Bladder and Diaphragm Hydraulic Accumulator Market

Bladder and Diaphragm Hydraulic Accumulator Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_710371 | Last Updated : January 05, 2026 |

Format : ![]()

![]()

![]()

![]()

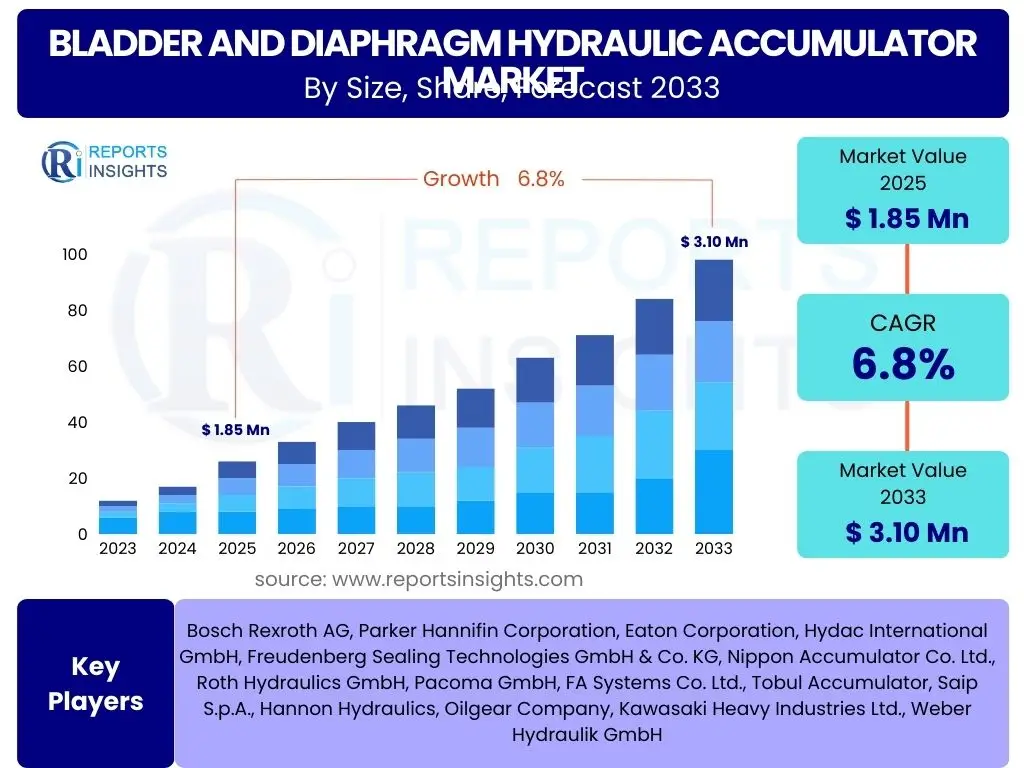

Bladder and Diaphragm Hydraulic Accumulator Market Size

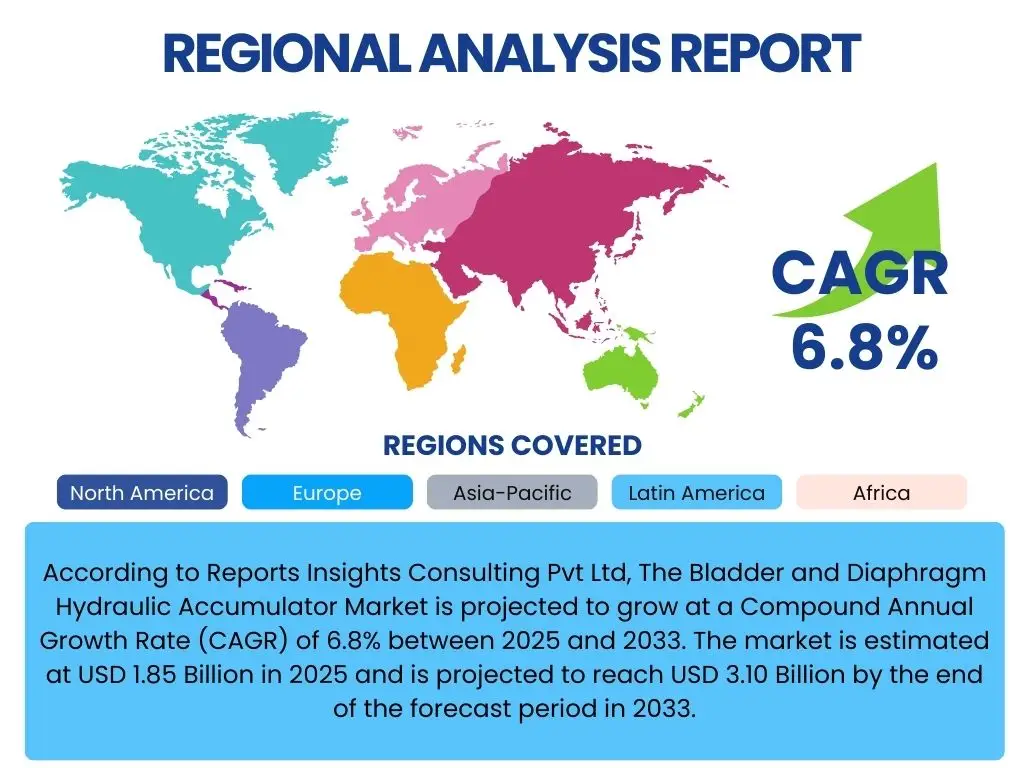

According to Reports Insights Consulting Pvt Ltd, The Bladder and Diaphragm Hydraulic Accumulator Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 1.85 Billion in 2025 and is projected to reach USD 3.10 Billion by the end of the forecast period in 2033.

Key Bladder and Diaphragm Hydraulic Accumulator Market Trends & Insights

Current market trends reveal a significant shift towards enhanced energy efficiency and sustainability in hydraulic systems. Users are increasingly seeking solutions that reduce operational costs and environmental impact, driving the demand for advanced accumulator technologies. There is also a notable emphasis on digitalization and smart system integration, as end-users look to leverage data for predictive maintenance and optimized performance. The demand for compact and lightweight accumulator designs is also on the rise, particularly in mobile applications where space and weight are critical considerations. These trends collectively underscore an industry-wide push for innovation, aiming to meet evolving operational demands and stringent regulatory standards.

The market is also witnessing an uptake in specialized applications requiring high-pressure resistance and robust performance in extreme environments. This includes sectors such as offshore oil and gas, heavy construction, and aerospace, where traditional accumulators may fall short. Furthermore, the global expansion of industrial automation and robotics contributes to the demand for reliable hydraulic components capable of precise control and rapid response. The trend toward modular hydraulic systems is simplifying installation and maintenance, making bladder and diaphragm accumulators more accessible and adaptable across various industrial setups. These dynamics indicate a market evolving not only through technological advancement but also through greater integration into complex, high-performance applications.

- Increasing demand for energy-efficient hydraulic systems.

- Growing adoption of smart accumulators with integrated sensors for predictive maintenance.

- Miniaturization and lightweight designs for mobile and compact machinery.

- Emphasis on sustainable materials and manufacturing processes.

- Expansion of hydraulic accumulator applications in renewable energy sectors.

- Development of high-pressure and high-temperature resistant designs for extreme environments.

- Rise in automation and robotics requiring precise hydraulic control.

- Increased focus on modular and easily replaceable hydraulic components.

AI Impact Analysis on Bladder and Diaphragm Hydraulic Accumulator

User queries regarding AI's impact on bladder and diaphragm hydraulic accumulators primarily revolve around enhancing efficiency, predictive maintenance, and autonomous operation. Stakeholders are keen to understand how AI can optimize accumulator performance, detect potential failures before they occur, and reduce downtime. The expectation is that AI-driven insights will lead to more intelligent hydraulic systems, offering improved reliability and lower lifecycle costs. Concerns also exist regarding data security, the complexity of integrating AI into existing infrastructure, and the need for skilled personnel to manage these advanced systems. Overall, there is a strong interest in leveraging AI to move beyond traditional reactive maintenance towards a proactive, data-informed approach to hydraulic system management.

The integration of artificial intelligence is poised to revolutionize how hydraulic accumulators are monitored and maintained, moving towards 'smart' systems that can self-diagnose and optimize their performance. This includes the use of machine learning algorithms to analyze sensor data from accumulators, predicting wear patterns, fluid contamination, and pressure fluctuations with unprecedented accuracy. Such capabilities promise to significantly extend the operational life of accumulators and prevent catastrophic failures. Moreover, AI can play a crucial role in system-level optimization, ensuring accumulators operate at peak efficiency within larger hydraulic circuits, thereby contributing to overall energy savings and reduced carbon footprint. The long-term vision involves fully autonomous hydraulic systems where AI dynamically adjusts accumulator parameters based on real-time operational demands, further enhancing system responsiveness and adaptability.

- Predictive Maintenance: AI algorithms analyze sensor data (pressure, temperature, vibration) to predict accumulator failure, allowing for proactive maintenance and reducing unexpected downtime.

- Performance Optimization: AI-driven control systems can adjust accumulator parameters in real-time to optimize energy storage and release, enhancing overall hydraulic system efficiency.

- Anomaly Detection: Machine learning models can identify subtle deviations from normal operating conditions, signaling potential issues before they escalate.

- Design & Simulation: AI assists in the design phase by simulating accumulator performance under various conditions, leading to more robust and efficient designs.

- Automated Diagnostics: AI-powered diagnostic tools can quickly pinpoint faults in hydraulic systems, including those related to accumulators, streamlining troubleshooting.

- Operational Efficiency: AI helps optimize fluid management and power consumption within hydraulic systems, leveraging accumulators for peak efficiency during cyclic operations.

Key Takeaways Bladder and Diaphragm Hydraulic Accumulator Market Size & Forecast

The bladder and diaphragm hydraulic accumulator market is set for robust expansion, driven primarily by increasing industrial automation, the imperative for energy efficiency, and the growing demand for reliable hydraulic solutions across diverse sectors. Key insights highlight a consistent upward trajectory in market value, reflecting the indispensable role these components play in modern machinery and infrastructure. The projected growth underscores a sustained need for power compensation, shock absorption, and emergency power in both mobile and industrial applications. This indicates a resilient market, less susceptible to short-term economic fluctuations due due to its foundational utility across various manufacturing and operational processes globally.

Furthermore, the market's evolution is characterized by technological advancements focusing on durability, performance in harsh environments, and integration with smart systems. The move towards more compact and high-performance designs, coupled with advancements in materials science, is addressing specific end-user requirements and opening new application avenues. Regions like Asia Pacific are emerging as significant growth engines, fueled by rapid industrialization and infrastructure development. The competitive landscape remains dynamic, with key players investing in R&D to capture market share through innovative product offerings. These factors collectively point to a healthy and expanding market with considerable opportunities for both established companies and new entrants focusing on specialized solutions.

- The market is projected for significant growth, reaching USD 3.10 Billion by 2033, demonstrating strong market demand.

- CAGR of 6.8% indicates a steady and healthy growth trajectory driven by industrial and mobile applications.

- Emphasis on energy efficiency and sustainable solutions is a primary market driver.

- Technological advancements in design, materials, and smart integration are crucial for market differentiation.

- Asia Pacific remains a key growth region due to ongoing industrialization and infrastructure projects.

- The market is resilient, supported by essential applications in machinery, construction, agriculture, and manufacturing.

Bladder and Diaphragm Hydraulic Accumulator Market Drivers Analysis

The global surge in industrial automation and the increasing mechanization of various sectors constitute a primary driver for the bladder and diaphragm hydraulic accumulator market. As industries strive for higher efficiency, precision, and productivity, the demand for sophisticated hydraulic systems, which often incorporate accumulators for energy storage and pulsation dampening, escalates. This trend is particularly evident in manufacturing, material handling, and heavy machinery sectors, where hydraulic accumulators are critical for optimizing operational cycles and reducing energy consumption. The continuous investment in smart factories and automated production lines worldwide further solidifies this driver's impact, ensuring a sustained need for these essential components.

Another significant driver is the growing focus on energy efficiency and environmental sustainability across industries. Hydraulic accumulators play a vital role in regenerative braking systems, energy recovery in cyclic operations, and maintaining constant pressure, thereby reducing the overall power consumption of hydraulic systems. With stricter environmental regulations and rising energy costs, businesses are actively seeking solutions that minimize their carbon footprint and operational expenditures. This impetus for green technologies positions bladder and diaphragm accumulators as indispensable components in achieving more sustainable and cost-effective hydraulic power management. The integration of accumulators in renewable energy infrastructure, such as wind turbine pitch control, also exemplifies this trend.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Industrial Automation & Mechanization | +1.8% | Global, particularly APAC (China, India), North America, Europe | Short to Long-term (2025-2033) |

| Growing Demand for Energy-Efficient Hydraulic Systems | +1.5% | Europe, North America, Japan | Mid to Long-term (2026-2033) |

| Expansion of Construction and Infrastructure Activities | +1.2% | APAC, Middle East & Africa, Latin America | Short to Mid-term (2025-2030) |

| Technological Advancements in Hydraulic Systems | +0.9% | Global | Long-term (2028-2033) |

| Rising Adoption in Mobile Equipment (Agriculture, Mining) | +0.8% | North America, Europe, Brazil, Australia | Short to Mid-term (2025-2030) |

| Focus on Predictive Maintenance and IIoT Integration | +0.6% | Developed Economies | Mid to Long-term (2027-2033) |

Bladder and Diaphragm Hydraulic Accumulator Market Restraints Analysis

One significant restraint in the bladder and diaphragm hydraulic accumulator market is the volatility in raw material prices, particularly for steel, rubber, and specialized alloys. These materials are crucial for the construction of accumulator shells and diaphragms/bladders, and their price fluctuations directly impact manufacturing costs. Such instability makes it challenging for manufacturers to maintain consistent pricing strategies and profit margins, potentially leading to higher end-product costs for consumers. This volatility is often influenced by global supply chain disruptions, geopolitical events, and demand-supply imbalances, creating an unpredictable cost environment for market participants.

Another impediment to market growth is the intense competition from alternative power transmission technologies and other energy storage solutions. While hydraulic accumulators offer distinct advantages in certain applications, the continuous development of electric and electromechanical actuators provides viable alternatives, especially in scenarios prioritizing noise reduction or where hydraulic power is deemed less efficient. The initial cost of installing and maintaining hydraulic systems, including accumulators, can also be higher compared to some electric counterparts, particularly for smaller-scale applications, which might deter potential buyers from adopting hydraulic solutions. Moreover, the need for specialized expertise in hydraulic system design and maintenance can also act as a barrier to wider adoption in regions with limited skilled labor.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile Raw Material Prices (Steel, Rubber, Alloys) | -0.7% | Global | Short to Mid-term (2025-2028) |

| High Initial Investment & Maintenance Costs | -0.5% | Developing Economies | Short to Mid-term (2025-2029) |

| Competition from Alternative Power Transmission Technologies | -0.4% | North America, Europe | Mid to Long-term (2027-2033) |

| Complexity in System Integration and Design | -0.3% | Emerging Markets | Short to Mid-term (2025-2028) |

| Lack of Skilled Workforce for Installation and Maintenance | -0.2% | Certain Developing Regions | Long-term (2028-2033) |

Bladder and Diaphragm Hydraulic Accumulator Market Opportunities Analysis

The burgeoning market for renewable energy infrastructure, particularly wind and solar power generation, presents a significant opportunity for the bladder and diaphragm hydraulic accumulator market. Accumulators are integral to the pitch control systems of wind turbines, providing rapid and precise blade adjustments for optimal energy capture and safety. As global investment in green energy solutions accelerates, the demand for reliable and efficient hydraulic components in this sector is expected to rise substantially. This represents a new frontier for market expansion, moving beyond traditional industrial applications into an area driven by environmental mandates and technological advancements in sustainable energy production. Furthermore, the development of tidal and wave energy technologies could also open up new niches for specialized hydraulic accumulators.

Another compelling opportunity lies in the retrofitting and upgrading of existing hydraulic systems to meet modern efficiency standards and incorporate smart technologies. Many legacy industrial and mobile equipment fleets operate with older, less efficient hydraulic systems. The push for greater operational efficiency, reduced energy consumption, and compliance with updated environmental regulations creates a strong incentive for end-users to upgrade their machinery with advanced hydraulic accumulators. This not only involves replacing older components but also integrating new smart accumulators equipped with sensors and IoT capabilities for real-time monitoring and predictive maintenance. This upgrade cycle represents a consistent revenue stream and allows manufacturers to introduce their latest innovations to a broad installed base, extending market reach and ensuring long-term relevance.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Adoption in Renewable Energy Sector (Wind Turbines) | +1.1% | Europe, North America, China, India | Mid to Long-term (2027-2033) |

| Retrofitting and Upgrading Existing Hydraulic Systems | +0.9% | Developed Economies | Short to Mid-term (2025-2030) |

| Emergence of Smart Accumulators with IoT and AI Integration | +0.8% | Global | Long-term (2028-2033) |

| Untapped Markets in Developing Economies (Infrastructure Growth) | +0.7% | Africa, Southeast Asia, Latin America | Short to Mid-term (2025-2030) |

| Growth in High-Pressure & Harsh Environment Applications | +0.6% | Oil & Gas, Marine, Aerospace | Mid to Long-term (2027-2033) |

Bladder and Diaphragm Hydraulic Accumulator Market Challenges Impact Analysis

One primary challenge facing the bladder and diaphragm hydraulic accumulator market is the stringent regulatory landscape, particularly concerning safety standards and environmental compliance. Hydraulic systems, operating under high pressures, are subject to rigorous safety protocols to prevent accidents and ensure operational reliability. Compliance with international standards such as CE, ASME, and ISO requires significant investment in product development, testing, and certification, which can increase manufacturing costs and time-to-market. Furthermore, environmental regulations concerning fluid disposal, leak prevention, and the use of certain materials or chemicals can impose additional burdens on manufacturers, necessitating continuous adaptation of product designs and processes. Navigating these complex and evolving regulatory requirements is a continuous hurdle for market participants.

Another significant challenge is the ongoing need for product innovation and differentiation in a highly competitive market. With numerous established players and continuous technological advancements, manufacturers must constantly invest in research and development to offer superior products that stand out. This includes developing accumulators with enhanced durability, higher pressure ratings, broader temperature ranges, and features that support integration with smart systems. Failing to innovate can lead to market share erosion and reduced profitability. Moreover, educating end-users about the long-term benefits of advanced accumulators, despite potentially higher initial costs, presents a communication challenge that requires effective market positioning and technical support strategies. The rapid pace of technological change in adjacent industries also places pressure on accumulator manufacturers to keep pace.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Safety and Environmental Regulations | -0.6% | Europe, North America | Short to Long-term (2025-2033) |

| Need for Continuous Product Innovation & Differentiation | -0.5% | Global | Mid to Long-term (2027-2033) |

| Technical Expertise Requirements for Maintenance & Service | -0.4% | Emerging Markets | Short to Mid-term (2025-2030) |

| Counterfeit Products & Intellectual Property Infringement | -0.3% | APAC (certain regions) | Short to Mid-term (2025-2028) |

| Supply Chain Disruptions and Geopolitical Instability | -0.2% | Global | Short-term (2025-2026) |

Bladder and Diaphragm Hydraulic Accumulator Market - Updated Report Scope

This report provides a comprehensive analysis of the global bladder and diaphragm hydraulic accumulator market, offering detailed insights into market size, growth drivers, restraints, opportunities, and challenges. It covers in-depth segmentation across various types, applications, and end-use industries, alongside a thorough regional breakdown. The report’s scope also encompasses the competitive landscape, profiling key market players and their strategic initiatives, including technological advancements and market expansion efforts. Special attention is given to the impact of emerging technologies like AI and IoT on market dynamics and future growth prospects. The aim is to equip stakeholders with actionable intelligence for strategic decision-making and investment planning within this evolving market.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.85 Billion |

| Market Forecast in 2033 | USD 3.10 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Bosch Rexroth AG, Parker Hannifin Corporation, Eaton Corporation, Hydac International GmbH, Freudenberg Sealing Technologies GmbH & Co. KG, Nippon Accumulator Co. Ltd., Roth Hydraulics GmbH, Pacoma GmbH, FA Systems Co. Ltd., Tobul Accumulator, Saip S.p.A., Hannon Hydraulics, Oilgear Company, Kawasaki Heavy Industries Ltd., Weber Hydraulik GmbH |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Bladder and Diaphragm Hydraulic Accumulator Market is comprehensively segmented by type, application, end-use industry, and operating pressure to provide a granular view of market dynamics. This detailed segmentation allows for a precise understanding of which product types are gaining traction, where they are predominantly applied, and which industries are driving their demand. By analyzing these segments, stakeholders can identify niche markets, assess competitive landscapes within specific categories, and tailor their product development and marketing strategies to target high-growth areas. The differentiation between bladder and diaphragm types is crucial as each offers distinct advantages for specific operational requirements, influencing adoption rates across various applications.

Further segmentation by end-use industry highlights the diverse utility of hydraulic accumulators, ranging from heavy machinery in construction and mining to precision control in manufacturing and aerospace. The growth within these sectors directly correlates with the demand for robust and efficient hydraulic systems. The mobile equipment segment, encompassing agriculture and automotive, represents a significant portion, driven by the need for shock absorption, energy recovery, and auxiliary power in compact designs. Conversely, industrial applications, including manufacturing and oil & gas, demand high-capacity accumulators for pulsation dampening and energy storage in static systems. Understanding these distinct needs across segments is vital for strategic market positioning and product portfolio optimization.

- By Type

- Bladder Accumulator: Known for high flow rates, excellent gas-to-fluid separation, and suitability for large volumes.

- Diaphragm Accumulator: Preferred for compact designs, lower volume applications, and cost-effectiveness.

- By Application

- Mobile Equipment: Utilized in construction machinery, agricultural vehicles, and material handling for shock absorption, suspension, and energy recovery.

- Industrial Equipment: Employed in manufacturing, presses, test stands, and power generation for pulsation dampening, energy storage, and pressure compensation.

- By End-Use Industry

- Construction: Heavy machinery, excavators, cranes.

- Agriculture: Tractors, harvesters, implements.

- Oil & Gas: Drilling rigs, offshore platforms, subsea equipment.

- Manufacturing: Machine tools, presses, assembly lines.

- Mining: Earthmoving equipment, crushers.

- Automotive: Braking systems, suspension systems.

- Marine: Steering gears, deck machinery.

- Aerospace & Defense: Landing gear, flight controls.

- Others: Renewable energy, medical equipment.

- By Operating Pressure

- Low-Pressure (Up to 150 bar)

- Medium-Pressure (150-350 bar)

- High-Pressure (Above 350 bar)

Regional Highlights

- North America: This region is a mature market characterized by the adoption of advanced hydraulic technologies, driven by robust manufacturing, construction, and oil & gas sectors. The emphasis on automation and energy efficiency fuels demand for high-performance accumulators. Significant R&D investments and a strong presence of key players contribute to market stability and growth.

- Europe: A leading region in adopting green technologies and stringent environmental regulations, Europe sees strong demand for energy-efficient hydraulic accumulators. The automotive, machinery, and renewable energy industries are key contributors. Germany, Italy, and France are prominent markets, focusing on precision engineering and smart hydraulic solutions.

- Asia Pacific (APAC): This region is projected to be the fastest-growing market, primarily due to rapid industrialization, increasing infrastructure development, and a booming manufacturing sector in countries like China, India, Japan, and South Korea. The expansion of construction, agriculture, and automotive industries significantly boosts the demand for hydraulic accumulators. Government initiatives supporting manufacturing and industrial growth further propel market expansion.

- Latin America: The market in Latin America is witnessing steady growth, driven by investments in infrastructure projects, mining activities, and agricultural mechanization, particularly in Brazil and Mexico. Economic stability and industrial development efforts are expected to increase the adoption of hydraulic accumulators in the coming years.

- Middle East & Africa (MEA): This region presents emerging opportunities, primarily from the oil & gas industry, ongoing infrastructure development, and diversification efforts beyond hydrocarbons. Countries like Saudi Arabia and UAE are investing in industrial and construction projects, leading to a gradual increase in demand for hydraulic accumulators. However, market growth can be influenced by geopolitical stability and commodity price fluctuations.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Bladder and Diaphragm Hydraulic Accumulator Market.- Bosch Rexroth AG

- Parker Hannifin Corporation

- Eaton Corporation

- Hydac International GmbH

- Freudenberg Sealing Technologies GmbH & Co. KG

- Nippon Accumulator Co. Ltd.

- Roth Hydraulics GmbH

- Pacoma GmbH

- FA Systems Co. Ltd.

- Tobul Accumulator

- Saip S.p.A.

- Hannon Hydraulics

- Oilgear Company

- Kawasaki Heavy Industries Ltd.

- Weber Hydraulik GmbH

- Epe Italiana S.p.A.

- Brevini Fluid Power S.p.A.

- Olaer (a Parker Hannifin brand)

- Fox S.p.A.

- Accumulators, Inc.

Frequently Asked Questions

What is a bladder hydraulic accumulator?

A bladder hydraulic accumulator is a device designed to store energy in the form of pressurized fluid. It consists of a fluid port, a gas section, and a flexible bladder that separates the fluid from a pre-charged gas (usually nitrogen). When fluid enters the accumulator, it compresses the gas in the bladder, storing energy. When system pressure drops, the compressed gas expands, forcing fluid back into the system. Bladder accumulators are known for high flow rates and efficient fluid separation.

How do diaphragm hydraulic accumulators differ from bladder accumulators?

Diaphragm hydraulic accumulators also store energy using a pre-charged gas separated from hydraulic fluid, but they use a flexible diaphragm instead of a bladder. Diaphragm accumulators are typically more compact and suitable for smaller fluid volumes and applications where space is a constraint. While bladder accumulators can handle higher flow rates and larger volumes, diaphragm types are often more cost-effective for lower capacity needs and offer reliable performance in shock absorption and pulsation dampening.

What are the primary applications of hydraulic accumulators?

Hydraulic accumulators serve several critical functions across various applications. Their primary uses include energy storage for intermittent demands, pulsation dampening to reduce pressure spikes and noise, shock absorption to mitigate hydraulic hammer, and emergency power supply in case of pump failure. They are extensively used in mobile equipment (e.g., construction, agriculture), industrial machinery (e.g., presses, machine tools), and specialized sectors like oil & gas, marine, and aerospace.

What factors drive the growth of the bladder and diaphragm hydraulic accumulator market?

Key drivers include the increasing demand for energy-efficient hydraulic systems, the global expansion of industrial automation and mechanization, and significant growth in the construction and infrastructure sectors. Additionally, technological advancements leading to compact, high-performance, and smart accumulators with integrated IoT capabilities are fueling market expansion. The rising adoption in renewable energy applications, particularly wind turbines, also contributes significantly to market growth.

How does AI impact the future of hydraulic accumulators?

AI is set to transform hydraulic accumulators by enabling advanced predictive maintenance, optimizing performance, and facilitating anomaly detection. AI algorithms can analyze real-time sensor data from accumulators to anticipate failures, adjust operational parameters for peak efficiency, and quickly diagnose issues. This integration will lead to smarter, more reliable, and cost-effective hydraulic systems, minimizing downtime and extending the operational lifespan of equipment.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted