Chlor Alkali Market

Chlor Alkali Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709920 | Last Updated : December 22, 2025 |

Format : ![]()

![]()

![]()

![]()

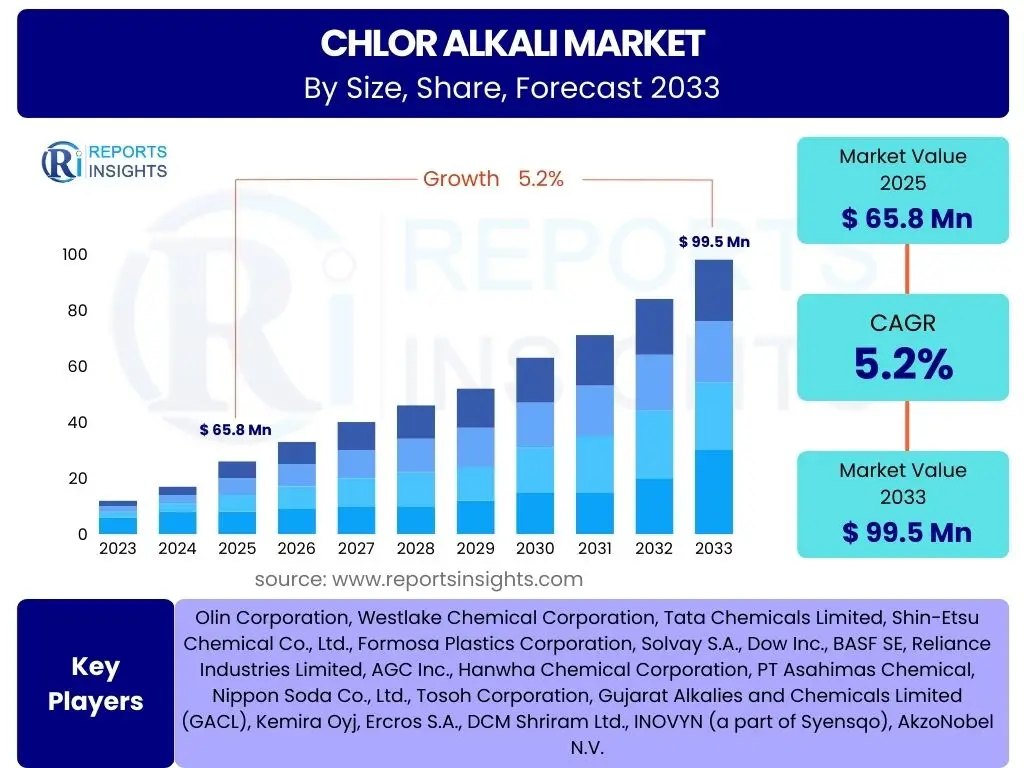

Chlor Alkali Market Size

According to Reports Insights Consulting Pvt Ltd, The Chlor Alkali Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.2% between 2025 and 2033. The market is estimated at USD 65.8 Billion in 2025 and is projected to reach USD 99.5 Billion by the end of the forecast period in 2033.

Key Chlor Alkali Market Trends & Insights

The Chlor Alkali market is experiencing significant shifts driven by increasing demand from diverse end-use industries, stringent environmental regulations pushing for sustainable production, and ongoing technological advancements in manufacturing processes. Users frequently inquire about the long-term impact of sustainability initiatives and the emergence of new applications for chlor-alkali products. Furthermore, the market is characterized by efforts to enhance energy efficiency and reduce carbon footprints, reflecting a broader industry commitment to environmental stewardship. Geopolitical factors also play a crucial role, influencing raw material supply chains and energy costs, thereby impacting regional market dynamics.

Technological innovations, particularly in membrane cell technology, are continuously improving the efficiency and environmental profile of chlor-alkali production, gradually replacing older, less sustainable methods. This transition is not only optimizing operational costs but also helping manufacturers comply with evolving regulatory landscapes. The expanding applications of derivatives in various sectors, including healthcare, automotive, and construction, further underscore the market's robust growth potential. The ongoing globalization of industrial activities continues to fuel demand, particularly in rapidly developing economies where infrastructure and manufacturing capabilities are expanding.

- Shift towards sustainable and energy-efficient membrane cell technology.

- Increasing demand from water treatment and pulp & paper industries.

- Growing adoption of PVC in construction and automotive sectors.

- Focus on reducing carbon footprint and waste generation in production.

- Impact of fluctuating energy prices on operational costs.

AI Impact Analysis on Chlor Alkali

The integration of Artificial Intelligence (AI) into the Chlor Alkali industry is a topic of growing interest, with users frequently exploring its potential to revolutionize production processes, enhance operational efficiency, and optimize resource utilization. AI applications are anticipated to significantly improve predictive maintenance, process control, and supply chain management, leading to reduced downtime and cost savings. There are also discussions around AI's role in real-time data analysis for quality control and process optimization, addressing the complex variables inherent in chemical manufacturing.

Concerns often revolve around the initial investment required for AI infrastructure, the need for specialized skill sets to manage and interpret AI systems, and data security challenges within industrial environments. However, the expectations for AI's influence are largely positive, focusing on its capacity to drive greater automation, improve safety protocols, and enable more precise control over highly sensitive chemical reactions. AI is also expected to contribute to more sustainable practices by optimizing energy consumption and minimizing waste generation throughout the production cycle.

- Enhanced predictive maintenance reducing equipment failures and downtime.

- Optimization of production parameters for improved yield and energy efficiency.

- Real-time monitoring and control of chemical processes for quality consistency.

- Supply chain optimization and demand forecasting for better inventory management.

- Automation of routine tasks, improving operational safety and reducing labor costs.

Key Takeaways Chlor Alkali Market Size & Forecast

The Chlor Alkali market is set for sustained growth, driven by a confluence of robust industrial demand, technological advancements, and a global pivot towards more sustainable manufacturing practices. Key takeaways from the market size and forecast analysis reveal that while traditional applications continue to provide a stable base, emerging uses in sectors like hydrogen production and advanced materials will be crucial for accelerating expansion. Users frequently inquire about the primary drivers for this growth and the potential for disruption from environmental regulations or alternative technologies.

The forecast period indicates a steady increase in market valuation, underpinned by the indispensable nature of chlor-alkali products in modern industrial economies. A critical insight is the increasing emphasis on operational efficiency and environmental compliance, which is compelling manufacturers to invest in state-of-the-art technologies and cleaner production methods. Furthermore, the expansion of chemical manufacturing and urban infrastructure in developing regions is expected to serve as a significant demand catalyst, ensuring a positive outlook for market participants. The ability of companies to innovate and adapt to these evolving market dynamics will largely determine their competitive advantage.

- Robust growth driven by diverse industrial applications and emerging sectors.

- Technological innovation, particularly in membrane cell technology, is key to efficiency and sustainability.

- Asia Pacific remains a dominant region for demand and production expansion.

- Environmental regulations continue to shape production methods and market dynamics.

- Strategic investments in R&D and capacity expansion are vital for market leadership.

Chlor Alkali Market Drivers Analysis

The Chlor Alkali market is primarily driven by the escalating demand from various end-use industries, particularly the chemical processing, pulp and paper, and water treatment sectors. Caustic soda and chlorine, the primary products of the chlor-alkali process, are fundamental raw materials for the production of a wide array of chemicals, plastics like PVC, and essential commodities. The continuous expansion of manufacturing capacities globally, especially in emerging economies, directly translates into increased consumption of these basic chemicals, underpinning market growth. Additionally, the growing global population and urbanization trends necessitate enhanced water treatment facilities, further boosting the demand for chlorine derivatives for disinfection purposes.

Another significant driver is the increasing adoption of polyvinyl chloride (PVC) in the construction and automotive industries. PVC's versatility, durability, and cost-effectiveness make it a preferred material for pipes, window frames, flooring, and various automotive components. As infrastructure development and housing projects continue to surge worldwide, the demand for PVC, and consequently for chlorine, is expected to remain robust. Furthermore, the rising awareness and stringent regulations regarding water quality and wastewater treatment globally are compelling industries and municipalities to invest more in purification processes, thereby driving the demand for chlorine for its disinfectant properties.

The ongoing industrialization in regions like Asia Pacific and Latin America, characterized by rapid economic development and expansion of manufacturing bases, provides a substantial impetus to the chlor-alkali market. These regions are witnessing significant investments in chemical production facilities, textile industries, and other sectors that rely heavily on caustic soda and chlorine. The inherent versatility and foundational role of chlor-alkali products across a multitude of industrial applications ensure their sustained relevance and demand, acting as a consistent growth engine for the market.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand from End-Use Industries (Chemicals, Pulp & Paper, Water Treatment) | +1.2% | Global | Short-Medium Term |

| Increasing PVC Consumption in Construction & Automotive | +0.8% | Asia Pacific, North America | Medium Term |

| Rising Focus on Water & Wastewater Treatment | +0.6% | North America, Europe, Asia Pacific | Medium-Long Term |

| Industrialization and Urbanization in Emerging Economies | +0.9% | Asia Pacific, Latin America | Short-Medium Term |

Chlor Alkali Market Restraints Analysis

The Chlor Alkali market faces notable restraints, primarily stemming from its energy-intensive production process, which makes it highly susceptible to fluctuations in electricity prices. Manufacturing caustic soda and chlorine consumes substantial amounts of electricity, and any volatility in energy markets directly impacts production costs and profitability. This vulnerability is particularly pronounced in regions heavily reliant on fossil fuels for power generation, where energy prices can be unpredictable, creating significant financial pressure on manufacturers and potentially hindering market expansion.

Furthermore, stringent environmental regulations and concerns about the ecological impact of chlorine and its byproducts pose a significant restraint. Governments worldwide are imposing stricter limits on emissions, waste disposal, and the use of certain chemicals, pushing manufacturers to invest in costly upgrades to comply with these standards. The phase-out of mercury cell technology, for instance, in favor of more environmentally friendly membrane cell technology, while beneficial for sustainability, requires substantial capital expenditure and can slow down production capacity growth in the short term. These regulatory hurdles can increase operational complexities and compliance costs for market players.

Another challenge includes the volatility of raw material prices, particularly salt (sodium chloride), which is a key input. Although salt is abundant, logistics and processing costs can vary, affecting overall production expenses. Additionally, the mature nature of some traditional applications in developed economies can lead to slower growth rates compared to emerging markets, presenting a geographical imbalance in market dynamism. Overcapacity in certain segments or regions can also lead to price erosion and reduced profit margins, making it difficult for new entrants and challenging for existing players to maintain market share and profitability.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Energy Consumption & Volatile Electricity Prices | -0.7% | Global, especially Europe | Short-Medium Term |

| Stringent Environmental Regulations and Emission Standards | -0.5% | Europe, North America | Medium-Long Term |

| Fluctuating Raw Material (Salt) Prices | -0.3% | Global | Short Term |

| Overcapacity in Certain Regional Markets | -0.4% | Asia Pacific | Short-Medium Term |

Chlor Alkali Market Opportunities Analysis

Significant opportunities in the Chlor Alkali market are emerging from the growing global emphasis on sustainable practices and the circular economy. The development of advanced, energy-efficient membrane cell technologies presents a key avenue for market players to reduce operational costs, enhance environmental performance, and gain a competitive edge. These technologies not only consume less energy but also produce higher-purity products and eliminate hazardous byproducts associated with older methods, aligning with global sustainability goals. Investing in research and development for these advanced processes can unlock new markets and improve profit margins.

The increasing demand for green hydrogen production, where chlorine is a byproduct, offers another substantial opportunity. As the world transitions towards cleaner energy sources, hydrogen is gaining prominence as a fuel and industrial feedstock. Chlor-alkali plants can be integrated into hydrogen production facilities, creating a symbiotic relationship that maximizes resource utilization and revenue streams. This synergy allows for the co-production of valuable chemicals while contributing to the burgeoning hydrogen economy, positioning chlor-alkali producers at the forefront of the green energy revolution.

Furthermore, the expansion of chemical manufacturing and infrastructure in rapidly developing economies, particularly across Asia Pacific and Latin America, presents immense growth prospects. These regions are characterized by a burgeoning middle class, increasing industrial output, and significant investments in urban development, all of which fuel the demand for chlor-alkali products. Strategic partnerships, capacity expansions, and localized production in these high-growth areas can enable market participants to capture a larger share and capitalize on robust regional demand, diversifying their market presence and revenue base.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Advancements in Energy-Efficient Membrane Cell Technology | +0.9% | Global | Medium-Long Term |

| Growing Demand for Green Hydrogen Production (Co-product) | +1.1% | Europe, North America, Asia Pacific | Long Term |

| Expansion of Chemical Industry in Emerging Economies | +0.7% | Asia Pacific, Latin America | Short-Medium Term |

| Development of New Applications in Specialized Chemical Production | +0.6% | Global | Medium Term |

Chlor Alkali Market Challenges Impact Analysis

The Chlor Alkali market faces significant challenges, notably the intense competition from existing producers and the threat of substitutes. The market is mature in several segments, leading to strong competition among established players who vie for market share through pricing strategies and production efficiencies. This competitive landscape can suppress profit margins, particularly during periods of oversupply. Moreover, the emergence of alternative technologies or materials that can perform similar functions to chlor-alkali products, albeit at a different cost or environmental profile, poses a long-term threat to traditional demand bases.

Another major challenge is the increasing regulatory scrutiny and public pressure concerning the environmental and health impacts of chlorine and its derivatives. Governments are progressively tightening regulations on emissions, waste management, and the transportation of hazardous chemicals, requiring significant investments in compliance and safety measures. This pressure extends beyond production to the entire supply chain, including storage and distribution, adding layers of complexity and cost for manufacturers. Companies must continuously adapt to evolving regulatory frameworks, which can vary significantly across regions, making global operations particularly complex.

Furthermore, managing the logistics and safe handling of hazardous materials such as chlorine presents an ongoing operational challenge. Chlorine is highly corrosive and toxic, necessitating specialized transportation, storage, and safety protocols to prevent accidents and environmental contamination. Any breach in these protocols can lead to severe penalties, reputational damage, and operational disruptions. The high capital expenditure required for setting up and upgrading chlor-alkali plants, coupled with the long gestation periods for such investments, also acts as a significant barrier to entry and expansion, further concentrating market power among a few large players.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Competition and Threat from Substitutes | -0.6% | Global | Medium-Long Term |

| Increasing Regulatory Scrutiny on Hazardous Chemicals | -0.8% | Europe, North America, Global | Medium Term |

| High Capital Expenditure for Plant Setup and Upgrades | -0.5% | Global | Long Term |

| Volatile Geopolitical Landscape Affecting Supply Chains | -0.4% | Global | Short Term |

Chlor Alkali Market - Updated Report Scope

This report provides an in-depth analysis of the Chlor Alkali market, encompassing historical data, current market dynamics, and future projections. It delivers comprehensive insights into market size, growth drivers, restraints, opportunities, and challenges, along with detailed segmentation and regional breakdowns to offer a holistic view of the industry landscape.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 65.8 Billion |

| Market Forecast in 2033 | USD 99.5 Billion |

| Growth Rate | 5.2% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Olin Corporation, Westlake Chemical Corporation, Tata Chemicals Limited, Shin-Etsu Chemical Co., Ltd., Formosa Plastics Corporation, Solvay S.A., Dow Inc., BASF SE, Reliance Industries Limited, AGC Inc., Hanwha Chemical Corporation, PT Asahimas Chemical, Nippon Soda Co., Ltd., Tosoh Corporation, Gujarat Alkalies and Chemicals Limited (GACL), Kemira Oyj, Ercros S.A., DCM Shriram Ltd., INOVYN (a part of Syensqo), AkzoNobel N.V. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Chlor Alkali market is comprehensively segmented by product type, application, and technology, reflecting the diverse nature of its output and end-user base. This granular segmentation allows for a detailed understanding of market dynamics, revealing which specific products, applications, or technologies are driving growth and where future opportunities lie. Analyzing these segments provides critical insights into the underlying demand drivers and technological shifts influencing the industry's trajectory. Each segment contributes uniquely to the overall market landscape, with varying growth rates and regional significance, necessitating a thorough examination for strategic planning.

The product segment, including caustic soda, chlorine, soda ash, and hydrogen, highlights the core chemical outputs of the chlor-alkali process, each serving distinct industrial purposes. Caustic soda, for example, is vital in alumina, pulp and paper, and textile industries, while chlorine is indispensable for PVC production, water treatment, and various organic and inorganic chemical syntheses. Understanding the demand trends within each product category is crucial for manufacturers to optimize production capacities and diversify their product portfolios.

Technology segmentation underscores the industry's evolution towards more efficient and environmentally friendly production methods, with membrane cell technology increasingly dominating the landscape over older, less sustainable diaphragm and mercury cell technologies. Furthermore, the application segment elucidates the broad utility of chlor-alkali products across a multitude of industries, ranging from heavy manufacturing to food processing, showcasing the market's fundamental importance to the global economy. Identifying high-growth applications allows market players to focus their expansion strategies and innovation efforts where demand is most robust.

- By Product: Caustic Soda (Liquid, Solid, Flakes), Chlorine (Gas, Liquid), Soda Ash, Hydrogen

- By Application: Pulp & Paper, Water Treatment, PVC Production, Organic Chemicals, Inorganic Chemicals, Textiles, Aluminum, Soaps & Detergents, Food & Beverages, Others

- By Technology: Membrane Cell, Diaphragm Cell, Mercury Cell

Regional Highlights

The Chlor Alkali market exhibits significant regional disparities in terms of production capacity, consumption patterns, and regulatory environments, making a geographical analysis crucial for understanding global market dynamics. Asia Pacific stands out as the largest and fastest-growing region, driven by rapid industrialization, urbanization, and a burgeoning manufacturing sector, particularly in countries like China and India. The region's expanding chemical industry, coupled with increasing infrastructure development and textile production, fuels a robust demand for chlor-alkali products. Significant investments in new production facilities and technological upgrades are commonplace, reflecting the region's pivotal role in global supply chains.

North America and Europe represent mature markets with established production capacities and stringent environmental regulations. While growth rates may be slower compared to Asia Pacific, these regions are at the forefront of technological innovation, particularly in adopting energy-efficient membrane cell technology and developing sustainable production practices. The emphasis here is on modernization, compliance with environmental standards, and optimizing existing facilities to maintain competitiveness. The demand for chlor-alkali in these regions is stable, supported by well-developed end-use industries such as chemical processing, water treatment, and pulp and paper.

Latin America and the Middle East & Africa (MEA) are emerging as regions with substantial growth potential. Latin America's market is driven by expanding agricultural and chemical sectors, alongside investments in infrastructure. The MEA region benefits from its abundant energy resources and ongoing industrial diversification initiatives, particularly in petrochemicals and water desalination, creating new avenues for chlor-alkali consumption. These regions are increasingly attractive for foreign investment and capacity expansion, as they offer growing demand and, in some cases, less stringent regulatory frameworks compared to developed economies, presenting unique opportunities for market penetration and growth.

- Asia Pacific: Dominant market share due to rapid industrialization, high demand from chemical and textile industries, and significant infrastructure development in China and India.

- North America: Stable market with strong demand from water treatment and PVC manufacturing, coupled with a focus on advanced, sustainable production technologies.

- Europe: Characterized by stringent environmental regulations driving the adoption of green technologies and a mature industrial base with consistent demand from various sectors.

- Latin America: Emerging market with growth fueled by expanding agricultural, chemical, and construction sectors, offering new opportunities for market players.

- Middle East & Africa (MEA): Growth driven by investments in petrochemicals, water desalination, and industrial diversification, leveraging abundant energy resources.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Chlor Alkali Market.- Olin Corporation

- Westlake Chemical Corporation

- Tata Chemicals Limited

- Shin-Etsu Chemical Co., Ltd.

- Formosa Plastics Corporation

- Solvay S.A.

- Dow Inc.

- BASF SE

- Reliance Industries Limited

- AGC Inc.

- Hanwha Chemical Corporation

- PT Asahimas Chemical

- Nippon Soda Co., Ltd.

- Tosoh Corporation

- Gujarat Alkalies and Chemicals Limited (GACL)

- Kemira Oyj

- Ercros S.A.

- DCM Shriram Ltd.

- INOVYN (a part of Syensqo)

- AkzoNobel N.V.

Frequently Asked Questions

What are the primary products of the Chlor Alkali process?

The primary products of the Chlor Alkali process are caustic soda (sodium hydroxide) and chlorine gas. These two fundamental chemicals are produced simultaneously through the electrolysis of a salt (sodium chloride) solution, alongside hydrogen gas as a co-product. These outputs serve as essential building blocks for a vast range of industrial applications.

What are the main applications of Chlor Alkali products?

Chlor Alkali products, particularly caustic soda and chlorine, have diverse applications across numerous industries. Caustic soda is crucial for the pulp and paper industry, alumina production, textile processing, and soap and detergent manufacturing. Chlorine is primarily used in PVC production, water treatment (disinfection), and the synthesis of organic and inorganic chemicals.

How has technology impacted Chlor Alkali production?

Technological advancements have significantly impacted Chlor Alkali production, with a notable shift from older mercury cell and diaphragm cell technologies to more energy-efficient and environmentally friendly membrane cell technology. Membrane cell technology offers improved product purity, reduced energy consumption, and eliminates hazardous byproducts like mercury, aligning with global sustainability goals.

What are the key drivers for Chlor Alkali market growth?

Key drivers for Chlor Alkali market growth include the increasing demand from end-use industries such as chemical processing, pulp and paper, and water treatment. Growing urbanization and infrastructure development, particularly the rising consumption of PVC in construction, also fuel demand. Additionally, expanding industrialization in emerging economies significantly contributes to market expansion.

What are the environmental concerns associated with the Chlor Alkali industry?

Environmental concerns in the Chlor Alkali industry primarily revolve around the energy-intensive nature of production, greenhouse gas emissions, and the potential release of hazardous chemicals like chlorine. Historically, mercury cell technology posed risks of mercury contamination. The industry is actively addressing these concerns through the adoption of cleaner technologies, waste reduction, and stringent environmental regulations to minimize ecological impact.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted