Cervical Cancer Diagnostic Market

Cervical Cancer Diagnostic Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707834 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

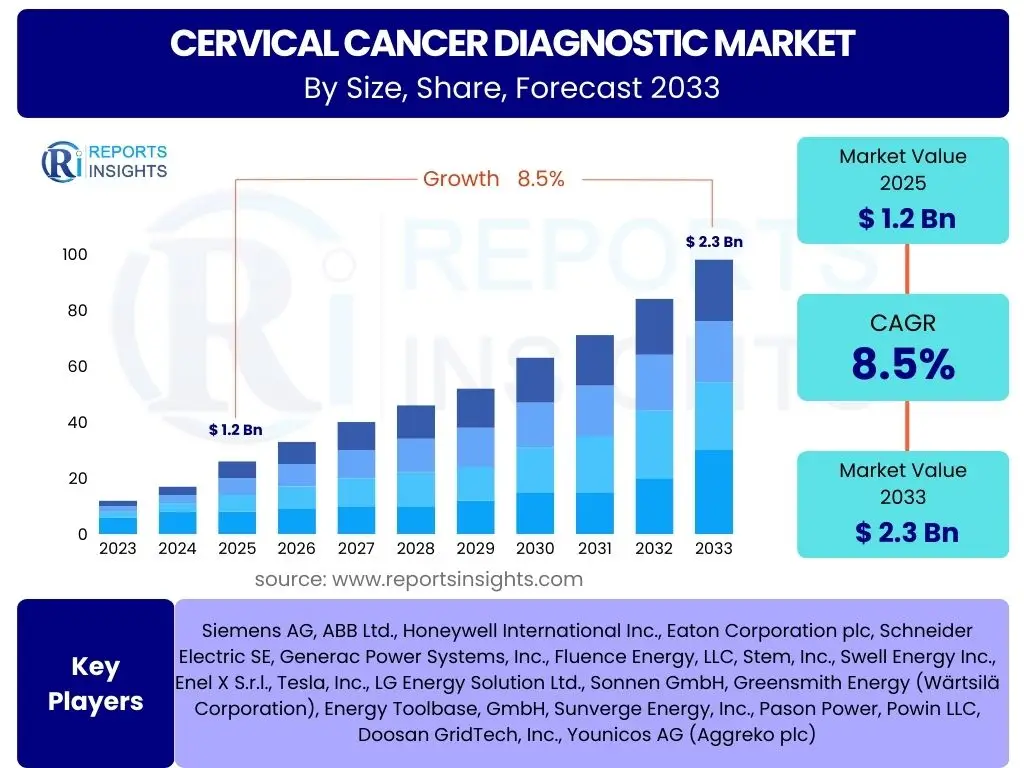

Cervical Cancer Diagnostic Market Size

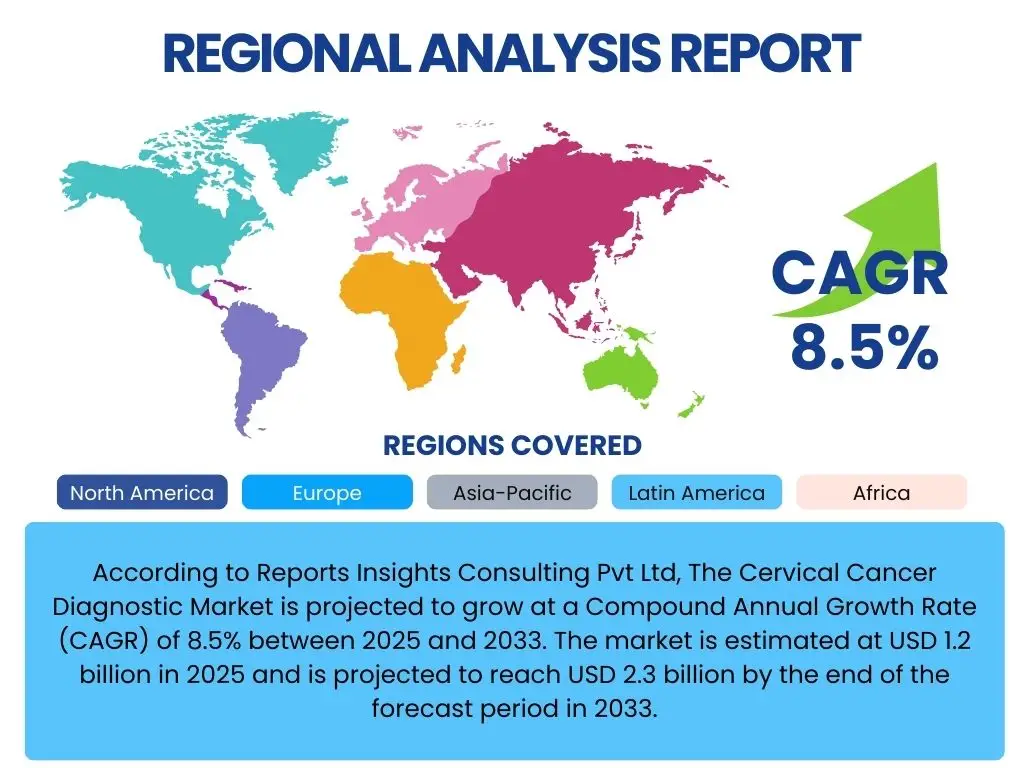

According to Reports Insights Consulting Pvt Ltd, The Cervical Cancer Diagnostic Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2025 and 2033. The market is estimated at USD 1.2 billion in 2025 and is projected to reach USD 2.3 billion by the end of the forecast period in 2033.

Key Cervical Cancer Diagnostic Market Trends & Insights

The Cervical Cancer Diagnostic market is experiencing a significant transformation driven by advancements in medical technology and increasing global awareness. A predominant trend observed is the shift towards more sensitive, specific, and less invasive diagnostic methods. This includes the widespread adoption of Human Papillomavirus (HPV) co-testing alongside traditional Pap smears, reflecting a deeper understanding of the causative agents of cervical cancer. The integration of molecular diagnostics is revolutionizing early detection, moving beyond cytological abnormalities to identify high-risk viral genotypes, thereby allowing for earlier intervention and improved patient outcomes.

Furthermore, there is a growing emphasis on point-of-care (POC) testing solutions, particularly in low-resource settings, to overcome infrastructure challenges and improve accessibility. These innovations aim to streamline diagnostic workflows, reduce turnaround times, and lower the overall burden on healthcare systems. Personalized medicine approaches are also beginning to influence diagnostic strategies, with a focus on tailoring screening intervals and diagnostic pathways based on individual risk factors and genetic predispositions, promising a future of highly efficient and patient-centric cervical cancer screening programs. The market is increasingly investing in automated and high-throughput screening technologies to manage the large volume of tests globally, enhancing efficiency and accuracy while minimizing human error.

- Increased adoption of HPV DNA testing and co-testing with Pap smears.

- Development of non-invasive and minimally invasive diagnostic techniques, including liquid biopsy.

- Rising demand for point-of-care (POC) diagnostic devices, particularly in developing regions.

- Integration of artificial intelligence and machine learning for enhanced image analysis and predictive diagnostics.

- Focus on automation and high-throughput screening solutions to improve laboratory efficiency.

- Emergence of biomarker-based diagnostics for improved risk stratification and prognosis.

AI Impact Analysis on Cervical Cancer Diagnostic

Artificial intelligence (AI) is rapidly emerging as a transformative force within the cervical cancer diagnostic landscape, promising to revolutionize screening, detection, and prognosis. Users frequently inquire about AI's ability to enhance accuracy, reduce subjectivity, and improve workflow efficiency in cytology and histology. AI algorithms are being developed and validated to analyze complex microscopic images from Pap smears and biopsies with remarkable precision, often surpassing human capabilities in detecting subtle cellular anomalies. This computational power helps to alleviate the workload of pathologists, address the shortage of skilled personnel, and standardize diagnostic interpretation across different laboratories, thereby reducing inter-observer variability and potential misdiagnoses. The integration of AI also extends to predictive analytics, where models can assess an individual's risk of developing cervical cancer based on various clinical, demographic, and genetic factors.

The primary benefit of AI in this field lies in its capacity for early and more accurate detection, which is crucial for successful treatment outcomes. AI-powered systems can flag suspicious slides for immediate review, prioritize high-risk cases, and even provide real-time diagnostic assistance during colposcopy. However, concerns regarding data privacy, the need for extensive, diverse training datasets, regulatory approval processes, and the ethical implications of relying on automated systems are frequently raised. Users also express interest in how AI can facilitate access to screening in remote or underserved areas by enabling remote diagnostics and improving the efficiency of existing diagnostic programs. Overcoming these challenges will be critical for the widespread adoption and successful integration of AI into routine clinical practice, ultimately leading to improved global cervical cancer prevention and control efforts.

- Enhanced image analysis for Pap smears and histopathology slides, improving detection accuracy and reducing false negatives.

- Automated screening and prioritization of high-risk samples, optimizing laboratory workflow and addressing personnel shortages.

- Development of predictive models for identifying individuals at higher risk of cervical cancer progression.

- Facilitation of remote diagnostics and telemedicine, expanding access to screening in underserved regions.

- Personalized treatment planning through AI-driven analysis of patient-specific data.

- Challenges include regulatory approval, data privacy concerns, and the need for robust validation datasets.

Key Takeaways Cervical Cancer Diagnostic Market Size & Forecast

The Cervical Cancer Diagnostic market is poised for robust growth, primarily fueled by the increasing global incidence of cervical cancer and a heightened emphasis on early detection and prevention. A critical insight derived from market analysis is the accelerating shift from traditional cytology-based screening towards more advanced molecular and biomarker-driven diagnostic methods, particularly HPV DNA testing. This transition reflects a broader recognition of the superior sensitivity and predictive value offered by these newer technologies, leading to more accurate diagnoses and better patient stratification. The market forecast underscores a sustained demand for innovative diagnostic solutions that can enhance screening efficacy, reduce diagnostic timelines, and improve accessibility, especially in regions with high disease burden and limited healthcare infrastructure.

Furthermore, technological advancements, including the advent of artificial intelligence in image analysis and the development of point-of-care testing, are significant catalysts driving market expansion. These innovations are not only improving the precision of diagnostics but also addressing operational challenges such as the shortage of trained personnel and the high volume of samples requiring analysis. The market's growth trajectory is also strongly influenced by global health initiatives and government-backed screening programs aimed at reducing cervical cancer mortality. Stakeholders should focus on developing cost-effective, scalable, and user-friendly diagnostic platforms to capitalize on the burgeoning opportunities in both established and emerging economies, ensuring widespread adoption and impact.

- Strong market growth driven by increasing cervical cancer prevalence and global health initiatives.

- Dominance and continued expansion of HPV testing and molecular diagnostics over traditional methods.

- Significant impact of technological innovation, including AI and point-of-care solutions, on market dynamics.

- Increasing focus on early detection and prevention as key strategies to reduce mortality rates.

- Growing demand for accessible and affordable diagnostic solutions, particularly in developing regions.

Cervical Cancer Diagnostic Market Drivers Analysis

The Cervical Cancer Diagnostic market is propelled by a confluence of powerful drivers, with the escalating global incidence and prevalence of cervical cancer standing as a primary catalyst. As the disease continues to pose a significant public health challenge worldwide, particularly in developing nations, the imperative for effective and widespread diagnostic tools becomes increasingly critical. This heightened disease burden naturally fosters greater investment in research and development, leading to the introduction of novel and improved diagnostic technologies. Moreover, governmental and non-governmental organizations are intensifying their efforts to implement national and regional cervical cancer screening programs, which significantly boosts the demand for diagnostic tests and associated services. These initiatives often include awareness campaigns that educate women about the importance of regular screening, further driving market expansion.

Another pivotal driver is the continuous advancement in diagnostic technologies. Innovations such as high-throughput HPV testing, liquid biopsy techniques, and the integration of artificial intelligence into pathology are transforming the diagnostic landscape. These technological leaps offer higher sensitivity, specificity, and efficiency, making early detection more reliable and accessible. The shift towards molecular diagnostics, which can detect the presence of oncogenic HPV strains before cellular changes occur, represents a paradigm shift from solely relying on cytological screening. Furthermore, a growing global awareness among women about cervical cancer, its causes, and the benefits of early screening empowers them to seek diagnostic services proactively, contributing significantly to market growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rising Incidence of Cervical Cancer Globally | +2.0% | Asia Pacific, Africa, Latin America | Long-term (2025-2033) |

| Technological Advancements in Diagnostic Methods | +1.8% | North America, Europe, Developed Asia Pacific | Mid to Long-term (2025-2033) |

| Increasing Awareness and Government Screening Programs | +1.5% | Global, particularly Emerging Economies | Mid to Long-term (2025-2033) |

| Growing Adoption of HPV Co-testing and Molecular Diagnostics | +1.2% | Global | Mid to Long-term (2025-2033) |

| Expansion of Healthcare Infrastructure and Access | +1.0% | Developing Regions (APAC, MEA, LATAM) | Long-term (2027-2033) |

Cervical Cancer Diagnostic Market Restraints Analysis

Despite the robust growth trajectory, the Cervical Cancer Diagnostic market faces several significant restraints that could impede its full potential. A primary challenge is the high cost associated with advanced diagnostic technologies, particularly molecular tests and automated systems. These expenses can be prohibitive for healthcare systems in low- and middle-income countries, where the burden of cervical cancer is often highest, limiting widespread adoption and accessibility. Furthermore, even in developed economies, budgetary constraints within public health programs can restrict the frequency and breadth of screening initiatives, slowing market penetration of newer, albeit more effective, diagnostic tools. The economic barrier remains a critical hurdle that requires innovative solutions to ensure equitable access to diagnostics globally.

Another substantial restraint is the lack of adequate healthcare infrastructure and skilled personnel, particularly in remote and underserved regions. The proper collection, processing, and interpretation of cervical cancer diagnostic samples, especially those involving cytology and colposcopy, demand trained professionals and well-equipped laboratories. Shortages of pathologists, cytotechnologists, and gynecologists can lead to delays in diagnosis, compromised test quality, and reduced screening coverage. Moreover, the social stigma associated with gynecological examinations and sexually transmitted infections (like HPV) can deter women from seeking screening services, even when available, posing a behavioral restraint that impacts compliance rates. Addressing these multifaceted challenges requires a combination of technological innovation, investment in healthcare infrastructure, and public health education campaigns.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of Advanced Diagnostic Technologies | -1.5% | Global, especially Low-Income Countries | Long-term (2025-2033) |

| Lack of Adequate Healthcare Infrastructure and Skilled Professionals | -1.2% | Africa, Rural Asia Pacific, Latin America | Long-term (2025-2033) |

| Social Stigma and Cultural Barriers to Screening | -0.8% | Certain Regions in Asia Pacific, MEA, LATAM | Long-term (2025-2033) |

| Regulatory Hurdles and Lengthy Approval Processes | -0.7% | Global, specific to new technologies | Mid-term (2025-2029) |

| False Positives/Negatives and Inter-observer Variability | -0.5% | Global, particularly traditional methods | Mid-term (2025-2029) |

Cervical Cancer Diagnostic Market Opportunities Analysis

The Cervical Cancer Diagnostic market presents several compelling opportunities for growth and innovation, driven by evolving healthcare needs and technological advancements. A significant opportunity lies in the development and widespread adoption of point-of-care (POC) diagnostic devices. These compact, rapid-testing solutions can revolutionize screening in remote areas and low-resource settings, where access to centralized laboratories is limited. POC tests, such as rapid HPV assays or visual inspection with acetic acid (VIA) enhanced by digital imaging, offer immediate results, enabling same-day treatment decisions and reducing patient follow-up loss, which is a major barrier to effective screening programs. The increasing emphasis on decentralized healthcare delivery models further amplifies the potential for these accessible diagnostic tools.

Another burgeoning opportunity is the integration of advanced molecular diagnostics, including liquid biopsy and biomarker-based tests. Liquid biopsy, which involves analyzing circulating tumor DNA (ctDNA) or other biomarkers in blood, offers a non-invasive alternative for detecting cervical cancer recurrence or monitoring treatment response, especially in cases where tissue biopsies are challenging. Furthermore, the application of artificial intelligence and machine learning in analyzing cytology and histopathology images, as well as in predicting disease progression, represents a vast untapped potential. These AI-driven solutions can significantly improve diagnostic accuracy, reduce the workload of pathologists, and enable personalized risk stratification. Additionally, expanding market penetration into emerging economies, characterized by large underserved populations and improving healthcare expenditure, provides substantial growth avenues for companies offering affordable and scalable diagnostic solutions.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development and Adoption of Point-of-Care (POC) Testing | +1.8% | Emerging Economies, Rural Areas Globally | Mid to Long-term (2026-2033) |

| Integration of AI and Machine Learning in Diagnostics | +1.6% | Developed Countries, Research-focused Regions | Mid to Long-term (2026-2033) |

| Emergence of Liquid Biopsy and Novel Biomarkers | +1.4% | Global, particularly in Research and Specialty Clinics | Long-term (2027-2033) |

| Market Penetration into Underserved Emerging Economies | +1.3% | Asia Pacific, Africa, Latin America | Long-term (2025-2033) |

| Government and NGO Initiatives for Mass Screening Programs | +1.0% | Global, particularly in Low-Resource Settings | Long-term (2025-2033) |

Cervical Cancer Diagnostic Market Challenges Impact Analysis

The Cervical Cancer Diagnostic market faces several inherent challenges that demand strategic attention from industry stakeholders and public health policymakers. A significant hurdle is the complex regulatory landscape governing diagnostic devices and tests, which varies considerably across different countries and regions. Stringent approval processes, coupled with evolving guidelines for new technologies like AI-powered diagnostics or novel molecular assays, can lead to prolonged development timelines and substantial costs for manufacturers. This regulatory burden can delay market entry for innovative solutions, ultimately hindering widespread patient access and slowing the pace of diagnostic improvement. Harmonization of regulatory standards and streamlined approval pathways are critical to overcoming this challenge.

Another major challenge involves ensuring data privacy and security, especially with the increasing digitalization of patient records and the use of AI for analyzing sensitive health information. Protecting patient confidentiality while leveraging large datasets for diagnostic development and validation is a delicate balance. Furthermore, disparities in healthcare access and quality, particularly between urban and rural areas or developed and developing nations, present a persistent challenge. Even when diagnostic technologies are available, the lack of trained healthcare professionals, inadequate infrastructure, and limited financial resources can impede their effective implementation and utilization, perpetuating inequalities in cervical cancer outcomes. Addressing these challenges requires a multi-pronged approach encompassing policy reforms, investment in infrastructure, workforce training, and ethical data governance frameworks.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Regulatory Landscape and Approval Processes | -1.0% | Global | Mid-term (2025-2030) |

| Data Privacy and Security Concerns with Digital Diagnostics | -0.8% | Global, particularly Developed Countries | Long-term (2025-2033) |

| Lack of Skilled Professionals for Advanced Technologies | -0.7% | Emerging Economies, Rural Areas | Long-term (2025-2033) |

| Disparities in Healthcare Access and Infrastructure | -0.6% | Africa, parts of Asia Pacific and Latin America | Long-term (2025-2033) |

| Ethical Considerations in AI Deployment for Diagnosis | -0.5% | Global | Mid to Long-term (2026-2033) |

Cervical Cancer Diagnostic Market - Updated Report Scope

This report provides a comprehensive and in-depth analysis of the Cervical Cancer Diagnostic market, offering a detailed understanding of its current size, historical performance, and future growth projections. It encapsulates key market dynamics, including drivers, restraints, opportunities, and challenges, along with a thorough examination of the impact of artificial intelligence. The scope extends to a detailed segmentation analysis across various parameters, offering granular insights into market segments and sub-segments, and highlights regional market performance and trends. The report also profiles leading companies, providing strategic insights for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.2 Billion |

| Market Forecast in 2033 | USD 2.3 Billion |

| Growth Rate | 8.5% CAGR |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Hologic, Inc., QIAGEN N.V., F. Hoffmann-La Roche Ltd., BD (Becton, Dickinson and Company), Abbott Laboratories, Danaher Corporation (Leica Biosystems), Thermo Fisher Scientific Inc., Quest Diagnostics Incorporated, Bio-Rad Laboratories, Inc., Siemens Healthineers AG, Dako (Agilent Technologies), Arbor Vita Corporation, Nipro Corporation, Advancells, Illumina, Inc., Exact Sciences Corporation, Cepheid (Danaher Corporation), Konica Minolta, Inc., GenMark Diagnostics, Inc., mdxhealth |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Cervical Cancer Diagnostic market is intricately segmented across various dimensions to provide a granular understanding of its structure and evolving dynamics. This comprehensive segmentation allows for a detailed analysis of market performance based on specific test types, products, technologies, end-users, and age groups. Each segment plays a crucial role in shaping the overall market, with distinct growth drivers and trends influencing their individual trajectories. Understanding these segmentations is vital for identifying key areas of investment, strategic planning, and targeted market penetration for various stakeholders.

- By Test Type: Pap Smear, HPV DNA Test, Colposcopy, Biopsy, Visual Inspection with Acetic Acid (VIA), Liquid Biopsy, Others

- By Product: Instruments, Kits & Reagents, Software & Services

- By Technology: Cytology-based Testing, Molecular-based Testing, Imaging-based Diagnosis

- By End-User: Hospitals, Diagnostic Centers, Specialty Clinics, Research & Academic Institutes, Public Health Laboratories

- By Age Group: Below 30 Years, 30-49 Years, Above 50 Years

Regional Highlights

- North America: Expected to maintain a dominant share due to advanced healthcare infrastructure, high awareness, favorable reimbursement policies, and early adoption of innovative diagnostic technologies. Significant research and development activities also contribute to its leading position.

- Europe: Characterized by established screening programs, increasing government funding for cancer research, and the presence of key market players. Growth is driven by the adoption of molecular diagnostics and a focus on improving screening coverage and efficiency.

- Asia Pacific (APAC): Projected to be the fastest-growing region, owing to the large population base, rising incidence of cervical cancer, improving healthcare expenditure, increasing awareness programs, and expanding access to diagnostic facilities in countries like China and India.

- Latin America: Demonstrates steady growth potential, driven by increasing awareness, improving healthcare access, and efforts to implement national screening programs, though challenges in infrastructure and affordability persist.

- Middle East and Africa (MEA): Represents an emerging market with significant untapped potential. Growth is anticipated due to rising awareness campaigns, improving healthcare infrastructure in select countries, and international collaborations aimed at combating cervical cancer.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Cervical Cancer Diagnostic Market.- Hologic, Inc.

- QIAGEN N.V.

- F. Hoffmann-La Roche Ltd.

- BD (Becton, Dickinson and Company)

- Abbott Laboratories

- Danaher Corporation (Leica Biosystems)

- Thermo Fisher Scientific Inc.

- Quest Diagnostics Incorporated

- Bio-Rad Laboratories, Inc.

- Siemens Healthineers AG

- Dako (Agilent Technologies)

- Arbor Vita Corporation

- Nipro Corporation

- Advancells

- Illumina, Inc.

- Exact Sciences Corporation

- Cepheid (Danaher Corporation)

- Konica Minolta, Inc.

- GenMark Diagnostics, Inc.

- mdxhealth

Frequently Asked Questions

What is cervical cancer and how is it primarily diagnosed?

Cervical cancer is a type of cancer that starts in the cells of the cervix, the lower part of the uterus that connects to the vagina. It is most often caused by long-term infection with certain types of human papillomavirus (HPV). Primary diagnosis typically involves screening tests such as the Pap smear (Papanicolaou test) and HPV DNA testing, which detect abnormal cells or the presence of high-risk HPV, respectively.

What are the key diagnostic methods for cervical cancer?

The primary diagnostic methods include the Pap smear, which examines cervical cells for abnormalities; HPV DNA testing, which identifies the presence of high-risk HPV strains; colposcopy, a procedure using a magnified view of the cervix to identify abnormal areas; and biopsies, where tissue samples are taken for microscopic examination to confirm cancer.

Is HPV testing more effective than the Pap Smear for cervical cancer screening?

HPV testing is generally considered more sensitive than a Pap smear for detecting high-risk HPV infections that cause cervical cancer. While Pap smears detect abnormal cell changes, HPV tests directly identify the virus. Many guidelines now recommend co-testing (both Pap and HPV tests) or primary HPV screening as they offer a more comprehensive and effective approach to early detection and risk stratification.

How is Artificial Intelligence (AI) being used in cervical cancer diagnosis?

AI is being utilized to enhance the accuracy and efficiency of cervical cancer diagnosis by analyzing cytology and histopathology images, identifying subtle cellular abnormalities that might be missed by the human eye. AI algorithms can also help in automating screening processes, prioritizing high-risk cases for immediate review, and developing predictive models for disease progression, thereby aiding in earlier detection and personalized treatment strategies.

What are the future trends in the cervical cancer diagnostic market?

Future trends include a continued shift towards molecular diagnostics and non-invasive methods like liquid biopsy, increased adoption of point-of-care (POC) testing, deeper integration of artificial intelligence and machine learning for enhanced analysis and automation, and a focus on personalized screening protocols based on individual risk factors and genetic profiles. There is also a strong drive towards expanding diagnostic accessibility in low-resource settings.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted