.5-0.8% | North America, Europe | Long-Term (2028-2033) |

Commercial Jet Engine Market Challenges Impact Analysis

The commercial jet engine market grapples with several profound challenges, including the intensive technological demands for achieving ever-higher fuel efficiency, significantly lower emissions, and reduced noise levels. These requirements necessitate continuous, substantial investment in cutting-edge research and development, often pushing the boundaries of material science, aerodynamics, and combustion technology. The complexity of these engineering feats is compounded by the need for rigorous testing and certification, which adds considerable time and cost to product development cycles.

Integrating complex new materials and advanced manufacturing processes, such as additive manufacturing, into mass production requires substantial investment and highly specialized expertise. This not only involves overcoming technical hurdles but also establishing robust quality control and supply chain management for novel components. Maintaining global supply chain resilience in the face of geopolitical tensions, trade disputes, and economic volatility also remains a critical operational hurdle, impacting production schedules, material availability, and cost efficiencies across the entire industry. The scarcity of skilled engineers and technicians specialized in aerospace propulsion further exacerbates these challenges.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Technological Complexity and Integration of New Innovations | -0.6-0.9% | Global | Long-Term (2025-2033) |

| Skilled Workforce Shortage and Talent Gap | -0.4-0.7% | North America, Europe, Asia Pacific | Mid-Term (2026-2031) |

| Intense Competition and Pricing Pressures from Market Players | -0.3-0.6% | Global | Short to Mid-Term (2025-2029) |

| Cybersecurity Risks and Data Integrity for Connected Engines | -0.2-0.4% | Global | Long-Term (2028-2033) |

| Global Economic Slowdowns and Impact on Airline Profitability | -0.5-0.8% | Global | Short-Term (2025-2027) |

Commercial Jet Engine Market - Updated Report Scope

This report offers an exhaustive analysis of the commercial jet engine market, meticulously detailing its size, growth projections, and influential market dynamics. It encompasses a thorough review of key trends, drivers, restraints, opportunities, and challenges shaping the industry landscape. The scope extends to a comprehensive segmentation analysis by engine type, application, and aircraft type, providing regional insights and profiling leading market participants to deliver a holistic view of the market's current state and future outlook.

The detailed analysis aims to equip stakeholders with actionable intelligence for strategic decision-making, covering historical performance from 2019-2023 and providing a robust forecast through 2033. Emphasis is placed on technological advancements, sustainability initiatives, and the competitive environment. Furthermore, the report offers customization options to meet specific research needs, ensuring maximum relevance and utility for a diverse range of industry players and investors.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 55.2 Billion |

| Market Forecast in 2033 | USD 86.7 Billion |

| Growth Rate | 5.8% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | General Electric Company, Rolls-Royce Holdings plc, Safran S.A., Pratt & Whitney (Raytheon Technologies Corporation), MTU Aero Engines AG, Honeywell International Inc., IHI Corporation, CFM International, Engine Alliance, Aviation Industry Corporation of China (AVIC), NPO Saturn, Kawasaki Heavy Industries, Mitsubishi Heavy Industries, Aero Engine Corporation of China (AECC), Williams International |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The commercial jet engine market is broadly segmented based on engine type, application, and the specific aircraft type they are designed to power. This granular segmentation provides a comprehensive understanding of demand patterns, technological requirements, and market dynamics across different aviation sectors. Analyzing these segments helps in identifying specific growth areas, competitive advantages, and tailoring strategies for diverse market needs, from powering efficient narrow-body commercial airliners to large wide-body cargo and passenger aircraft. Each segment is influenced by distinct operational demands and regulatory landscapes.

Further sub-segmentation within these categories allows for a more detailed analysis, distinguishing between different generations of engine technology and their suitability for various operational profiles. For example, turbofan engines are the dominant type for commercial passenger aircraft, but their design varies significantly between narrow-body and wide-body applications. Understanding these distinctions is crucial for manufacturers, airlines, and investors to navigate the complexities of the global market efficiently.

- Engine Type:

- Turbofan: The most common type for commercial jets, offering high thrust and fuel efficiency.

- Turboprop: Primarily used for regional aircraft, emphasizing efficiency at lower altitudes and speeds.

- Others: Includes emerging technologies such as geared turbofans, open rotor concepts, and future hybrid-electric designs.

- Application:

- Commercial Aviation: Engines for passenger transport across various routes.

- Cargo Aviation: Engines designed for freight aircraft, often prioritizing durability and thrust for heavy loads.

- Aircraft Type:

- Narrow-Body Aircraft: Engines for single-aisle jets (e.g., Airbus A320 family, Boeing 737 family), dominating short to medium-haul routes.

- Wide-Body Aircraft: Engines for twin-aisle jets (e.g., Airbus A330, A350, Boeing 777, 787), used for long-haul and high-capacity routes.

- Regional Jets: Engines for smaller aircraft serving regional routes, balancing performance with operational flexibility.

Regional Highlights

The global commercial jet engine market exhibits diverse growth patterns and operational characteristics across different geographical regions. North America and Europe represent mature markets, characterized by extensive fleet modernization programs and significant investments in advanced aerospace research and development. These regions are also at the forefront of implementing stringent environmental regulations, driving demand for innovative, greener engine technologies.

The Asia Pacific region, however, stands out as the fastest-growing market, propelled by rapidly increasing air travel demand, the expansion of new airline ventures, and substantial investments in aviation infrastructure. Emerging economies in Latin America and the Middle East & Africa are also demonstrating robust growth, driven by enhanced regional connectivity, the establishment of new strategic airline hubs, and a rising middle class with increased propensity for air travel. Each region presents unique opportunities and challenges for jet engine manufacturers and service providers.

- North America: A mature market with strong demand for fleet replacement and next-generation engines. It is a hub for R&D in aerospace, driven by major aircraft manufacturers and engine OEMs, with significant emphasis on operational efficiency and technological upgrades.

- Europe: Characterized by a strong focus on environmental regulations and sustainability initiatives. This region is a leader in the development of hybrid-electric and hydrogen propulsion technologies, alongside continuous investment in fuel-efficient turbofan engines to meet strict emissions targets.

- Asia Pacific (APAC): Projected to be the fastest-growing market due to the rapid expansion of air passenger traffic, increasing disposable incomes, and substantial orders for new aircraft from burgeoning airlines. China and India are particularly significant contributors to this growth.

- Latin America: An emerging growth region driven by expanding regional connectivity and increasing air travel. The market here focuses on both new aircraft procurement and the enhancement of existing fleets to improve operational efficiency and serve growing demand.

- Middle East and Africa (MEA): Characterized by strategic hub development and a growing demand for wide-body aircraft and their associated high-thrust engines, particularly in the Middle East. Africa’s aviation sector is also expanding, driven by intra-continental travel and fleet modernization.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Commercial Jet Engine Market.- General Electric Company

- Rolls-Royce Holdings plc

- Safran S.A.

- Pratt & Whitney (Raytheon Technologies Corporation)

- MTU Aero Engines AG

- Honeywell International Inc.

- IHI Corporation

- CFM International

- Engine Alliance

- Aviation Industry Corporation of China (AVIC)

- NPO Saturn

- Kawasaki Heavy Industries

- Mitsubishi Heavy Industries

- Aero Engine Corporation of China (AECC)

- Williams International

Frequently Asked Questions

Analyze common user questions about the Commercial Jet Engine market and generate a concise list of summarized FAQs reflecting key topics and concerns.What factors are driving the growth of the commercial jet engine market?

The market is primarily driven by increasing global air passenger traffic, the ongoing modernization of airline fleets with more fuel-efficient aircraft, and a strong industry-wide focus on sustainable aviation technologies to meet evolving environmental regulations and reduce operational costs.

How is artificial intelligence (AI) impacting commercial jet engine technology?

AI is significantly impacting the commercial jet engine sector by enabling advanced predictive maintenance, optimizing engine performance in real-time through data analytics, enhancing design and simulation processes for new engines, and improving manufacturing quality control, leading to greater efficiency, reliability, and safety across the engine lifecycle.

What are the main challenges faced by the commercial jet engine industry?

Key challenges include the substantial capital investment required for research and development of advanced engine technologies, stringent environmental regulations necessitating costly upgrades, the complexity of integrating new materials and manufacturing processes like additive manufacturing, and maintaining resilient global supply chains amidst geopolitical and economic uncertainties.

Which regions are expected to show the most significant growth in the commercial jet engine market?

The Asia Pacific region is anticipated to exhibit the most substantial growth due to rapidly increasing air travel demand, expanding airline fleets, and developing aviation infrastructure. North America and Europe will also see steady growth driven by fleet modernization and a strong focus on sustainable aviation solutions.

What are the key technological trends shaping the future of jet engines?

Key technological trends include the development of engines compatible with sustainable aviation fuels (SAFs), research into hybrid-electric and hydrogen propulsion systems for ultra-low emissions, the widespread adoption of additive manufacturing for lighter and more complex components, and the integration of digital twin technology for enhanced performance monitoring and predictive maintenance.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted