Clot Management Device Market

Clot Management Device Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700079 | Last Updated : July 22, 2025 |

Format : ![]()

![]()

![]()

![]()

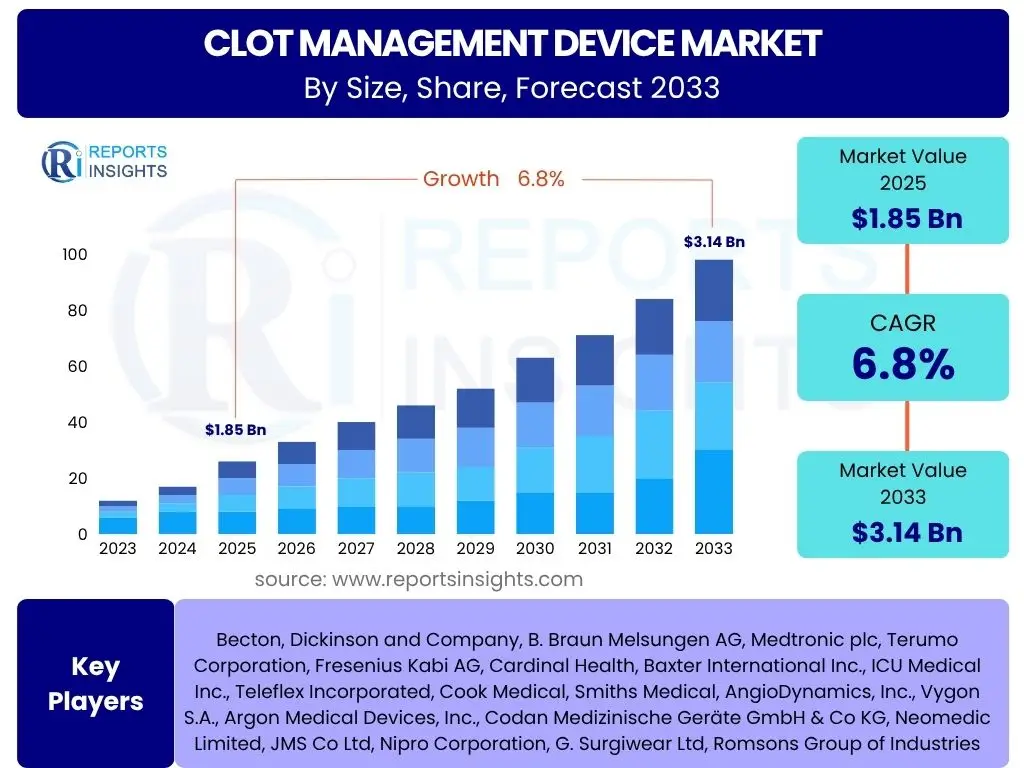

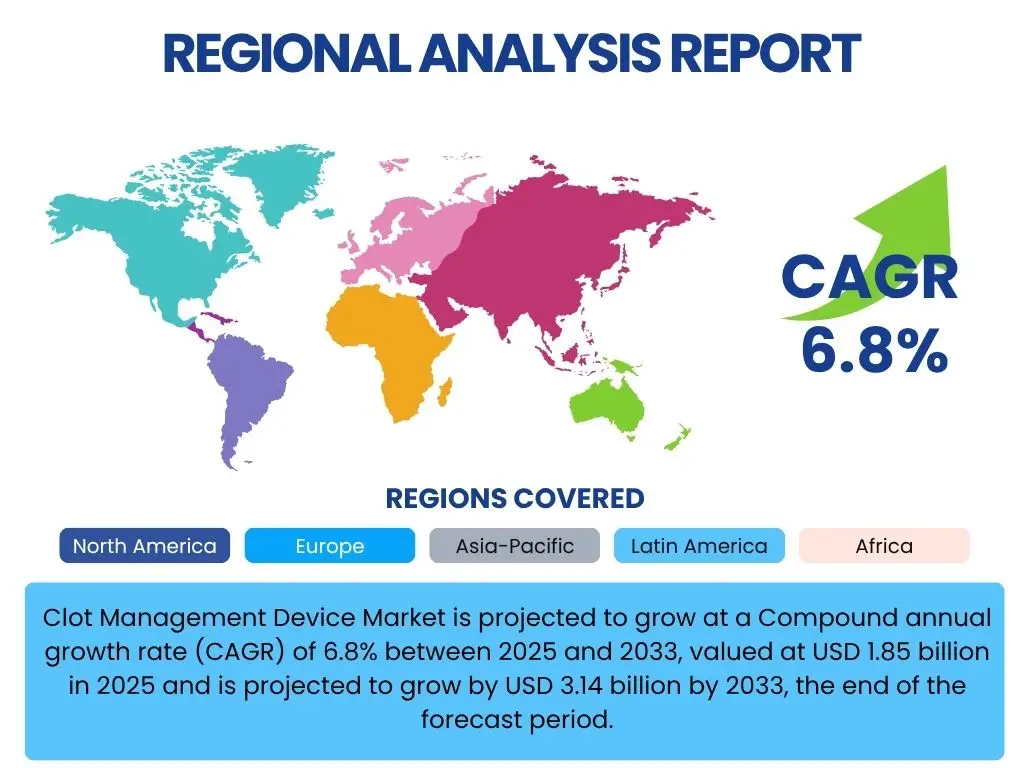

Clot Management Device Market is projected to grow at a Compound annual growth rate (CAGR) of 6.8% between 2025 and 2033, valued at USD 1.85 billion in 2025 and is projected to grow by USD 3.14 billion by 2033, the end of the forecast period.

Key Clot Management Device Market Trends & Insights

The clot management device market is undergoing significant transformation, driven by an increasing global burden of thrombotic disorders and continuous technological advancements. Key trends shaping this industry include the growing adoption of minimally invasive procedures, a shift towards more sophisticated and patient-friendly devices, and the integration of artificial intelligence for enhanced diagnostic accuracy and treatment planning. The market is also witnessing a surge in demand for retrievable inferior vena cava (IVC) filters and advanced mechanical thrombectomy devices, fueled by their improved safety profiles and clinical efficacy. Furthermore, increasing awareness campaigns regarding early diagnosis and management of venous thromboembolism (VTE) and arterial clots are contributing to higher adoption rates of these critical medical devices. The expansion of healthcare infrastructure in emerging economies and rising healthcare expenditure are also pivotal factors influencing market dynamics and opening new avenues for growth and innovation.

- Rising prevalence of cardiovascular diseases and neurological conditions.

- Technological advancements leading to more efficient and safer devices.

- Growing preference for minimally invasive surgical procedures.

- Increasing aging population susceptible to thrombotic events.

- Expansion of healthcare infrastructure and accessibility in developing regions.

AI Impact Analysis on Clot Management Device

Artificial intelligence (AI) is poised to revolutionize the clot management device market by enhancing diagnostic capabilities, optimizing treatment pathways, and improving patient outcomes. AI algorithms can analyze complex imaging data, such as CT scans and MRIs, with greater speed and accuracy than traditional methods, enabling earlier and more precise detection of clots. This predictive analytics capability assists clinicians in identifying patients at high risk of thrombotic events, allowing for proactive intervention. Furthermore, AI can aid in the development of smarter devices, integrating real-time data for adaptive device performance and personalized treatment strategies. From guiding interventional procedures with enhanced precision to monitoring post-treatment recovery and predicting potential complications, AI's influence is expanding across the entire care continuum, promising more effective and safer clot management solutions.

- Enhanced diagnostic accuracy and speed through AI-powered image analysis.

- Optimized treatment planning and personalized interventions via predictive analytics.

- Development of smart, adaptive clot management devices.

- Improved patient monitoring and early detection of complications.

- Streamlined clinical workflows and reduced procedure times.

Key Takeaways Clot Management Device Market Size & Forecast

- The global clot management device market is projected for substantial growth, reflecting increasing demand for effective thrombotic interventions.

- Anticipated to reach USD 3.14 billion by 2033, demonstrating a robust Compound Annual Growth Rate (CAGR) of 6.8% from 2025 to 2033.

- Market expansion is significantly driven by the rising incidence of cardiovascular, neurological, and peripheral vascular diseases globally.

- Technological innovations in thrombectomy, embolectomy, and IVC filters are key contributors to market value appreciation.

- North America and Europe currently dominate the market, attributed to advanced healthcare infrastructure and high adoption rates of novel therapies.

- Asia Pacific is expected to exhibit the fastest growth, propelled by improving healthcare access, increasing medical tourism, and a large patient pool.

- Minimally invasive procedures are gaining traction, influencing product development and market dynamics towards safer and more efficient devices.

- Strategic collaborations, mergers, and acquisitions among market players are prevalent, aiming to expand product portfolios and regional presence.

Clot Management Device Market Drivers Analysis

The clot management device market is propelled by a confluence of factors that underscore its critical role in modern healthcare. A primary driver is the escalating global burden of thrombotic disorders, including deep vein thrombosis (DVT), pulmonary embolism (PE), ischemic stroke, and myocardial infarction. These conditions necessitate prompt and effective intervention, driving demand for advanced clot management solutions. Alongside this, continuous advancements in medical device technology have led to the development of more sophisticated, efficient, and safer devices, such as next-generation mechanical thrombectomy systems and retrievable IVC filters, which enhance clinical outcomes and reduce procedure times. Furthermore, the demographic shift towards an aging global population, who are inherently more susceptible to developing blood clots, significantly contributes to market expansion. Increased awareness among both healthcare professionals and patients regarding the importance of early diagnosis and treatment of thrombotic events also plays a crucial role in fostering market growth. Finally, supportive reimbursement policies in developed economies and a growing emphasis on improving healthcare infrastructure worldwide are creating a favorable environment for the adoption of these life-saving devices.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Prevalence of Thrombotic Disorders: The rising incidence of conditions like DVT, PE, ischemic stroke, and myocardial infarction globally directly fuels the demand for effective clot management solutions. Lifestyle changes, comorbidities, and an aging population contribute to this growing patient pool. | +1.8% | Global, particularly North America, Europe, Asia Pacific | Long-term (2025-2033) |

| Technological Advancements in Devices: Continuous innovation in device design, materials, and mechanisms (e.g., advanced stent retrievers, aspiration catheters, bioresorbable filters) leads to improved efficacy, safety, and minimally invasive options, driving their adoption. | +1.5% | North America, Europe, Japan, Emerging Economies (adoption) | Mid-to-Long term (2025-2033) |

| Growing Aging Population: Elderly individuals are at a higher risk of developing blood clots due to age-related physiological changes, immobility, and increased prevalence of chronic diseases, leading to a larger patient base requiring clot management. | +1.2% | Global, especially Japan, Europe, North America | Long-term (2025-2033) |

| Rising Awareness and Early Diagnosis: Increased public and professional awareness about thrombotic conditions, coupled with improved diagnostic techniques, results in earlier detection and intervention, expanding the treated patient population. | +1.0% | Developed Countries, steadily increasing in Emerging Markets | Mid-to-Long term (2025-2033) |

| Favorable Reimbursement Policies and Healthcare Infrastructure Development: Supportive reimbursement frameworks in key markets reduce out-of-pocket costs for patients and providers, encouraging procedure adoption. Expanding healthcare facilities in developing regions also broadens access. | +0.8% | North America, Western Europe, gradually in parts of Asia Pacific | Mid-to-Long term (2025-2033) |

Clot Management Device Market Restraints Analysis

Despite robust growth drivers, the clot management device market faces several significant restraints that could impede its full potential. A primary limiting factor is the high cost associated with advanced clot management devices and the interventional procedures they enable. These expenses can be prohibitive for patients in regions with limited insurance coverage or for healthcare systems operating under stringent budget constraints, particularly in developing economies. Furthermore, the inherent risks and potential complications associated with these invasive procedures, such as vessel damage, hemorrhage, or device migration, can deter both clinicians and patients, leading to a more cautious approach to adoption. Stringent regulatory approval processes, especially in major markets like the U.S. and Europe, impose lengthy and costly development cycles for new devices, delaying market entry and innovation. Lastly, a critical shortage of skilled healthcare professionals specialized in performing complex interventional procedures for clot management in certain regions can limit the widespread accessibility and utilization of these advanced devices, regardless of their availability.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of Devices and Procedures: The significant capital investment required for advanced clot management devices and the high cost of interventional procedures can limit affordability and accessibility, particularly in price-sensitive markets or regions with limited healthcare budgets. | -1.5% | Global, more pronounced in Emerging Economies | Long-term (2025-2033) |

| Risk of Complications Associated with Procedures: Despite advancements, interventional clot management procedures carry inherent risks such as bleeding, vessel perforation, infection, or device-related complications, leading to a cautious approach among patients and clinicians. | -1.0% | Global | Mid-to-Long term (2025-2033) |

| Stringent Regulatory Approvals: The rigorous and time-consuming regulatory approval processes, especially for novel devices in major markets, delay product launches and increase development costs, potentially stifling innovation and market entry. | -0.8% | North America (FDA), Europe (MDR), Japan | Mid-term (2025-2029) |

| Lack of Skilled Professionals and Infrastructure: A shortage of trained interventional cardiologists, neurologists, and specialized support staff, along with inadequate cath lab infrastructure in some regions, limits the widespread adoption and utilization of advanced devices. | -0.7% | Developing Economies, rural areas in Developed Countries | Long-term (2025-2033) |

Clot Management Device Market Opportunities Analysis

The clot management device market is ripe with opportunities that promise to redefine its trajectory and expand its reach. A significant avenue for growth lies in the increasing focus on minimally invasive procedures. These techniques offer numerous benefits, including reduced patient recovery times, lower complication rates, and shorter hospital stays, aligning with modern healthcare trends and patient preferences. Consequently, there is an escalating demand for devices specifically designed for these less intrusive interventions. Furthermore, the vast, largely untapped potential of emerging markets, particularly in Asia Pacific, Latin America, and parts of the Middle East and Africa, represents a substantial opportunity. These regions are experiencing rapid economic growth, improving healthcare infrastructure, and a rising prevalence of target diseases, creating a fertile ground for market penetration. The continuous development of next-generation devices, incorporating advanced materials, smart features, and improved navigation capabilities, also presents a lucrative opportunity to capture market share through superior product offerings. Lastly, the integration of telemedicine and remote patient monitoring solutions, especially for post-procedure follow-up and long-term anticoagulation management, offers a chance to enhance patient care continuity and expand the application scope of clot management strategies.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of Minimally Invasive Procedures: The shift towards less invasive surgical and interventional techniques drives demand for compatible clot management devices, offering benefits like reduced patient trauma, shorter recovery, and lower healthcare costs. | +1.7% | Global, especially Developed Countries | Mid-to-Long term (2025-2033) |

| Untapped Emerging Markets: Significant growth potential exists in developing economies due to improving healthcare infrastructure, rising disposable incomes, increasing awareness, and a large underserved patient population for thrombotic disorders. | +1.5% | Asia Pacific, Latin America, Middle East & Africa | Long-term (2025-2033) |

| Development of Next-Generation Devices: Innovation in smart devices with integrated imaging, AI-assisted navigation, robotic guidance, and advanced material science creates new market segments and expands clinical applications, offering superior outcomes. | +1.3% | North America, Europe, Japan, China | Mid-to-Long term (2025-2033) |

| Telemedicine and Remote Patient Monitoring Integration: Expanding use of telehealth for pre-procedural assessment, post-procedural follow-up, and chronic anticoagulation management offers new avenues for patient engagement and continuum of care, potentially increasing device usage through better adherence and monitoring. | +0.9% | Developed Countries primarily, growing interest in developing regions | Mid-term (2025-2029) |

Clot Management Device Market Challenges Impact Analysis

The clot management device market, despite its promising outlook, must navigate several formidable challenges that could constrain its growth and widespread adoption. Intense competition among market players is a significant hurdle, leading to pricing pressures and potentially hindering profitability and investment in research and development for smaller companies. The complex and often fragile global supply chains for medical devices pose another challenge, as disruptions stemming from geopolitical events, natural disasters, or pandemics can severely impact product availability and timely delivery, affecting patient care. Furthermore, ethical considerations and patient safety remain paramount; any perceived or actual issues with device efficacy, long-term complications, or recalls can severely erode physician and patient trust, leading to a decline in adoption. Finally, with the increasing connectivity of medical devices, data security and patient privacy concerns are emerging as critical challenges. Safeguarding sensitive health information from cyber threats and ensuring compliance with evolving data protection regulations adds complexity and cost to device development and deployment.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Competition and Pricing Pressure: The presence of numerous global and regional players leads to aggressive competition, potentially driving down prices and impacting profit margins, which can stifle innovation and market entry for new players. | -1.2% | Global, especially competitive in North America and Europe | Mid-to-Long term (2025-2033) |

| Supply Chain Disruptions: Geopolitical instability, global health crises, and raw material shortages can disrupt manufacturing and distribution, leading to product delays or unavailability, impacting market growth and patient access. | -0.9% | Global | Short-to-Mid term (2025-2027), potentially recurring |

| Ethical Considerations and Patient Safety: Maintaining the highest standards of patient safety and addressing ethical concerns related to device usage, long-term efficacy, and potential complications are crucial. Any adverse events or recalls can significantly impact market confidence. | -0.8% | Global, subject to regulatory scrutiny | Ongoing |

| Data Security and Privacy Concerns: With the increasing integration of smart and connected devices, safeguarding patient data from cyber threats and ensuring compliance with stringent data protection regulations (e.g., GDPR, HIPAA) presents a complex and evolving challenge. | -0.6% | Developed Countries with strict data laws | Ongoing |

Clot Management Device Market - Updated Report Scope

This comprehensive market research report delves into the intricate dynamics of the global Clot Management Device Market, offering a robust analysis of its current landscape and future growth trajectories. The study provides critical insights into market size, growth drivers, restraints, opportunities, and challenges, meticulously segmented by device type, application, end-user, and technology. It presents a detailed competitive analysis, profiling key market players and their strategic initiatives, alongside an in-depth regional assessment highlighting key trends and growth pockets across major geographies. Leveraging a blend of primary and secondary research methodologies, the report aims to equip stakeholders with actionable intelligence for informed decision-making and strategic planning within this vital medical device sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.85 Billion |

| Market Forecast in 2033 | USD 3.14 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Medtronic, Boston Scientific Corporation, Johnson & Johnson, Terumo Corporation, Edwards Lifesciences, Teleflex Incorporated, Getinge AB, Penumbra Inc, Inari Medical Inc, Argon Medical Devices Inc, AngioDynamics, Spectranetics Corporation, Stryker, Abbott, Vascular Solutions Inc, Cardiva Medical Inc, InspireMD Inc, Clotbust Systems, Thrombovision, MicroVention Inc |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Clot Management Device Market is meticulously segmented to provide a granular view of its diverse components and understand the varied demands across different healthcare settings and patient needs. This comprehensive segmentation allows for a precise analysis of growth opportunities, competitive landscapes, and regional market behaviors. Understanding these segments is crucial for stakeholders to tailor their strategies, optimize product development, and target specific market niches effectively. Each segment reflects unique drivers, technological preferences, and end-user requirements, contributing distinctly to the overall market valuation and future trajectory. The breakdown covers device types, the specific medical applications where these devices are utilized, the primary end-users of these devices, and the underlying technological principles.

- By Device Type: This segment categorizes clot management devices based on their mechanism of action and design, offering a clear picture of product preferences and technological adoption.

- Mechanical Thrombectomy Devices: These devices are designed to physically remove blood clots from vessels.

- Aspiration Devices: These devices use suction to remove fresh blood clots. They are often preferred for their speed and ability to clear large clot burdens, particularly in acute ischemic stroke cases. Their usage is increasing due to improved catheter designs and suction power.

- Stent Retrievers: Employing a self-expanding stent-like structure, these devices ensnare and retrieve blood clots. They are highly effective in recanalizing occluded vessels, especially in large vessel occlusion strokes, leading to significant neurological improvement. Their efficacy has made them a cornerstone in neurovascular interventions.

- Other Mechanical Thrombectomy Devices: This sub-segment includes various other tools such as fragmentation devices, rotational thrombectomy devices, or rheolytic thrombectomy systems designed for specific clot characteristics or anatomical locations. They offer alternative or complementary approaches to clot removal, broadening treatment options for complex cases.

- Embolism Protection Devices: These devices are deployed to prevent distal embolization of debris during interventional procedures, particularly in angioplasty and stenting procedures in carotid or peripheral arteries. They act as a safeguard against stroke or other embolic complications by capturing dislodged plaque or thrombi, ensuring patient safety.

- Catheters: Essential tools used to access and navigate through the vasculature for diagnostic or therapeutic purposes, often used in conjunction with other clot management devices.

- Balloon Catheters: Used to dilate stenosed vessels, these catheters can also be employed to occlude a vessel temporarily during clot removal procedures to prevent distal embolization, or for aspiration-assisted thrombectomy.

- Guiding Catheters: Providing support and a pathway for other interventional devices (like stent retrievers or aspiration catheters) to reach the target vessel, these catheters are crucial for precise and stable device delivery in complex anatomies.

- Filters: Devices designed to capture and prevent blood clots from traveling to vital organs like the lungs, primarily used in patients with contraindications to anticoagulant therapy or those who fail such therapy.

- Inferior Vena Cava (IVC) Filters: Placed in the inferior vena cava to prevent pulmonary embolism by trapping clots originating from the lower extremities or pelvic veins.

- Retrievable Filters: Designed for temporary placement, these filters can be removed once the risk of pulmonary embolism has subsided or the patient can resume anticoagulant therapy, minimizing long-term complications associated with permanent implants.

- Permanent Filters: Intended for lifelong implantation, these are used in patients with chronic, high risk of pulmonary embolism who cannot receive or tolerate anticoagulation indefinitely.

- Inferior Vena Cava (IVC) Filters: Placed in the inferior vena cava to prevent pulmonary embolism by trapping clots originating from the lower extremities or pelvic veins.

- Dilators: Used to create or enlarge an opening or passageway in anatomical structures, particularly to facilitate the insertion of larger devices or sheaths into blood vessels. They ensure smooth and safe access for complex procedures.

- Snares: Wire loop devices used to retrieve foreign bodies, fragments of catheters, or migrated devices from within the vascular system. They offer a non-surgical option for retrieving misplaced or broken medical components.

- Other Clot Management Devices: This broad category includes niche devices or emerging technologies such as specialized guidewires, access sheaths, or adjunctive tools that support various clot management procedures, catering to specific clinical needs not covered by the primary categories.

- Mechanical Thrombectomy Devices: These devices are designed to physically remove blood clots from vessels.

- By Application: This segment examines where clot management devices are predominantly used, reflecting the prevalence of specific thrombotic diseases across different medical specialties.

- Cardiology: Encompasses devices used in conditions like myocardial infarction (heart attack) and other cardiac-related thrombotic events, including interventions for coronary artery blockages and atrial appendage occlusion.

- Neurology: Focuses on devices critical for treating acute ischemic stroke caused by blood clots in cerebral arteries. This is a rapidly growing segment due to increased awareness and advancements in neuro-interventional techniques.

- Peripheral Vascular: Includes devices used for conditions affecting arteries and veins outside the heart and brain, such as deep vein thrombosis (DVT), pulmonary embolism (PE), and peripheral arterial disease (PAD).

- Oncology: Addresses the management of blood clots that frequently occur in cancer patients due to the disease itself, chemotherapy, or prolonged immobility. Devices here are used to manage cancer-associated thrombosis.

- Other Applications: Covers miscellaneous applications such as clot management in renal dialysis patients, trauma-induced thrombosis, or other rare thrombotic conditions.

- By End-user: This segmentation highlights the primary settings where clot management procedures are performed, indicating infrastructure requirements and patient flow.

- Hospitals: The largest end-user segment, comprising general hospitals, university hospitals, and specialized medical centers equipped with advanced cath labs and operating rooms capable of performing complex interventional procedures.

- Ambulatory Surgical Centers (ASCs): Increasingly adopting less complex clot management procedures, especially for peripheral vascular interventions, due to their cost-effectiveness and patient convenience.

- Specialty Clinics: Including cardiology clinics, neurology clinics, and vascular clinics that offer diagnostic services and sometimes outpatient procedures related to clot management.

- Diagnostic Centers: Facilities primarily focused on imaging and diagnostic services that aid in the detection and characterization of blood clots, guiding subsequent treatment decisions.

- Other End-users: This may include emergency medical services (EMS) for initial stabilization and transport, or home care settings for long-term management of conditions like DVT with portable devices.

- By Technology: This segment delineates the fundamental approach used by the devices to manage clots, showcasing the evolution from traditional methods to advanced mechanical interventions.

- Mechanical Thrombectomy: Involves the physical removal of clots using devices like aspiration catheters, stent retrievers, or rotational devices. This is a dominant and rapidly growing technology due to its immediate efficacy, especially in acute ischemic stroke.

- Pharmacological Thrombectomy (device-assisted): Refers to the use of clot-dissolving drugs (thrombolytics) delivered directly to the clot site, often assisted by specialized catheters or infusion devices for targeted drug delivery, enhancing efficacy and minimizing systemic side effects.

- Filtration: Encompasses the use of filters, predominantly IVC filters, to prevent blood clots from reaching the lungs, thereby preventing pulmonary embolism. This technology focuses on prophylaxis rather than direct clot removal.

- Other Technologies: Includes a range of adjunctive or emerging technologies such as image-guided systems, interventional ultrasound, or electromagnetic navigation systems that enhance the precision, safety, and efficiency of clot management procedures.

Regional Highlights

The global clot management device market exhibits significant regional variations in terms of adoption rates, technological advancements, and market growth, reflecting diverse healthcare infrastructures, disease prevalence, and regulatory environments. Understanding these regional dynamics is crucial for market players to tailor their strategies and capitalize on emerging opportunities.

- North America: This region stands as the largest and most mature market for clot management devices. Its dominance is attributed to a high prevalence of cardiovascular and neurological disorders, well-established healthcare infrastructure, favorable reimbursement policies, and early adoption of advanced medical technologies. The presence of key market players, high R&D investments, and extensive public awareness campaigns about thrombotic conditions also contribute significantly to its leading position. The United States, in particular, drives a substantial portion of this market due owing to its high healthcare expenditure and advanced interventional cardiology and neurology practices.

- Europe: The European market for clot management devices is robust, characterized by a sophisticated healthcare system, increasing aging population, and a strong emphasis on patient safety and innovative therapies. Western European countries like Germany, France, and the UK are key contributors, benefiting from advanced medical research, a high incidence of chronic diseases, and supportive government initiatives for healthcare modernization. However, stringent regulatory frameworks and healthcare budget constraints in some nations can pose challenges. The region is also a hub for medical device innovation, consistently introducing new and improved devices.

- Asia Pacific (APAC): Positioned as the fastest-growing region in the clot management device market, APAC offers immense growth opportunities. This growth is fueled by a burgeoning patient population, improving healthcare infrastructure, rising disposable incomes, and increasing awareness about thrombotic disorders. Countries like China, India, and Japan are at the forefront of this expansion. While Japan represents a mature market with advanced technologies, China and India are emerging as critical markets due to their large underserved populations, increasing medical tourism, and growing investments in healthcare facilities. The region is also witnessing a shift towards adopting advanced Western medical technologies and practices.

- Latin America: This region is experiencing steady growth in the clot management device market, driven by improving economic conditions, expanding healthcare access, and a rising prevalence of non-communicable diseases. Countries such as Brazil, Mexico, and Argentina are key markets, investing in healthcare infrastructure development and adopting advanced medical devices. However, challenges related to affordability, uneven distribution of healthcare facilities, and regulatory complexities can impact the pace of market expansion.

- Middle East and Africa (MEA): The MEA region is an evolving market for clot management devices, primarily driven by increasing healthcare expenditure, a rising burden of chronic diseases, and a growing emphasis on specialized medical care. The Gulf Cooperation Council (GCC) countries, particularly Saudi Arabia and UAE, are leading the adoption due to significant investments in modernizing healthcare facilities and attracting medical tourism. Challenges include lower awareness levels, limited healthcare infrastructure in some sub-regions, and dependence on imports for advanced devices.

Top Key Players:

The market research report covers the analysis of key stake holders of the Clot Management Device Market. Some of the leading players profiled in the report include -:- Medtronic

- Boston Scientific Corporation

- Johnson & Johnson

- Terumo Corporation

- Edwards Lifesciences

- Teleflex Incorporated

- Getinge AB

- Penumbra Inc

- Inari Medical Inc

- Argon Medical Devices Inc

- AngioDynamics

- Spectranetics Corporation

- Stryker

- Abbott

- Vascular Solutions Inc

- Cardiva Medical Inc

- InspireMD Inc

- Clotbust Systems

- Thrombovision

- MicroVention Inc

Frequently Asked Questions:

What are clot management devices and why are they important?

Clot management devices are specialized medical instruments used to diagnose, prevent, and treat blood clots within the vascular system. These devices are crucial for managing life-threatening conditions such as deep vein thrombosis (DVT), pulmonary embolism (PE), and ischemic stroke, where timely and effective intervention can prevent severe complications, minimize organ damage, and significantly improve patient outcomes and survival rates. Their importance stems from their ability to physically remove clots or prevent their migration, offering a direct therapeutic approach.

What are the key growth drivers for the clot management device market?

The clot management device market is primarily driven by the increasing global prevalence of thrombotic disorders, including heart attacks and strokes, which necessitate immediate intervention. Continuous advancements in medical device technology, leading to more efficient and minimally invasive devices, also significantly fuel market growth. Furthermore, a growing aging population, who are at a higher risk of developing blood clots, along with rising awareness and improved diagnostic capabilities, contribute substantially to the market's expansion.

What are the major types of clot management devices?

The major types of clot management devices include mechanical thrombectomy devices, such as aspiration devices and stent retrievers, designed for physical clot removal. Also prominent are embolism protection devices, which prevent clot fragments from traveling, and various types of catheters, including balloon and guiding catheters, used for access and support. Additionally, filters, particularly Inferior Vena Cava (IVC) filters (both retrievable and permanent), are crucial for preventing pulmonary embolism by trapping clots.

Which regions offer significant opportunities in the clot management device market?

While North America and Europe currently dominate the clot management device market due to advanced healthcare infrastructure and high adoption rates, the Asia Pacific region presents the most significant growth opportunities. This is attributed to its large and aging population, rapidly improving healthcare infrastructure, increasing healthcare expenditure, and a rising awareness of thrombotic disorders. Latin America and parts of the Middle East and Africa also show promising growth potential as their healthcare systems continue to develop and expand access to modern medical technologies.

How is AI impacting clot management devices?

Artificial intelligence is profoundly impacting the clot management device market by enhancing diagnostic accuracy through advanced image analysis for clot detection and characterization. AI-powered algorithms aid in optimizing treatment planning by predicting patient response and tailoring interventions. Furthermore, AI contributes to the development of smarter, more precise devices by enabling real-time feedback and navigation during procedures, ultimately improving the safety and efficacy of clot management interventions and leading to better patient outcomes.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted