Blood and Organ Bank Market

Blood and Organ Bank Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701361 | Last Updated : July 29, 2025 |

Format : ![]()

![]()

![]()

![]()

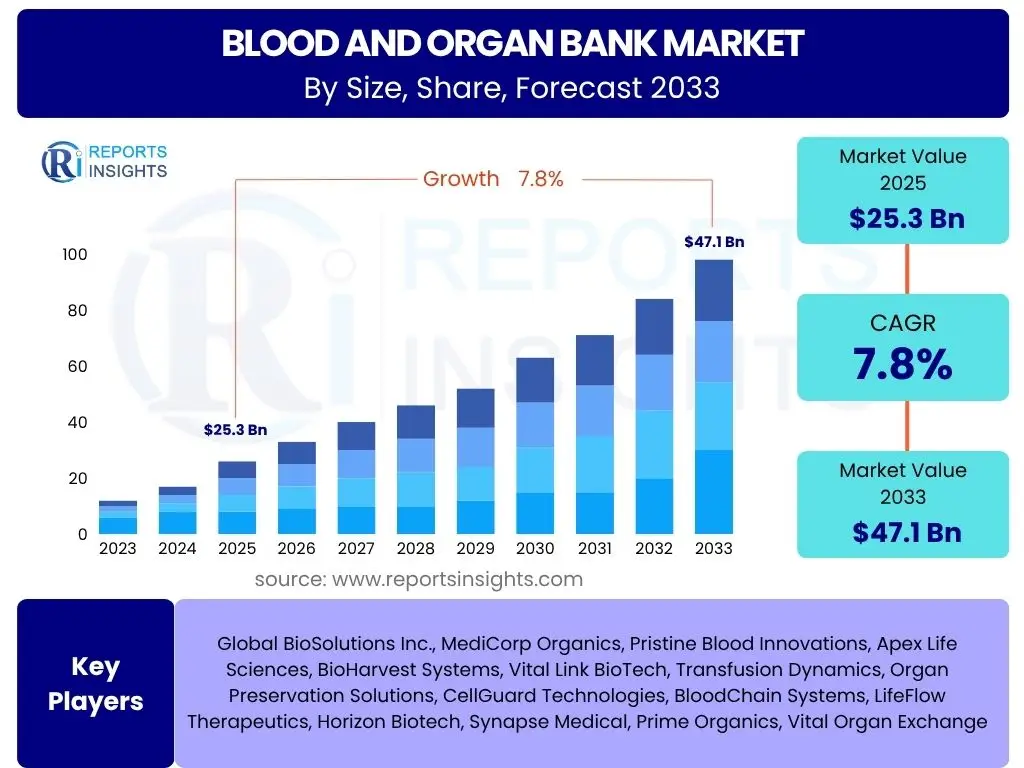

Blood and Organ Bank Market Size

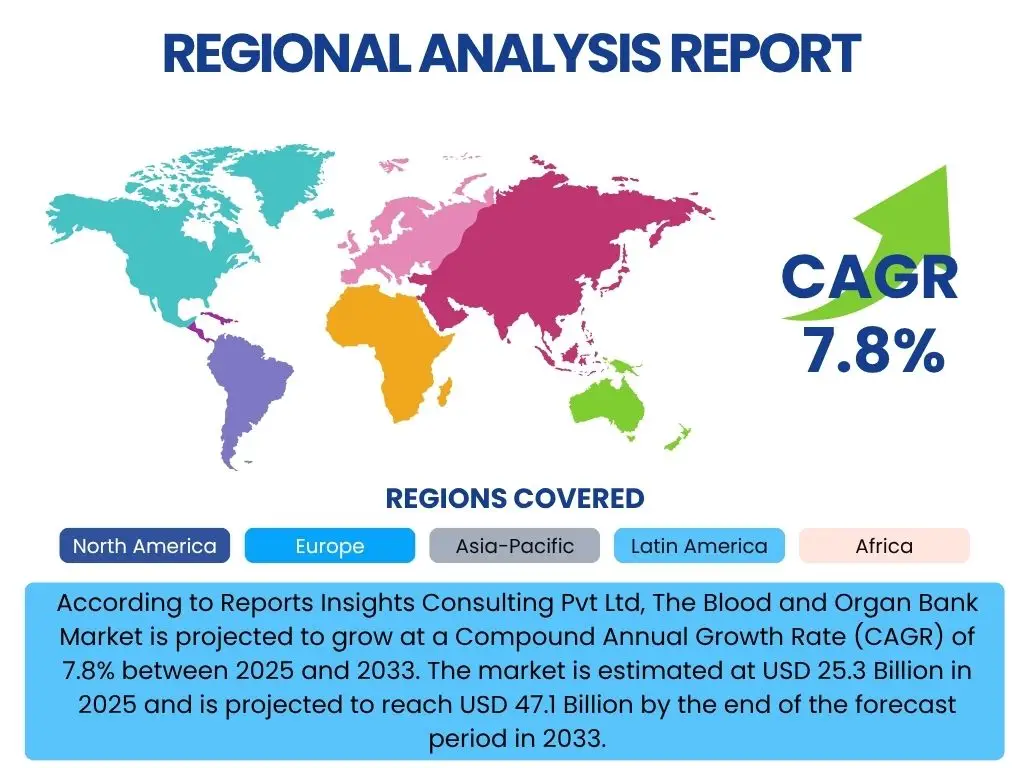

According to Reports Insights Consulting Pvt Ltd, The Blood and Organ Bank Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033. The market is estimated at USD 25.3 Billion in 2025 and is projected to reach USD 47.1 Billion by the end of the forecast period in 2033.

Key Blood and Organ Bank Market Trends & Insights

The Blood and Organ Bank market is undergoing significant transformation driven by advancements in medical science, technological integration, and evolving healthcare needs. Common user questions often revolve around how these factors are shaping the future of organ and blood management, particularly concerning donor availability, operational efficiency, and the ethical implications of new technologies. The market is witnessing a shift towards more streamlined, digitally integrated systems for better inventory management and distribution, aiming to overcome traditional logistical challenges.

Furthermore, increased research and development in areas such as regenerative medicine, synthetic blood substitutes, and xenotransplantation are creating new avenues for addressing critical shortages. There is also a growing emphasis on personalized medicine, leading to more precise donor-recipient matching and a reduction in rejection rates. These trends collectively underscore a move towards a more robust, efficient, and patient-centric blood and organ banking ecosystem.

- Digitalization and automation of blood and organ management systems for enhanced efficiency and traceability.

- Rising adoption of regenerative medicine and cell therapies, influencing demand for specific biological materials.

- Increasing focus on personalized transplantation, driven by advanced tissue typing and immunosuppressive therapies.

- Expansion of global collaboration networks to facilitate cross-border sharing of rare blood types and organs.

- Development of novel preservation techniques extending the viability of blood and organ products.

AI Impact Analysis on Blood and Organ Bank

User inquiries regarding the impact of Artificial Intelligence (AI) on the Blood and Organ Bank sector frequently explore its potential to revolutionize operational workflows, improve donor-recipient matching accuracy, and enhance overall safety and efficiency. AI is increasingly being leveraged to analyze vast datasets, including patient medical histories, genetic profiles, and donor information, to identify optimal matches with unprecedented precision. This capability is critical in reducing transplant rejection rates and improving patient outcomes, directly addressing a core challenge in transplantation medicine.

Beyond matching, AI's influence extends to optimizing logistics, cold chain management, and inventory prediction. Predictive analytics powered by AI algorithms can forecast demand for specific blood types or organs, minimizing waste and ensuring timely availability. Additionally, AI-driven solutions are being explored for automated screening of blood products for pathogens and for assessing organ viability, thereby enhancing safety protocols. While concerns exist regarding data privacy and the ethical implications of AI-driven allocation decisions, the overwhelming consensus points towards AI as a transformative force capable of making blood and organ banking more intelligent, responsive, and ultimately, life-saving.

- AI-driven optimization of donor-recipient matching algorithms, significantly improving transplant success rates.

- Enhanced logistical planning and inventory management through predictive analytics for blood and organ demand.

- Automated screening and quality assessment of blood products and organs, reducing human error and improving safety.

- Development of decision support systems for clinicians in organ allocation, ensuring equitable and efficient distribution.

- Accelerated research and development in identifying new preservation methods and understanding organ viability.

Key Takeaways Blood and Organ Bank Market Size & Forecast

Common user questions about the Blood and Organ Bank market size and forecast often focus on the primary drivers of growth, the resilience of the market against various challenges, and the long-term investment opportunities available. A significant takeaway is the consistent upward trajectory of the market, primarily fueled by the escalating global burden of chronic diseases requiring transfusions and transplants, coupled with an aging population that increasingly requires such interventions. This underlying demand ensures sustained growth despite intermittent challenges related to donor shortages or logistical complexities.

Another crucial insight is the pivotal role of technological innovation in shaping the market's future. Advancements in preservation techniques, diagnostic tools, and digital platforms for inventory and logistics management are not merely incremental improvements but represent fundamental shifts that enhance efficiency and expand capabilities. Consequently, investment in research and development, alongside strategic partnerships to improve infrastructure, will be key determinants of success for market participants. The forecast indicates a robust market with ample opportunities for entities capable of integrating cutting-edge solutions and navigating the evolving regulatory and ethical landscape.

- The market is poised for significant growth, driven by increasing chronic disease prevalence and an aging global population.

- Technological advancements in preservation, testing, and AI-driven matching are critical growth enablers.

- Donor scarcity remains a persistent challenge, necessitating innovative solutions in donor recruitment and alternative therapies.

- Regional disparities in healthcare infrastructure and regulatory frameworks will influence market growth patterns.

- Strategic collaborations among healthcare providers, research institutions, and technology firms are vital for market expansion.

Blood and Organ Bank Market Drivers Analysis

The Blood and Organ Bank market is propelled by a confluence of factors that collectively drive demand and foster innovation. A primary driver is the global increase in the incidence of chronic diseases such as kidney failure, liver disease, cardiovascular conditions, and various cancers, which necessitate organ transplantation or regular blood transfusions. This epidemiological shift places continuous demand on blood and organ banks worldwide.

Additionally, advancements in medical technology and surgical techniques have significantly improved the success rates of transplants and transfusions, making these procedures more viable and accessible. Coupled with a rising geriatric population, who are more susceptible to age-related organ failures and require extensive healthcare support, the market experiences sustained demand. Government initiatives, increasing healthcare expenditure, and growing public awareness about organ donation also contribute significantly to market expansion by improving infrastructure and donor pools.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Prevalence of Chronic Diseases | +1.5% | Global | Long-term |

| Advancements in Transplantation and Transfusion Techniques | +1.2% | Developed Nations (North America, Europe) | Mid-term |

| Rising Geriatric Population | +1.0% | North America, Europe, East Asia | Long-term |

| Growing Awareness and Government Initiatives for Organ Donation | +0.8% | Global | Mid-term |

| Increasing Healthcare Expenditure and Infrastructure Development | +0.7% | Asia Pacific, Latin America | Mid-term |

Blood and Organ Bank Market Restraints Analysis

Despite robust growth drivers, the Blood and Organ Bank market faces several significant restraints that impede its full potential. A persistent and critical challenge is the chronic shortage of available donors, both for blood and organs. Demand consistently outstrips supply, leading to long waiting lists for organ transplants and potential delays in life-saving transfusions, particularly for rare blood types. This scarcity is a direct consequence of a relatively small donor pool compared to the vast patient need, often compounded by logistical hurdles in retrieval and transport.

Furthermore, the high cost associated with blood and organ collection, processing, storage, and distribution, combined with the expensive nature of transplantation surgeries and post-operative care, acts as a significant barrier. These costs can be prohibitive for patients and healthcare systems, particularly in developing economies, limiting access to essential services. Stringent regulatory frameworks and complex ethical considerations surrounding donation and allocation also add layers of complexity and can slow down the adoption of new technologies or expansion of services. Concerns about disease transmission through donated products, although rare due to advanced screening, continue to pose a psychological barrier and necessitate rigorous and costly testing protocols.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Shortage of Donors (Blood and Organ) | -1.5% | Global | Long-term |

| High Cost of Procedures and Infrastructure | -1.0% | Developing Nations, Payer Systems | Long-term |

| Strict Regulatory Frameworks and Ethical Concerns | -0.8% | Europe, North America | Mid-term |

| Logistical Complexities and Cold Chain Management | -0.5% | Global, Remote Regions | Short-term |

| Risk of Disease Transmission (despite screening) | -0.4% | Global | Short-term |

Blood and Organ Bank Market Opportunities Analysis

Despite existing challenges, the Blood and Organ Bank market presents numerous opportunities for innovation and growth. A significant area of potential lies in the advancement of alternative therapies, such as the development of artificial organs, xenotransplantation, and lab-grown tissues. These emerging technologies hold the promise of alleviating donor shortages by providing viable substitutes or supplements, thereby transforming the landscape of organ replacement and reducing patient waiting lists. Extensive research in these fields is opening doors for entirely new product categories and service offerings.

Furthermore, the expansion into untapped emerging economies offers substantial growth prospects. These regions often have large populations with increasing healthcare demands but underdeveloped blood and organ banking infrastructures. Investing in these markets, establishing partnerships, and adapting services to local needs can unlock considerable market share. The integration of advanced digital technologies like AI, blockchain, and big data analytics can revolutionize supply chain efficiency, enhance donor matching accuracy, and improve traceability, creating more robust and reliable systems. Public-private partnerships and increased funding for research and infrastructure development also represent key opportunities to address systemic issues and accelerate market evolution.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Artificial Organs and Xenotransplantation | +1.8% | Global | Long-term |

| Expansion into Emerging Economies | +1.5% | Asia Pacific, Latin America, Africa | Mid-term to Long-term |

| Integration of AI, Blockchain, and Big Data for Supply Chain Optimization | +1.2% | Developed Nations | Mid-term |

| Growth in Personalized Medicine and Cell & Gene Therapies | +1.0% | Global | Long-term |

| Public-Private Partnerships for Infrastructure Development | +0.9% | Developing Nations | Mid-term |

Blood and Organ Bank Market Challenges Impact Analysis

The Blood and Organ Bank market faces several inherent challenges that demand strategic solutions. One critical challenge is maintaining the integrity of the cold chain and ensuring optimal preservation conditions from donor to recipient. The highly perishable nature of blood and organs requires sophisticated logistical networks and specialized equipment, making transport and storage complex and expensive, particularly across vast geographical distances or in regions with limited infrastructure. Any lapse in the cold chain can render products unusable, leading to wastage and endangering patient lives.

Another significant hurdle is donor recruitment and retention. Despite awareness campaigns, the pool of eligible donors remains insufficient to meet the ever-growing demand, especially for organs and specific blood types. Ethical dilemmas surrounding organ allocation, particularly in situations of scarcity, also present a complex challenge, requiring transparent and equitable policies. Furthermore, the sensitive nature of patient and donor data makes cybersecurity a paramount concern, as breaches could lead to severe privacy violations and undermine public trust. The market also faces competition from evolving alternative therapies, which, while offering new solutions, can also shift demand away from traditional blood and organ banking services, prompting the need for continuous adaptation and innovation.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Maintaining Cold Chain Integrity and Logistics | -1.2% | Global, especially Developing Regions | Short-term |

| Donor Recruitment and Retention | -1.0% | Global | Long-term |

| Ethical Dilemmas in Organ Allocation | -0.7% | Global | Mid-term |

| Cybersecurity Risks for Sensitive Data | -0.6% | Global | Short-term |

| Competition from Alternative Therapies | -0.5% | Developed Nations | Mid-term |

Blood and Organ Bank Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Blood and Organ Bank market, offering a detailed assessment of its current landscape, historical performance, and future growth projections. The scope encompasses a thorough examination of market dynamics, including key drivers, restraints, opportunities, and challenges influencing industry expansion. It further delves into a detailed segmentation analysis, categorizing the market by product/service, application, end-user, and key geographical regions, providing a granular understanding of market trends and revenue streams across various segments. The report also features profiles of leading market players, competitive landscape analysis, and a projection of the market's trajectory through 2033, serving as an essential resource for stakeholders seeking strategic insights.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 25.3 Billion |

| Market Forecast in 2033 | USD 47.1 Billion |

| Growth Rate | 7.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global BioSolutions Inc., MediCorp Organics, Pristine Blood Innovations, Apex Life Sciences, BioHarvest Systems, Vital Link BioTech, Transfusion Dynamics, Organ Preservation Solutions, CellGuard Technologies, BloodChain Systems, LifeFlow Therapeutics, Horizon Biotech, Synapse Medical, Prime Organics, Vital Organ Exchange |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Blood and Organ Bank market is segmented to provide a granular view of its various components and their respective contributions to overall market dynamics. This segmentation helps in identifying specific growth areas, understanding consumer preferences, and evaluating competitive landscapes within distinct market niches. By dissecting the market based on product types, applications, and end-users, stakeholders can pinpoint key investment opportunities and develop targeted strategies that cater to diverse requirements across the healthcare ecosystem.

Each segment within the market reflects unique demand drivers and technological advancements. For instance, the blood products segment is driven by routine medical needs and emergency care, while the organ products segment is influenced by chronic disease prevalence and transplant success rates. Similarly, end-user segments like hospitals and research institutions have distinct needs for blood and organ banking services, influencing service delivery models and technological adoption. This comprehensive segmentation analysis is crucial for a nuanced understanding of market behavior and future projections.

- By Product/Service:

- Blood Products: Whole Blood, Plasma, Platelets, Red Blood Cells, Other Blood Components

- Organ Products: Kidney, Liver, Heart, Lung, Pancreas, Intestine, Other Organs

- Services: Collection, Processing, Storage, Distribution, Testing

- By Application:

- Transfusions

- Transplants

- Research & Development

- By End-User:

- Hospitals

- Specialty Clinics

- Academic & Research Institutions

- Pharmaceutical & Biotechnology Companies

Regional Highlights

- North America: This region dominates the Blood and Organ Bank market, driven by advanced healthcare infrastructure, high healthcare expenditure, significant R&D investments, and a high prevalence of chronic diseases. The presence of leading research institutions and well-established regulatory frameworks also contributes to its market leadership. Early adoption of advanced technologies like AI and automated systems is a key characteristic.

- Europe: Characterized by strong government support for healthcare, increasing awareness about organ donation, and a growing geriatric population, Europe represents a substantial market. However, stringent regulatory policies and varying levels of donor participation across countries influence regional growth dynamics. Focus on quality control and ethical considerations is paramount.

- Asia Pacific (APAC): Expected to exhibit the highest growth rate, primarily due to rapidly improving healthcare infrastructure, a large patient pool, increasing medical tourism, and rising healthcare expenditure in countries like China, India, and Japan. Opportunities abound for technology adoption and the establishment of new blood and organ banking facilities to meet burgeoning demand.

- Latin America: This region shows promising growth potential, fueled by increasing investment in healthcare, rising prevalence of non-communicable diseases, and improving access to medical services. Challenges include fragmented healthcare systems and socio-economic disparities, but efforts towards international collaborations and public awareness campaigns are driving progress.

- Middle East and Africa (MEA): The MEA region is a nascent but emerging market, with growth driven by increasing government initiatives to improve healthcare services, rising incidence of chronic diseases, and a growing focus on medical tourism in certain countries. Infrastructure development and partnerships are key to unlocking its full market potential, especially in areas with limited access to advanced medical facilities.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Blood and Organ Bank Market.- Global BioSolutions Inc.

- MediCorp Organics

- Pristine Blood Innovations

- Apex Life Sciences

- BioHarvest Systems

- Vital Link BioTech

- Transfusion Dynamics

- Organ Preservation Solutions

- CellGuard Technologies

- BloodChain Systems

- LifeFlow Therapeutics

- Horizon Biotech

- Synapse Medical

- Prime Organics

- Vital Organ Exchange

- MedGene Innovations

- SecureBio Labs

- Quantum Health Solutions

- Regenesis Bio

- Future Blood Banks

Frequently Asked Questions

What factors are driving the growth of the Blood and Organ Bank market?

The market is primarily driven by the increasing global prevalence of chronic diseases requiring transfusions and transplants, an aging population, and significant advancements in medical technologies and surgical techniques. Growing awareness about organ donation and supportive government initiatives also contribute to market expansion.

How is artificial intelligence impacting the Blood and Organ Bank sector?

AI is transforming the sector by enhancing donor-recipient matching accuracy, optimizing logistics and inventory management through predictive analytics, and improving the automated screening and quality assessment of blood and organs. It aims to increase efficiency, reduce waste, and enhance patient safety.

What are the main challenges faced by the Blood and Organ Bank market?

Key challenges include the persistent shortage of donors, the high costs associated with collection, processing, and transplantation, stringent regulatory frameworks, logistical complexities in maintaining the cold chain, and the ongoing risk of disease transmission through donated products.

Which regions are expected to show significant growth in the Blood and Organ Bank market?

The Asia Pacific region is anticipated to exhibit the highest growth rate due to improving healthcare infrastructure, a large patient pool, and increasing healthcare expenditure. North America currently dominates the market due to advanced technology adoption and robust healthcare systems.

What emerging opportunities exist within the Blood and Organ Bank market?

Significant opportunities lie in the development of artificial organs and xenotransplantation, expansion into emerging economies with underserved healthcare needs, and the integration of advanced digital technologies like blockchain for enhanced supply chain integrity and data management.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted