Cladding System Equipment Market

Cladding System Equipment Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_710206 | Last Updated : December 30, 2025 |

Format : ![]()

![]()

![]()

![]()

Cladding System Equipment Market Size

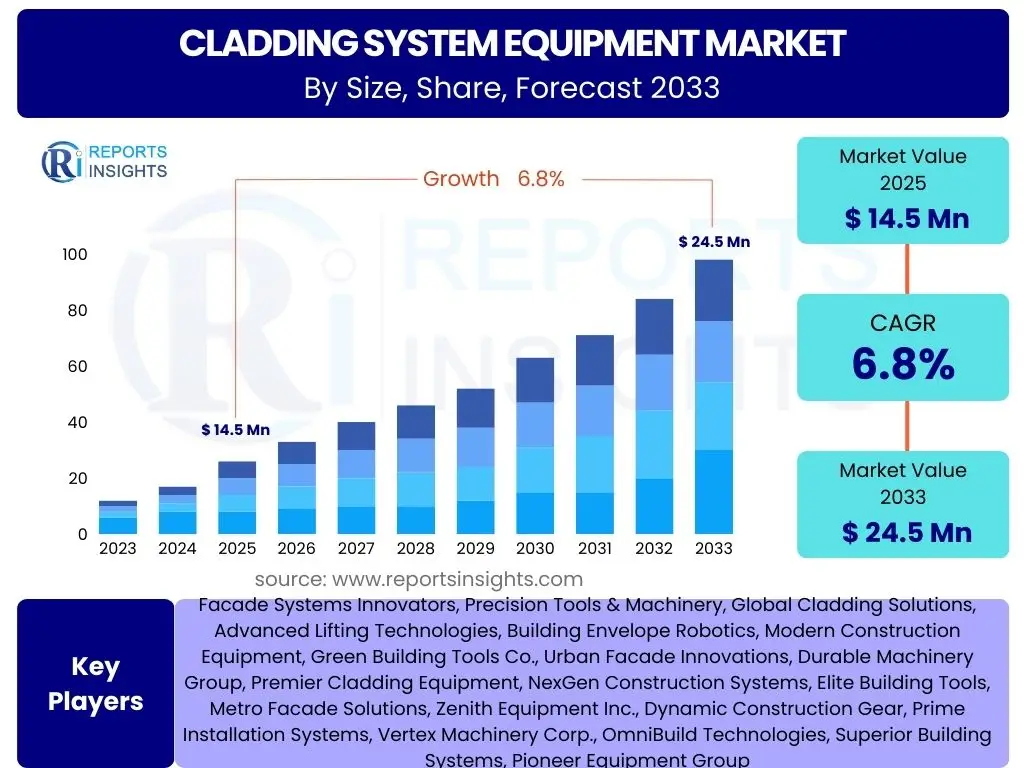

According to Reports Insights Consulting Pvt Ltd, The Cladding System Equipment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 14.5 billion in 2025 and is projected to reach USD 24.5 billion by the end of the forecast period in 2033. This substantial growth is primarily driven by increasing global construction activities, a rising demand for energy-efficient building solutions, and the ongoing development of innovative cladding materials and installation technologies. The market's expansion reflects a global shift towards sustainable and aesthetically pleasing architectural designs, necessitating advanced and efficient equipment for facade construction and renovation.

The consistent growth trajectory indicates a robust market environment, supported by both new construction projects and extensive renovation endeavors across residential, commercial, and industrial sectors. Emerging economies, in particular, are witnessing rapid urbanization and infrastructure development, which significantly contributes to the demand for cladding system equipment. Furthermore, stringent building codes and evolving architectural preferences for durable, low-maintenance, and visually appealing exteriors are compelling developers and contractors to adopt sophisticated cladding solutions, thereby fueling the demand for specialized installation and maintenance machinery.

Key Cladding System Equipment Market Trends & Insights

User inquiries frequently highlight emerging patterns in material innovation, automation in installation processes, and the increasing focus on sustainability and performance. These questions revolve around understanding how new technologies and shifting industry priorities are reshaping the landscape of cladding system equipment. The core interest lies in identifying trends that promise greater efficiency, safety, and environmental responsibility within facade construction, directly impacting operational strategies and investment decisions across the value chain.

A significant trend observed is the growing adoption of modular and prefabricated cladding systems, which necessitate specialized equipment for efficient handling, lifting, and installation. This approach minimizes on-site labor, reduces waste, and accelerates project timelines, aligning with modern construction demands for speed and precision. Another key insight is the increasing integration of smart technologies, such as sensors for monitoring structural integrity and energy performance, into cladding systems, requiring equipment capable of precise placement and connectivity. The emphasis on high-performance materials, including advanced composites and sustainable options, also drives demand for tools designed for specific material properties and installation requirements.

- Modular and Prefabricated Systems: Increased demand for equipment supporting off-site fabrication and rapid on-site assembly, improving project timelines and reducing labor costs.

- Automation and Robotics: Growing use of automated lifting, positioning, and fastening systems to enhance safety, precision, and efficiency in cladding installation.

- Sustainable Materials: Focus on equipment compatible with eco-friendly cladding materials, such as recycled composites and bio-based panels, driven by environmental regulations and green building initiatives.

- Smart Facade Integration: Development of tools for installing cladding systems that incorporate intelligent features like sensors for energy management and structural health monitoring.

- Enhanced Safety Standards: Introduction of equipment designed with advanced safety features to comply with stricter industry regulations and protect on-site workers.

- Digitalization and BIM Integration: Use of Building Information Modeling (BIM) for precise planning and coordination, influencing the design and functionality of specialized equipment.

AI Impact Analysis on Cladding System Equipment

Common user questions regarding AI's impact on cladding system equipment often center on its potential to revolutionize design, manufacturing, and installation processes. Stakeholders are keen to understand how artificial intelligence can contribute to predictive maintenance, optimize material usage, enhance safety protocols, and streamline complex project management. There is a general expectation that AI will lead to more intelligent, efficient, and autonomous operations within the cladding industry, addressing long-standing challenges related to precision, waste, and labor shortages.

AI's influence is increasingly evident in the design and planning phases of cladding projects. AI-powered software can optimize panel layouts, minimize material waste, and identify potential installation challenges before construction begins, leading to significant cost savings and improved efficiency. In manufacturing, AI contributes to quality control by analyzing production data and identifying defects, ensuring higher standards for cladding components. For equipment itself, AI is enabling predictive maintenance, where sensors on machinery collect data analyzed by AI to anticipate failures, schedule maintenance, and reduce downtime, thereby extending the lifespan and reliability of the equipment. This intelligent approach enhances overall operational efficiency and safety across the cladding system lifecycle.

- Predictive Maintenance: AI algorithms analyze equipment performance data to forecast maintenance needs, reducing unplanned downtime and extending machinery lifespan.

- Optimized Design and Material Usage: AI-powered software optimizes cladding panel layouts and material cutting patterns, minimizing waste and improving cost efficiency.

- Automated Quality Control: AI vision systems detect defects in cladding materials during manufacturing and installation, ensuring higher quality standards.

- Enhanced Project Management: AI assists in scheduling, resource allocation, and risk assessment for cladding projects, leading to more efficient execution.

- Robotics and Automation Integration: AI enables autonomous operation and navigation for robotic cladding installation equipment, improving precision and safety.

- Safety Monitoring: AI systems monitor work sites for potential hazards and worker safety, issuing alerts and improving overall site safety protocols.

Key Takeaways Cladding System Equipment Market Size & Forecast

User queries frequently focus on understanding the core implications of the market's growth trajectory and its future potential. They aim to distill the most critical insights regarding investment opportunities, market stability, and the long-term viability of engaging in this sector. The emphasis is on discerning actionable information that can guide strategic planning and capitalize on the projected expansion of the cladding system equipment market, particularly given the strong CAGR and significant market value increase by 2033.

The market is poised for robust expansion, driven by foundational shifts in global construction practices towards sustainability and advanced building aesthetics. Investors and industry players should recognize the sustained demand for high-performance and energy-efficient building envelopes, which will continue to fuel innovation in cladding materials and installation equipment. The projected growth from USD 14.5 billion to USD 24.5 billion signifies a resilient market with substantial opportunities for new entrants and existing players to innovate, expand their product portfolios, and penetrate emerging regional markets. Strategic investments in automation, modular construction techniques, and sustainable equipment solutions will be crucial for capturing market share and ensuring long-term competitiveness in this evolving landscape.

- Significant Market Expansion: The market is projected to grow substantially from USD 14.5 billion in 2025 to USD 24.5 billion by 2033, indicating strong investment potential.

- Sustainable Growth Drivers: Key drivers include increasing construction activity, focus on energy efficiency, and demand for advanced, aesthetic building solutions.

- Technological Integration is Key: Adoption of automation, AI, and digital tools will be critical for efficiency, safety, and competitive advantage.

- Emerging Market Opportunities: Rapid urbanization and infrastructure development in developing regions will contribute significantly to market growth.

- Focus on Product Innovation: Continuous innovation in equipment for specialized materials and modular construction methods will be essential for market leadership.

Cladding System Equipment Market Drivers Analysis

The growth of the cladding system equipment market is fundamentally underpinned by several powerful macroeconomic and industry-specific drivers. These include the global surge in construction activities, particularly in residential and commercial sectors, fueled by urbanization and population growth. Additionally, increasing awareness and stringent regulations regarding building energy efficiency are compelling property developers to adopt advanced cladding systems that offer superior thermal insulation and weather protection, subsequently boosting the demand for specialized installation equipment. The continuous innovation in cladding materials, introducing lighter, more durable, and aesthetically versatile options, also necessitates the development and adoption of sophisticated machinery for their precise handling and installation, thereby acting as a significant market driver.

Furthermore, government initiatives and investments in infrastructure development across various regions play a crucial role in stimulating demand. These projects often involve large-scale commercial and public buildings where modern, high-performance cladding is a preferred choice, directly impacting the need for efficient and reliable equipment. The rising demand for renovation and retrofitting of existing buildings, aimed at enhancing their lifespan, aesthetic appeal, and energy performance, further contributes to market expansion. As older buildings are upgraded to meet contemporary standards and design preferences, the need for advanced cladding removal and installation tools becomes paramount.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increased Global Construction Activity | +1.5% | Asia Pacific, Middle East & Africa, North America | Short-term to Long-term |

| Rising Demand for Energy-Efficient Buildings | +1.2% | Europe, North America, Developed Asia Pacific | Medium-term to Long-term |

| Technological Advancements in Cladding Materials | +0.9% | Global | Medium-term |

| Growth in Renovation and Retrofitting Projects | +0.8% | Europe, North America | Short-term to Medium-term |

Cladding System Equipment Market Restraints Analysis

Despite the positive market outlook, several significant restraints could impede the growth of the cladding system equipment market. One primary concern is the high initial capital investment required for purchasing advanced and specialized equipment. This cost can be prohibitive for smaller construction firms or those operating in regions with limited financial resources, hindering widespread adoption. Additionally, the volatility in raw material prices, particularly for metals and composites used in both cladding materials and equipment manufacturing, can lead to increased production costs and, consequently, higher equipment prices, impacting affordability and demand. The availability of skilled labor for operating and maintaining sophisticated cladding machinery also poses a challenge, as a shortage of trained professionals can slow down project execution and limit the effective utilization of advanced equipment.

Furthermore, stringent and evolving environmental regulations related to construction waste disposal and material sourcing can add complexity and cost to cladding projects. Compliance with these regulations often requires specific equipment or modifications to existing processes, creating barriers for some market participants. Economic slowdowns or political instability in key construction markets can also lead to a deferral or cancellation of large-scale projects, directly reducing the demand for new cladding system equipment. These multifaceted restraints necessitate strategic planning and adaptive business models to mitigate their potential negative impacts on market expansion.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Capital Investment | -1.0% | Global, particularly emerging economies | Short-term to Medium-term |

| Volatility in Raw Material Prices | -0.7% | Global | Short-term |

| Shortage of Skilled Labor | -0.6% | North America, Europe, Developed Asia Pacific | Medium-term to Long-term |

| Complex Regulatory Frameworks | -0.5% | Europe, North America | Medium-term |

Cladding System Equipment Market Opportunities Analysis

The cladding system equipment market is ripe with opportunities driven by several transformative trends and unmet demands. A significant opportunity lies in the burgeoning market for smart and integrated facade systems, which combine traditional cladding functions with advanced technologies such as embedded sensors, solar panels, and dynamic shading. The development of specialized equipment capable of precisely installing and connecting these sophisticated systems presents a substantial growth avenue. Furthermore, the global emphasis on green building certifications and sustainable construction practices is creating demand for equipment that supports the installation of eco-friendly and recycled cladding materials, offering a niche for innovation and market differentiation.

Another major opportunity stems from the rapid urbanization and industrialization occurring in emerging economies, particularly across Asia Pacific and the Middle East. These regions are undertaking massive infrastructure projects and urban developments, driving an unprecedented demand for modern building materials and efficient installation solutions. Manufacturers who can tailor their equipment to meet the specific needs, cost structures, and project scales of these markets stand to gain a significant competitive advantage. Additionally, the increasing focus on worker safety and efficiency in construction sites opens opportunities for robotic and automated cladding installation systems, which not only enhance safety but also improve project timelines and reduce labor costs, addressing persistent industry challenges.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Smart and Integrated Facade Systems | +1.1% | North America, Europe, Developed Asia Pacific | Medium-term to Long-term |

| Expansion in Emerging Economies and Urbanization | +1.0% | Asia Pacific, Latin America, Middle East & Africa | Short-term to Long-term |

| Increasing Adoption of Robotics and Automation | +0.9% | Global | Medium-term |

| Demand for Sustainable and Green Building Solutions | +0.8% | Europe, North America | Medium-term to Long-term |

Cladding System Equipment Market Challenges Impact Analysis

The cladding system equipment market faces several inherent challenges that demand strategic responses from industry participants. The complexity and diversity of cladding materials and systems, ranging from traditional brick to advanced composite panels and glass facades, necessitate highly specialized and often proprietary equipment. This fragmentation can lead to higher development costs for manufacturers and increased inventory complexity for equipment providers, as a single piece of machinery may not be universally applicable across all project types. Furthermore, the construction industry is highly susceptible to economic downturns, which can lead to project delays or cancellations, directly impacting the demand for new equipment and services.

Another significant challenge involves intense price competition within the equipment manufacturing sector, particularly from local producers in various regions. This competition can erode profit margins and pressure manufacturers to continuously innovate while maintaining cost-effectiveness. The long lifecycle of heavy construction equipment also presents a challenge, as companies may defer new purchases in favor of maintaining existing machinery, thus slowing down market penetration for new technologies. Addressing these challenges requires a focus on versatile, modular equipment designs, robust after-sales support, and strategic market positioning to differentiate offerings and sustain growth.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Customization Needs for Diverse Cladding Types | -0.8% | Global | Short-term to Long-term |

| Intense Price Competition | -0.7% | Asia Pacific, Global | Short-term |

| Economic Volatility and Project Delays | -0.6% | Global | Short-term to Medium-term |

| Long Equipment Lifecycle and Maintenance Over Replacement | -0.5% | Global | Long-term |

Cladding System Equipment Market - Updated Report Scope

This comprehensive market report offers an in-depth analysis of the global Cladding System Equipment Market, providing critical insights into its current size, historical performance, and future growth projections up to 2033. It meticulously covers key market trends, growth drivers, restraints, opportunities, and challenges influencing the industry landscape. The report also includes a detailed segmentation analysis by equipment type, application, and end-use, alongside a thorough regional assessment, aiming to provide stakeholders with a holistic understanding of market dynamics and strategic foresight.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 14.5 billion |

| Market Forecast in 2033 | USD 24.5 billion |

| Growth Rate | 6.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Facade Systems Innovators, Precision Tools & Machinery, Global Cladding Solutions, Advanced Lifting Technologies, Building Envelope Robotics, Modern Construction Equipment, Green Building Tools Co., Urban Facade Innovations, Durable Machinery Group, Premier Cladding Equipment, NexGen Construction Systems, Elite Building Tools, Metro Facade Solutions, Zenith Equipment Inc., Dynamic Construction Gear, Prime Installation Systems, Vertex Machinery Corp., OmniBuild Technologies, Superior Building Systems, Pioneer Equipment Group |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The global cladding system equipment market is meticulously segmented to provide a granular understanding of its diverse components and their respective market dynamics. These segments are primarily defined by equipment type, application, and end-use sector, each reflecting distinct operational requirements and growth opportunities. The segmentation analysis helps in identifying which types of equipment are experiencing the highest demand, where they are most critically applied, and in which sectors their utilization is most prevalent. This detailed breakdown facilitates strategic planning for manufacturers, distributors, and end-users, enabling them to target specific market niches with tailored solutions.

Each segment contributes uniquely to the overall market landscape. For instance, lifting and access equipment forms the backbone of large-scale installation projects, while specialized cutting and fabrication tools are essential for bespoke and complex architectural designs. The application segments highlight the lifecycle of cladding, from initial fabrication and installation to ongoing maintenance and eventual demolition. Furthermore, the end-use sectors illustrate how residential, commercial, and industrial construction projects each drive specific demands for cladding equipment, shaped by varying building codes, aesthetic preferences, and performance requirements. Understanding these interdependencies is crucial for developing comprehensive market strategies.

- By Equipment Type: This segment includes a broad range of machinery vital for the entire cladding process.

- Lifting and Access Equipment: Essential for vertical and horizontal movement of cladding panels and personnel, comprising cranes (tower, mobile), scaffolding systems (modular, rolling), aerial work platforms (boom lifts, scissor lifts), and hoists and winches.

- Cutting and Fabrication Equipment: Tools for processing raw cladding materials into desired shapes and sizes, such as panel saws, CNC routers for precision cuts, bending machines, and shearing machines.

- Fastening and Fixing Tools: Used for securing cladding panels to the building structure, including power drills, riveters, adhesive application systems for bonding, and welding equipment for metal frames.

- Handling and Installation Tools: Specialized equipment for safe and efficient placement of panels, encompassing vacuum lifters, panel clamps, and various specialized hand tools.

- Surface Preparation and Finishing Equipment: Machinery for preparing the facade for cladding and for final finishing, like grinding and polishing machines, cleaning equipment, and sealant applicators.

- Safety Equipment: Crucial for ensuring worker safety during installation, including harnesses, fall protection systems, and safety netting.

- By Application: This segment categorizes the market based on the primary purpose of the equipment's use.

- Installation: The largest segment, focusing on equipment used for mounting new cladding systems onto building structures.

- Maintenance and Repair: Equipment utilized for inspection, cleaning, and replacing damaged cladding components to preserve facade integrity and aesthetics.

- Demolition and Removal: Tools and machinery employed for safely dismantling and removing old or damaged cladding systems, often during renovation projects.

- Fabrication: Equipment used in workshops or on-site to cut, shape, and prepare cladding materials before installation.

- By End-Use Sector: This segment differentiates demand based on the type of building or project.

- Residential Buildings: Equipment used in single-family homes, multi-story apartments, and condominiums, driven by housing demand and aesthetic preferences.

- Commercial Buildings: Includes offices, retail centers, hotels, and educational institutions, characterized by larger-scale projects and demand for aesthetic and performance-driven cladding.

- Industrial Buildings: Facilities such as factories, warehouses, and power plants, where durability, insulation, and protective cladding are paramount.

- Infrastructure: Public sector projects like government buildings, transportation hubs, and healthcare facilities, often requiring robust and high-security cladding solutions.

Regional Highlights

The global cladding system equipment market exhibits diverse growth patterns and demands across different geographical regions, influenced by varying construction activities, regulatory landscapes, and economic developments. North America and Europe represent mature markets characterized by stringent building codes, a strong emphasis on energy efficiency, and significant investments in renovation and retrofitting projects. These regions often lead in the adoption of advanced and automated cladding installation technologies, driven by high labor costs and a focus on worker safety. The demand here is frequently for specialized equipment that can handle complex designs and high-performance materials, supporting sustainable construction practices and architectural innovation.

Asia Pacific, however, stands out as the fastest-growing market, propelled by rapid urbanization, extensive infrastructure development, and a burgeoning construction sector in countries like China, India, and Southeast Asian nations. This region witnesses a massive influx of new commercial, residential, and industrial projects, creating a high volume demand for both basic and advanced cladding equipment. While cost-effectiveness remains a key consideration, there's a growing inclination towards modern, efficient, and safer equipment. Latin America and the Middle East & Africa regions are also experiencing significant growth, fueled by urbanization, tourism infrastructure development, and diversification efforts away from traditional economies, leading to increased construction spending and a corresponding demand for cladding system equipment.

- North America: A mature market characterized by strong regulatory frameworks for building safety and energy efficiency. High adoption of automated and precision equipment for complex architectural designs and green building initiatives. Significant demand driven by both new construction and extensive renovation projects.

- Europe: Leads in sustainable building practices and innovative cladding solutions. Strict environmental regulations and a focus on thermal performance drive demand for advanced equipment compatible with eco-friendly materials. Renovation and retrofitting of aging infrastructure are major contributors to market growth.

- Asia Pacific (APAC): The fastest-growing region due to rapid urbanization, massive infrastructure development, and burgeoning residential and commercial construction in countries like China, India, and ASEAN nations. Demand is high for a wide range of equipment, from cost-effective solutions to increasingly sophisticated machinery.

- Latin America: Experiencing steady growth fueled by urbanization, public infrastructure investments, and increasing foreign direct investment in real estate. The market is evolving with a growing demand for modern cladding systems and associated installation equipment.

- Middle East and Africa (MEA): Marked by significant construction booms, particularly in the GCC countries, driven by tourism, economic diversification, and mega-projects. High demand for aesthetic, high-performance cladding equipment for iconic structures and luxury developments. Infrastructure development also plays a crucial role.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Cladding System Equipment Market.- Facade Systems Innovators

- Precision Tools & Machinery

- Global Cladding Solutions

- Advanced Lifting Technologies

- Building Envelope Robotics

- Modern Construction Equipment

- Green Building Tools Co.

- Urban Facade Innovations

- Durable Machinery Group

- Premier Cladding Equipment

- NexGen Construction Systems

- Elite Building Tools

- Metro Facade Solutions

- Zenith Equipment Inc.

- Dynamic Construction Gear

- Prime Installation Systems

- Vertex Machinery Corp.

- OmniBuild Technologies

- Superior Building Systems

- Pioneer Equipment Group

Frequently Asked Questions

What is the projected growth rate for the Cladding System Equipment Market?

The Cladding System Equipment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033, reaching an estimated value of USD 24.5 billion by 2033.

Which factors are primarily driving the market for cladding system equipment?

Key drivers include increased global construction activity, rising demand for energy-efficient buildings, technological advancements in cladding materials, and growth in renovation and retrofitting projects across various sectors.

How is AI impacting the cladding system equipment market?

AI is significantly impacting the market through predictive maintenance for equipment, optimized design and material usage, automated quality control, enhanced project management, and the integration of robotics for safer and more precise installation.

What are the main types of equipment covered in this market?

The market covers a wide range of equipment including lifting and access equipment (cranes, scaffolding), cutting and fabrication equipment (saws, CNC routers), fastening and fixing tools, handling and installation tools, and surface preparation equipment.

Which region is expected to lead market growth for cladding system equipment?

The Asia Pacific region is anticipated to be the fastest-growing market, driven by rapid urbanization, extensive infrastructure development, and a booming construction sector in countries like China and India.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted