BPA Free Can Market

BPA Free Can Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702577 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

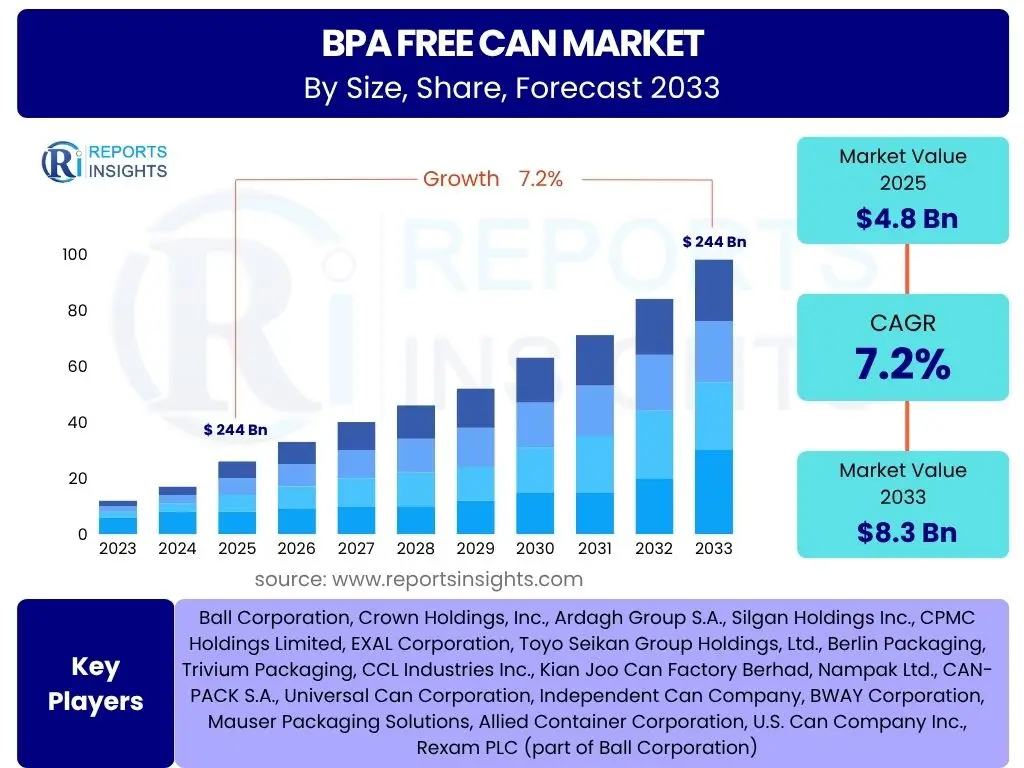

BPA Free Can Market Size

According to Reports Insights Consulting Pvt Ltd, The BPA Free Can Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.2% between 2025 and 2033. The market is estimated at USD 4.8 billion in 2025 and is projected to reach USD 8.3 billion by the end of the forecast period in 2033. This robust growth trajectory is primarily driven by increasing consumer awareness regarding health implications associated with Bisphenol A (BPA) and stringent regulatory frameworks globally.

The consistent expansion of the food and beverage industry, coupled with innovations in packaging materials and coating technologies, further underpins this market's upward trend. Manufacturers are investing significantly in research and development to offer safer and more sustainable packaging solutions, aligning with evolving consumer preferences and environmental concerns. The market's size reflects a collective shift towards healthier living and corporate responsibility in product packaging.

Key BPA Free Can Market Trends & Insights

Users frequently inquire about the emerging trends and significant insights shaping the BPA Free Can market, seeking to understand the dynamics influencing its growth and direction. Analysis reveals a strong emphasis on consumer health consciousness, pushing demand for safer food contact materials. Furthermore, sustainability initiatives and advanced material science are pivotal, driving innovation in can linings and production processes to meet both safety and environmental criteria.

The market is observing a significant pivot towards plant-based and other non-BPA chemical coatings, moving beyond traditional epoxy resins. This shift is accompanied by increased adoption of lightweight materials and improved recycling infrastructures to enhance the overall eco-friendliness of can packaging. Regional regulatory divergences and varying consumer adoption rates also present a complex landscape, requiring adaptable market strategies.

- Growing consumer awareness regarding health risks associated with BPA.

- Stringent regulatory pressure for the adoption of BPA-free packaging solutions.

- Technological advancements in alternative coatings and materials, including plant-based and acrylic options.

- Increasing demand for sustainable and recyclable packaging solutions.

- Expansion of BPA-free cans into new product categories beyond traditional food and beverages, such as personal care and pharmaceuticals.

- Focus on lightweight can designs to reduce transportation costs and environmental impact.

- Development of smart packaging features, including enhanced traceability and temperature indicators.

AI Impact Analysis on BPA Free Can

Common user questions regarding AI's impact on the BPA Free Can sector center on how artificial intelligence can optimize production, enhance quality control, and influence market analytics. AI is increasingly being leveraged to streamline manufacturing processes, from predictive maintenance of machinery to optimizing material usage and reducing waste in can production. This leads to higher operational efficiency and cost savings.

Furthermore, AI-powered analytics are transforming market research and consumer behavior prediction for BPA-free products. By processing vast datasets, AI can identify emerging consumer preferences for specific can types or coatings, allowing manufacturers to adapt their product offerings more rapidly. It also aids in supply chain optimization, predicting demand fluctuations and ensuring a stable supply of alternative raw materials, thereby bolstering the market's resilience and responsiveness to evolving demands.

- AI-driven predictive maintenance enhancing the efficiency and longevity of BPA-free can manufacturing equipment.

- Optimization of raw material sourcing and inventory management through AI-powered supply chain analytics.

- Enhanced quality control and defect detection in BPA-free can production lines using computer vision and machine learning.

- Improved demand forecasting and market trend analysis for BPA-free products through advanced AI algorithms.

- Development of new BPA-free coating formulations and materials using AI for accelerated R&D.

- Personalized marketing and consumer engagement strategies informed by AI-driven insights into health-conscious consumers.

Key Takeaways BPA Free Can Market Size & Forecast

Users are keen to extract concise, actionable insights from the BPA Free Can market's size and forecast, focusing on the most critical aspects for decision-making. The primary takeaway is the market's unequivocal growth, driven by an irreversible shift in consumer preference towards healthier and safer packaging options. This shift is further solidified by proactive global regulatory bodies enforcing stricter standards for food contact materials, creating a fertile ground for sustained expansion.

Another significant insight highlights the pivotal role of innovation in alternative coating technologies and sustainable production methods. Companies that prioritize investment in advanced, environmentally friendly materials and efficient manufacturing processes are poised to capture significant market share. The forecast also underscores the increasing integration of BPA-free solutions across a broader spectrum of industries, extending beyond traditional food and beverage applications, signifying diversification and new revenue streams.

- Robust and consistent market growth is projected, indicating a strong long-term investment outlook.

- Consumer health concerns and stringent regulations are the primary growth catalysts.

- Technological advancements in alternative coatings are critical for market differentiation and expansion.

- Sustainability and recyclability are increasingly vital factors influencing purchasing decisions and market competitiveness.

- Diversification of BPA-free can applications into new sectors like personal care and pharmaceuticals offers significant growth avenues.

- The market is transitioning towards more eco-friendly and economically viable production processes.

BPA Free Can Market Drivers Analysis

The BPA Free Can market is propelled by a confluence of factors, primarily centered on evolving consumer preferences and stringent regulatory landscapes. Heightened consumer awareness regarding the potential health risks associated with Bisphenol A (BPA) has fostered a significant demand for safer packaging alternatives. This awareness, coupled with a general societal shift towards healthier lifestyles, prompts manufacturers to adopt BPA-free solutions to maintain brand reputation and meet market expectations.

Furthermore, global regulatory bodies are increasingly implementing and enforcing stricter norms concerning food contact materials, effectively mandating the reduction or elimination of BPA in packaging. This legislative push creates a non-negotiable requirement for manufacturers, thereby accelerating the adoption of BPA-free cans across various industries. Innovations in materials science and coating technologies also play a crucial role, providing viable and effective alternatives to traditional BPA-containing linings, making the transition more feasible for producers.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Consumer Health Awareness | +2.1% | Global, particularly North America, Europe | Short to Long-term (2025-2033) |

| Stringent Food Safety Regulations | +1.8% | Europe, North America, parts of Asia Pacific | Medium to Long-term (2026-2033) |

| Growing Demand for Packaged Food & Beverages | +1.5% | Asia Pacific, Latin America, Middle East & Africa | Short to Medium-term (2025-2030) |

| Technological Advancements in Coatings | +1.2% | Global | Medium to Long-term (2027-2033) |

| Sustainability and Recycling Initiatives | +0.6% | Europe, North America | Long-term (2029-2033) |

BPA Free Can Market Restraints Analysis

Despite significant growth drivers, the BPA Free Can market faces several notable restraints that could temper its expansion. One primary challenge is the higher production cost associated with BPA-free coatings and materials compared to conventional BPA-based alternatives. This increased cost can translate to higher end-product prices, potentially impacting competitiveness, especially in price-sensitive markets or for producers with tight margins.

Another restraint involves the complexities of scaling up production of new, alternative coating technologies. Ensuring consistent quality, supply chain stability, and adherence to various food contact material regulations across different regions presents a significant hurdle for manufacturers. Furthermore, the market faces competition from other packaging materials like glass, plastic, and Tetra Pak, which may offer different cost or convenience advantages, requiring continuous innovation and clear differentiation for BPA-free cans to maintain their market position.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Higher Production Cost of BPA-Free Materials | -1.3% | Global | Short to Medium-term (2025-2028) |

| Availability and Volatility of Raw Material Prices | -0.8% | Global, especially emerging markets | Short to Medium-term (2025-2029) |

| Competition from Alternative Packaging Materials | -0.7% | Global | Medium to Long-term (2026-2033) |

| Lack of Standardization in Global Regulations | -0.5% | Cross-regional | Medium-term (2027-2031) |

BPA Free Can Market Opportunities Analysis

The BPA Free Can market is rich with opportunities, driven by evolving consumer demands and technological advancements. One significant area for growth lies in the expansion into emerging economies. As disposable incomes rise in regions like Asia Pacific and Latin America, coupled with increasing urbanization, the demand for packaged food and beverages is set to surge, creating a vast untapped market for BPA-free solutions that align with health trends observed in developed nations.

Moreover, continuous innovation in coating technologies presents a lucrative opportunity. The development of new, high-performance, and cost-effective BPA-free linings, including sustainable and bio-based options, can not only address existing production challenges but also open doors for new applications and product categories. The market also benefits from strategic collaborations between packaging manufacturers, food and beverage companies, and research institutions to co-develop custom solutions and accelerate market adoption, fostering a more robust ecosystem for BPA-free packaging.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Emerging Markets | +1.9% | Asia Pacific, Latin America, Middle East & Africa | Medium to Long-term (2026-2033) |

| Technological Innovation in Coating Solutions | +1.5% | Global | Short to Long-term (2025-2033) |

| Diversification into New Product Categories (e.g., Baby Food) | +1.0% | Global, particularly developed markets | Medium-term (2027-2031) |

| Strategic Partnerships and Collaborations | +0.7% | Global | Short to Medium-term (2025-2030) |

BPA Free Can Market Challenges Impact Analysis

The BPA Free Can market is not without its challenges, which can impact adoption rates and market stability. One significant challenge pertains to raw material price volatility and supply chain disruptions. The specialized nature of BPA-free coatings means their constituent raw materials can be subject to price fluctuations and availability issues, impacting manufacturing costs and production schedules. Ensuring a stable and cost-effective supply chain for these unique materials is crucial for sustained market growth.

Another key challenge involves the complexity of consumer perception and education. While awareness of BPA's potential health risks is growing, widespread understanding of BPA-free alternatives and their specific benefits still varies. Misinformation or lack of clear communication can hinder consumer trust and adoption. Furthermore, the global regulatory landscape for BPA-free materials is fragmented, with different standards and timelines across regions, posing compliance challenges for international manufacturers seeking to standardize their products and processes.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Raw Material Price Volatility & Supply Chain Issues | -1.1% | Global | Short to Medium-term (2025-2029) |

| Consumer Misinformation and Education Gap | -0.9% | Global | Medium-term (2026-2031) |

| Regulatory Complexities and Compliance Costs | -0.6% | Cross-regional | Medium to Long-term (2027-2033) |

| Ensuring Performance and Durability of New Coatings | -0.4% | Global | Short-term (2025-2027) |

BPA Free Can Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the BPA Free Can market, covering historical data from 2019 to 2023, a base year of 2024, and forecasts extending through 2033. The scope encompasses detailed segmentation analysis by material, application, end-use industry, and capacity, offering granular insights into market dynamics across various categories. It also includes an extensive regional analysis spanning North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa, highlighting key growth drivers, restraints, opportunities, and challenges unique to each geography. The report also profiles leading market participants, offering a competitive landscape view and strategic recommendations for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 4.8 billion |

| Market Forecast in 2033 | USD 8.3 billion |

| Growth Rate | 7.2% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Ball Corporation, Crown Holdings, Inc., Ardagh Group S.A., Silgan Holdings Inc., CPMC Holdings Limited, EXAL Corporation, Toyo Seikan Group Holdings, Ltd., Berlin Packaging, Trivium Packaging, CCL Industries Inc., Kian Joo Can Factory Berhad, Nampak Ltd., CAN-PACK S.A., Universal Can Corporation, Independent Can Company, BWAY Corporation, Mauser Packaging Solutions, Allied Container Corporation, U.S. Can Company Inc., Rexam PLC (part of Ball Corporation) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The BPA Free Can market is meticulously segmented to provide a granular understanding of its diverse components and drivers. These segmentations allow for a detailed analysis of market dynamics across various dimensions, revealing specific growth pockets, consumer preferences, and technological shifts. The primary segmentation categories include material type, application, end-use industry, and can capacity, each offering unique insights into the market's structure and potential.

Analysis by material type examines the prevalent use of aluminum, steel, and tinplate, reflecting the industry's reliance on specific metals for different can types and their respective advantages in terms of recyclability, durability, and cost. Application segmentation differentiates between food, beverage, aerosol, and general line cans, highlighting the dominant sectors adopting BPA-free solutions. The end-use industry breakdown further dissects the market into sub-industries such as various food and beverage categories, personal care, and healthcare, illustrating the expanding reach of BPA-free packaging. Capacity segmentation provides insights into preferred can sizes for different products, impacting production efficiencies and consumer convenience.

- By Material:

- Aluminum

- Steel

- Tinplate

- Others

- By Application:

- Food Cans

- Beverage Cans

- Aerosol Cans

- General Line Cans

- By End-use Industry:

- Food & Beverage

- Fruits & Vegetables

- Meat & Seafood

- Dairy & Desserts

- Beverages

- Pet Food

- Personal Care

- Healthcare

- Others (Paints, Chemicals)

- Food & Beverage

- By Capacity:

- 0-250 ml

- 251-500 ml

- 501-750 ml

- Above 750 ml

Regional Highlights

- North America: The North American market is a significant adopter of BPA-free cans, driven by high consumer health awareness and proactive regulatory initiatives, particularly in the United States and Canada. The region benefits from established packaging infrastructure and a strong presence of key market players, leading to early adoption of innovative BPA-free solutions across food and beverage sectors.

- Europe: Europe stands out due to its stringent regulatory environment regarding food contact materials, which has significantly pushed the adoption of BPA-free packaging. Countries like Germany, France, and the UK are leading in sustainable packaging trends and advanced coating technologies, fostering a robust market for BPA-free cans, further supported by high consumer demand for safe and eco-friendly products.

- Asia Pacific (APAC): The Asia Pacific region is projected to be the fastest-growing market for BPA-free cans, fueled by rapid urbanization, increasing disposable incomes, and a growing middle-class population. Countries such as China, India, and Japan are experiencing a surge in demand for packaged food and beverages, alongside rising health consciousness, driving the shift towards safer packaging solutions.

- Latin America: The Latin American market for BPA-free cans is exhibiting steady growth, influenced by evolving consumer preferences and increasing awareness regarding food safety. Economic development and the expansion of the retail sector in countries like Brazil and Mexico are contributing to the rising demand for packaged goods, thereby creating opportunities for BPA-free packaging adoption.

- Middle East & Africa (MEA): The MEA region presents emerging opportunities for the BPA-free can market. Growth is primarily driven by increasing investments in food and beverage processing, coupled with a nascent but growing consumer awareness about health and safety. While starting from a smaller base, the region is expected to witness gradual adoption of BPA-free solutions as regulatory frameworks mature and consumer education improves.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the BPA Free Can Market.- Ball Corporation

- Crown Holdings, Inc.

- Ardagh Group S.A.

- Silgan Holdings Inc.

- CPMC Holdings Limited

- EXAL Corporation

- Toyo Seikan Group Holdings, Ltd.

- Berlin Packaging

- Trivium Packaging

- CCL Industries Inc.

- Kian Joo Can Factory Berhad

- Nampak Ltd.

- CAN-PACK S.A.

- Universal Can Corporation

- Independent Can Company

- BWAY Corporation

- Mauser Packaging Solutions

- Allied Container Corporation

- U.S. Can Company Inc.

- Rexam PLC (part of Ball Corporation)

Frequently Asked Questions

What is a BPA Free Can?

A BPA Free Can is a food or beverage container manufactured without the use of Bisphenol A (BPA) in its internal lining. BPA is a chemical often used in epoxy resins for can coatings, and BPA-free cans utilize alternative coatings, such as acrylic or polyester-based materials, to ensure food safety and consumer health.

Why is BPA-free packaging important?

BPA-free packaging is important because BPA has been linked to potential health concerns, including hormonal disruptions and reproductive issues, when it leaches into food or beverages. Opting for BPA-free cans reduces consumer exposure to this chemical, aligning with increasing consumer demand for safer food contact materials and regulatory health guidelines.

What is the projected growth rate for the BPA Free Can Market?

The BPA Free Can Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.2% between 2025 and 2033. This growth is primarily driven by heightened consumer awareness, stricter health regulations, and continuous innovation in alternative coating technologies.

What are the key drivers of the BPA Free Can Market?

Key drivers include increasing consumer health awareness regarding BPA's potential risks, stringent food safety regulations mandating BPA-free packaging, and technological advancements in the development of safer and more effective alternative can coatings and materials.

Which regions are leading in BPA Free Can adoption?

North America and Europe are currently leading in BPA Free Can adoption due to established regulatory frameworks and high consumer health consciousness. However, the Asia Pacific region is projected to be the fastest-growing market, driven by expanding economies and increasing awareness.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted