Chromite Market

Chromite Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707392 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

Chromite Market Size

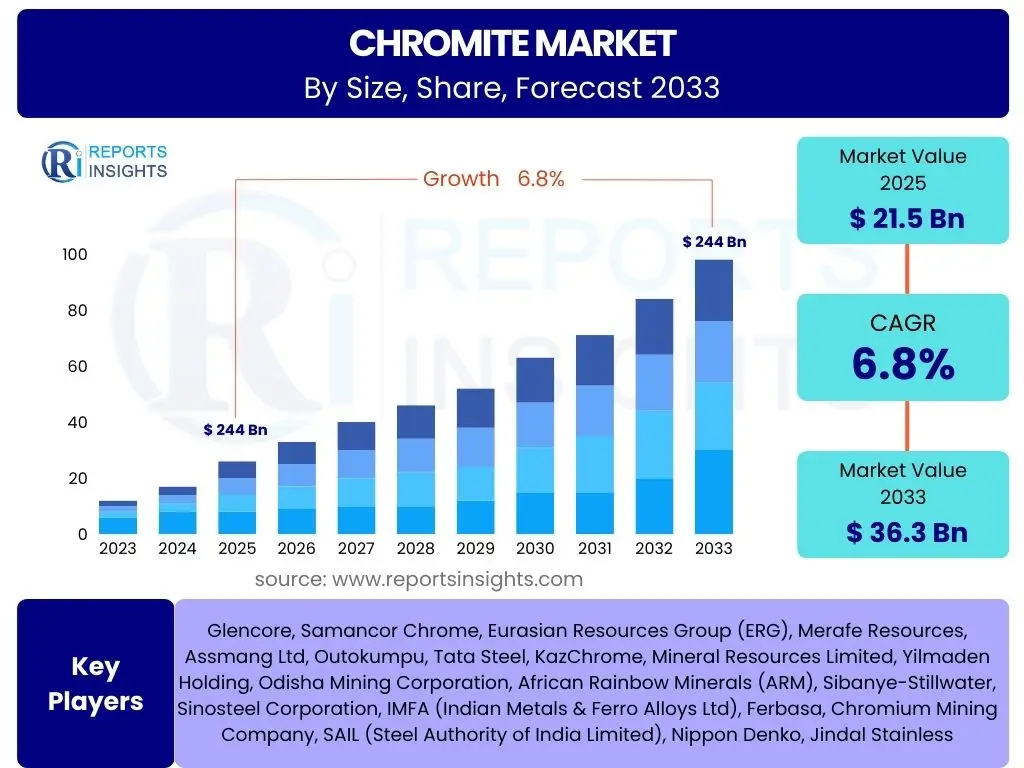

According to Reports Insights Consulting Pvt Ltd, The Chromite Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 21.5 Billion in 2025 and is projected to reach USD 36.3 Billion by the end of the forecast period in 2033.

Key Chromite Market Trends & Insights

The global chromite market is profoundly influenced by several prevailing trends, primarily driven by industrial expansion and technological advancements. A significant trend is the sustained and increasing demand for stainless steel, a primary end-use application for ferrochrome derived from chromite. This demand is fueled by global urbanization, infrastructure development, and the automotive sector's continuous evolution, particularly in emerging economies. The properties of stainless steel, such as corrosion resistance and durability, ensure its indispensability across various industries, thereby directly impacting chromite consumption.

Another prominent trend involves the growing emphasis on sustainable mining practices and responsible sourcing of minerals. As environmental regulations become more stringent and corporate social responsibility gains prominence, market participants are investing in advanced processing technologies to reduce environmental footprints, minimize waste, and improve energy efficiency. This includes exploring beneficiation techniques that enhance chromite recovery from lower-grade ores and reduce energy intensity. Furthermore, there is an increasing focus on circular economy principles, with efforts to enhance recycling of chromium-containing materials, which, while reducing the demand for virgin chromite in some areas, also promotes a more efficient resource utilization model within the broader metals industry.

Technological innovations in ferrochrome production, such as the adoption of more energy-efficient furnaces and improved smelting processes, are also shaping the market. These advancements aim to reduce production costs and environmental impact, making the supply chain more resilient and competitive. Additionally, geopolitical factors and trade policies significantly influence supply chain dynamics, leading to strategic investments in new mining projects and processing facilities to secure stable supplies. The market is also witnessing a gradual shift towards regional self-sufficiency in chromite processing, driven by a desire to add value domestically and reduce reliance on single-source imports.

- Persistent demand from the stainless steel industry for ferrochrome production.

- Increased focus on sustainable mining and processing technologies to reduce environmental impact.

- Advancements in beneficiation techniques for improved chromite recovery from diverse ore grades.

- Growing investment in regional processing capabilities to enhance supply chain resilience.

- Development of energy-efficient smelting technologies in the ferrochrome sector.

AI Impact Analysis on Chromite

The integration of Artificial intelligence (AI) is poised to significantly transform various facets of the chromite industry, from exploration and mining to processing and supply chain management. Users frequently inquire about how AI can enhance operational efficiency, reduce costs, and improve safety within the typically labor-intensive mining sector. AI applications, such as predictive analytics, machine learning algorithms, and automation, offer the potential to optimize resource extraction by analyzing vast datasets from geological surveys, drilling operations, and sensor data. This enables more precise identification of ore bodies, efficient mine planning, and dynamic adjustments to extraction strategies, ultimately leading to higher yields and reduced waste.

Furthermore, AI is expected to revolutionize processing plants by enabling real-time monitoring and control of complex operations. For instance, AI-powered systems can optimize grinding, flotation, and smelting processes, leading to improved chromite recovery rates and reduced energy consumption. Predictive maintenance, another key AI application, can anticipate equipment failures, minimizing costly downtime and extending the lifespan of machinery. Beyond operational efficiencies, AI can also enhance supply chain transparency and logistics, optimizing inventory management, transportation routes, and demand forecasting, thereby creating a more responsive and resilient chromite market. However, concerns regarding data security, the initial capital investment required for AI implementation, and the need for a skilled workforce capable of managing these advanced systems are also prevalent among stakeholders.

The long-term influence of AI extends to research and development within the chromite sector. AI and machine learning can accelerate the discovery of new applications for chromite and its derivatives, as well as optimize the development of novel materials. By simulating various chemical reactions and material properties, AI can significantly reduce the time and resources traditionally required for innovation. This technological shift is not only about incremental improvements but also about fostering a paradigm shift towards smart mining and processing, where data-driven decisions replace conventional methods, leading to unprecedented levels of efficiency, sustainability, and competitive advantage across the chromite value chain. Addressing the technological adoption curve and ensuring data integrity will be critical for realizing these benefits fully.

- Optimized geological exploration and resource modeling through AI-driven data analysis.

- Enhanced operational efficiency in mining via predictive maintenance and autonomous equipment.

- Improved chromite processing and recovery rates through AI-controlled beneficiation and smelting.

- Streamlined supply chain management and logistics with AI-powered forecasting and route optimization.

- Accelerated research and development for new chromite applications and material science.

Key Takeaways Chromite Market Size & Forecast

The chromite market's forecast indicates a robust growth trajectory, primarily fueled by the unwavering demand from the global stainless steel industry. Users frequently inquire about the primary drivers sustaining this growth and the long-term prospects of the market. The consistent expansion of infrastructure projects, urbanization, and industrial manufacturing worldwide continues to underpin the need for stainless steel, positioning ferrochrome (a key derivative of chromite) as an indispensable alloy. This foundational demand ensures a stable and expanding market for chromite ore, despite potential short-term fluctuations driven by economic cycles or geopolitical events.

A significant takeaway is the strategic importance of chromite as a critical mineral, vital for various industrial applications beyond metallurgy, including refractories and chemicals. The market's resilience is further supported by innovations in extraction and processing technologies, which aim to enhance efficiency and reduce environmental impact. These technological advancements are crucial for unlocking new reserves and improving the economics of mining, especially for lower-grade ores. The forecast highlights an increasing emphasis on sustainable practices and responsible sourcing across the value chain, which is becoming a prerequisite for market access and social license to operate for major players.

Furthermore, the geographical distribution of chromite reserves and processing capabilities remains a key factor, with a concentration of production in specific regions influencing global supply dynamics. The market's future growth is expected to be more diversified, with emerging economies playing an increasingly vital role in both chromite production and consumption. Investment in new mining projects and downstream processing facilities in these regions will be pivotal to meeting the projected demand and ensuring supply security. The overall outlook points towards a dynamic market driven by industrial growth, technological innovation, and a growing commitment to sustainability.

- Steady growth driven by global stainless steel demand, especially from infrastructure and automotive sectors.

- Chromite remains a critical mineral with diverse applications beyond metallurgy.

- Technological advancements in mining and processing are enhancing efficiency and sustainability.

- Geopolitical factors and regional supply dynamics significantly influence market stability.

- Increasing focus on sustainable sourcing and environmentally responsible mining practices.

Chromite Market Drivers Analysis

The chromite market is predominantly driven by the robust and continuous demand from the stainless steel industry. Stainless steel, an alloy critical for its corrosion resistance and durability, is extensively used in construction, automotive, consumer goods, and industrial machinery sectors. As global population grows and economies expand, particularly in developing regions, the consumption of stainless steel escalates, directly translating into higher demand for ferrochrome, which is produced from chromite. This direct correlation makes the health of the stainless steel industry a primary indicator for the chromite market's growth trajectory.

Beyond stainless steel, the increasing demand from the refractory industry also serves as a significant driver. Chromite-based refractories are essential for lining high-temperature furnaces and kilns in steel, cement, and glass manufacturing due to their excellent thermal stability and resistance to chemical attack. Industrial growth across these sectors, particularly in Asia Pacific, fuels the demand for new and replacement refractory materials. Furthermore, the chemical industry utilizes chromite for producing various chromium chemicals, which find applications in pigments, leather tanning, and wood preservation, contributing to the overall market expansion.

Urbanization and infrastructure development worldwide provide an underlying impetus for chromite demand. As cities expand and new infrastructure projects, such as bridges, buildings, and transportation networks, are initiated, the need for stainless steel and other chromite-derived products intensifies. This long-term trend, coupled with ongoing technological advancements that make chromite extraction and processing more efficient and environmentally sound, creates a positive feedback loop for market growth. The strategic importance of chromite for national industrial bases further encourages investment and sustained demand.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Stainless Steel Production | +2.5% | Asia Pacific (China, India), Europe, North America | Long-term (2025-2033) |

| Increasing Demand from Refractory Industry | +1.8% | Global, particularly industrializing nations | Mid-term (2025-2030) |

| Expansion of Chemical Industry Applications | +0.9% | Europe, North America, Asia Pacific | Long-term (2025-2033) |

| Urbanization and Infrastructure Development | +1.6% | Emerging Economies (India, Southeast Asia, Africa) | Long-term (2025-2033) |

Chromite Market Restraints Analysis

The chromite market faces several significant restraints that can impede its growth trajectory. One primary constraint is the volatility in raw material prices, particularly for chromite ore and the energy required for its processing. Fluctuations in supply due to geopolitical instability in key mining regions, labor disputes, or logistical challenges can lead to erratic price movements, impacting the profitability of ferrochrome producers and ultimately the demand for chromite. This price instability makes long-term planning challenging for market participants and can deter new investments in the sector.

Environmental regulations and escalating concerns over the ecological impact of mining and processing activities pose another substantial restraint. Strict environmental compliance requirements, including those related to waste management, water usage, and carbon emissions, increase operational costs for mining companies. The public's growing awareness of environmental degradation associated with resource extraction can also lead to protests and delays in obtaining necessary permits for new projects or expansions, thereby limiting supply growth. Adherence to these regulations often necessitates significant capital expenditure on advanced pollution control technologies.

Furthermore, the high energy costs associated with the smelting of ferrochrome, an energy-intensive process, can also act as a restraint. Regions with high electricity prices or unreliable energy supply may find it challenging to maintain competitive production costs. While efforts are underway to adopt more energy-efficient technologies, these investments require substantial upfront capital. Lastly, the potential for substitution by alternative materials in certain applications, although limited for chromite's core uses, could marginally impact demand. For instance, in some refractory applications, alternative materials might be considered if chromite prices become excessively high or supply becomes unreliable, though the unique properties of chromite generally ensure its indispensability.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile Raw Material Prices | -1.2% | Global, particularly major importing/exporting regions | Short-term to Mid-term (2025-2028) |

| Stringent Environmental Regulations | -0.8% | Europe, North America, parts of Asia Pacific | Long-term (2025-2033) |

| High Energy Costs for Processing | -0.7% | Regions with high industrial electricity rates | Mid-term (2025-2030) |

| Geopolitical Instability in Key Mining Regions | -1.0% | Africa, Central Asia | Short-term to Mid-term (2025-2028) |

Chromite Market Opportunities Analysis

The chromite market presents several compelling opportunities for growth and innovation. One significant opportunity lies in the advancement and adoption of new beneficiation technologies. These technologies aim to improve the recovery rates of chromite from lower-grade ores and waste streams, which were previously considered uneconomical. As high-grade chromite deposits become scarcer, developing efficient and cost-effective methods to process complex or leaner ores becomes crucial. This not only extends the lifespan of existing mines but also opens up new potential reserves, diversifying the global supply base and reducing reliance on a few concentrated sources.

Another key opportunity emerges from the increasing global focus on the circular economy and resource efficiency. While stainless steel recycling is well-established, there is growing potential for more comprehensive recycling and recovery of chromium from industrial wastes and end-of-life products where chromite is used. Developing technologies to efficiently recover chromium from refractory linings, chemical wastes, and other sources can provide a secondary supply of chromium, complementing virgin chromite production. This approach not only aligns with sustainability goals but can also provide a more stable and regionally diversified supply of chromium, reducing reliance on primary extraction and enhancing material security.

Furthermore, emerging applications for chromium in advanced materials and niche industries offer promising growth avenues. While metallurgical applications dominate, research into new uses for chromium compounds in areas such as energy storage, catalysis, and specialized alloys could create incremental demand. Innovations in ferrochrome production, including the use of renewable energy sources for smelting and the development of carbon-neutral processes, also represent significant opportunities. Companies that can demonstrate a commitment to sustainable production and supply chain transparency are likely to gain a competitive advantage and access to markets with stringent environmental and social governance (ESG) requirements, thereby positioning themselves for long-term growth.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Advancements in Beneficiation Technologies | +1.5% | Global, particularly in mining regions | Mid-term to Long-term (2026-2033) |

| Increased Focus on Recycling and Circular Economy | +1.0% | Europe, North America, Developed Asia Pacific | Long-term (2027-2033) |

| Emerging Niche Applications for Chromium | +0.7% | Global, research-driven economies | Long-term (2028-2033) |

| Investment in Sustainable and Green Mining Practices | +0.8% | Global, driven by ESG mandates | Mid-term to Long-term (2026-2033) |

Chromite Market Challenges Impact Analysis

The chromite market faces several notable challenges that can impact its operational stability and growth. One significant challenge pertains to the geopolitical risks and supply chain vulnerabilities. A considerable portion of global chromite reserves and production is concentrated in a few countries, making the market susceptible to political instability, regulatory changes, or export restrictions in these regions. Disruptions from these sources can lead to supply shortages, price surges, and increased volatility, compelling end-users to seek diversified sourcing strategies or invest in alternative materials, albeit with limitations. Managing these geopolitical risks requires robust supply chain resilience and strategic international partnerships.

Another pressing challenge involves adherence to increasingly stringent environmental, social, and governance (ESG) standards. Mining operations inherently carry environmental impacts, and chromite mining is no exception. Companies must navigate complex regulations concerning land reclamation, water management, waste disposal, and carbon emissions. Furthermore, social aspects, such as community engagement, labor rights, and ensuring a safe working environment, are under intense scrutiny. Failing to meet these ESG expectations can lead to operational delays, reputational damage, financial penalties, and a potential loss of social license to operate, particularly from investors who are increasingly prioritizing sustainable practices.

Market competition, particularly in the ferrochrome segment, presents an ongoing challenge. The oversupply of ferrochrome in certain periods, driven by expansion in production capacities, can lead to downward pressure on prices, squeezing profit margins for chromite miners. This intensifies competition among producers, requiring continuous efforts to optimize production costs, improve efficiency, and innovate. Finally, the fluctuating demand from end-use industries, particularly the cyclical nature of the stainless steel market, can pose a challenge for chromite producers to match supply precisely with demand, leading to inventory management issues and price instability during downturns. Addressing these challenges necessitates strategic investments, proactive risk management, and a commitment to sustainable and responsible business practices.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Geopolitical Risks and Supply Chain Vulnerabilities | -1.5% | Global, particularly reliant on key producers | Short-term to Mid-term (2025-2029) |

| Adherence to Stringent ESG Standards | -0.9% | Global, especially developed markets | Long-term (2025-2033) |

| Intense Market Competition and Price Pressures | -0.6% | Global, particularly major ferrochrome producers | Mid-term (2025-2030) |

| Fluctuating Demand from End-Use Industries | -0.7% | Global, tied to economic cycles | Short-term (2025-2027) |

Chromite Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Chromite Market, offering a detailed understanding of its size, historical performance, and future growth projections. It meticulously examines the key trends shaping the industry, explores the impactful role of Artificial Intelligence, and outlines critical drivers, restraints, opportunities, and challenges. The report delivers a granular segmentation analysis across various applications and grades, complemented by a thorough regional assessment. Furthermore, it profiles key market participants, providing stakeholders with strategic insights to navigate the evolving market landscape and make informed business decisions.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 21.5 Billion |

| Market Forecast in 2033 | USD 36.3 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Glencore, Samancor Chrome, Eurasian Resources Group (ERG), Merafe Resources, Assmang Ltd, Outokumpu, Tata Steel, KazChrome, Mineral Resources Limited, Yilmaden Holding, Odisha Mining Corporation, African Rainbow Minerals (ARM), Sibanye-Stillwater, Sinosteel Corporation, IMFA (Indian Metals & Ferro Alloys Ltd), Ferbasa, Chromium Mining Company, SAIL (Steel Authority of India Limited), Nippon Denko, Jindal Stainless |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Chromite Market is comprehensively segmented to provide a detailed understanding of its diverse applications, various grades, and geographical distribution, enabling stakeholders to identify specific growth avenues and market dynamics. This segmentation is crucial for targeted strategic planning and investment decisions within the complex chromite value chain. Each segment reflects unique demand drivers and supply characteristics, influenced by technological advancements, industrial trends, and regional economic factors.

By application, the market is primarily driven by the metallurgical industry, particularly the production of ferrochrome essential for stainless steel. However, significant demand also arises from the refractory sector for high-temperature applications and the chemical industry for the production of chromium compounds. The foundry industry and other niche applications also contribute to the market's overall size. The grade-based segmentation differentiates chromite ore based on its chemical composition and physical properties, which dictate its suitability for metallurgical, refractory, or chemical uses, each commanding different pricing and market specifications.

Regional segmentation provides insights into the geographical distribution of chromite mining, processing, and consumption. This highlights key producing regions, major consuming markets, and the trade flows influencing global supply-demand balances. Understanding these distinct segments allows for a granular analysis of market trends, competitive landscapes, and regulatory environments, offering a holistic view of the chromite industry's multifaceted nature and its response to global economic shifts and industrial evolution.

- By Application:

- Metallurgy (Ferrochrome, Stainless Steel Production): Dominant segment driven by global stainless steel demand, especially in construction, automotive, and consumer goods.

- Refractories: Essential for lining high-temperature furnaces in steel, cement, and glass industries due to its high melting point and chemical stability.

- Chemicals: Used in the production of various chromium chemicals for pigments, leather tanning, and wood preservation.

- Foundry: Utilized in the casting industry as a facing sand or mold coating due to its high thermal conductivity and low thermal expansion.

- Others: Includes minor applications in specialized ceramics, abrasives, and as a mineral specimen.

- By Grade:

- Metallurgical Grade: High chromium-to-iron ratio, primarily used for ferrochrome production.

- Refractory Grade: Suitable for high-temperature applications, characterized by specific chemical compositions and physical properties.

- Chemical Grade: Lower chromium content, used in the production of various chromium chemicals.

- By Region:

- North America: Stable demand from established industrial sectors, focusing on advanced processing.

- Europe: Stringent environmental regulations and focus on high-value applications and recycling.

- Asia Pacific (APAC): Largest and fastest-growing market due to rapid industrialization, especially in China and India.

- Latin America: Emerging market with growing industrial base and potential for new resource development.

- Middle East and Africa (MEA): Significant chromite reserves and increasing local processing capabilities, particularly in South Africa and Turkey.

Regional Highlights

- Asia Pacific (APAC): Dominates the global chromite market, largely driven by the extensive industrial growth in China and India. These countries are not only major consumers of ferrochrome and stainless steel but also increasingly significant players in chromite ore imports and ferrochrome production. Rapid urbanization, infrastructure development, and expanding manufacturing sectors in the region fuel sustained demand for chromite and its derivatives. Investments in steel production capacities and chemical industries further bolster APAC's position as the primary growth engine for the chromite market.

- Middle East and Africa (MEA): This region is a crucial hub for chromite mining, with South Africa being the world's largest producer and holding the vast majority of global reserves. Other significant producers include Turkey and Kazakhstan. The region is increasingly focused on value addition through local ferrochrome production, reducing raw material exports and boosting economic development. Geopolitical stability and investment in mining infrastructure in these countries significantly impact global chromite supply dynamics.

- Europe: Characterized by mature industrial economies with a strong focus on high-quality stainless steel and specialized refractory products. While chromite mining is limited, Europe is a major importer of chromite ore and ferrochrome, with a strong emphasis on sustainable sourcing, environmental compliance, and technological innovation in downstream processing. The region also plays a key role in the research and development of new chromium applications.

- North America: Features a developed industrial base with consistent demand from the stainless steel, chemical, and refractory sectors. The region relies heavily on imports for chromite ore, focusing on efficient processing and high-value applications. Technological advancements in manufacturing and a strong emphasis on environmental regulations shape the market dynamics here, encouraging the adoption of cleaner production technologies.

- Latin America: Represents an emerging market for chromite consumption, driven by growing industrialization and infrastructure development in countries like Brazil. While not a major chromite producer, the region's increasing demand for stainless steel and industrial minerals contributes to the global market, with potential for future local resource exploration and processing.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Chromite Market.- Glencore

- Samancor Chrome

- Eurasian Resources Group (ERG)

- Merafe Resources

- Assmang Ltd

- Outokumpu

- Tata Steel

- KazChrome

- Mineral Resources Limited

- Yilmaden Holding

- Odisha Mining Corporation

- African Rainbow Minerals (ARM)

- Sibanye-Stillwater

- Sinosteel Corporation

- IMFA (Indian Metals & Ferro Alloys Ltd)

- Ferbasa

- Chromium Mining Company

- SAIL (Steel Authority of India Limited)

- Nippon Denko

- Jindal Stainless

Frequently Asked Questions

What is chromite and what are its primary uses?

Chromite is an iron chromium oxide mineral, serving as the only economically viable ore for chromium. Its primary uses are in the production of ferrochrome for stainless steel, followed by applications in refractories for high-temperature furnaces, and in the chemical industry for various chromium compounds.

What factors are driving the growth of the chromite market?

The chromite market's growth is predominantly driven by the surging global demand for stainless steel, increased consumption from the refractory industry, expansion in the chemical sector, and large-scale urbanization and infrastructure development projects worldwide.

Which regions are key players in the chromite market?

Asia Pacific (especially China and India) is the largest consuming and importing region, while the Middle East and Africa (particularly South Africa, Turkey, and Kazakhstan) are the primary chromite ore producing regions. Europe and North America are significant importers and consumers of finished products.

What challenges does the chromite market face?

Key challenges include volatile raw material prices, stringent environmental regulations increasing operational costs, high energy costs for processing, geopolitical instability in major mining regions, and intense market competition from oversupply in the ferrochrome segment.

How is AI impacting the chromite industry?

AI is influencing the chromite industry by optimizing geological exploration, enhancing operational efficiency in mining through predictive maintenance and automation, improving processing and recovery rates, streamlining supply chain management, and accelerating research into new applications for chromium.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted