Brown Sugar Market

Brown Sugar Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708656 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

Brown Sugar Market Size

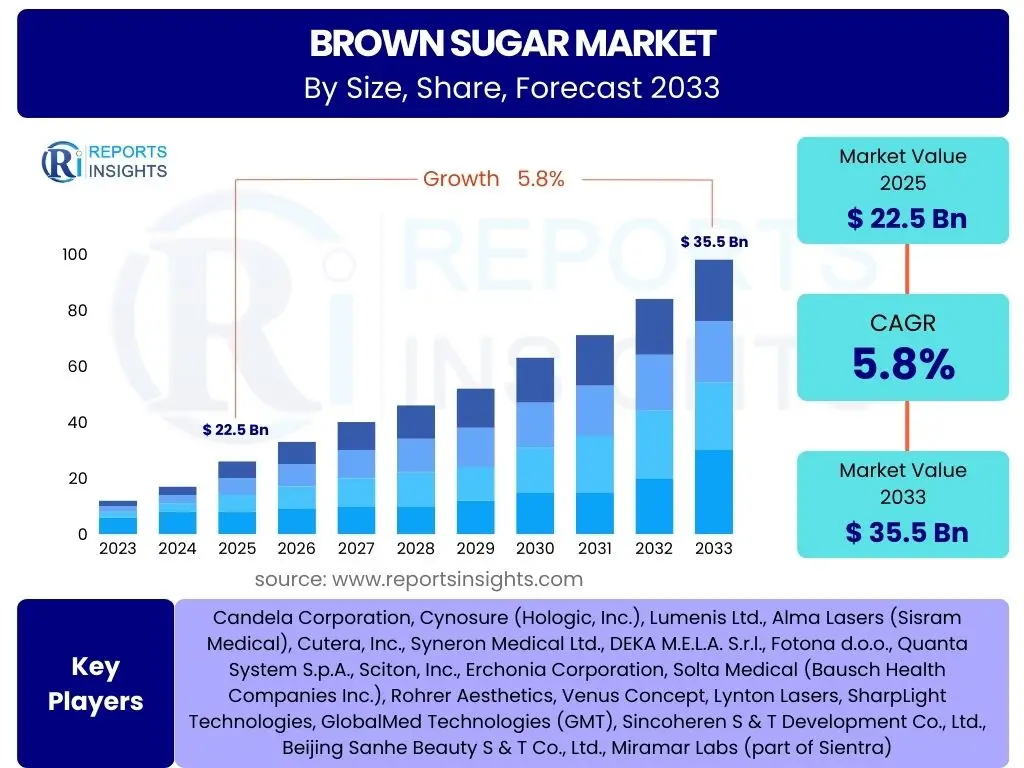

According to Reports Insights Consulting Pvt Ltd, The Brown Sugar Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 22.5 Billion in 2025 and is projected to reach USD 35.5 Billion by the end of the forecast period in 2033.

Key Brown Sugar Market Trends & Insights

User queries regarding brown sugar market trends frequently revolve around evolving consumer preferences, the impact of health and wellness movements, and diversification of product applications. Consumers are increasingly seeking natural and less processed alternatives to refined white sugar, driving demand for various forms of brown sugar. The trend towards premiumization and specialty ingredients in culinary and beverage sectors also significantly influences market dynamics, with artisanal and ethically sourced brown sugar varieties gaining traction.

Furthermore, the market is witnessing an expansion in the industrial application of brown sugar beyond traditional bakery and confectionery. The growing interest in home baking and gourmet cooking, spurred by lifestyle changes and digital culinary content, contributes to the increased retail consumption. Innovations in product packaging and formulation to enhance shelf life and convenience are also emerging as significant trends, catering to modern consumer demands for ease of use and reduced waste.

- Growing consumer preference for natural and less processed sweeteners.

- Increased demand from the gourmet food and beverage industry for premium brown sugar variants.

- Expansion of brown sugar applications in savory dishes and health-conscious products.

- Rising popularity of home baking and cooking activities globally.

- Emphasis on sustainable and ethically sourced brown sugar products.

AI Impact Analysis on Brown Sugar

Common user questions regarding AI's impact on the brown sugar industry often focus on supply chain optimization, predictive analytics for demand and pricing, and enhancing agricultural practices. AI and machine learning algorithms are being increasingly adopted to streamline complex global supply chains, from sugarcane cultivation to processing and distribution of brown sugar. This includes optimizing logistics routes, managing inventory levels more efficiently, and reducing waste throughout the value chain, leading to significant cost savings and improved operational efficiency.

Moreover, AI plays a crucial role in demand forecasting and price prediction, enabling producers and distributors to make more informed decisions. By analyzing vast datasets including historical sales, weather patterns, economic indicators, and consumer sentiment, AI models can provide highly accurate forecasts, mitigating risks associated with market volatility. This predictive capability extends to identifying optimal planting and harvesting times for sugarcane, thus enhancing yield and quality, which directly impacts brown sugar production. Furthermore, AI-powered quality control systems are emerging, using computer vision to inspect brown sugar for impurities or inconsistencies, ensuring high product standards before reaching consumers.

- AI-driven optimization of brown sugar supply chain logistics and inventory management.

- Enhanced demand forecasting and price prediction using machine learning algorithms.

- Precision agriculture techniques for sugarcane cultivation, improving yield and quality.

- Automated quality control and inspection systems for brown sugar processing.

- Data-driven insights for sustainable sourcing and production practices.

Key Takeaways Brown Sugar Market Size & Forecast

Analysis of common user questions regarding the brown sugar market size and forecast consistently highlights interest in the market's growth trajectory, primary drivers, and long-term sustainability. The market is positioned for steady expansion, fueled by a confluence of evolving consumer tastes and strategic industrial applications. Its moderate yet consistent growth rate underscores its stable position within the broader sweetener landscape, indicating resilience against alternative products and health-related concerns, albeit with necessary adaptations.

A significant takeaway is the pivotal role of product diversification and market penetration strategies in sustaining this growth. As consumers seek out more 'natural' and distinct flavor profiles, brown sugar, in its various forms, offers a compelling alternative to highly refined sugars. The forecast points towards continued innovation in application, especially within the gourmet food, artisanal beverage, and health-conscious product segments, which will be crucial for achieving the projected market values and solidifying its market presence.

- Consistent growth projected through 2033, driven by diverse applications and consumer preferences.

- Rising demand for natural sweeteners is a primary catalyst for market expansion.

- Significant opportunities in premium and specialty food and beverage sectors.

- Market resilience despite evolving health trends, through product differentiation.

- Innovation in product forms and packaging will be critical for sustained market value.

Brown Sugar Market Drivers Analysis

The brown sugar market is fundamentally driven by a shift in global consumer preferences towards natural and less processed food ingredients. As awareness surrounding the processing methods of food increases, brown sugar, perceived as a more natural alternative to white refined sugar due to its molasses content, gains favor. This consumer sentiment is particularly strong in developed economies where health and wellness trends heavily influence purchasing decisions, leading to a steady uptake in household and industrial consumption.

Another significant driver is the expansive growth and innovation within the food and beverage industry. Brown sugar offers distinct flavor profiles and textural properties that are highly valued in bakery, confectionery, and gourmet beverage applications. Its caramel notes and moistening effects are indispensable in a wide array of products, from artisanal breads and specialty coffees to intricate desserts, thereby securing its position as a preferred ingredient for product development and enhancement across various food categories.

Furthermore, rising disposable incomes in emerging economies, coupled with urbanization and Westernization of diets, are stimulating demand for processed foods and sweet treats. This demographic shift provides a fertile ground for market expansion, as a larger consumer base gains access to and develops a taste for products incorporating brown sugar. The increasing global culinary exploration also contributes, with brown sugar being a staple in many traditional and contemporary international cuisines, solidifying its ingredient appeal.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing consumer preference for natural sweeteners | +1.5% | North America, Europe, Asia Pacific | 2025-2033 (Long-term) |

| Expansion of the food and beverage industry | +1.2% | Global, particularly APAC and Latin America | 2025-2033 (Long-term) |

| Increased demand from bakery and confectionery sectors | +1.0% | Global | 2025-2030 (Mid-term) |

| Rising disposable incomes in developing regions | +0.8% | Asia Pacific, Latin America, Africa | 2028-2033 (Long-term) |

| Diversification of product applications | +0.7% | Europe, North America | 2025-2033 (Mid to Long-term) |

Brown Sugar Market Restraints Analysis

Despite its growth, the brown sugar market faces significant restraints, primarily stemming from global health concerns related to sugar consumption. Public health campaigns and dietary guidelines advocating for reduced sugar intake directly impact consumer purchasing habits across all sugar categories, including brown sugar. While often perceived as healthier than white sugar, brown sugar still contributes to overall caloric intake and can lead to health issues if consumed excessively, thus prompting consumers to seek lower-sugar or sugar-free alternatives.

Another critical restraint is the intense competition from alternative sweeteners, both natural and artificial. The market is saturated with a variety of substitutes such as stevia, erythritol, aspartame, and sucralose, which often boast zero-calorie or low-calorie profiles, appealing to a health-conscious demographic. Additionally, other natural sweeteners like honey, maple syrup, and agave nectar also compete for market share, offering distinct flavors and perceived health benefits that can divert consumers away from brown sugar.

Furthermore, the volatility in raw material prices, particularly sugarcane, significantly impacts the production costs of brown sugar. Fluctuations in weather patterns, agricultural policies, and global commodity markets can lead to unpredictable pricing for sugarcane, subsequently affecting the profitability and stability of brown sugar producers. Such price instability can challenge market growth, making it difficult for manufacturers to maintain consistent pricing and profit margins, especially in a competitive environment where consumers are price-sensitive.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Health concerns related to excessive sugar consumption | -1.3% | Global, particularly North America, Europe | 2025-2033 (Long-term) |

| Availability of alternative natural and artificial sweeteners | -1.0% | Global | 2025-2033 (Long-term) |

| Volatility in raw material (sugarcane) prices | -0.8% | Global, especially sugar-producing regions | 2025-2030 (Mid-term) |

| Strict government regulations on sugar content | -0.6% | Europe, North America, parts of Asia | 2026-2033 (Mid to Long-term) |

| Perceived higher cost compared to white refined sugar | -0.5% | Developing markets, price-sensitive segments | 2025-2030 (Mid-term) |

Brown Sugar Market Opportunities Analysis

The brown sugar market presents substantial opportunities for growth, particularly through product innovation and the development of specialized variants. There is a burgeoning demand for organic, unrefined, and ethically sourced brown sugar, appealing to environmentally conscious consumers and those seeking premium ingredients. Manufacturers can capitalize on this by introducing new product lines that emphasize these attributes, such as fair-trade brown sugar or brown sugar with unique regional origins, thereby commanding higher price points and attracting niche markets.

Expansion into emerging markets also represents a significant growth avenue. As economies in Asia Pacific, Latin America, and Africa continue to develop, rising disposable incomes and changing dietary patterns are creating a larger consumer base for diverse food products, including brown sugar. Strategic investments in distribution networks, localized marketing campaigns, and partnerships with local food manufacturers can help tap into these rapidly expanding markets, fostering substantial market penetration and revenue growth.

Furthermore, the growing popularity of e-commerce and direct-to-consumer sales channels offers an effective way to reach a broader audience and facilitate market expansion. Online platforms reduce geographical barriers and enable smaller, specialized brown sugar producers to compete with larger players by showcasing unique products and narratives. Leveraging digital marketing and social media can also enhance brand visibility and consumer engagement, transforming the purchase journey and opening up new sales pathways for brown sugar products globally.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Product innovation and specialty variants (e.g., organic, fair-trade) | +1.8% | Global, particularly North America, Europe | 2025-2033 (Long-term) |

| Expansion into emerging markets (APAC, Latin America, Africa) | +1.5% | Asia Pacific, Latin America, Africa | 2026-2033 (Long-term) |

| Growth in e-commerce and direct-to-consumer sales channels | +1.1% | Global | 2025-2030 (Mid-term) |

| Increased use in cosmetics and personal care products | +0.9% | North America, Europe, Asia Pacific | 2027-2033 (Long-term) |

| Sustainable sourcing and production initiatives | +0.7% | Europe, North America | 2025-2033 (Mid to Long-term) |

Brown Sugar Market Challenges Impact Analysis

The brown sugar market faces several significant challenges, one of which is the increasing regulatory scrutiny and taxation on sugar products globally. Governments, driven by public health concerns, are implementing sugar taxes and stricter labeling requirements to curb sugar consumption. These measures can increase the cost of brown sugar for both producers and consumers, potentially leading to reduced demand and forcing manufacturers to reformulate products or absorb higher operational expenses, impacting market profitability and growth.

Another persistent challenge is the complex and often volatile global supply chain for sugarcane. Brown sugar production relies heavily on the cultivation of sugarcane, which is susceptible to unpredictable weather patterns, including droughts, floods, and storms, exacerbated by climate change. These environmental factors can lead to crop failures, reduced yields, and disruptions in raw material supply, causing price spikes and supply shortages that directly impact brown sugar production and market stability.

Furthermore, intense competition not only from other sweeteners but also within the brown sugar segment itself, poses a challenge for maintaining market share and differentiation. With numerous brands offering similar brown sugar products, it becomes difficult for companies to stand out and justify premium pricing. This competitive landscape necessitates continuous investment in brand building, product innovation, and efficient cost management to remain viable, putting pressure on profit margins and requiring strategic adaptation.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing regulatory pressures and sugar taxes | -1.2% | Global, particularly Europe, North America | 2025-2033 (Long-term) |

| Climate change impact on sugarcane production | -1.0% | Global sugar-producing regions | 2025-2033 (Long-term) |

| Supply chain disruptions and logistics complexities | -0.9% | Global | 2025-2030 (Mid-term) |

| Intense competition and price wars among manufacturers | -0.7% | Global | 2025-2033 (Mid to Long-term) |

| Consumer perception management regarding "natural" claims | -0.6% | North America, Europe | 2026-2033 (Long-term) |

Brown Sugar Market - Updated Report Scope

This comprehensive market insights report meticulously analyzes the brown sugar market, providing an in-depth understanding of its current landscape and future trajectory. The scope encompasses detailed segmentation across various types, forms, applications, and distribution channels, offering a granular view of market dynamics. It also includes an extensive regional analysis, highlighting key market trends and opportunities in major geographical areas.

The report is designed to equip stakeholders with actionable intelligence by evaluating key market drivers, restraints, opportunities, and challenges. It further profiles leading industry players, assessing their strategies, market presence, and competitive positioning. This holistic approach ensures a robust and forward-looking perspective on the brown sugar industry, catering to strategic business planning and investment decisions.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 22.5 Billion |

| Market Forecast in 2033 | USD 35.5 Billion |

| Growth Rate | 5.8% CAGR |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Associated British Foods plc, Sudzucker AG, Nordzucker AG, American Crystal Sugar Company, Cargill, Incorporated, Bunge Limited, Cosun Beet Company (Royal Cosun), Florida Crystals Corporation, Louis Dreyfus Company, Tate & Lyle plc, Mitsui & Co., Ltd., Tereos S.C.A., Raizen S.A., Wilmar International Limited, Al Ghurair Foods, EID Parry (India) Limited, RCL Foods Limited, Südzucker Group, Westway Feed Products, Imperial Sugar Company |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The brown sugar market is intricately segmented to provide a comprehensive understanding of its various facets, catering to diverse consumer and industrial demands. This segmentation allows for a detailed examination of market dynamics across different product types, physical forms, end-use applications, and distribution channels, thereby revealing specific growth drivers and opportunities within each sub-segment.

By dissecting the market into these distinct categories, stakeholders can identify key areas for investment, product development, and targeted marketing strategies. For instance, understanding the demand for liquid brown sugar versus granulated forms, or its specific use in confectionery versus pharmaceuticals, enables businesses to tailor their offerings more effectively and respond to nuanced market requirements across the global landscape.

- By Type: Light Brown Sugar, Dark Brown Sugar, Muscovado Sugar, Turbinado Sugar, Demerara Sugar, Others

- By Form: Granulated, Powdered, Liquid/Syrup, Cubes

- By Application: Food and Beverages (Bakery & Confectionery, Dairy & Frozen Desserts, Beverages, Sauces & Seasonings, Processed Foods), Cosmetics & Personal Care, Pharmaceuticals, Retail/Household, Animal Feed, Others

- By Distribution Channel: Supermarkets/Hypermarkets, Convenience Stores, Online Retail, Specialty Stores, Direct Sales

Regional Highlights

Geographical analysis reveals significant disparities and opportunities across global brown sugar markets. North America and Europe, characterized by high disposable incomes and a strong focus on health and gourmet food trends, drive demand for specialty and organic brown sugar products. The established food and beverage industries in these regions are key consumers, particularly in premium bakery and beverage sectors.

Asia Pacific (APAC) stands out as a high-growth region, propelled by its large population base, rapid urbanization, and rising middle-class incomes. Countries like India and China are experiencing increasing consumption of processed foods and traditional sweets that often incorporate brown sugar. This region also boasts significant sugarcane production, making it a crucial hub for both supply and demand.

Latin America is another vital region, being a major producer and consumer of sugar, including brown sugar. The strong presence of the food processing industry and traditional culinary uses contribute significantly to its market share. The Middle East and Africa (MEA) exhibit emerging market potential, with growing food processing sectors and a gradual shift in consumer preferences towards diverse food ingredients. These regions represent future growth frontiers, contingent on economic development and increasing market penetration.

- North America: Significant market for specialty and organic brown sugar, driven by health trends and strong food processing industry.

- Europe: High demand for premium brown sugar in bakery, confectionery, and gourmet food applications, with a focus on sustainable sourcing.

- Asia Pacific (APAC): Fastest-growing market due to large population, rising disposable incomes, and increasing consumption in traditional and processed foods.

- Latin America: Key production and consumption region, with a strong presence in local culinary traditions and a growing industrial food sector.

- Middle East and Africa (MEA): Emerging market with increasing urbanization and industrialization, leading to diversified food product demand.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Brown Sugar Market.- Associated British Foods plc

- Sudzucker AG

- Nordzucker AG

- American Crystal Sugar Company

- Cargill, Incorporated

- Bunge Limited

- Cosun Beet Company (Royal Cosun)

- Florida Crystals Corporation

- Louis Dreyfus Company

- Tate & Lyle plc

- Mitsui & Co., Ltd.

- Tereos S.C.A.

- Raizen S.A.

- Wilmar International Limited

- Al Ghurair Foods

- EID Parry (India) Limited

- RCL Foods Limited

- Südzucker Group

- Westway Feed Products

- Imperial Sugar Company

Frequently Asked Questions

Analyze common user questions about the Brown Sugar market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is brown sugar and how does it differ from white sugar?

Brown sugar is sucrose sugar with the addition of molasses, which gives it its characteristic brown color, distinct flavor, and moist texture. White sugar is pure sucrose with all molasses removed during processing, resulting in a drier, crystalline product. The molasses in brown sugar provides minerals not found in white sugar, though in small quantities.

Is brown sugar considered a healthier alternative to white sugar?

While brown sugar contains trace minerals from molasses that white sugar lacks, the nutritional difference between the two is minimal for general dietary purposes. Both are sources of calories and simple carbohydrates. The perception of brown sugar being "healthier" is largely due to its less processed nature, but moderation is advised for both.

What are the primary applications of brown sugar in the market?

Brown sugar is widely used across various applications, predominantly in the food and beverage industry. Key segments include bakery and confectionery for its distinct flavor and moistening properties, as well as in beverages, sauces, and processed foods. It also finds niche uses in cosmetics and personal care products for exfoliation and skin conditioning.

Which regions are leading the brown sugar market in terms of consumption and production?

Asia Pacific is a leading region for both production and consumption, driven by large populations and extensive sugarcane cultivation. North America and Europe are significant consumers, particularly for premium and specialty brown sugar variants, largely due to their developed food industries and evolving consumer preferences.

What is the future outlook for the brown sugar market?

The brown sugar market is projected for steady growth, driven by increasing consumer demand for natural sweeteners and expanding applications in the food and beverage sector. While facing challenges from health concerns and alternative sweeteners, opportunities in product innovation, e-commerce, and emerging markets are expected to sustain its positive trajectory.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted