Buprenorphine Hydrochloride Injection Market

Buprenorphine Hydrochloride Injection Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703564 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

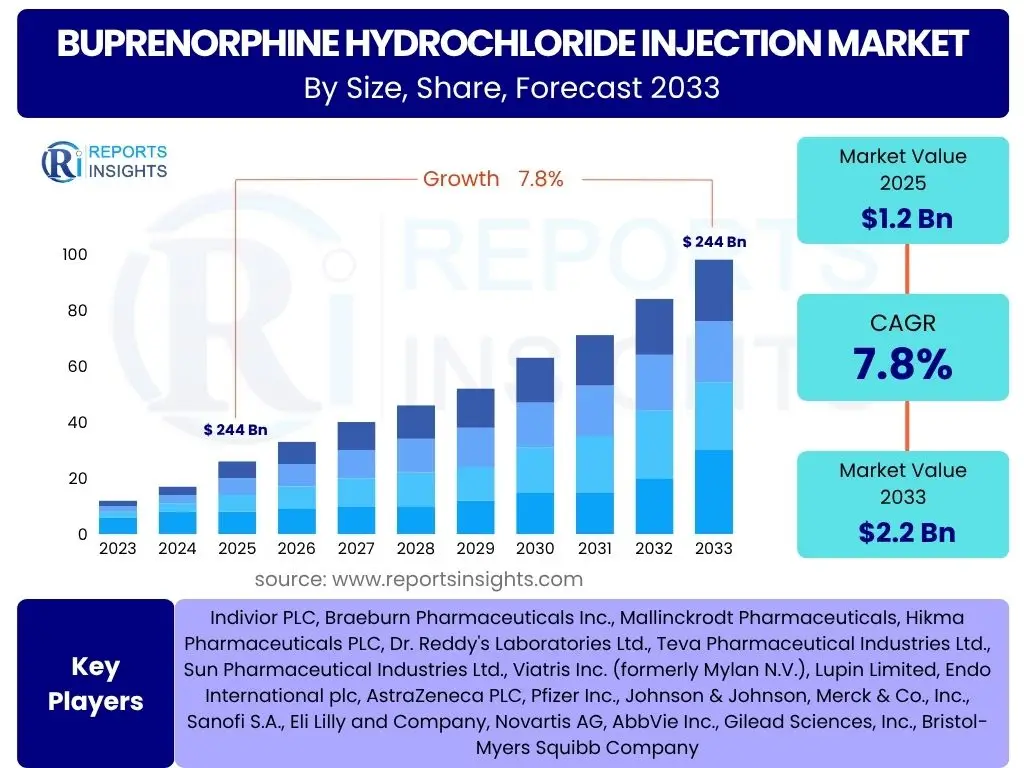

Buprenorphine Hydrochloride Injection Market Size

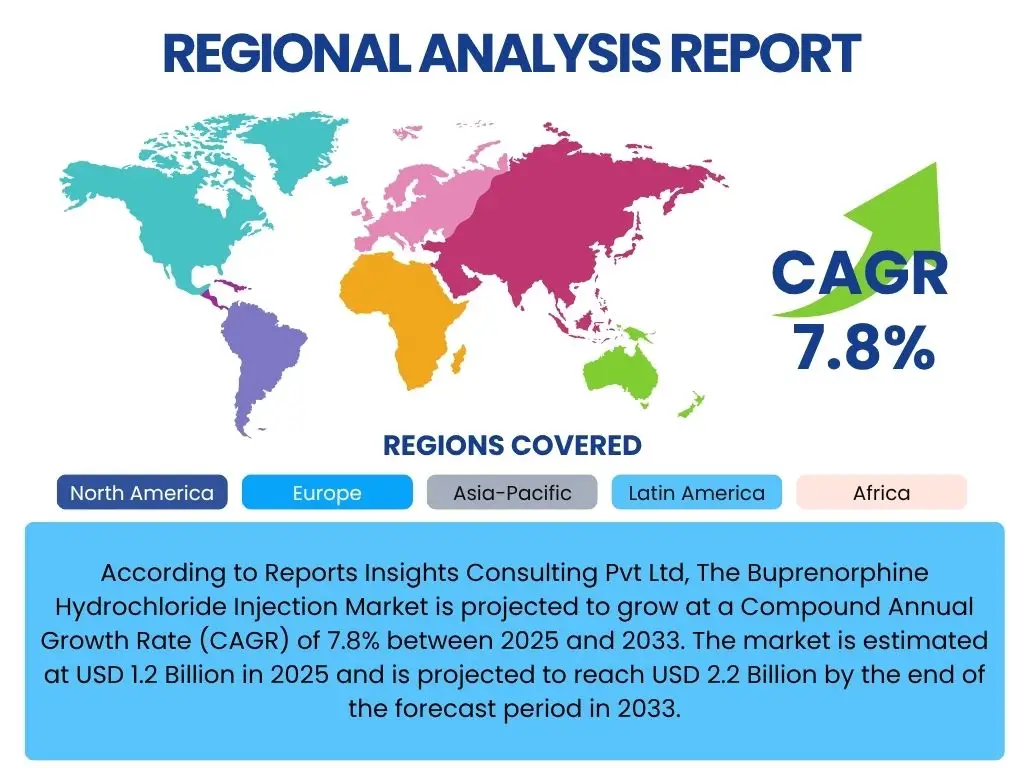

According to Reports Insights Consulting Pvt Ltd, The Buprenorphine Hydrochloride Injection Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033. The market is estimated at USD 1.2 Billion in 2025 and is projected to reach USD 2.2 Billion by the end of the forecast period in 2033.

Key Buprenorphine Hydrochloride Injection Market Trends & Insights

The Buprenorphine Hydrochloride Injection market is experiencing significant shifts driven by evolving healthcare policies, increased awareness regarding opioid use disorder (OUD), and advancements in addiction treatment methodologies. Stakeholders are keen to understand emerging patterns in patient demographics, treatment accessibility, and the adoption of novel drug delivery systems. A primary area of focus is the move towards long-acting injectable formulations, which offer improved patient adherence and reduced diversion risk, addressing common challenges associated with daily medication regimens. Furthermore, there is a growing emphasis on integrated care models that combine pharmacotherapy with behavioral health services, shaping market dynamics and influencing prescribing practices.

Regulatory support and public health initiatives aimed at combating the opioid crisis are profoundly impacting market growth. Governments globally are allocating substantial resources to expand access to medication-assisted treatment (MAT), with buprenorphine being a cornerstone therapy. This includes simplifying prescribing guidelines, increasing the number of certified providers, and enhancing reimbursement policies. Such policy shifts are not only expanding the patient pool but also fostering innovation in product development and market penetration strategies. Understanding these regulatory nuances and their regional variations is crucial for market participants seeking to optimize their strategic positioning.

Technological advancements in drug delivery and manufacturing processes are also notable trends. The pharmaceutical industry is investing in research and development to create more stable, patient-friendly, and cost-effective buprenorphine formulations. This includes exploring biodegradable polymers, implantable devices, and novel syringe designs that enhance ease of administration and patient comfort. Additionally, the integration of digital health solutions for patient monitoring, treatment adherence tracking, and virtual consultations is gaining traction, promising to further optimize treatment outcomes and expand the reach of buprenorphine injection therapies.

- Shift towards long-acting injectable formulations for improved adherence.

- Increasing government support and public health initiatives for MAT.

- Integration of buprenorphine treatment within broader behavioral health services.

- Advancements in drug delivery technologies enhancing patient convenience.

- Expansion of tele-health and digital platforms for OUD management.

AI Impact Analysis on Buprenorphine Hydrochloride Injection

The integration of Artificial intelligence (AI) is set to revolutionize various facets of the Buprenorphine Hydrochloride Injection market, addressing user inquiries regarding enhanced treatment efficacy, optimized patient management, and streamlined drug development. AI algorithms can analyze vast datasets from electronic health records, genomic information, and clinical trials to identify patient cohorts most likely to benefit from buprenorphine therapy, thereby facilitating personalized medicine approaches. This precision can lead to improved patient outcomes by tailoring treatment plans, predicting potential adverse effects, and optimizing dosing strategies. Users are keen to understand how AI can reduce the trial-and-error approach often seen in addiction treatment, leading to faster and more effective interventions.

Furthermore, AI holds significant potential in enhancing drug discovery and development processes for new buprenorphine formulations or complementary therapies. By utilizing machine learning to screen compound libraries, predict molecular interactions, and model drug pharmacokinetics, AI can drastically cut down the time and cost associated with preclinical research. For the Buprenorphine Hydrochloride Injection market, this could mean faster development of next-generation long-acting injectables or combination therapies with improved safety profiles and efficacy. Users anticipate that AI-driven insights will accelerate the availability of innovative solutions to combat the opioid epidemic, addressing the urgent public health need for more effective treatments.

Beyond drug development, AI is poised to optimize the operational aspects of the buprenorphine supply chain and patient access. AI-powered predictive analytics can forecast demand, manage inventory, and identify potential supply chain disruptions, ensuring consistent availability of the injection. In the realm of patient management, AI tools can support healthcare providers by analyzing patient adherence data, identifying individuals at risk of relapse, and flagging those who might benefit from immediate intervention or changes in their treatment plan. This proactive approach, enabled by AI, is expected to enhance treatment retention rates and improve long-term recovery outcomes for patients receiving Buprenorphine Hydrochloride Injection, meeting user expectations for more robust and responsive healthcare systems.

- Enhanced precision in patient selection and personalized dosing through data analytics.

- Accelerated drug discovery and development for novel buprenorphine formulations.

- Optimized supply chain management and demand forecasting for the injection.

- Improved patient monitoring and relapse prediction using AI algorithms.

- Streamlined clinical trials for new buprenorphine-based therapies.

Key Takeaways Buprenorphine Hydrochloride Injection Market Size & Forecast

A central takeaway from the Buprenorphine Hydrochloride Injection market analysis is its robust and consistent growth trajectory, underscoring its pivotal role in addressing the global opioid crisis. Users frequently inquire about the certainty and drivers behind this sustained expansion. The forecast of the market reaching USD 2.2 Billion by 2033 from USD 1.2 Billion in 2025, at a CAGR of 7.8%, indicates a strong confidence in its continued adoption. This growth is primarily fueled by rising incidence of opioid use disorder, increasing government support for medication-assisted treatment (MAT), and the introduction of innovative, patient-centric formulations that enhance adherence and safety. The market’s resilience is also attributed to its essential nature as a life-saving treatment, making it less susceptible to economic fluctuations compared to other pharmaceutical sectors.

Another significant insight revolves around the increasing preference for long-acting injectable forms of buprenorphine. User queries often highlight the importance of formulations that reduce dosing frequency and potential for misuse. The market forecast reflects a shift towards these advanced products, as they offer substantial benefits in terms of patient compliance, reduced stigma, and diminished diversion risks. This evolution in product offerings is a key driver for market expansion, as it broadens the appeal and accessibility of buprenorphine therapy to a wider patient population. Pharmaceutical companies are strategically investing in research and development to capture this growing demand for convenient and effective treatment options.

Finally, the report highlights the critical influence of supportive regulatory environments and growing public health awareness on market expansion. Questions from users frequently touch upon the impact of policy changes and awareness campaigns. Favorable reimbursement policies, reduced barriers to prescribing, and intensified public education campaigns about OUD and MAT are directly contributing to the upward revision of market size projections. These factors not only expand the addressable patient base but also foster a more accepting and informed ecosystem for addiction treatment, ensuring that the Buprenorphine Hydrochloride Injection market continues its upward trajectory over the forecast period. The concerted effort from healthcare providers, policymakers, and advocacy groups is instrumental in solidifying this market's growth.

- Consistent market expansion driven by escalating opioid use disorder rates.

- Strong demand for long-acting injectable buprenorphine formulations.

- Supportive government policies and public health initiatives are key growth catalysts.

- Innovation in drug delivery systems enhances market appeal and patient adherence.

- Market resilience driven by the essential nature of addiction treatment.

Buprenorphine Hydrochloride Market Drivers Analysis

The Buprenorphine Hydrochloride Injection market is propelled by a confluence of critical factors directly addressing the escalating global opioid crisis. A primary driver is the alarming rise in opioid use disorder (OUD) prevalence across various demographics and geographies, necessitating effective and accessible treatment options. Governments and healthcare organizations worldwide are intensifying efforts to combat this crisis through public health campaigns, increased funding for addiction services, and the promotion of medication-assisted treatment (MAT) as the gold standard for OUD. This heightened public and governmental focus creates a robust demand for buprenorphine, a core component of MAT, driving its market expansion.

Furthermore, the evolving regulatory landscape, particularly in major economies like North America and Europe, significantly contributes to market growth. Policies aimed at expanding access to MAT, such as loosening restrictions on buprenorphine prescribing and increasing the number of certified prescribers, are dismantling barriers to treatment. Favorable reimbursement policies from both public and private insurers also make buprenorphine injection therapies more affordable and accessible for patients, thereby stimulating market demand. These regulatory tailwinds provide a strong foundation for pharmaceutical companies to invest further in research, development, and commercialization of buprenorphine-based products, including innovative injectable formulations.

Innovation in drug delivery systems and the development of long-acting buprenorphine injections represent another potent driver. These advanced formulations offer distinct advantages, such as improved patient adherence, reduced potential for diversion, and decreased frequency of administration, which collectively enhance treatment outcomes and patient convenience. The shift from daily oral medications to monthly or even longer-acting injections addresses critical challenges in OUD treatment, making it more appealing for both patients and healthcare providers. This technological progression not only expands the therapeutic options available but also solidifies buprenorphine's position as a preferred treatment modality, further fueling market growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Prevalence of Opioid Use Disorder (OUD) | +2.5% | North America, Europe, Oceania | Short to Mid-term (2025-2030) |

| Growing Adoption of Medication-Assisted Treatment (MAT) | +2.0% | Global, particularly developed economies | Mid to Long-term (2025-2033) |

| Favorable Regulatory Policies and Reimbursement | +1.5% | United States, Canada, Western Europe | Short to Mid-term (2025-2030) |

| Advancements in Long-Acting Injectable Formulations | +1.0% | Global, especially high-income countries | Mid to Long-term (2028-2033) |

| Increased Awareness and Reduced Stigma of OUD | +0.8% | Global, with regional variations | Mid to Long-term (2027-2033) |

Buprenorphine Hydrochloride Market Restraints Analysis

Despite the strong growth drivers, the Buprenorphine Hydrochloride Injection market faces several significant restraints that could impede its full potential. A primary challenge is the societal stigma associated with opioid use disorder (OUD) and the treatments for it, including medication-assisted treatment (MAT). This stigma can deter individuals from seeking necessary treatment, discourage healthcare providers from offering buprenorphine, and even influence policy decisions, thereby limiting patient access and market penetration. Overcoming deep-seated prejudices requires extensive public education and cultural shifts, which are inherently slow and complex processes, thus posing a persistent restraint on market expansion.

Another considerable restraint involves the regulatory hurdles and the relatively stringent requirements for prescribing and administering buprenorphine. While some regulations have been relaxed to expand access, the need for specialized training and certification for prescribers (though less restrictive now) can still limit the number of healthcare professionals who can offer this treatment. Additionally, concerns about the potential for diversion or misuse of buprenorphine, even in its injectable forms, lead to ongoing monitoring and regulatory oversight that can increase administrative burdens for providers and manufacturers. These complexities can slow down market entry for new products and limit the overall scalability of treatment programs.

Furthermore, the high cost associated with buprenorphine hydrochloride injection therapies, particularly the long-acting formulations, can act as a barrier to widespread adoption, especially in regions with less developed healthcare infrastructures or limited insurance coverage. While reimbursement policies are improving, out-of-pocket costs can still be prohibitive for many patients. Competition from other OUD treatment modalities, including different formulations of buprenorphine (e.g., sublingual films) or alternative medications, also presents a restraint by fragmenting the market. Moreover, the availability of generic versions of some buprenorphine products can exert downward pressure on pricing, impacting revenue growth for innovators and potentially limiting investment in future research and development for more advanced injections.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Social Stigma Associated with OUD and MAT | -1.8% | Global, culturally sensitive regions | Long-term (2025-2033) |

| Regulatory Complexities and Prescriber Limitations | -1.5% | United States, select European countries | Mid-term (2025-2030) |

| High Treatment Cost and Reimbursement Challenges | -1.2% | Developing Economies, Payer-driven markets | Short to Mid-term (2025-2030) |

| Competition from Alternative OUD Treatments | -0.8% | Global, established pharmaceutical markets | Mid-term (2025-2030) |

| Limited Infrastructure for Addiction Treatment | -0.7% | Rural Areas, Low-income countries | Long-term (2025-2033) |

Buprenorphine Hydrochloride Market Opportunities Analysis

Significant opportunities for growth exist within the Buprenorphine Hydrochloride Injection market, particularly in expanding treatment accessibility and developing novel formulations. One key opportunity lies in penetrating underserved patient populations, especially in rural areas or communities with limited access to specialized addiction treatment centers. The advent of long-acting injectable buprenorphine, which reduces the need for frequent clinic visits, creates a viable pathway to reach these patients through primary care settings or telehealth models. This expansion of access not only addresses a critical public health need but also opens up vast untapped market segments, promising substantial growth for market players capable of wide distribution and provider training.

The continuous innovation in drug delivery systems presents another compelling opportunity. Research and development focused on creating even longer-acting injectable buprenorphine formulations, potentially quarterly or bi-annually administered, could significantly enhance patient convenience and adherence. Furthermore, exploring combination therapies where buprenorphine is co-formulated with other therapeutic agents to address co-occurring mental health conditions or enhance treatment efficacy represents a lucrative avenue. Companies investing in such cutting-edge formulations stand to gain a competitive edge by offering differentiated products that meet evolving patient and provider needs, attracting new users to buprenorphine injection therapy.

Geographical expansion, particularly into emerging markets and regions where OUD prevalence is rising but treatment options are limited, offers substantial growth prospects. Countries in Asia Pacific and parts of Latin America, despite having significant opioid-related challenges, often lack comprehensive MAT programs. Educating healthcare systems, advocating for policy changes, and establishing robust supply chains in these regions could unlock considerable market potential. Strategic partnerships with local pharmaceutical companies, government bodies, and non-governmental organizations could facilitate market entry and accelerate the adoption of Buprenorphine Hydrochloride Injection, transforming global OUD treatment landscapes and generating new revenue streams for market participants.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Underserved Patient Populations | +2.2% | Rural Areas, Low-income Communities (Global) | Mid to Long-term (2026-2033) |

| Development of Ultra-Long-Acting Formulations | +1.8% | High-income Countries, Research-focused Markets | Long-term (2028-2033) |

| Geographical Expansion into Emerging Markets | +1.5% | Asia Pacific, Latin America, Eastern Europe | Mid to Long-term (2027-2033) |

| Integration with Telehealth and Digital Health Platforms | +1.0% | North America, Western Europe | Short to Mid-term (2025-2030) |

| Strategic Partnerships for Market Penetration | +0.8% | Global, particularly new market entrants | Short to Mid-term (2025-2030) |

Buprenorphine Hydrochloride Market Challenges Impact Analysis

The Buprenorphine Hydrochloride Injection market, while promising, contends with several significant challenges that require strategic navigation. One prominent challenge is the ongoing battle against the illicit diversion and misuse of buprenorphine, despite efforts to develop abuse-deterrent formulations. While injectable forms inherently reduce some risks associated with oral medications, vigilance is still required to prevent unauthorized distribution. This concern often leads to heightened regulatory scrutiny and prescriber hesitancy, limiting the overall reach and accessibility of the treatment. Addressing this challenge requires continuous innovation in drug design, coupled with robust monitoring systems and prescriber education to ensure safe and appropriate use.

Another substantial challenge stems from the complex and often fragmented healthcare infrastructure for addiction treatment. Many regions lack sufficient numbers of trained healthcare professionals, specialized clinics, or integrated care models necessary for widespread adoption of buprenorphine injection therapy. This deficit in infrastructure can impede patient access, particularly in rural or underserved areas, even if the medication itself is available. Bridging this gap requires significant investment in workforce development, expansion of treatment facilities, and fostering interdisciplinary collaboration, which are long-term undertakings with substantial resource implications for market growth.

Furthermore, maintaining patient adherence and retention in long-term OUD treatment remains a significant hurdle. While long-acting injections improve compliance compared to daily dosing, factors such as patient motivation, co-occurring mental health disorders, and socio-economic determinants can still lead to treatment discontinuation. The high cost of some advanced injectable formulations, despite improving reimbursement, can also pose a financial burden on patients and healthcare systems, potentially limiting sustained access. Overcoming these adherence and financial challenges necessitates comprehensive patient support programs, flexible payment options, and continuous efforts to demonstrate the long-term cost-effectiveness and societal benefits of buprenorphine treatment, ensuring sustained market demand.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Risk of Diversion and Misuse | -1.6% | Global, particularly countries with high OUD rates | Short to Mid-term (2025-2030) |

| Limited Treatment Infrastructure and Trained Personnel | -1.3% | Rural Areas, Developing Nations | Long-term (2025-2033) |

| Patient Adherence and Retention Challenges | -1.0% | Global, varies by patient population | Mid-term (2025-2030) |

| Navigating Evolving Regulatory Landscape | -0.9% | United States, European Union | Short to Mid-term (2025-2028) |

| Pricing Pressure from Generic Competition | -0.6% | Established Pharmaceutical Markets | Mid-term (2027-2033) |

Buprenorphine Hydrochloride Injection Market - Updated Report Scope

This comprehensive market report provides an in-depth analysis of the Buprenorphine Hydrochloride Injection market, covering historical trends, current market dynamics, and future projections. The scope encompasses detailed segmentation analysis by various criteria, regional breakdowns, competitive landscape assessment, and a thorough examination of market drivers, restraints, opportunities, and challenges. The report aims to offer strategic insights to stakeholders, enabling informed decision-making and identification of growth avenues within the evolving opioid use disorder treatment landscape, specifically focusing on injectable buprenorphine formulations and their impact on patient outcomes and public health initiatives.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.2 Billion |

| Market Forecast in 2033 | USD 2.2 Billion |

| Growth Rate | 7.8% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Indivior PLC, Braeburn Pharmaceuticals Inc., Mallinckrodt Pharmaceuticals, Hikma Pharmaceuticals PLC, Dr. Reddy's Laboratories Ltd., Teva Pharmaceutical Industries Ltd., Sun Pharmaceutical Industries Ltd., Viatris Inc. (formerly Mylan N.V.), Lupin Limited, Endo International plc, AstraZeneca PLC, Pfizer Inc., Johnson & Johnson, Merck & Co., Inc., Sanofi S.A., Eli Lilly and Company, Novartis AG, AbbVie Inc., Gilead Sciences, Inc., Bristol-Myers Squibb Company |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Buprenorphine Hydrochloride Injection market is meticulously segmented to provide granular insights into its various facets, enabling a clearer understanding of market dynamics and growth opportunities. This segmentation helps stakeholders to identify high-growth areas, target specific patient populations, and tailor product development and marketing strategies. By categorizing the market based on product type, application, distribution channel, and end-user, the report offers a multi-dimensional view of how different segments contribute to the overall market value and how their individual trajectories are shaped by prevailing market forces, regulatory changes, and technological advancements. This granular analysis is crucial for strategic decision-making and competitive positioning.

The segmentation by type primarily distinguishes between subcutaneous and intramuscular injections, reflecting differences in administration methods and patient preferences, as well as the potential for other emerging forms like implantable devices. Each type caters to specific clinical needs and offers varying benefits in terms of patient comfort, duration of action, and ease of administration. Furthermore, the application segment highlights the primary therapeutic uses of buprenorphine hydrochloride injection, predominantly in opioid use disorder (OUD) treatment, but also in pain management and anesthesia, revealing the drug's versatility and diverse market potential beyond addiction therapy. Understanding the demand across these applications is vital for portfolio diversification.

Distribution channels and end-user segments provide critical insights into the market's commercial pathways and the primary consumers of these injections. Hospital pharmacies, retail pharmacies, online pharmacies, and specialty clinics represent the key avenues through which the product reaches patients, each with its own logistical and regulatory considerations. Simultaneously, analyzing end-users such as hospitals, specialty clinics, rehabilitation centers, and homecare settings helps to discern where demand originates and how healthcare delivery models influence product consumption. This comprehensive segmentation framework allows for a nuanced assessment of the market, identifying areas of high growth, competitive intensity, and potential for strategic partnerships, ultimately guiding informed business decisions across the value chain.

- By Type:

- Subcutaneous Injection

- Intramuscular Injection

- Others (e.g., Implantable)

- By Application:

- Opioid Use Disorder (OUD) Treatment

- Pain Management

- Anesthesia

- Post-operative Analgesia

- By Distribution Channel:

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- Specialty Clinics & Centers

- By End-User:

- Hospitals

- Specialty Clinics

- Rehabilitation Centers

- Homecare Settings

Regional Highlights

The Buprenorphine Hydrochloride Injection market exhibits distinct regional dynamics driven by varying prevalences of opioid use disorder (OUD), healthcare infrastructure, regulatory frameworks, and government initiatives. North America, particularly the United States and Canada, stands as the dominant market, primarily due to the severe opioid crisis in these countries, robust government funding for medication-assisted treatment (MAT), and favorable reimbursement policies. The region has seen significant investments in expanding access to buprenorphine treatment, coupled with a high adoption rate of long-acting injectable formulations, making it a key growth engine for the global market. Policy reforms aimed at reducing barriers to treatment and increasing prescriber capacity further solidify North America's leading position.

Europe represents another substantial market, characterized by diverse regulatory approaches and varying OUD prevalence across countries. Western European nations, such as the UK, Germany, and France, are witnessing increasing awareness and adoption of buprenorphine injections, supported by public health programs and established healthcare systems. Eastern Europe, while currently smaller, presents emerging opportunities as countries in the region begin to address their own opioid challenges and invest in MAT infrastructure. The European market's growth is often driven by national healthcare systems and their evolving guidelines for addiction treatment, alongside the efforts of pharmaceutical companies to secure market approvals and expand distribution networks across the continent.

The Asia Pacific (APAC) region is projected to emerge as a high-growth market, albeit from a smaller base, driven by rising OUD rates in countries like Australia, China, and India, coupled with improving healthcare access and increasing healthcare expenditure. While MAT adoption is still nascent in many parts of APAC compared to Western counterparts, growing awareness, government initiatives, and the expansion of pharmaceutical distribution networks are creating fertile ground for market expansion. Latin America and the Middle East and Africa (MEA) also present nascent opportunities, with regional growth spurred by efforts to address substance use disorders and improve public health outcomes. These regions are characterized by a growing recognition of the need for effective OUD treatments and a gradual increase in healthcare investment, albeit with challenges related to infrastructure and affordability.

- North America: Dominant market due to severe opioid crisis, robust government funding for MAT, and favorable reimbursement policies. High adoption of long-acting injectables.

- Europe: Significant market driven by varying OUD prevalence, diverse regulatory approaches, and established healthcare systems, with growing adoption in Western Europe and emerging opportunities in Eastern Europe.

- Asia Pacific (APAC): High-growth potential owing to rising OUD rates, improving healthcare infrastructure, and increasing healthcare expenditure, with nascent but expanding MAT programs.

- Latin America: Emerging market with increasing recognition of opioid challenges and a gradual increase in healthcare investment, requiring significant infrastructure development.

- Middle East and Africa (MEA): Nascent market with growing awareness and improving healthcare access, but facing challenges related to infrastructure and affordability.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Buprenorphine Hydrochloride Injection Market.- Indivior PLC

- Braeburn Pharmaceuticals Inc.

- Mallinckrodt Pharmaceuticals

- Hikma Pharmaceuticals PLC

- Dr. Reddy's Laboratories Ltd.

- Teva Pharmaceutical Industries Ltd.

- Sun Pharmaceutical Industries Ltd.

- Viatris Inc. (formerly Mylan N.V.)

- Lupin Limited

- Endo International plc

- AstraZeneca PLC

- Pfizer Inc.

- Johnson & Johnson

- Merck & Co., Inc.

- Sanofi S.A.

- Eli Lilly and Company

- Novartis AG

- AbbVie Inc.

- Gilead Sciences, Inc.

- Bristol-Myers Squibb Company

Frequently Asked Questions

What is Buprenorphine Hydrochloride Injection used for?

Buprenorphine Hydrochloride Injection is primarily used for the treatment of opioid use disorder (OUD) as part of a comprehensive treatment plan that includes counseling and psychosocial support. It is also utilized for the management of moderate to severe pain and sometimes in anesthesia or post-operative analgesia.

How large is the Buprenorphine Hydrochloride Injection market?

The Buprenorphine Hydrochloride Injection market is estimated at USD 1.2 Billion in 2025 and is projected to reach USD 2.2 Billion by the end of 2033, growing at a Compound Annual Growth Rate (CAGR) of 7.8% during the forecast period.

What are the main drivers of the Buprenorphine Hydrochloride Injection market?

Key drivers include the increasing global prevalence of opioid use disorder (OUD), growing adoption of medication-assisted treatment (MAT), favorable regulatory policies and reimbursement, and advancements in long-acting injectable formulations that improve patient adherence and convenience.

Are there new developments in Buprenorphine Hydrochloride Injection formulations?

Yes, significant developments include the increasing availability and preference for long-acting injectable formulations, which offer extended release over weeks or months, reducing dosing frequency and improving patient adherence. Research is also ongoing for ultra-long-acting and potentially implantable forms.

What is the forecast for the Buprenorphine Hydrochloride Injection market?

The Buprenorphine Hydrochloride Injection market is forecasted to experience robust growth, driven by continued efforts to combat the opioid crisis, expanding access to MAT, and ongoing innovations in drug delivery. It is projected to grow at a CAGR of 7.8% from 2025 to 2033.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted