Cocoa Butter Equivalent Market

Cocoa Butter Equivalent Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706214 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

Cocoa Butter Equivalent Market Size

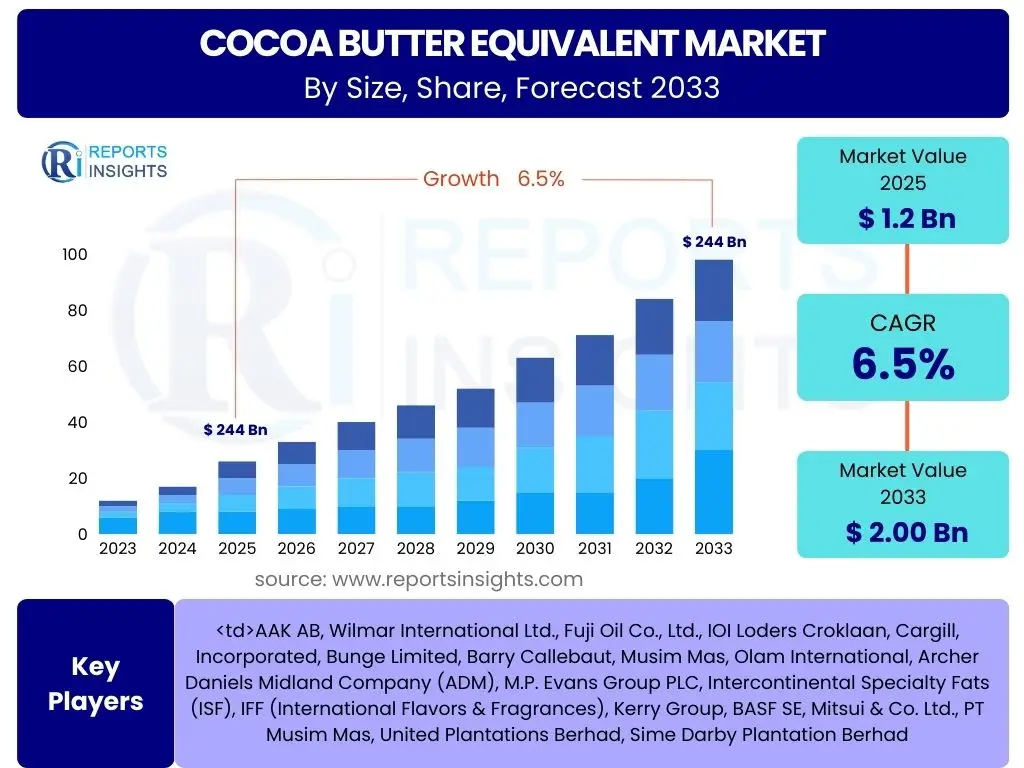

According to Reports Insights Consulting Pvt Ltd, The Cocoa Butter Equivalent Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2025 and 2033. The market is estimated at USD 1.2 Billion in 2025 and is projected to reach USD 2.00 Billion by the end of the forecast period in 2033. This consistent growth trajectory is primarily driven by the escalating demand for cost-effective and functionally versatile alternatives to traditional cocoa butter, particularly within the confectionery and food processing industries. The inherent price volatility of natural cocoa butter, coupled with its finite supply, continues to push manufacturers towards exploring and adopting suitable equivalents.

The market's expansion is further supported by the increasing global consumption of chocolate and related confectionery products, especially in emerging economies where affordability plays a crucial role. As consumer preferences evolve, there is a growing emphasis on products that offer stable sensory profiles and extended shelf life, attributes effectively provided by Cocoa Butter Equivalents (CBEs). The technological advancements in fat processing and modification techniques have also enabled the production of high-quality CBEs that closely mimic the melting properties and texture of natural cocoa butter, thereby broadening their application scope across various food categories.

Key Cocoa Butter Equivalent Market Trends & Insights

Common user inquiries regarding Cocoa Butter Equivalent market trends frequently center on the balance between cost efficiency and product quality, the influence of sustainable sourcing, and the evolving regulatory landscape concerning labeling. Users are keen to understand how manufacturers are addressing consumer demands for natural ingredients while simultaneously managing supply chain complexities and price fluctuations of conventional cocoa butter. There is a discernible interest in the development of plant-based and allergen-free CBEs, reflecting broader dietary shifts and health consciousness. Furthermore, the role of technological innovation in improving the functional properties and sensory attributes of CBEs, making them more indistinguishable from natural cocoa butter, is a recurring theme in user questions, highlighting the industry's continuous pursuit of performance enhancement and market acceptance.

The market for Cocoa Butter Equivalents is significantly shaped by the confectionery industry's relentless pursuit of cost optimization without compromising product integrity. The inherent volatility in cocoa bean prices, often influenced by weather patterns, political stability in key growing regions, and speculative trading, compels chocolate and confectionery manufacturers to seek stable and economically viable alternatives. CBEs offer a compelling solution by providing similar textural and melting characteristics to natural cocoa butter, but at a more predictable and often lower cost, enabling companies to maintain profitability and competitive pricing for their end products. This trend is particularly pronounced in mass-market confectionery segments where price sensitivity is a major factor driving consumer purchasing decisions. Moreover, the consistency in supply of raw materials for CBEs, such as palm oil, shea butter, and sal fat, often mitigates the supply chain risks associated with cocoa, further solidifying their appeal.

Another crucial trend observed in the CBE market is the increasing focus on sustainability and ethical sourcing. As consumers become more aware of the environmental and social impacts of agricultural practices, there is a rising demand for ingredients that are responsibly sourced. This extends to the fats and oils used in CBE production, with a particular emphasis on certified sustainable palm oil (CSPO) and responsibly harvested shea and sal fats. Manufacturers are investing in certifications and transparent supply chains to meet these evolving consumer and regulatory expectations, differentiating their products in a competitive market. Furthermore, advancements in fat fractionation and interesterification technologies are enabling the creation of CBEs with improved functional properties, such as enhanced bloom resistance and better crystallization behavior, which are critical for the quality and shelf stability of chocolate and compound coatings. These technological innovations not only improve product performance but also support the broader industry shift towards more efficient and sustainable production methods, thereby expanding the applicability and market acceptance of CBEs across diverse confectionery and food applications globally.

- Rising demand for cost-effective alternatives to natural cocoa butter due to price volatility.

- Growing emphasis on sustainable and ethically sourced raw materials for CBE production, particularly certified palm oil.

- Technological advancements in fat processing improving the functional and sensory properties of CBEs.

- Increasing adoption of CBEs in confectionery and bakery due to their stable characteristics and extended shelf life.

- Expansion into diverse food applications beyond traditional chocolate, including spreads and frozen desserts.

AI Impact Analysis on Cocoa Butter Equivalent

User queries regarding the impact of Artificial Intelligence (AI) on the Cocoa Butter Equivalent market frequently revolve around its potential to optimize production processes, enhance product quality, and revolutionize supply chain management. Users are interested in how AI could predict raw material price fluctuations, thereby enabling more strategic procurement decisions and mitigating risks associated with supply chain disruptions. There is also significant curiosity about AI's role in the development of novel CBE formulations, particularly in mimicking the complex rheological and sensory profiles of natural cocoa butter more precisely. Furthermore, questions arise concerning the automation of quality control, predictive maintenance of manufacturing equipment, and the use of AI-driven insights for demand forecasting, all of which aim to improve efficiency and reduce operational costs within the CBE production landscape.

AI's influence on the Cocoa Butter Equivalent market extends significantly to optimizing production and R&D processes. Machine learning algorithms can analyze vast datasets from fat processing, including crystallization profiles, melting curves, and fatty acid compositions, to predict optimal blending ratios and processing conditions for desired CBE properties. This not only accelerates product development cycles, allowing manufacturers to quickly adapt to market demands and replicate specific cocoa butter characteristics, but also ensures consistent quality across batches. By precisely controlling parameters such as temperature, pressure, and agitation during interesterification or fractionation, AI-driven systems can minimize waste, improve yield, and enhance the overall efficiency of CBE production, leading to cost savings and increased competitiveness for manufacturers. Furthermore, predictive analytics can identify potential equipment failures or maintenance needs, thereby reducing downtime and ensuring continuous operation in CBE manufacturing facilities.

Beyond internal operations, AI also holds considerable potential for transforming the supply chain and market intelligence within the CBE sector. AI-powered platforms can monitor global commodity markets, weather patterns, and geopolitical events to provide real-time insights into the supply and price volatility of raw materials like palm oil, shea butter, and sal fat. This allows procurement teams to make more informed decisions, hedge against price risks, and secure raw materials more efficiently. Moreover, AI can analyze consumer trends and sales data to forecast demand for confectionery products, enabling CBE producers to align their production schedules with anticipated market needs, thereby optimizing inventory levels and reducing waste. The application of AI in market analysis can also identify emerging application areas or regional growth pockets for CBEs, guiding strategic market entry and investment decisions, ensuring that the industry remains agile and responsive to the dynamic global food landscape.

- AI-driven optimization of CBE production parameters for enhanced yield and consistency.

- Predictive analytics for raw material procurement, mitigating price volatility and supply chain risks.

- AI-assisted formulation of novel CBE blends to precisely mimic natural cocoa butter properties.

- Automation and predictive maintenance of manufacturing equipment, reducing downtime.

- Advanced demand forecasting for confectionery and food applications, optimizing inventory and production.

Key Takeaways Cocoa Butter Equivalent Market Size & Forecast

Common user questions regarding key takeaways from the Cocoa Butter Equivalent market size and forecast frequently highlight the primary drivers of growth, the underlying reasons for its increasing adoption, and the long-term sustainability of the market. Users are keen to understand if the market growth is predominantly driven by economic factors like cocoa price volatility, or if functional advantages and evolving consumer preferences also play a significant role. There is a strong interest in the regional dynamics, particularly which geographies are emerging as key consumption hubs or production centers for CBEs. Furthermore, users often inquire about the future prospects of CBEs in light of growing consumer demand for "clean label" products and the industry's commitment to sustainable sourcing, seeking insights into how these factors will shape the market's trajectory over the forecast period.

A primary takeaway from the Cocoa Butter Equivalent market forecast is its robust growth, fundamentally propelled by the economic necessity for stable and cost-effective fat solutions in the confectionery and food industries. The persistent volatility of natural cocoa butter prices, influenced by unpredictable agricultural yields and global demand fluctuations, consistently positions CBEs as an attractive alternative. Manufacturers are increasingly recognizing CBEs not merely as substitutes but as integral components that offer reliable supply, predictable pricing, and consistent functional properties critical for large-scale production. This reliability ensures sustained profitability and competitive advantage, especially for companies operating in the high-volume segments of the confectionery market, which are highly sensitive to raw material cost fluctuations.

Another significant insight derived from the market analysis is the expanding functional versatility and improving quality of CBEs, which are contributing to their broader acceptance beyond traditional chocolate applications. Advances in lipid technology and processing techniques have enabled CBEs to closely mimic the specific melting profiles, textural attributes, and sensory characteristics of natural cocoa butter, making them suitable for a wider range of products including bakery items, dairy alternatives, and specialty confections. This technological progression addresses consumer and manufacturer demands for high-quality alternatives that do not compromise on the final product's sensory experience. Furthermore, the growing emphasis on sustainable sourcing and ethical production practices within the fats and oils industry, particularly concerning palm and shea, is positively influencing the perception and adoption of CBEs, aligning with global trends towards responsible ingredient procurement and strengthening their market position for the long term.

- Market growth is primarily driven by the need for cost stability and functional consistency amidst natural cocoa butter price volatility.

- Technological advancements are enhancing CBE quality, enabling broader application across confectionery and other food sectors.

- Sustainability initiatives in raw material sourcing (e.g., certified palm oil) are crucial for market acceptance and future growth.

- Emerging economies present significant growth opportunities due to increasing confectionery consumption and price sensitivity.

- The market is adapting to consumer demands for both affordability and responsible sourcing, pushing innovation in CBE formulation.

Cocoa Butter Equivalent Market Drivers Analysis

The Cocoa Butter Equivalent market is primarily driven by the inherent price volatility and supply chain inconsistencies associated with natural cocoa butter. As the global demand for chocolate and confectionery products continues to surge, particularly in developing economies, the pressure on cocoa supply chains intensifies, leading to fluctuating prices. CBEs offer a stable and more predictable cost structure, enabling manufacturers to manage production expenses more effectively and maintain competitive pricing for their finished goods. This economic advantage is a powerful incentive for adoption, especially for large-scale producers.

Beyond economic factors, the functional benefits offered by CBEs are also significant drivers. They provide consistent melting profiles, textural properties, and bloom resistance, which are crucial for the quality and shelf life of chocolate and compound coatings. Manufacturers appreciate the ability of CBEs to maintain product stability and appearance over time, reducing waste and enhancing consumer appeal. Furthermore, the increasing global population and rising disposable incomes, especially in Asia Pacific and Latin America, are fueling the demand for confectionery, indirectly boosting the need for CBEs as key ingredients to meet this expanding market.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Cocoa Butter Price Volatility | +1.5% | Global, particularly Europe & North America (major consumers) | Short to Medium Term (2025-2029) |

| Cost-Effectiveness & Supply Stability | +1.2% | Global, high relevance in emerging APAC & Latin America | Long Term (2025-2033) |

| Functional Superiority (e.g., Bloom Resistance) | +0.8% | Developed markets with high quality standards (Europe, North America) | Medium Term (2027-2031) |

| Growth in Confectionery & Processed Food Industry | +1.0% | Asia Pacific, Latin America, Middle East & Africa | Long Term (2025-2033) |

Cocoa Butter Equivalent Market Restraints Analysis

Despite significant growth drivers, the Cocoa Butter Equivalent market faces notable restraints, primarily centered around consumer perception and regulatory complexities. A substantial segment of consumers, particularly in developed markets, maintains a strong preference for products containing only "natural" cocoa butter, viewing CBEs as inferior or less authentic. This perception can limit market penetration and growth, especially in premium chocolate segments where ingredient purity is a key marketing point. Overcoming this ingrained consumer bias requires extensive education and transparent labeling, which can be challenging and costly for manufacturers.

Another significant restraint comes from the intricate and varied regulatory frameworks governing the use and labeling of CBEs across different regions. Regulations regarding the permissible percentage of CBEs in chocolate, and how these products must be labeled (e.g., "vegetable fat in chocolate," "compound chocolate"), differ considerably from one country to another. This regulatory fragmentation creates barriers to international trade and product standardization, requiring manufacturers to develop region-specific formulations and packaging, which adds to operational complexity and costs. Furthermore, the potential for negative publicity related to the sourcing of raw materials for some CBEs, such as palm oil, due to environmental concerns, can also act as a restraint, prompting companies to invest heavily in sustainable certification and public relations efforts.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Consumer Preference for Natural Cocoa Butter | -0.7% | Europe & North America | Long Term (2025-2033) |

| Complex & Varied Regulatory Landscape | -0.5% | Global, particularly EU and other regulated markets | Long Term (2025-2033) |

| Raw Material Price Volatility (e.g., Palm Oil) | -0.3% | Global, especially Southeast Asia (production) | Short to Medium Term (2025-2029) |

| Competition from Other Specialty Fats | -0.2% | Global | Medium Term (2027-2031) |

Cocoa Butter Equivalent Market Opportunities Analysis

Significant opportunities in the Cocoa Butter Equivalent market arise from the growing consumer demand for plant-based and vegan food products. As more consumers adopt plant-centric diets for health, ethical, or environmental reasons, there is an increasing need for ingredients that align with these preferences. CBEs, derived from various vegetable oils such as shea, palm, sal, and illipe, are inherently plant-based, making them ideal for developing vegan chocolate and confectionery products that require a fat system mimicking cocoa butter's unique melting profile. This trend opens up new market segments and allows manufacturers to cater to a broader consumer base, especially within the rapidly expanding vegan food industry.

Another key opportunity lies in continuous innovation in fat processing technologies to develop next-generation CBEs with enhanced sensory and functional attributes. Research and development efforts are focused on creating CBEs that not only replicate the snap and melt of natural cocoa butter but also offer improved oxidative stability, extended shelf life, and better compatibility with various confectionery ingredients. Furthermore, the development of CBEs from novel or underutilized fat sources could provide new avenues for sustainable and diversified sourcing, reducing reliance on a few primary raw materials and enhancing supply chain resilience. Emerging markets, particularly in Asia Pacific and Latin America, also represent substantial untapped potential, as rising incomes and changing dietary habits in these regions drive an increased demand for affordable and diverse confectionery options, which CBEs are uniquely positioned to fulfill.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Plant-Based & Vegan Food Market | +1.3% | North America, Europe, increasingly Asia Pacific | Long Term (2025-2033) |

| Technological Advancements in Fat Modification | +1.0% | Global, particularly R&D hubs in Europe & North America | Medium to Long Term (2027-2033) |

| Expansion into New Food Applications | +0.9% | Global, diverse food processing industries | Medium Term (2027-2031) |

| Emerging Market Penetration | +1.1% | Asia Pacific, Latin America, Middle East & Africa | Long Term (2025-2033) |

Cocoa Butter Equivalent Market Challenges Impact Analysis

The Cocoa Butter Equivalent market faces significant challenges, notably from a persistent negative consumer perception and labeling complexity. Many consumers perceive CBEs as "less natural" or inferior to pure cocoa butter, especially in markets where premium chocolate commands high value. This perception is often amplified by clean-label trends, where consumers seek products with minimal processing and simple ingredient lists. This public perception can deter market growth, particularly for products aiming for a premium positioning, and necessitates extensive marketing and educational efforts to shift consumer attitudes, which represents a substantial investment for manufacturers.

Another critical challenge is navigating the fluctuating raw material prices and the complexities of sustainable sourcing, particularly for key ingredients like palm oil and shea butter. While CBEs offer stability compared to cocoa, their own raw materials are subject to market volatility, geopolitical events, and environmental concerns such as deforestation and labor practices. Ensuring a stable and ethically sourced supply chain requires robust traceability systems, certifications (e.g., RSPO for palm oil), and continuous engagement with suppliers, which adds significant operational costs and risks. Compliance with diverse and evolving international regulations regarding fat composition in chocolate products and country-specific labeling requirements also presents a complex hurdle for manufacturers aiming for global market reach, forcing them to adapt formulations and packaging for different regions, thereby increasing production complexity and costs.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Negative Consumer Perception & Clean Label Trend | -0.8% | Europe, North America, increasingly Asia Pacific | Long Term (2025-2033) |

| Raw Material Sourcing Sustainability & Ethics | -0.6% | Global, particularly Southeast Asia (palm) & West Africa (shea) | Long Term (2025-2033) |

| Complex Regulatory Compliance & Labeling | -0.4% | Global, varying by specific regional market | Medium to Long Term (2027-2033) |

| Maintaining Sensory Profile & Quality Consistency | -0.3% | Global | Ongoing (2025-2033) |

Cocoa Butter Equivalent Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Cocoa Butter Equivalent market, offering detailed insights into its current size, historical performance, and future growth projections. The scope encompasses a thorough examination of market drivers, restraints, opportunities, and challenges that influence the industry's trajectory. The report also features an exhaustive segmentation analysis by type, application, and form, alongside a detailed regional outlook covering key geographies. Furthermore, it profiles leading market players, offering a competitive landscape view, and includes an AI impact analysis to understand emerging technological influences. This structured approach aims to equip stakeholders with actionable intelligence for strategic decision-making within the dynamic Cocoa Butter Equivalent sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.2 Billion |

| Market Forecast in 2033 | USD 2.00 Billion |

| Growth Rate | 6.5% |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | AAK AB, Wilmar International Ltd., Fuji Oil Co., Ltd., IOI Loders Croklaan, Cargill, Incorporated, Bunge Limited, Barry Callebaut, Musim Mas, Olam International, Archer Daniels Midland Company (ADM), M.P. Evans Group PLC, Intercontinental Specialty Fats (ISF), IFF (International Flavors & Fragrances), Kerry Group, BASF SE, Mitsui & Co. Ltd., PT Musim Mas, United Plantations Berhad, Sime Darby Plantation Berhad |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Cocoa Butter Equivalent market is comprehensively segmented to provide a granular understanding of its diverse components and their respective market dynamics. This segmentation is crucial for identifying specific growth pockets, understanding demand patterns across different product categories, and analyzing the competitive landscape. The market is primarily segmented by type of raw material used, by application in various industries, and by the form in which CBEs are supplied to manufacturers. Each segment reflects unique market drivers, restraints, opportunities, and challenges, influencing their individual growth trajectories within the broader CBE market.

Understanding these segmentations allows stakeholders to pinpoint areas of high growth and potential investment. For instance, the 'By Type' segment differentiates CBEs based on their primary fat source, such as palm oil, shea butter, or sal fat, each offering distinct functional properties and varying levels of sustainability concerns. The 'By Application' segment highlights the diverse end-use industries, with confectionery being the dominant segment, but also noting significant uptake in bakery, dairy, cosmetics, and pharmaceuticals, indicating broadening utility. The 'By Form' segment, categorizing CBEs as solid or liquid, addresses different manufacturing requirements and logistical considerations. This detailed segmentation analysis aids in strategic planning, product development, and market entry strategies for companies operating or looking to enter the Cocoa Butter Equivalent industry.

- By Type:

- Palm Oil-based CBE

- Shea Butter-based CBE

- Sal Fat-based CBE

- Kokum Butter-based CBE

- Illipe Butter-based CBE

- Other Blends

- By Application:

- Confectionery

- Chocolate

- Compound Coatings

- Candies & Chews

- Bakery Products

- Biscuits & Cookies

- Cakes & Pastries

- Fillings & Spreads

- Dairy & Desserts

- Ice Cream Coatings

- Frozen Desserts

- Dairy Analogues

- Cosmetics & Personal Care

- Pharmaceuticals

- Confectionery

- By Form:

- Solid

- Liquid

Regional Highlights

- Europe: Europe represents a significant market for Cocoa Butter Equivalents, driven by its well-established confectionery industry and stringent regulations regarding fat content in chocolate. Countries like Germany, the UK, and France are major consumers of chocolate products, and manufacturers in these regions often utilize CBEs to manage costs and achieve specific textural properties. While regulations on the inclusion of vegetable fats in chocolate vary, the economic advantages and consistent quality offered by CBEs continue to drive their adoption. The region also exhibits a growing focus on sustainable sourcing, particularly for palm oil and shea butter, influencing supplier choices and driving demand for certified CBEs.

- North America: The North American market for Cocoa Butter Equivalents is characterized by a strong demand for confectionery and processed food products, coupled with a pragmatic approach to ingredient sourcing. The United States, in particular, showcases high consumption of chocolate and compound coatings, where CBEs are widely used for their functional benefits such as bloom resistance and extended shelf life, as well as cost stabilization. The emphasis on innovation in food processing and the growing trend towards plant-based ingredients further support the adoption of CBEs in this region. Regulatory environments, while distinct from Europe, also guide the permissible use and labeling of these alternative fats.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing market for Cocoa Butter Equivalents, propelled by rapidly expanding economies, increasing disposable incomes, and a burgeoning middle-class population. Countries like China, India, and Southeast Asian nations are witnessing significant growth in their confectionery and bakery sectors. The demand for affordable chocolate and sweet treats is high, making CBEs an attractive ingredient solution for local and international manufacturers aiming to cater to this price-sensitive yet high-volume market. Furthermore, the region is a major producer of key raw materials for CBEs, such as palm oil, ensuring supply chain efficiency and cost advantages.

- Latin America: Latin America is experiencing robust growth in the confectionery market, contributing to the rising demand for Cocoa Butter Equivalents. Countries such as Brazil, Mexico, and Argentina exhibit strong domestic consumption of chocolate and related products. The need for cost-effective fat solutions that can withstand varying climatic conditions and ensure product stability is a key driver for CBE adoption in this region. Local manufacturers are increasingly integrating CBEs to optimize production costs and expand their product offerings across different price points, catering to diverse consumer segments.

- Middle East and Africa (MEA): The MEA region presents emerging opportunities for the Cocoa Butter Equivalent market. Growth is fueled by increasing urbanization, Westernization of dietary patterns, and rising disposable incomes, leading to a higher consumption of confectionery. While the market is currently smaller compared to other regions, its high growth potential is noteworthy. The reliance on imported finished goods and ingredients, coupled with a growing local food manufacturing base, drives the demand for versatile and economically viable ingredients like CBEs to meet the expanding consumer base and establish competitive domestic industries.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Cocoa Butter Equivalent Market.- AAK AB

- Wilmar International Ltd.

- Fuji Oil Co., Ltd.

- IOI Loders Croklaan

- Cargill, Incorporated

- Bunge Limited

- Barry Callebaut

- Musim Mas

- Olam International

- Archer Daniels Midland Company (ADM)

- M.P. Evans Group PLC

- Intercontinental Specialty Fats (ISF)

- IFF (International Flavors & Fragrances)

- Kerry Group

- BASF SE

- Mitsui & Co. Ltd.

- PT Musim Mas

- United Plantations Berhad

- Sime Darby Plantation Berhad

- IOI Corporation Berhad

Frequently Asked Questions

What is Cocoa Butter Equivalent (CBE)?

Cocoa Butter Equivalent (CBE) is a type of vegetable fat that possesses similar physical and chemical properties to natural cocoa butter, particularly its sharp melting profile and texture. CBEs are derived from various non-lauric vegetable oils such as shea butter, palm oil, sal fat, kokum butter, and illipe butter. They are primarily used in the confectionery industry to replace a portion of or all of the more expensive and supply-volatile natural cocoa butter, while maintaining the desired mouthfeel and consistency of chocolate products.

Why is Cocoa Butter Equivalent used in chocolate and confectionery?

Cocoa Butter Equivalent is primarily used in chocolate and confectionery to address the high cost and price volatility of natural cocoa butter, ensuring more stable production costs. Additionally, CBEs offer consistent functional properties such as a sharp melting point, which contributes to the characteristic 'snap' and smooth melt-in-mouth texture of chocolate, along with good bloom resistance, which helps maintain product appearance and shelf life, especially in varying temperature conditions.

What are the primary types of raw materials used for CBEs?

The primary types of raw materials used for Cocoa Butter Equivalents (CBEs) include palm oil fractions (such as palm mid-fractions), shea butter, sal fat, kokum butter, and illipe butter. These fats are selected for their unique fatty acid compositions and melting profiles, which can be modified through processes like fractionation and interesterification to closely mimic the physical characteristics of natural cocoa butter, allowing them to be blended or used individually to achieve desired confectionery properties.

What are the key market trends influencing the CBE industry?

Key market trends influencing the Cocoa Butter Equivalent industry include the increasing demand for cost-effective alternatives to natural cocoa butter due to its price volatility and supply constraints. There is also a significant trend towards sustainable and ethically sourced raw materials, particularly for palm and shea-based CBEs. Furthermore, technological advancements in fat processing are leading to improved functional properties and sensory profiles of CBEs, broadening their application beyond traditional confectionery into other food categories and plant-based products.

What are the regulatory considerations for using CBEs in food products?

Regulatory considerations for using Cocoa Butter Equivalents (CBEs) in food products vary significantly by region. In the European Union, specific regulations permit the use of up to 5% non-cocoa vegetable fats (including CBEs) in chocolate products, provided they are clearly labeled. Other regions, such as the United States, have different labeling requirements and standards for products containing vegetable fats instead of or in addition to cocoa butter. Manufacturers must comply with these diverse national and international food standards regarding composition, processing, and allergen declarations to ensure market access and consumer transparency.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted