Calcined Anthracite Market

Calcined Anthracite Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709201 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

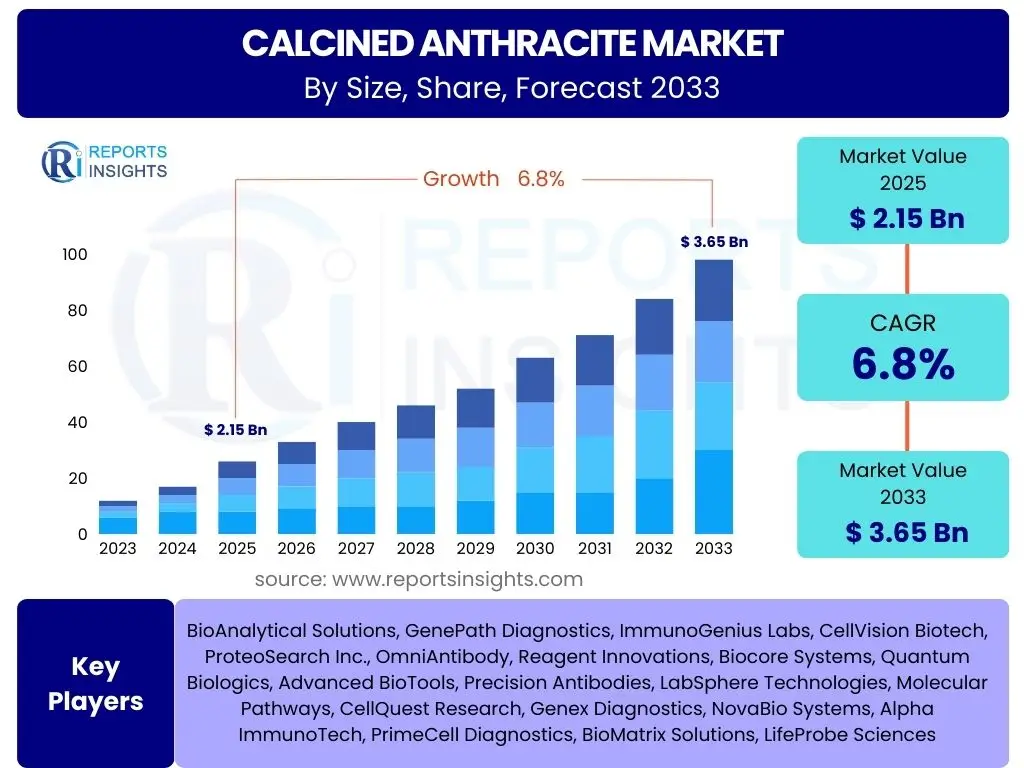

Calcined Anthracite Market Size

According to Reports Insights Consulting Pvt Ltd, The Calcined Anthracite Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 2.15 Billion in 2025 and is projected to reach USD 3.65 Billion by the end of the forecast period in 2033.

Key Calcined Anthracite Market Trends & Insights

The Calcined Anthracite market is currently experiencing several transformative trends, driven by evolving industrial demands and environmental considerations. Common user inquiries often revolve around the shift towards cleaner production processes, the increasing adoption of electric arc furnaces (EAFs) in steelmaking, and the growing demand for high-quality carbon materials in new applications. Users are particularly interested in how these trends influence pricing, supply chain stability, and the long-term sustainability of calcined anthracite as a critical industrial input. The market is increasingly focused on product customization to meet specific performance requirements in diverse end-use sectors.

Another significant area of user interest lies in the geographical redistribution of demand and production capabilities. With industrial growth shifting towards Asia Pacific, particularly China and India, there is a keen focus on local supply dynamics and trade flows. Users also frequently inquire about the impact of raw material availability, such as the quality and accessibility of metallurgical anthracite, and how these factors shape market competitiveness. Furthermore, the development of advanced calcination technologies aimed at reducing energy consumption and environmental footprint is a recurring theme, highlighting the industry's commitment to innovation and efficiency.

- Growing demand from electric arc furnaces (EAFs) in steel manufacturing.

- Increased focus on high-purity calcined anthracite for specialized applications.

- Shift towards sustainable and environmentally compliant production methods.

- Expansion of applications beyond traditional metallurgy, including water treatment.

- Consolidation of market players and strategic partnerships to secure raw material supply.

AI Impact Analysis on Calcined Anthracite

The integration of Artificial Intelligence (AI) within the Calcined Anthracite sector is a burgeoning area of interest for stakeholders, with users frequently posing questions about its potential to revolutionize operations. Key concerns and expectations center on AI's ability to optimize various stages of the value chain, from raw material procurement and processing to logistics and demand forecasting. Users envision AI facilitating more efficient resource utilization, reducing operational costs, and enhancing product consistency, which is crucial for high-specification applications of calcined anthracite. The precision afforded by AI-driven analytics is expected to lead to significant improvements in quality control and process efficiency.

Specifically, the impact of AI is anticipated in areas such as predictive maintenance for calcination kilns, optimizing energy consumption during the calcination process, and improving supply chain resilience through advanced data analytics. AI-powered systems can analyze vast datasets to predict market fluctuations, manage inventory levels more effectively, and identify potential bottlenecks before they arise. While the direct application of AI in the physical production of calcined anthracite might be limited to process control and optimization, its indirect influence on market intelligence, strategic planning, and operational efficiency is expected to be profound, making the industry more responsive and competitive.

- Optimization of raw material sourcing and inventory management through predictive analytics.

- Enhanced process control and energy efficiency in calcination kilns using AI algorithms.

- Improved quality control and consistency of calcined anthracite products.

- Advanced demand forecasting and supply chain management for reduced lead times.

- Implementation of predictive maintenance to minimize operational downtime and costs.

Key Takeaways Calcined Anthracite Market Size & Forecast

The Calcined Anthracite market is poised for robust growth over the forecast period, driven by fundamental shifts in industrial processes and increasing demand from key end-use sectors. User inquiries consistently highlight the importance of understanding the market's trajectory, particularly the underlying factors contributing to its expansion. The projected Compound Annual Growth Rate (CAGR) of 6.8% signals a healthy market environment, underpinned by the indispensable role of calcined anthracite in various high-value applications. The significant increase from USD 2.15 Billion in 2025 to USD 3.65 Billion by 2033 underscores the sustained reliance on this material and its expanding utility across industries.

A crucial takeaway is the resilience of the calcined anthracite market despite environmental scrutiny, primarily due to its unique properties and lack of immediate substitutes in many critical applications, especially in metallurgy. The forecast growth indicates that investments in new production capacities and technological advancements will be vital to meet future demand. Furthermore, the market's expansion will be heavily influenced by the pace of industrialization in emerging economies and the global transition towards more efficient and sustainable manufacturing practices that still require high-purity carbon sources. These elements combine to paint a picture of a stable yet dynamic market with significant opportunities for innovation and growth.

- Significant market growth projected with a CAGR of 6.8% from 2025 to 2033.

- Metallurgical industries, especially steel and aluminum, remain the primary growth drivers.

- Increasing emphasis on product purity and consistency to meet stringent industry standards.

- Emerging applications in water treatment and energy storage offer new revenue streams.

- Market expansion is highly dependent on global industrial production and infrastructure development.

Calcined Anthracite Market Drivers Analysis

The Calcined Anthracite market is predominantly driven by the robust demand from the global metallurgical industry, particularly steel and aluminum production. Calcined anthracite serves as a crucial recarburizer in steelmaking, contributing to the carbon content and quality of the final product. The ongoing expansion of global infrastructure projects, urbanization, and industrialization, especially in developing economies, directly fuels the demand for steel and aluminum, thereby boosting the consumption of calcined anthracite. The shift towards Electric Arc Furnaces (EAFs) in steel production, which often require high-quality carbon sources, further amplifies this demand.

Beyond traditional metallurgy, the growing need for water treatment solutions globally acts as a significant driver. Calcined anthracite is increasingly utilized as a filter media due to its excellent adsorption properties and chemical stability. The stringent environmental regulations concerning water quality and the scarcity of potable water resources are compelling municipalities and industrial sectors to adopt advanced filtration technologies, thereby creating new avenues for market growth. This diversification of applications, coupled with the consistent demand from core industries, establishes a strong foundation for the market's continued expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Steel and Aluminum Production | +1.5% | Asia Pacific, North America, Europe | Short-to-Medium Term (2025-2030) |

| Increasing Adoption of Electric Arc Furnaces (EAFs) | +1.2% | Global, particularly Europe, North America, China | Medium Term (2026-2031) |

| Rising Demand in Water Treatment Applications | +0.9% | Global, especially developing regions | Medium-to-Long Term (2027-2033) |

| Infrastructure Development & Urbanization | +1.0% | Asia Pacific, Latin America, MEA | Short-to-Medium Term (2025-2030) |

Calcined Anthracite Market Restraints Analysis

Despite its critical applications, the Calcined Anthracite market faces several significant restraints that could impede its growth trajectory. Environmental regulations, particularly those targeting carbon emissions and industrial pollution, pose a considerable challenge. The energy-intensive nature of the calcination process results in greenhouse gas emissions, leading to increased compliance costs and potential operational restrictions for producers. Stricter environmental policies in key manufacturing regions, such as Europe and North America, compel manufacturers to invest in costly abatement technologies or face production limitations, impacting profitability and market competitiveness.

Another major restraint is the availability and fluctuating prices of raw material, primarily high-grade anthracite. Anthracite mining is concentrated in specific regions, and geopolitical factors, labor disputes, and mining regulations can disrupt supply chains, leading to price volatility. Furthermore, the emergence of alternative carbon materials, such as petroleum coke or synthetic graphite, in certain applications presents a competitive threat. While calcined anthracite offers superior properties for specific uses, cost-effectiveness and increasing supply of alternatives could lead to substitution in less demanding applications, thereby restraining market expansion. The high capital expenditure required for setting up calcination plants also acts as a barrier to entry for new players.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Environmental Regulations | -0.8% | Europe, North America, China | Medium-to-Long Term (2027-2033) |

| Fluctuations in Raw Anthracite Prices and Availability | -0.6% | Global | Short-to-Medium Term (2025-2029) |

| Competition from Alternative Carbon Materials | -0.5% | Global | Medium Term (2026-2031) |

| High Energy Costs for Calcination | -0.4% | Global | Short Term (2025-2027) |

Calcined Anthracite Market Opportunities Analysis

The Calcined Anthracite market presents several compelling opportunities for growth and innovation, particularly through the exploration of new application areas and technological advancements. One significant opportunity lies in the burgeoning energy storage sector, specifically in the production of battery materials. As the demand for electric vehicles (EVs) and grid-scale energy storage solutions continues to surge, there is a growing need for high-purity carbon materials, where calcined anthracite could play a specialized role, especially in niche battery chemistries or as an additive. Research and development into these advanced applications could unlock substantial market value.

Furthermore, technological advancements in the calcination process itself offer opportunities for improved efficiency, reduced environmental impact, and lower production costs. Innovations in furnace design, heat recovery systems, and emission control technologies can enhance sustainability and operational profitability, making calcined anthracite more competitive. The increasing demand for specialized, ultra-high-purity calcined anthracite for sensitive industrial processes also creates premium market segments. Strategic collaborations with end-use industries to develop tailored products, coupled with market expansion into developing regions with growing industrial bases, represent further avenues for significant market growth.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Energy Storage (Battery Materials) | +1.2% | Global, particularly Asia Pacific, Europe | Medium-to-Long Term (2028-2033) |

| Technological Advancements in Calcination Processes | +0.8% | Global | Medium Term (2026-2031) |

| Development of High-Purity & Specialty Products | +0.7% | North America, Europe, Japan | Medium-to-Long Term (2027-2033) |

| Market Penetration in Emerging Economies | +1.0% | Asia Pacific, Latin America, Africa | Short-to-Medium Term (2025-2030) |

Calcined Anthracite Market Challenges Impact Analysis

The Calcined Anthracite market faces several inherent challenges that demand strategic responses from industry players. One significant challenge is the inherent volatility of raw material prices. Anthracite, as a mined commodity, is subject to global supply-demand dynamics, geopolitical tensions, and transport costs, leading to unpredictable price fluctuations. This instability makes it difficult for calcined anthracite producers to manage costs effectively and maintain stable pricing for their end products, impacting profitability and long-term planning. Ensuring a consistent supply of high-quality raw anthracite at competitive prices remains a perennial concern.

Another critical challenge is the intense competition from alternative carbon sources. While calcined anthracite holds a strong position in specific applications due to its unique properties, cheaper alternatives like petroleum coke can pose a threat in less stringent uses. Market players must continuously demonstrate the superior value proposition of calcined anthracite to counter this competition. Furthermore, the industry is grappling with the need to enhance its sustainability profile, particularly in reducing its carbon footprint. Investing in cleaner production technologies and adhering to evolving environmental standards while maintaining cost-effectiveness is a complex balancing act, representing a significant long-term challenge for the sector.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile Raw Material Prices (Anthracite) | -0.7% | Global | Short-to-Medium Term (2025-2029) |

| Intense Competition from Substitute Products | -0.6% | Global | Medium Term (2026-2031) |

| High Logistics and Transportation Costs | -0.5% | Global | Short Term (2025-2027) |

| Need for Sustainable Production Practices | -0.4% | Europe, North America | Medium-to-Long Term (2027-2033) |

Calcined Anthracite Market - Updated Report Scope

This report provides a comprehensive analysis of the global Calcined Anthracite market, offering in-depth insights into its size, growth drivers, restraints, opportunities, and challenges across various segments and regions. The study includes a detailed forecast from 2025 to 2033, examining historical trends from 2019 to 2023 to provide a holistic view of market dynamics. It aims to equip stakeholders with actionable intelligence to make informed strategic decisions.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.15 Billion |

| Market Forecast in 2033 | USD 3.65 Billion |

| Growth Rate | 6.8% CAGR |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Carbon Graphite International, Carbide Industries, Rio Tinto Alcan, RWE Supply & Trading, Anshan Iron and Steel Group, Shougang Group, Baosteel Group, POSCO, Nippon Steel & Sumitomo Metal, Gerdau S.A., ArcelorMittal, Glencore, Xcoal Energy & Resources, Anglo American, Peabody Energy, China Shenhua Energy Company, Coal India Limited, Siberian Anthracite, Reading Anthracite Company, Lehigh Anthracite |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Calcined Anthracite market is extensively segmented to provide granular insights into its diverse applications, end-use industries, and geographical spread. This segmentation allows for a detailed understanding of market dynamics, identifying specific areas of growth and opportunity. The primary segmentation categories include application, end-use industry, and geographic region, each offering unique perspectives on consumption patterns and market potential. This detailed breakdown facilitates targeted strategic planning and investment decisions for market participants.

The applications segment highlights the versatility of calcined anthracite, from its traditional role in metallurgy to emerging uses in environmental solutions and advanced materials. Simultaneously, the end-use industry segment provides clarity on the major industrial consumers and their specific requirements, which directly influence product specifications and market demand. Regional segmentation, on the other hand, underscores the geographical disparities in production, consumption, and regulatory environments, offering insights into localized market trends and growth drivers across different parts of the world.

- By Application:

- Carbon Electrode Production

- Water Treatment

- Metallurgical Industries

- Steel

- Aluminum

- Foundries

- Chemical Industries

- Battery Materials

- Other Industrial Applications

- By End-Use Industry:

- Steel Manufacturing

- Aluminum Smelting

- Foundries

- Chemical Processing

- Environmental Applications

- Energy Storage

- Other Manufacturing

- By Region:

- North America

- Europe

- Asia Pacific (APAC)

- Latin America

- Middle East & Africa (MEA)

Regional Highlights

The global Calcined Anthracite market exhibits significant regional variations in terms of demand, supply, and growth dynamics. Asia Pacific stands out as the dominant region and is projected to maintain the highest growth rate during the forecast period. This robust growth is primarily attributable to the rapid industrialization, extensive infrastructure development, and burgeoning manufacturing sectors, particularly steel and aluminum production, in countries like China and India. These nations are not only major producers but also the largest consumers of calcined anthracite, driven by their massive industrial bases and increasing urbanization. The region's expanding industrial footprint, coupled with lower production costs in certain areas, makes it a critical hub for the calcined anthracite market.

North America and Europe represent mature markets for calcined anthracite, characterized by stringent environmental regulations and a focus on high-quality, specialized applications. While the growth rate in these regions may be slower compared to Asia Pacific, demand remains stable due to the advanced metallurgical industries and increasing adoption of calcined anthracite in environmental applications, such as water filtration. The shift towards Electric Arc Furnaces (EAFs) in steel production in these regions further supports a steady demand for high-purity carbon materials. Innovation in sustainable production methods and advanced materials also originates significantly from these regions.

Latin America and the Middle East & Africa (MEA) are emerging markets with considerable growth potential. Latin America, particularly Brazil, benefits from its growing steel industry and infrastructure projects, driving demand for metallurgical inputs. The MEA region is witnessing increased investments in industrial development and mining activities, which are expected to boost the consumption of calcined anthracite in the long term. However, these regions often face challenges related to economic stability and the development of robust supply chain infrastructure, which can influence market penetration and growth rates.

Overall, the global landscape for calcined anthracite is characterized by a strong demand pull from Asia Pacific, sustained consumption in developed economies, and nascent but promising growth in emerging markets. Regional trade flows and strategic partnerships play a crucial role in ensuring the efficient distribution of calcined anthracite to meet diverse industrial needs worldwide.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Calcined Anthracite Market.- Carbon Graphite International

- Carbide Industries

- Rio Tinto Alcan

- RWE Supply & Trading

- Anshan Iron and Steel Group

- Shougang Group

- Baosteel Group

- POSCO

- Nippon Steel & Sumitomo Metal

- Gerdau S.A.

- ArcelorMittal

- Glencore

- Xcoal Energy & Resources

- Anglo American

- Peabody Energy

- China Shenhua Energy Company

- Coal India Limited

- Siberian Anthracite

- Reading Anthracite Company

- Lehigh Anthracite

Frequently Asked Questions

What is calcined anthracite used for?

Calcined anthracite is primarily used as a recarburizer in steel manufacturing, an additive in aluminum production, and a carbon raiser in foundries. It also serves as a filter media in water treatment and has applications in chemical industries and battery materials due to its high purity and carbon content.

What are the key drivers of the Calcined Anthracite market?

The market is driven by robust growth in global steel and aluminum production, increasing adoption of electric arc furnaces (EAFs), rising demand for water treatment solutions, and extensive infrastructure development and urbanization worldwide.

What are the main challenges facing the Calcined Anthracite market?

Key challenges include volatile prices of raw anthracite, intense competition from alternative carbon materials, high logistics and transportation costs, and the increasing need for sustainable and environmentally compliant production practices.

Which region dominates the Calcined Anthracite market?

Asia Pacific currently dominates the Calcined Anthracite market, primarily due to rapid industrialization and significant steel and aluminum production in countries such as China and India.

How is AI impacting the Calcined Anthracite industry?

AI is impacting the industry through optimization of raw material sourcing, enhanced process control and energy efficiency in calcination, improved quality control, advanced demand forecasting, and predictive maintenance to reduce operational downtime.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted