CO2 Production Plant Market

CO2 Production Plant Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709691 | Last Updated : December 12, 2025 |

Format : ![]()

![]()

![]()

![]()

CO2 Production Plant Market Size

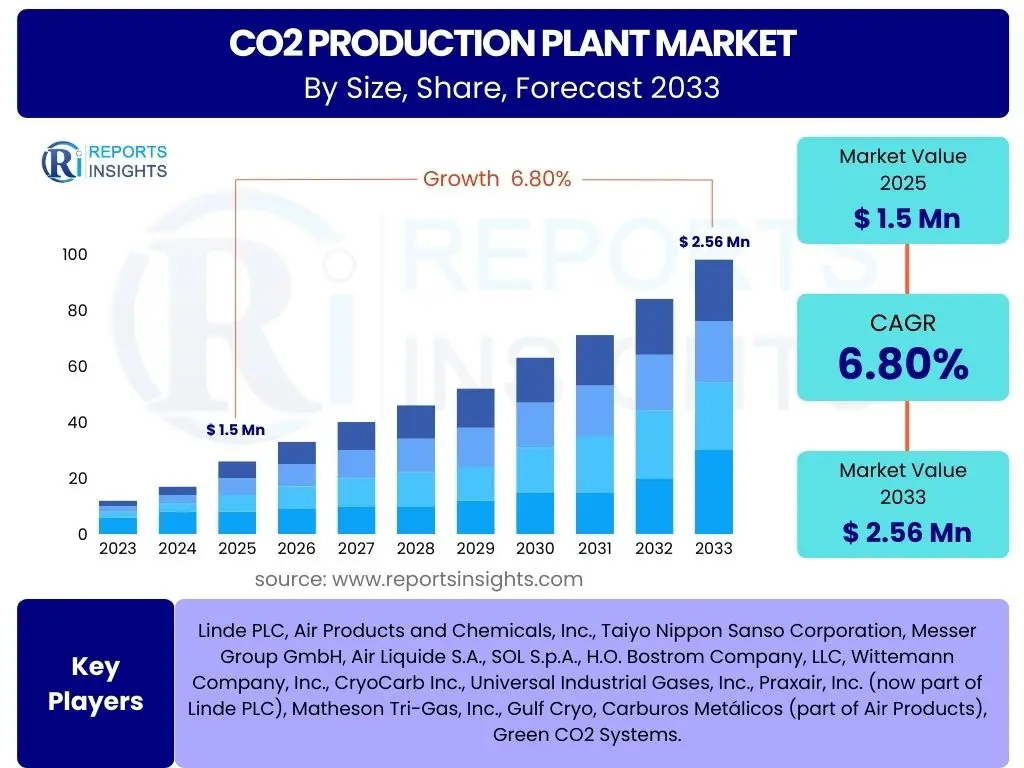

According to Reports Insights Consulting Pvt Ltd, The CO2 Production Plant Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 1.5 billion in 2025 and is projected to reach USD 2.56 billion by the end of the forecast period in 2033.

Key CO2 Production Plant Market Trends & Insights

The CO2 Production Plant market is currently experiencing dynamic shifts driven by increasing industrial demand, environmental regulations, and technological advancements. Key insights indicate a strong movement towards more efficient and sustainable CO2 capture and purification technologies. Users frequently inquire about the integration of carbon capture, utilization, and storage (CCUS) technologies, the rising demand for high-purity CO2 across various sectors, and the impact of global decarbonization efforts on market growth. There is a clear interest in understanding how these trends will influence investment opportunities and operational strategies for CO2 production facilities.

Another significant trend revolves around the diversification of CO2 sources. While industrial by-products remain a primary source, interest in direct air capture (DAC) and biomass-derived CO2 is growing, albeit still in nascent stages for large-scale production. The market is also witnessing an emphasis on modular and scalable plant designs to cater to varied industrial capacities and geographical demands. This shift is critical for enabling distributed CO2 production and reducing transportation costs, which are significant components of the overall CO2 supply chain.

- Increasing adoption of Carbon Capture, Utilization, and Storage (CCUS) technologies.

- Growing demand for high-purity CO2 in diverse end-use industries such as food & beverage, healthcare, and chemicals.

- Focus on energy-efficient and cost-effective CO2 production processes.

- Emergence of modular and scalable CO2 plant designs.

- Diversification of CO2 sources beyond traditional industrial by-products, including direct air capture (DAC).

- Stringent environmental regulations driving demand for CO2 capture solutions.

- Technological advancements in purification and liquefaction processes.

AI Impact Analysis on CO2 Production Plant

Users frequently express curiosity about how Artificial Intelligence (AI) can revolutionize the CO2 Production Plant sector, focusing on areas like operational efficiency, predictive maintenance, and process optimization. The general expectation is that AI will play a pivotal role in enhancing the reliability and cost-effectiveness of these complex facilities. Specific concerns often relate to the implementation challenges, data security, and the return on investment for integrating AI solutions into existing infrastructure. There is a strong user interest in practical applications and case studies demonstrating tangible benefits.

AI's influence is anticipated to extend across the entire lifecycle of a CO2 production plant, from initial design and engineering to ongoing operations and maintenance. By leveraging advanced algorithms and machine learning, plant operators can achieve real-time monitoring, anomaly detection, and optimization of energy consumption and feedstock utilization. This not only leads to significant operational savings but also contributes to improved safety records and reduced environmental footprints, aligning with broader sustainability goals within the industry. The adoption of AI is still in its early stages but is rapidly gaining traction as companies seek competitive advantages.

- Optimization of plant operational parameters for enhanced efficiency and yield.

- Predictive maintenance schedules for critical equipment, reducing downtime and operational costs.

- Real-time monitoring and control of CO2 capture, purification, and liquefaction processes.

- Improved energy management and consumption reduction through AI-driven insights.

- Enhanced safety protocols through anomaly detection and risk assessment.

- Automated fault diagnosis and troubleshooting for faster resolution of issues.

- Data-driven decision-making for supply chain optimization and resource allocation.

Key Takeaways CO2 Production Plant Market Size & Forecast

Common user questions regarding market size and forecast for CO2 production plants often center on understanding the primary growth drivers, the impact of emerging technologies, and the long-term sustainability of demand. The key takeaway is a market poised for steady growth, underpinned by non-discretionary industrial demand and the increasing imperative for carbon management. Users are particularly interested in how regulatory frameworks and global sustainability initiatives will influence the market trajectory and potential investment returns over the forecast period.

The market's resilience is evident in the diverse applications of CO2, ranging from food and beverage to advanced manufacturing and carbon sequestration. While initial capital expenditure remains a consideration, the operational efficiencies gained through modern plant designs and process improvements are attracting sustained investment. The forecast indicates that regional disparities in growth will largely be influenced by local industrial development, energy policies, and the maturity of environmental regulations, making a nuanced regional analysis critical for stakeholders.

- Steady market expansion driven by consistent industrial demand and environmental mandates.

- Significant investment opportunities in new plant construction and technology upgrades.

- Diverse application portfolio of CO2 ensures market stability and broad growth potential.

- Regional growth influenced by industrialization, energy policies, and regulatory landscapes.

- Technological advancements in capture and purification are critical for market competitiveness.

- Growing emphasis on sustainable CO2 sourcing and utilization strategies.

- Forecasted growth highlights the essential role of CO2 production in modern economies.

CO2 Production Plant Market Drivers Analysis

The global CO2 Production Plant market is significantly propelled by the escalating demand for carbon dioxide across various industries, coupled with stringent environmental regulations pushing for industrial decarbonization. The food and beverage sector, in particular, requires high-purity CO2 for carbonation, packaging, and refrigeration, while the medical industry uses it for diagnostic and therapeutic purposes. Industrial applications, such as welding, water treatment, and chemical synthesis, also contribute substantially to demand. This consistent and diversified consumption base forms a robust foundation for market expansion.

Furthermore, the increasing global emphasis on climate change mitigation and the development of carbon capture, utilization, and storage (CCUS) technologies are acting as powerful drivers. Governments and industries worldwide are investing in solutions to capture CO2 from large point sources, such as power plants and industrial facilities, which then requires processing and purification in CO2 production plants. This dual impetus of industrial necessity and environmental responsibility creates a favorable environment for sustained market growth and innovation.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand from Food & Beverage Industry | +1.5% | North America, Europe, Asia Pacific | Short to Medium Term (2025-2029) |

| Expanding Industrial Applications (Welding, Chemical) | +1.2% | Asia Pacific, Latin America, Middle East | Medium Term (2026-2031) |

| Increasing Adoption of CCUS Technologies | +1.8% | Europe, North America, Japan | Medium to Long Term (2027-2033) |

| Medical and Pharmaceutical Sector Demand | +0.8% | Global | Short to Medium Term (2025-2030) |

| Governmental Regulations and Incentives for Decarbonization | +1.0% | Europe, North America, China | Medium to Long Term (2026-2033) |

CO2 Production Plant Market Restraints Analysis

Despite the positive growth outlook, the CO2 Production Plant market faces several significant restraints that could impede its expansion. One primary challenge is the high capital expenditure required for establishing new CO2 production and purification facilities. The initial investment includes the cost of advanced capture technologies, compression units, liquefaction systems, storage tanks, and elaborate distribution networks, which can be prohibitive for smaller players or in regions with limited access to financing. This high entry barrier often leads to market consolidation among larger, well-established industrial gas companies.

Another critical restraint is the energy-intensive nature of CO2 capture and processing. Technologies such as amine-based absorption, while effective, require substantial energy input for regeneration, leading to high operational costs and a potentially larger carbon footprint if the energy source is fossil-fuel based. The fluctuating energy prices can significantly impact the profitability of these plants, making long-term financial planning challenging. Additionally, the complex logistics and infrastructure required for safe CO2 transportation and storage also present considerable hurdles, particularly for remote industrial sources or end-users.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Expenditure for Plant Setup | -1.2% | Global, particularly developing regions | Short to Medium Term (2025-2030) |

| Energy-Intensive Capture and Purification Processes | -1.0% | Global, especially regions with high energy costs | Short to Long Term (2025-2033) |

| Complex Logistics and Infrastructure for CO2 Transport | -0.8% | Remote areas, cross-border operations | Medium Term (2026-2032) |

| Fluctuating Raw Material (Source Gas) Availability and Purity | -0.5% | Specific industrial hubs | Short Term (2025-2028) |

| Public Perception and Regulatory Hurdles for Carbon Storage | -0.7% | North America, Europe | Long Term (2028-2033) |

CO2 Production Plant Market Opportunities Analysis

Significant opportunities are emerging within the CO2 Production Plant market, primarily driven by advancements in CO2 utilization technologies and the increasing demand for green CO2. The development of new applications for captured CO2, such as its use as a feedstock for producing synthetic fuels, polymers, and building materials, is creating entirely new revenue streams for producers. This circular economy approach to carbon management not only reduces emissions but also adds value to a previously considered waste product. Such innovations are attracting substantial research and development investments and fostering new partnerships across industries.

Furthermore, the global push for sustainability and the concept of carbon neutrality are opening avenues for the adoption of more sustainable CO2 sourcing methods, including direct air capture (DAC) and bioenergy with carbon capture and storage (BECCS). While these technologies are currently expensive, ongoing research and economies of scale are expected to drive down costs, making them viable long-term solutions. Regions with abundant renewable energy resources are particularly well-positioned to capitalize on these trends, producing low-carbon or negative-carbon CO2. The market also presents opportunities for modular and decentralized CO2 production units, especially in developing economies where large-scale centralized infrastructure may not be feasible.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Advancements in CO2 Utilization Technologies (CCU) | +1.3% | Global, R&D hubs | Medium to Long Term (2027-2033) |

| Emergence of Direct Air Capture (DAC) Solutions | +1.1% | North America, Europe, Australia | Long Term (2029-2033) |

| Growing Demand for Sustainable/Green CO2 | +0.9% | Europe, North America | Medium Term (2026-2031) |

| Development of Modular and Decentralized Plant Solutions | +0.7% | Developing economies, remote industrial sites | Short to Medium Term (2025-2030) |

| Strategic Partnerships and Collaborations for Project Development | +0.6% | Global | Short to Medium Term (2025-2029) |

CO2 Production Plant Market Challenges Impact Analysis

The CO2 Production Plant market faces several significant challenges that can hinder its full potential. One of the primary hurdles is the high energy consumption and associated operational costs of CO2 capture and purification processes. While demand for CO2 is robust, making the production process economically viable, especially under fluctuating energy prices, remains a critical challenge. This economic pressure often requires advanced technological solutions that are not always readily accessible or affordable for all market participants, particularly in regions with less developed industrial infrastructure.

Another major challenge involves the scalability and integration of advanced CO2 capture technologies with existing industrial facilities. Retrofitting older plants with new carbon capture units can be technically complex, disruptive to operations, and entail substantial capital investment. Furthermore, the development of a comprehensive CO2 transport and storage infrastructure is still in its nascent stages in many parts of the world. Without reliable pipelines, shipping, or long-term geological storage solutions, the full benefits of CO2 capture cannot be realized, limiting market growth and increasing logistical complexities for producers and users alike.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Energy Consumption & Operational Costs | -1.1% | Global, particularly energy-intensive industries | Short to Long Term (2025-2033) |

| Lack of Comprehensive CO2 Transport & Storage Infrastructure | -0.9% | Developing regions, landlocked countries | Medium to Long Term (2027-2033) |

| Technological Barriers for Cost-Effective Capture at Scale | -0.7% | Global | Medium Term (2026-2031) |

| Regulatory Uncertainty and Evolving Policy Landscape | -0.6% | Emerging markets | Short to Medium Term (2025-2030) |

| Competition from Alternative Technologies/Sourcing | -0.4% | Specific application segments | Short Term (2025-2028) |

CO2 Production Plant Market - Updated Report Scope

This report provides an in-depth analysis of the global CO2 Production Plant market, encompassing a detailed examination of market size, growth trends, and future projections. It delves into the factors driving market expansion, significant restraints impeding growth, and the emerging opportunities and challenges that will shape the industry landscape. The scope includes a thorough segmentation analysis by source, technology, application, and end-use, offering granular insights into the market dynamics. Furthermore, the report presents a comprehensive regional outlook and profiles key market players, aiding stakeholders in making informed strategic decisions and identifying growth avenues within the CO2 production ecosystem.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.5 billion |

| Market Forecast in 2033 | USD 2.56 billion |

| Growth Rate | 6.8% CAGR |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Linde PLC, Air Products and Chemicals, Inc., Taiyo Nippon Sanso Corporation, Messer Group GmbH, Air Liquide S.A., SOL S.p.A., H.O. Bostrom Company, LLC, Wittemann Company, Inc., CryoCarb Inc., Universal Industrial Gases, Inc., Praxair, Inc. (now part of Linde PLC), Matheson Tri-Gas, Inc., Gulf Cryo, Carburos Metálicos (part of Air Products), Green CO2 Systems. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The CO2 Production Plant market is meticulously segmented to provide a granular understanding of its diverse components and drivers. These segments are primarily based on the source of CO2, the technologies employed for capture and purification, the specific applications of the produced CO2, and the end-use industries that consume it. This multi-dimensional segmentation allows for a detailed analysis of market dynamics, growth potential, and competitive landscapes across various niches within the industry, enabling stakeholders to identify precise investment opportunities and strategic focus areas.

- By Source: This segment includes Industrial By-products (such as those from Ammonia, Ethanol, Hydrogen, and other chemical processes), Flue Gas (from Power Generation, Cement, and Steel Production), Biogenic Sources (like Fermentation and Biomass Combustion), and Direct Air Capture.

- By Technology: Key technologies include Absorption (e.g., Amine Scrubbing, Physical Solvents), Adsorption (e.g., Pressure Swing Adsorption (PSA), Temperature Swing Adsorption (TSA)), Membrane Separation, Cryogenic Distillation, and Direct Air Capture Technology.

- By Application: Major applications comprise Food & Beverage (for carbonation and preservation), Industrial Gases (for welding, metal fabrication, fire suppression), Medical & Pharmaceutical (for therapeutics and diagnostics), Chemical Feedstock (for Urea production, Methanol synthesis, Enhanced Oil Recovery (EOR), Polymers), Water Treatment, Agriculture (greenhouse enrichment), and others.

- By End-Use Industry: This categorizes demand from sectors such as Food & Beverage, Chemicals, Healthcare, Oil & Gas, Agriculture, Metal & Mining, Wastewater Treatment, and others.

Regional Highlights

- North America: This region demonstrates robust growth, driven by an advanced industrial base, significant investments in CCUS technologies, and high demand from the food & beverage and oil & gas sectors. The United States and Canada are leading with strong regulatory support for carbon management.

- Europe: Europe is at the forefront of decarbonization efforts, with stringent environmental policies and substantial funding for carbon capture and utilization projects. Countries like Germany, the UK, and Norway are key players, particularly in exploring sustainable CO2 sources and utilization.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing market, fueled by rapid industrialization, increasing demand for CO2 in diverse applications (especially food & beverage and chemicals), and growing environmental awareness in economies such as China, India, and Japan.

- Latin America: This region shows steady growth, primarily due to expanding industrial activities and increasing demand from the food & beverage sector. Brazil and Mexico are emerging markets with potential for new CO2 production facilities.

- Middle East and Africa (MEA): The MEA region is witnessing growth driven by investments in the oil & gas sector (particularly for EOR applications) and the development of new industrial hubs. Saudi Arabia and UAE are significant contributors to the regional market.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the CO2 Production Plant Market.- Linde PLC

- Air Products and Chemicals, Inc.

- Taiyo Nippon Sanso Corporation

- Messer Group GmbH

- Air Liquide S.A.

- SOL S.p.A.

- H.O. Bostrom Company, LLC

- Wittemann Company, Inc.

- CryoCarb Inc.

- Universal Industrial Gases, Inc.

- Praxair, Inc.

- Matheson Tri-Gas, Inc.

- Gulf Cryo

- Carburos Metálicos

- Green CO2 Systems

Frequently Asked Questions

Analyze common user questions about the CO2 Production Plant market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is a CO2 production plant?

A CO2 production plant is an industrial facility designed to capture, purify, and often liquefy carbon dioxide from various sources, making it suitable for commercial and industrial applications. These plants typically employ technologies like absorption, adsorption, or cryogenic distillation to separate CO2 from other gases and process it to required purity levels.

What are the primary applications of CO2 produced by these plants?

CO2 produced from these plants has diverse applications, including carbonation in the food and beverage industry, inerting and welding in industrial manufacturing, medical therapies and diagnostics, chemical feedstock for products like urea and methanol, enhanced oil recovery (EOR), and agricultural applications such as greenhouse enrichment.

What are the main sources of CO2 for production plants?

CO2 production plants source carbon dioxide from various origins, including industrial by-products from processes like ammonia or ethanol production, flue gas from power generation and cement plants, biogenic sources such as fermentation, and increasingly, direct air capture technologies.

How do environmental regulations impact the CO2 Production Plant market?

Environmental regulations significantly influence the market by driving the demand for carbon capture technologies from industrial emitters. Policies aimed at decarbonization and carbon neutrality create incentives for industries to capture CO2, which then needs processing in production plants, thereby boosting market growth and innovation.

What are the key technological advancements in CO2 production?

Key technological advancements include more energy-efficient capture methods (e.g., advanced amine solvents), improved purification techniques, modular plant designs for scalability, and the development of direct air capture (DAC) and various carbon utilization (CCU) technologies that transform captured CO2 into valuable products.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted