Bioga and Biomethane Market

Bioga and Biomethane Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701368 | Last Updated : July 29, 2025 |

Format : ![]()

![]()

![]()

![]()

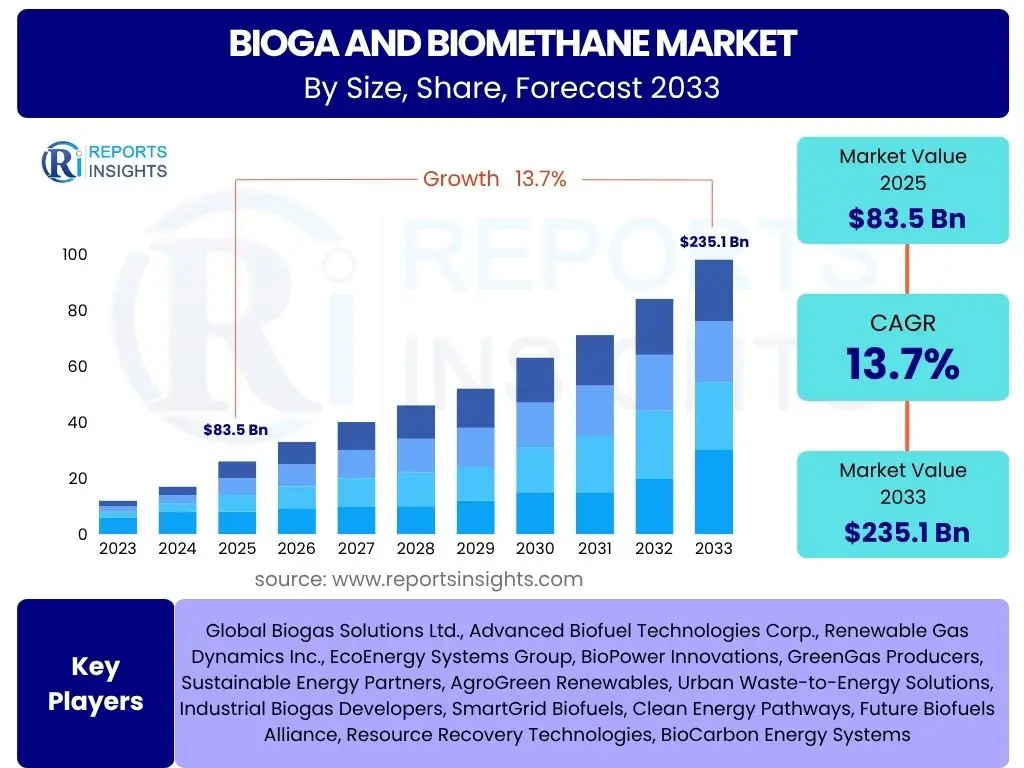

Bioga and Biomethane Market Size

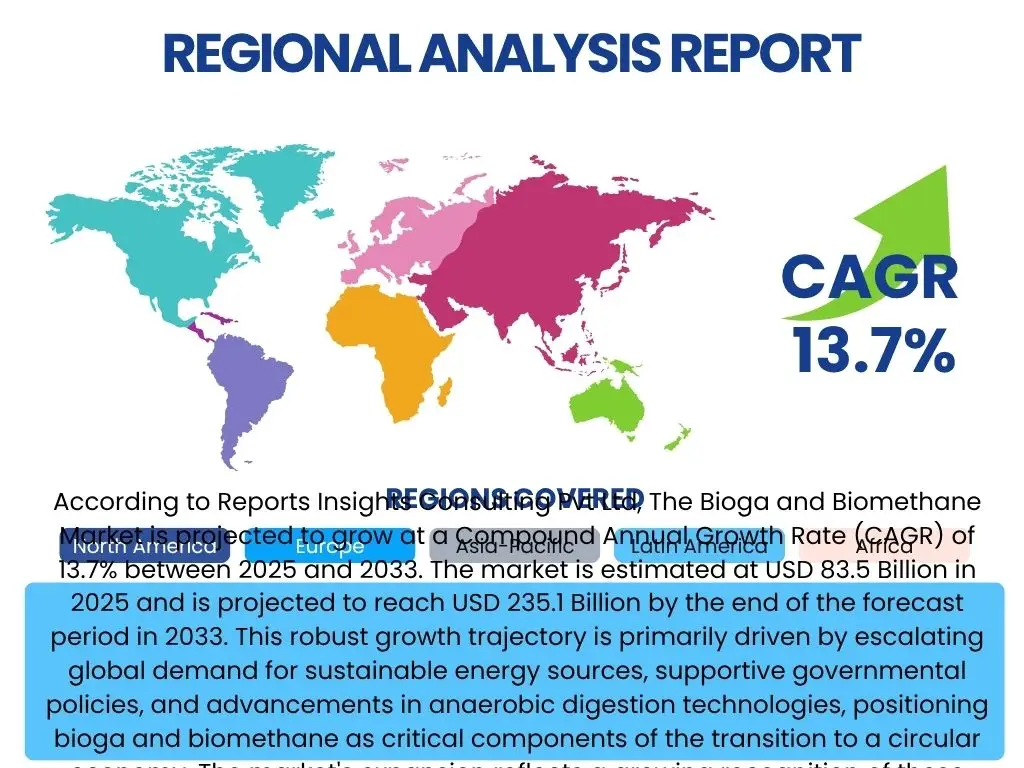

According to Reports Insights Consulting Pvt Ltd, The Bioga and Biomethane Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 13.7% between 2025 and 2033. The market is estimated at USD 83.5 Billion in 2025 and is projected to reach USD 235.1 Billion by the end of the forecast period in 2033. This robust growth trajectory is primarily driven by escalating global demand for sustainable energy sources, supportive governmental policies, and advancements in anaerobic digestion technologies, positioning bioga and biomethane as critical components of the transition to a circular economy. The market's expansion reflects a growing recognition of these biofuels' multifaceted benefits, including waste management, reduction of greenhouse gas emissions, and enhancement of energy independence.

Key Bioga and Biomethane Market Trends & Insights

User inquiries concerning the Bioga and Biomethane market frequently highlight the evolving landscape shaped by environmental concerns, technological advancements, and shifting energy policies. Common questions explore the adoption rate of these biofuels, their integration into existing energy infrastructures, and the role of innovation in optimizing production processes. There is significant interest in understanding how various regions are incentivizing and supporting the deployment of bioga and biomethane projects, as well as the emerging applications beyond traditional power generation. The focus remains on scalability, cost-effectiveness, and the overall environmental footprint of these renewable energy solutions.

A prominent trend in the market is the increasing sophistication of feedstock diversification. While agricultural waste and municipal solid waste remain primary inputs, there is a growing interest in utilizing industrial wastewater, food processing residues, and even algal biomass to produce bioga. This diversification helps mitigate feedstock supply volatility and enhances the economic viability of projects by tapping into readily available, often problematic, waste streams. Furthermore, the development of advanced pre-treatment technologies and digester designs is improving conversion efficiencies, making the overall production process more robust and economically attractive for a wider range of organic materials.

Another significant insight revolves around the rising demand for biomethane as a transport fuel and for injection into natural gas grids. This shift from simple bioga combustion for electricity generation to higher-value biomethane applications reflects a maturation of the market and increasing recognition of biomethane's versatility. Regulatory frameworks and incentive programs, particularly in Europe and North America, are increasingly favoring grid injection and vehicle fuel use, offering premium prices and stimulating investment in upgrading technologies. This trend is pivotal for decarbonizing the transport sector and leveraging existing gas infrastructure for renewable energy distribution.

- Policy and regulatory support: Growing government incentives, subsidies, and mandates for renewable energy integration and waste management drive market expansion.

- Technological advancements in anaerobic digestion: Innovations in digester design, pre-treatment methods, and gas upgrading technologies enhance efficiency and reduce production costs.

- Increased demand for renewable natural gas (RNG): Biomethane is gaining traction as a direct substitute for fossil natural gas in various applications, including transportation and grid injection.

- Circular economy integration: Bioga and biomethane production contributes to waste reduction, nutrient recycling, and greenhouse gas emission mitigation, aligning with circular economy principles.

- Diversification of feedstocks: Utilization of a broader range of organic waste materials, including industrial residues, agricultural waste, and municipal solid waste, ensures feedstock security and reduces dependence on single sources.

- Decentralized energy production: Small-to-medium scale bioga plants are increasingly deployed at farms and industrial sites, fostering local energy independence and waste valorization.

- Synergies with hydrogen economy: Research and development into integrating biomethane production with green hydrogen initiatives, such as through steam methane reforming of biomethane, are emerging trends.

- Carbon capture and utilization (CCU): Interest in capturing CO2 from bioga upgrading processes for various industrial applications or storage, enhancing the net climate benefits.

AI Impact Analysis on Bioga and Biomethane

Common user questions regarding AI's impact on the Bioga and Biomethane sector often center on its potential to optimize complex biological and engineering processes, enhance operational efficiency, and provide predictive insights for better resource management. Users are keen to understand how AI can address challenges related to feedstock variability, digester stability, and gas quality control, which are critical for maximizing output and ensuring economic viability. The overarching expectation is that AI will usher in a new era of precision, automation, and data-driven decision-making within the bioga and biomethane value chain, transforming traditional operational models into more intelligent and resilient systems.

AI's influence is anticipated to be particularly transformative in feedstock management and process optimization. Machine learning algorithms can analyze vast datasets concerning feedstock composition, seasonal availability, and pre-treatment requirements to predict optimal blending ratios, thereby ensuring stable and efficient digester performance. Furthermore, AI-powered systems can monitor real-time operational parameters such as temperature, pH levels, and volatile fatty acid concentrations within anaerobic digesters, identifying anomalies and predicting potential issues before they escalate. This predictive maintenance capability minimizes downtime, reduces operational costs, and significantly improves the overall reliability and output of bioga plants.

Beyond the operational aspects, AI is poised to play a crucial role in optimizing the entire value chain, from site selection and project planning to energy distribution and market integration. Advanced analytics can model the economic feasibility of new projects by integrating variables like local waste availability, energy demand, and regulatory incentives. In terms of market integration, AI can forecast energy prices and demand fluctuations, enabling plant operators to optimize gas production and injection schedules for maximum revenue. This holistic application of AI promises to unlock new efficiencies, enhance profitability, and accelerate the widespread adoption of bioga and biomethane technologies.

- Predictive Maintenance: AI algorithms analyze sensor data from digesters and upgrading equipment to predict potential failures, reducing downtime and maintenance costs.

- Process Optimization: Machine learning models optimize operating parameters (temperature, pH, hydraulic retention time) to maximize bioga yield and quality.

- Feedstock Management: AI assists in analyzing feedstock composition and predicting optimal blending ratios for consistent and efficient anaerobic digestion.

- Supply Chain Logistics: AI-driven solutions optimize the collection and transport of organic waste, reducing logistical costs and improving feedstock availability.

- Energy Market Integration: AI tools forecast energy prices and demand, enabling smart dispatch of biomethane into the grid or for direct use, maximizing revenue.

- Quality Control and Assurance: AI-powered sensors and analytics ensure consistent gas quality for grid injection or vehicle fuel applications, meeting stringent standards.

- Remote Monitoring and Control: AI facilitates real-time monitoring and automated adjustments of plant operations, enhancing efficiency and reducing manual intervention.

- Resource Efficiency: AI identifies opportunities for water and nutrient recovery from digestate, promoting a more circular and sustainable operation.

Key Takeaways Bioga and Biomethane Market Size & Forecast

User queries regarding the key takeaways from the Bioga and Biomethane market size and forecast consistently seek succinct summaries of the market's growth potential, primary drivers, and the critical factors influencing its future trajectory. There is a strong interest in understanding the most impactful trends that will shape investment decisions and policy frameworks. Essentially, users want to distill the complex market analysis into actionable insights that highlight where the most significant opportunities lie and what challenges need to be strategically addressed for sustainable expansion. The demand is for clarity on the market's fundamental strengths and its long-term viability as a renewable energy solution.

A primary takeaway is the undeniable and robust growth trajectory of the market, driven by an urgent global need for decarbonization and enhanced energy security. The significant projected CAGR indicates that bioga and biomethane are not merely niche solutions but are emerging as mainstream components of the diversified energy mix. This growth is underpinned by continuous innovation in production technologies, enabling greater efficiency and cost-effectiveness, which in turn makes these biofuels increasingly competitive with traditional fossil fuels. The expanding recognition of their environmental benefits, including methane emission reduction and waste valorization, further solidifies their market position.

Another crucial insight is the increasing strategic importance of biomethane for grid injection and transportation fuel applications. This evolution signifies a move towards higher-value utilization, unlocking greater revenue streams and providing a more direct pathway for decarbonizing hard-to-abate sectors. The market's future will largely be shaped by the continued development of supportive regulatory frameworks, the availability of sustainable feedstock, and the effective integration of advanced digital technologies like AI. Addressing the challenges of high capital expenditure and infrastructure limitations will be paramount for fully realizing the market's extensive potential and ensuring its pivotal role in the global energy transition.

- Accelerated Growth: The Bioga and Biomethane market is poised for substantial growth through 2033, driven by sustainability mandates and energy independence goals.

- Policy Driven Expansion: Favorable government policies, incentives, and renewable energy targets are primary catalysts for market development.

- Focus on Biomethane: Increasing emphasis on upgrading bioga to biomethane for grid injection and vehicular fuel represents a key value proposition and growth area.

- Waste-to-Energy Solution: The market plays a crucial role in sustainable waste management, transforming organic waste into valuable energy resources.

- Technological Innovations: Continuous improvements in anaerobic digestion and gas upgrading technologies are enhancing efficiency and reducing costs.

- Global Market Penetration: While Europe leads, North America and Asia Pacific are emerging as significant growth regions with substantial untapped potential.

- Diversified Applications: Beyond power generation, applications in heating, industrial processes, and transport are diversifying revenue streams and market opportunities.

- Investment Attractiveness: The predictable revenue streams and environmental benefits make the market increasingly attractive for private and public investments.

Bioga and Biomethane Market Drivers Analysis

The Bioga and Biomethane market is propelled by a confluence of powerful drivers stemming from environmental imperatives, economic advantages, and strategic energy policies. A paramount driver is the global commitment to reducing greenhouse gas emissions and combating climate change, with bioga and biomethane offering a viable pathway to decarbonize the energy and waste sectors. The increasing volume of organic waste generated worldwide, coupled with the need for sustainable waste management solutions, naturally positions bioga production as an attractive and environmentally responsible option. These factors collectively create a robust demand for renewable gas, fostering market expansion and investment.

Governmental support and regulatory frameworks play a pivotal role in accelerating market growth. Policies such as feed-in tariffs, renewable energy mandates, tax incentives, and carbon credit schemes significantly improve the economic viability of bioga and biomethane projects, attracting both domestic and international investments. Moreover, the emphasis on energy security and diversification of energy sources, particularly in regions dependent on imported fossil fuels, provides a strategic impetus for developing indigenous renewable gas production capabilities. This drive for energy independence reinforces the market's long-term growth prospects.

Technological advancements in anaerobic digestion and gas upgrading processes are further amplifying market drivers. Innovations leading to improved efficiency, reduced operational costs, and enhanced gas quality make bioga and biomethane more competitive and adaptable for various applications, including grid injection and vehicular fuel. The growing recognition of biomethane as a drop-in replacement for fossil natural gas, capable of utilizing existing infrastructure, significantly reduces barriers to adoption. This combination of policy support, environmental benefits, and technological progress creates a strong foundation for sustained market expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Renewable Energy & GHG Emission Reduction Targets | +2.5% | Global, particularly EU, North America, China, India | Mid-to-Long Term (2025-2033) |

| Supportive Government Policies & Incentives (Feed-in Tariffs, Subsidies) | +2.0% | Europe, North America, Japan, South Korea | Mid Term (2025-2029) |

| Growing Focus on Sustainable Waste Management & Circular Economy Principles | +1.8% | Global, particularly urbanized regions | Mid-to-Long Term (2025-2033) |

| Advancements in Anaerobic Digestion & Gas Upgrading Technologies | +1.5% | Global | Short-to-Mid Term (2025-2028) |

| Rising Energy Security Concerns & Diversification of Energy Mix | +1.2% | Europe, Asia Pacific (import-dependent nations) | Mid-to-Long Term (2025-2033) |

Bioga and Biomethane Market Restraints Analysis

Despite the significant growth potential, the Bioga and Biomethane market faces several notable restraints that could impede its accelerated expansion. A primary concern is the relatively high upfront capital expenditure required for establishing bioga production facilities and upgrading plants. This substantial initial investment can be a deterrent for new entrants and smaller developers, particularly when compared to the perceived lower initial costs of conventional energy projects. The financial hurdle often necessitates robust financial incentives and long-term policy certainty to de-risk investments and attract sufficient capital, which is not consistently available across all regions.

Another significant restraint involves the challenges associated with feedstock availability, consistency, and quality. While organic waste streams are abundant, their collection, transportation, and pre-treatment can be logistically complex and costly. The variability in feedstock composition directly impacts the efficiency and stability of anaerobic digestion processes, potentially leading to inconsistent bioga yields and quality. Additionally, competition for specific feedstocks from other industries, such as composting or animal feed production, can drive up input costs and affect the economic viability of bioga projects, particularly in densely populated or agriculturally intensive areas.

Furthermore, regulatory complexities and grid integration challenges pose considerable hurdles. The diverse and often evolving regulatory frameworks across different jurisdictions can create uncertainty for project developers, making it difficult to plan and execute projects efficiently. Integrating biomethane into existing natural gas grids requires adherence to stringent quality standards, which necessitates advanced upgrading technologies and specialized infrastructure. The capacity of existing gas grids to accommodate increasing volumes of biomethane, along with associated connection charges and bureaucratic procedures, can limit the pace of market penetration and expansion, especially in less developed regions.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Expenditure (CAPEX) for Plant Setup & Upgrading | -1.5% | Global, particularly developing economies | Mid-to-Long Term (2025-2033) |

| Feedstock Availability, Consistency, & Quality Challenges | -1.0% | Regional, depending on waste generation & agriculture patterns | Mid-to-Long Term (2025-2033) |

| Complex Regulatory Frameworks & Permitting Procedures | -0.8% | Country-specific, varying by legal systems | Short-to-Mid Term (2025-2028) |

| Competition from Alternative Renewable Energy Technologies (e.g., Solar, Wind) | -0.7% | Global | Mid-to-Long Term (2025-2033) |

| Public Perception & Not-In-My-Backyard (NIMBY) Syndrome | -0.5% | Localized, especially in densely populated areas | Short-to-Mid Term (2025-2028) |

Bioga and Biomethane Market Opportunities Analysis

The Bioga and Biomethane market presents numerous compelling opportunities for growth, driven by an evolving energy landscape and increasing environmental consciousness. A significant opportunity lies in the expansion of biomethane utilization in the transportation sector, particularly for heavy-duty vehicles and public transport fleets. As policies push for decarbonization of transport, biomethane offers a readily available and economically viable alternative to fossil fuels, leveraging existing natural gas vehicle infrastructure. This application not only reduces emissions but also contributes to improved urban air quality, creating a strong market pull for purified biomethane.

Another substantial opportunity resides in the broader integration of bioga and biomethane into industrial processes and the existing natural gas grid. Industries seeking to reduce their carbon footprint are increasingly exploring biomethane as a direct replacement for fossil natural gas in heating and process applications. Furthermore, the capacity for biomethane injection into gas grids allows for the decarbonization of residential and commercial heating, offering a robust and dispatchable renewable energy source that complements intermittent renewables like wind and solar. This grid integration enhances energy system flexibility and stability, unlocking new revenue streams for producers.

Technological advancements and the exploration of novel feedstocks also represent significant growth avenues. Innovations in dry anaerobic digestion, co-digestion techniques, and more efficient gas upgrading technologies are expanding the range of treatable organic waste streams and improving overall energy recovery. The potential for integrating bioga production with carbon capture and utilization (CCU) technologies, as well as exploring pathways for bioga-derived hydrogen production, further broadens the market's scope and enhances its long-term sustainability profile. These emerging opportunities underscore the versatility and evolving role of bioga and biomethane in the future energy economy.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion of Biomethane Use in Transportation Sector (RNG Vehicles) | +2.0% | North America, Europe, China | Mid-to-Long Term (2025-2033) |

| Increasing Demand for Biomethane Grid Injection & Industrial Heating | +1.8% | Europe, North America, Japan | Mid-to-Long Term (2025-2033) |

| Development of Novel Feedstocks & Advanced Pre-treatment Technologies | +1.5% | Global | Short-to-Mid Term (2025-2028) |

| Integration with Carbon Capture & Utilization (CCU) Technologies | +1.2% | Europe, North America | Long Term (2029-2033) |

| Decentralized Bioga Plants for On-Site Energy Production & Waste Management | +1.0% | Developing Economies, Rural Areas | Mid-to-Long Term (2025-2033) |

Bioga and Biomethane Market Challenges Impact Analysis

The Bioga and Biomethane market, despite its promising outlook, faces several significant challenges that require strategic solutions for sustained growth. A major hurdle is the substantial initial capital investment required for constructing and commissioning bioga plants, particularly those equipped with advanced biomethane upgrading technologies. This high CAPEX can be a barrier for smaller developers and can deter investment in regions with less supportive financial mechanisms or perceived higher investment risks. Overcoming this challenge necessitates innovative financing models, government guarantees, and clearer, long-term policy signals to de-risk projects and attract a broader range of investors.

Another critical challenge revolves around the complex and often fragmented regulatory landscape across different countries and regions. Varied permitting requirements, differing grid injection standards, and inconsistent support schemes create uncertainties for project developers, leading to delays and increased development costs. Achieving greater regulatory harmonization and establishing streamlined permitting processes are essential for accelerating project deployment and fostering cross-border investments. Additionally, ensuring a stable and predictable policy environment, which includes long-term incentives, is crucial for building investor confidence and fostering market maturity.

Furthermore, technical challenges related to optimizing anaerobic digestion processes for diverse feedstocks and ensuring consistent, high-quality biomethane production persist. Managing feedstock variability, preventing process instability, and efficiently removing impurities from raw bioga require continuous research and development. The cost-effectiveness of biomethane compared to conventional natural gas, particularly in periods of low fossil fuel prices, also remains a challenge. Addressing these technical and economic hurdles through innovation, economies of scale, and targeted policy interventions is vital for enhancing the competitiveness and widespread adoption of bioga and biomethane.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Upfront Investment & Project Financing Difficulties | -1.3% | Global, particularly emerging markets | Mid-to-Long Term (2025-2033) |

| Lack of Standardized Policies & Regulatory Frameworks Across Regions | -1.0% | Global, especially between different economic blocs | Short-to-Mid Term (2025-2028) |

| Infrastructure Limitations for Biomethane Grid Injection & Distribution | -0.9% | Country-specific, varying by grid maturity | Mid-to-Long Term (2025-2033) |

| Feedstock Competition & Logistics Management | -0.8% | Localized, depending on waste generation & other industries | Short-to-Mid Term (2025-2028) |

| Public Acceptance & Social Barriers to Plant Siting | -0.6% | Localized, urban areas | Short-to-Mid Term (2025-2028) |

Bioga and Biomethane Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Bioga and Biomethane market, offering insights into its current size, historical performance, and future growth projections. It delineates key trends, opportunities, drivers, and restraints influencing market dynamics, along with a detailed impact analysis of artificial intelligence. The report meticulously segments the market by feedstock, application, and production method, providing a granular view of various sub-sectors. Regional analyses offer crucial perspectives on market development across major geographies, highlighting key country-level contributions. Furthermore, the report profiles leading market players, offering a competitive landscape overview crucial for strategic decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 83.5 Billion |

| Market Forecast in 2033 | USD 235.1 Billion |

| Growth Rate | 13.7% |

| Number of Pages | 265 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Biogas Solutions Ltd., Advanced Biofuel Technologies Corp., Renewable Gas Dynamics Inc., EcoEnergy Systems Group, BioPower Innovations, GreenGas Producers, Sustainable Energy Partners, AgroGreen Renewables, Urban Waste-to-Energy Solutions, Industrial Biogas Developers, SmartGrid Biofuels, Clean Energy Pathways, Future Biofuels Alliance, Resource Recovery Technologies, BioCarbon Energy Systems |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Bioga and Biomethane market is comprehensively segmented to provide a detailed understanding of its diverse components and their respective growth drivers. These segmentations are crucial for identifying specific market niches, understanding consumer preferences, and pinpointing investment opportunities across the value chain. The primary classifications typically revolve around the type of feedstock utilized, the end-use application of the produced bioga or biomethane, and the specific production method employed. Each segment exhibits unique characteristics, technological requirements, and market dynamics, contributing distinctly to the overall market landscape.

The segmentation by feedstock highlights the diverse origins of organic matter used for bioga production, ranging from agricultural residues and animal manure to municipal solid waste and industrial effluents. Understanding the prevalence and availability of these different feedstocks is essential for regional market analysis and for developing scalable and sustainable projects. Similarly, segmenting by application elucidates the various end-uses of bioga and biomethane, from traditional power generation and heating to more advanced applications like vehicle fuel and grid injection. This application-based view helps in assessing the market's contribution to decarbonizing different sectors of the economy.

Furthermore, the market is segmented by production method, primarily distinguishing between anaerobic digestion and gasification processes. Anaerobic digestion is the most common method for bioga production from wet organic waste, while gasification is increasingly explored for dryer, solid biomass. Analyzing these methodologies helps in understanding technological preferences, efficiency rates, and the suitability of each process for different types of feedstock and scales of operation. This multi-faceted segmentation provides a robust framework for assessing the market's current structure and forecasting its future evolution.

- By Feedstock

- Agricultural Waste (e.g., crop residues, manure)

- Industrial Waste (e.g., food processing waste, wastewater sludge)

- Municipal Solid Waste (MSW)

- Energy Crops (e.g., maize silage, grass silage)

- Animal Manure

- Others (e.g., sewage sludge, algal biomass)

- By Application

- Power Generation (Electricity)

- Vehicular Fuel (Bio-CNG, Bio-LNG)

- Heating (Industrial, Residential, Commercial)

- Industrial Use (Process heat, chemical feedstock)

- Grid Injection (Natural Gas Grid)

- By Production Method

- Anaerobic Digestion (Wet, Dry, Co-digestion)

- Gasification (Thermo-chemical conversion)

Regional Highlights

The Bioga and Biomethane market exhibits significant regional variations, influenced by differing regulatory environments, feedstock availability, energy demands, and technological adoption rates. Europe currently leads the market, driven by robust policy support, mature waste management infrastructure, and ambitious renewable energy targets. Countries like Germany, France, Italy, and the Nordic nations have established extensive bioga and biomethane production capacities, with a strong emphasis on grid injection and sustainable waste management practices. The region's experience in developing sophisticated incentive schemes and advanced technologies positions it as a benchmark for other global markets.

North America, particularly the United States and Canada, represents a rapidly growing market, propelled by increasing awareness of methane emissions, supportive federal and state-level incentives (e.g., Renewable Fuel Standard in the U.S.), and abundant agricultural and landfill waste. The focus in this region is significantly shifting towards the production of renewable natural gas (RNG) for the transportation sector and pipeline injection, leveraging the extensive natural gas pipeline infrastructure. Latin America is an emerging market with substantial potential, largely due to its vast agricultural resources and growing need for sustainable waste treatment solutions, though investment and regulatory frameworks are still developing.

Asia Pacific is projected to be one of the fastest-growing regions, with China and India at the forefront. Rapid urbanization, increasing waste generation, and escalating energy demand are key drivers. Both countries are implementing policies to promote bioga production for rural energy access, waste management, and industrial applications. While the market in APAC is still in its nascent stages compared to Europe, the sheer scale of waste generated and the government's commitment to renewable energy present enormous long-term opportunities. The Middle East and Africa (MEA) region, while having significant untapped potential, faces challenges related to infrastructure development and consistent policy support, but opportunities exist in specific countries with strong agricultural bases or waste management needs.

- Europe: Dominant market due to strong government support (feed-in tariffs, quotas), established waste management infrastructure, and high environmental awareness. Emphasis on grid injection and transport fuel.

- North America: Rapidly growing market, primarily driven by the production of Renewable Natural Gas (RNG) from agricultural waste and landfills for transportation and pipeline injection, supported by federal and state incentives.

- Asia Pacific (APAC): Emerging as a high-growth region, especially China and India, propelled by increasing waste generation, energy demand, and governmental initiatives to promote rural energy and waste treatment.

- Latin America: Significant untapped potential due to abundant agricultural biomass and rising waste volumes; however, market development is contingent on establishing robust policy frameworks and attracting investment.

- Middle East and Africa (MEA): Nascent market with opportunities in countries focused on sustainable development and waste-to-energy solutions, though scalability faces infrastructure and policy challenges.

- Germany: Pioneer in bioga production with extensive plant numbers and high utilization rates for power and heat.

- France: Strong growth in biomethane production for grid injection, supported by favorable tariffs and national energy plans.

- United States: Leading the development of RNG for transport, driven by federal incentives and corporate sustainability goals.

- China: Massive potential with a focus on large-scale bioga projects for rural energy and waste treatment, aiming for energy self-sufficiency.

- India: Significant focus on decentralized bioga plants for rural households and community energy, addressing cooking fuel and waste issues.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Bioga and Biomethane Market.- Global Biogas Solutions Ltd.

- Advanced Biofuel Technologies Corp.

- Renewable Gas Dynamics Inc.

- EcoEnergy Systems Group

- BioPower Innovations

- GreenGas Producers

- Sustainable Energy Partners

- AgroGreen Renewables

- Urban Waste-to-Energy Solutions

- Industrial Biogas Developers

- SmartGrid Biofuels

- Clean Energy Pathways

- Future Biofuels Alliance

- Resource Recovery Technologies

- BioCarbon Energy Systems

- EnviroGas Production Co.

- TerraBio Energy Group

- Global Renewable Fuels

- SynTech Biogas Ltd.

- PowerGen Biofuels Inc.

Frequently Asked Questions

Analyze common user questions about the Bioga and Biomethane market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is bioga and biomethane, and how are they produced?

Bioga is a renewable gas produced from the anaerobic digestion of organic matter (e.g., agricultural waste, municipal solid waste) in the absence of oxygen. It primarily consists of methane (CH4) and carbon dioxide (CO2). Biomethane is purified bioga, where carbon dioxide and other impurities are removed, resulting in a gas with properties similar to conventional natural gas, suitable for grid injection or use as vehicle fuel.

Why are bioga and biomethane considered important for the future energy mix?

Bioga and biomethane are crucial for the future energy mix because they offer a sustainable pathway for waste management, reduce greenhouse gas emissions by capturing methane, and provide a reliable, dispatchable renewable energy source. They enhance energy security by diversifying supply and can utilize existing gas infrastructure, facilitating the decarbonization of hard-to-abate sectors like heavy transport and industrial heating.

What are the primary applications of bioga and biomethane?

Bioga is primarily used for generating electricity and heat through combustion in combined heat and power (CHP) plants. Biomethane, after upgrading, has higher-value applications: it can be injected into natural gas grids, used as a direct substitute for natural gas in industrial and residential heating, or compressed/liquefied for use as a renewable fuel for vehicles (Bio-CNG, Bio-LNG).

What are the main challenges hindering the growth of the bioga and biomethane market?

Key challenges include high initial capital expenditures for plant construction and upgrading, ensuring consistent and cost-effective feedstock supply, and navigating complex and often inconsistent regulatory frameworks across different regions. Additionally, public perception issues and the need for significant infrastructure development for biomethane distribution can impede market expansion.

How do government policies and incentives impact the bioga and biomethane market?

Government policies and incentives, such as feed-in tariffs, tax credits, renewable energy mandates, and carbon pricing mechanisms, are critical drivers for the bioga and biomethane market. They improve the economic viability of projects, de-risk investments for developers, and accelerate the adoption of these renewable fuels by making them competitive with fossil fuels and supporting necessary infrastructure development.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted