Barrier Film Market

Barrier Film Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706712 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

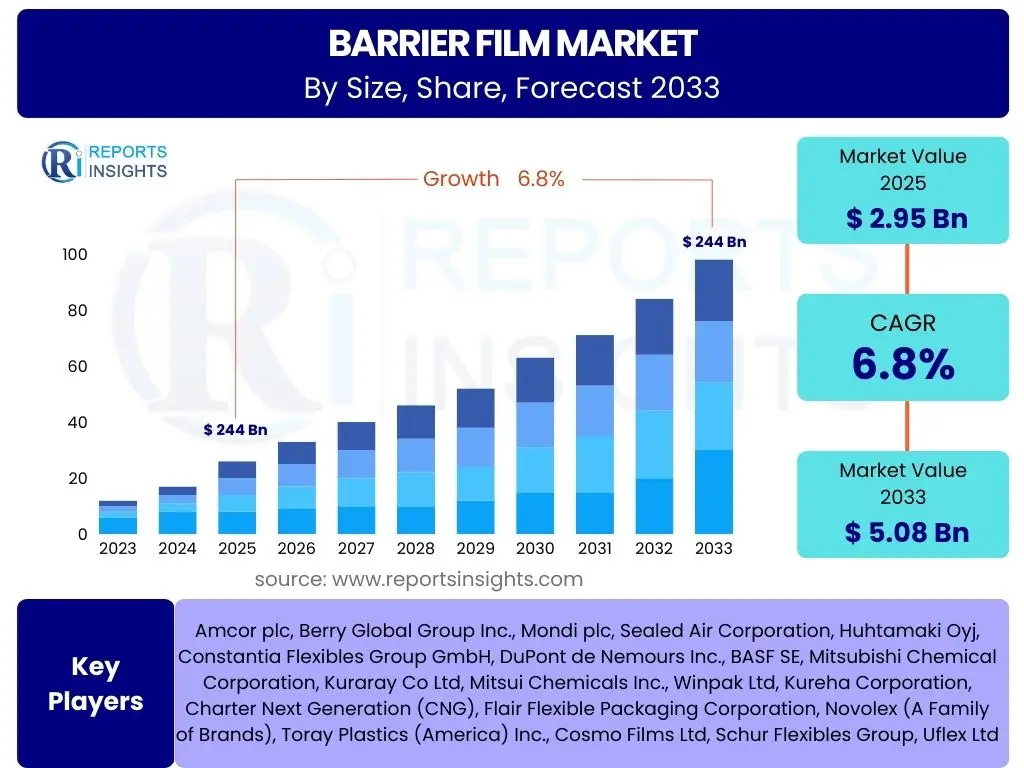

Barrier Film Market Size

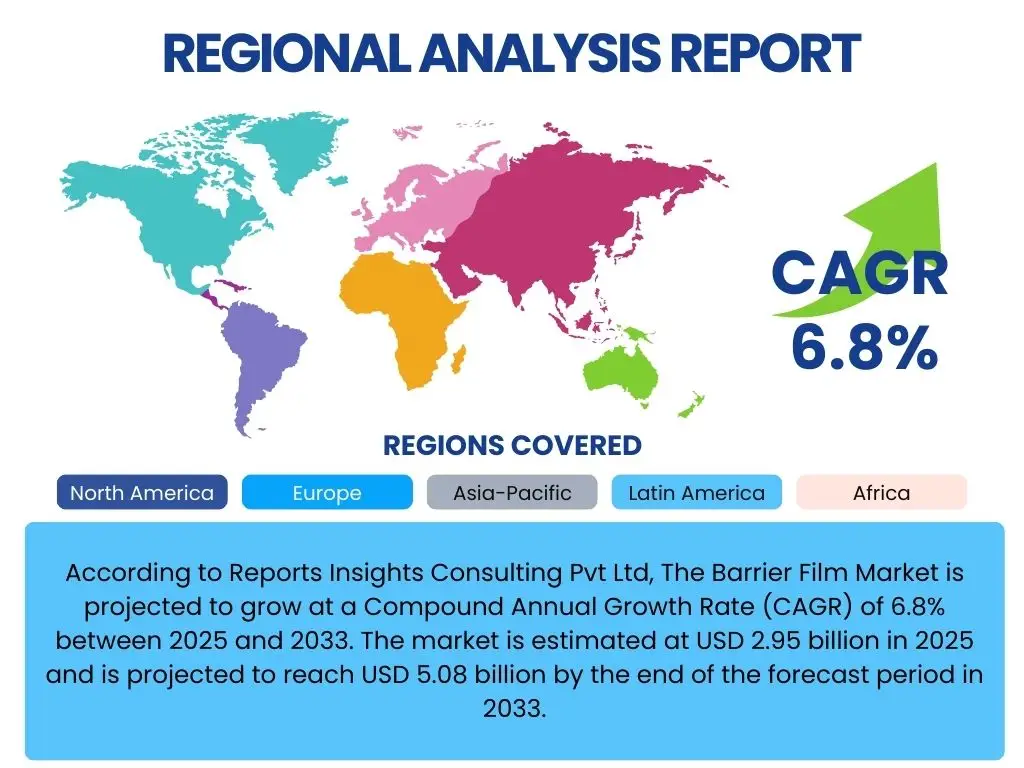

According to Reports Insights Consulting Pvt Ltd, The Barrier Film Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 2.95 billion in 2025 and is projected to reach USD 5.08 billion by the end of the forecast period in 2033.

Key Barrier Film Market Trends & Insights

The barrier film market is experiencing significant transformation driven by evolving consumer demands, stringent regulatory landscapes, and advancements in material science. Key trends revolve around the increasing adoption of sustainable packaging solutions, the demand for extended shelf life in various product categories, and the integration of advanced barrier technologies. Industries such as food and beverage, pharmaceuticals, and personal care are at the forefront of this evolution, continuously seeking innovative film solutions that offer superior protection, improved aesthetics, and reduced environmental impact.

Furthermore, the rapid expansion of e-commerce platforms is necessitating robust and protective packaging, boosting the demand for high-performance barrier films capable of withstanding diverse shipping conditions while maintaining product integrity. The market is also witnessing a push towards circular economy principles, prompting manufacturers to invest in research and development for films that are not only effective barriers but also recyclable, biodegradable, or compostable. This shift is reshaping supply chains and product development strategies across the barrier film industry.

- Growing demand for sustainable and eco-friendly barrier solutions, including recyclable, biodegradable, and compostable films.

- Increased adoption of high-performance barrier films for extended shelf life, particularly in the food and beverage and pharmaceutical sectors.

- Integration of advanced material technologies, such as nanomaterials and bio-based polymers, to enhance barrier properties.

- Rapid expansion of e-commerce driving the need for durable and protective packaging solutions.

- Rise in consumption of packaged and convenience foods globally, fueling demand for flexible barrier packaging.

- Focus on lightweighting and source reduction in packaging to minimize material usage and transportation costs.

- Development of smart and active packaging incorporating barrier layers for enhanced product monitoring and preservation.

AI Impact Analysis on Barrier Film

Artificial intelligence (AI) is poised to significantly transform various facets of the barrier film industry, from manufacturing processes to supply chain management and product development. Users frequently inquire about how AI can optimize production efficiency, enhance quality control, and facilitate the design of novel film formulations. The technology is expected to introduce unprecedented levels of precision and automation, addressing long-standing challenges related to material consistency and defect detection.

Furthermore, AI algorithms can analyze vast datasets to predict material performance under different conditions, optimize blending ratios for multi-layer films, and even forecast market demand with greater accuracy. This predictive capability can lead to reduced waste, optimized inventory levels, and more responsive supply chains. The integration of AI also holds the potential to accelerate the development cycle for new barrier film products, allowing companies to bring innovative and sustainable solutions to market faster, thereby gaining a competitive edge.

- Enhanced quality control through AI-driven visual inspection systems, detecting microscopic defects in real-time.

- Optimization of manufacturing processes by AI algorithms adjusting parameters for maximum efficiency and reduced waste.

- Predictive maintenance for production machinery, minimizing downtime and improving operational reliability.

- Supply chain optimization through AI-powered demand forecasting and inventory management, leading to greater efficiency and cost savings.

- Accelerated research and development of new barrier film formulations using AI for material property prediction and simulation.

- Improved energy efficiency in production facilities via AI-based energy management systems.

- Development of personalized or customized barrier film solutions based on AI analysis of specific product requirements.

Key Takeaways Barrier Film Market Size & Forecast

The barrier film market is set for robust expansion through 2033, primarily propelled by the escalating demand for high-performance packaging across diverse end-use industries. A significant takeaway is the dual emphasis on functionality and sustainability, with market players increasingly investing in recyclable, compostable, and bio-based barrier solutions to meet evolving regulatory standards and consumer preferences. The food and beverage sector remains a dominant application area, driven by global population growth and the rising consumption of processed and packaged foods, necessitating films that extend shelf life and maintain product freshness.

Moreover, the pharmaceutical and healthcare sectors are emerging as critical growth engines, with stringent requirements for product protection and integrity boosting the demand for advanced barrier films. Regional dynamics indicate strong growth in Asia Pacific, attributed to industrialization and expanding consumer markets, while North America and Europe continue to lead in technological innovation and the adoption of sustainable practices. The market's future trajectory will largely depend on advancements in material science, the cost-effectiveness of sustainable alternatives, and the industry's ability to navigate complex regulatory frameworks while delivering high-performance solutions.

- The Barrier Film Market is projected for substantial growth, driven by increasing packaging demand across industries.

- Sustainability initiatives, including the development of recyclable and biodegradable films, are crucial growth drivers.

- The Food & Beverage sector will remain the largest application segment, emphasizing extended shelf life and freshness.

- Pharmaceuticals and healthcare are rapidly growing segments due to strict barrier requirements for product integrity.

- Asia Pacific is expected to demonstrate the fastest growth due to industrial expansion and rising disposable incomes.

- Technological advancements in material science are continuously improving film properties and expanding application possibilities.

- Market participants are focusing on strategic partnerships and mergers to enhance capabilities and expand market reach.

Barrier Film Market Drivers Analysis

The barrier film market is significantly propelled by several key drivers, primarily the escalating global demand for packaged goods across diverse industries. The imperative to extend product shelf life, ensure food safety, and protect sensitive items from external contaminants such as moisture, oxygen, and light has made barrier films indispensable. This need is particularly acute in the food and beverage sector, where efficient packaging is critical for reducing spoilage and waste. The rapid expansion of e-commerce further amplifies this demand, as products require robust packaging to withstand transit and handling while maintaining their quality.

Additionally, advancements in material science and manufacturing technologies have led to the development of more sophisticated and cost-effective barrier film solutions. Innovations in multi-layer co-extrusion, coating technologies, and the incorporation of advanced polymers enable films to offer superior barrier properties at competitive prices. Furthermore, growing consumer awareness regarding product safety, coupled with increasing disposable incomes globally, especially in emerging economies, fuels the consumption of packaged food and pharmaceutical products, consequently boosting the demand for high-performance barrier films.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Packaged Food and Beverages | +1.5% | Global, particularly Asia Pacific, Latin America | 2025-2033 |

| Growth in Pharmaceutical and Healthcare Packaging | +1.2% | North America, Europe, Asia Pacific | 2025-2033 |

| Expansion of E-commerce and Online Retail | +1.0% | Global, especially North America, Asia Pacific | 2025-2030 |

| Technological Advancements in Barrier Materials and Production | +0.8% | Global | 2028-2033 |

| Focus on Extended Shelf Life and Food Waste Reduction | +0.7% | Global | 2025-2033 |

Barrier Film Market Restraints Analysis

Despite robust growth prospects, the barrier film market faces several significant restraints that could impede its expansion. One primary challenge is the volatility of raw material prices, particularly for petrochemical-derived polymers, which directly impacts production costs and profit margins for manufacturers. Fluctuations in crude oil prices and the supply chain disruptions can lead to unpredictable pricing environments, making long-term planning and investment more complex.

Another substantial restraint is the increasing stringency of environmental regulations concerning plastic waste and pollution. Many multi-layer barrier films, while effective, are challenging to recycle due to their composite nature, leading to their disposal in landfills or incineration. This regulatory pressure, particularly in developed regions like Europe and North America, is pushing manufacturers to invest heavily in costly research and development for sustainable alternatives, which may not always match the performance or cost-effectiveness of traditional films. Consumer preference for sustainable packaging also exerts pressure, potentially limiting the adoption of non-recyclable solutions. The high initial capital investment required for advanced barrier film production technologies also acts as a barrier to entry for new players and can slow down innovation for existing ones, particularly for small and medium-sized enterprises.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile Raw Material Prices | -0.9% | Global | 2025-2030 |

| Stringent Environmental Regulations and Sustainability Concerns | -1.1% | Europe, North America | 2025-2033 |

| Complexity and Cost of Recycling Multi-Layer Films | -0.8% | Global | 2025-2033 |

| Competition from Alternative Packaging Materials (e.g., Glass, Metal) | -0.5% | Global | 2025-2030 |

Barrier Film Market Opportunities Analysis

The barrier film market is poised for significant opportunities driven by the global imperative for sustainable packaging solutions and the continuous demand for enhanced product protection. The development and commercialization of advanced recyclable, biodegradable, and compostable barrier films present a major avenue for growth. As regulations tighten and consumer preferences shift towards eco-friendly products, companies that can offer high-performance sustainable alternatives will gain a substantial competitive advantage. This includes innovation in mono-material barrier films that facilitate easier recycling without compromising barrier properties, along with films derived from renewable resources.

Furthermore, the rapid economic growth and increasing urbanization in emerging economies, particularly in Asia Pacific and Latin America, are creating vast untapped markets for packaged goods, thus fueling demand for barrier films. These regions offer immense potential for market penetration and expansion. Additionally, the increasing focus on customized and intelligent packaging solutions, such as those integrating sensors for freshness monitoring or tamper evidence, opens new niches for specialized barrier films. The healthcare and pharmaceutical sectors, with their stringent requirements for sterile and protected packaging, also present sustained opportunities for high-value, specialized barrier film applications, driven by an aging global population and advancements in medical treatments.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Sustainable and Recyclable Barrier Films | +1.3% | Global, particularly Europe, North America | 2025-2033 |

| Untapped Potential in Emerging Economies | +1.0% | Asia Pacific, Latin America, Middle East & Africa | 2025-2033 |

| Innovation in Active and Smart Packaging Solutions | +0.8% | Global | 2028-2033 |

| Growing Demand for Pharmaceutical and Medical Packaging | +0.7% | Global | 2025-2033 |

| Technological Advancements in Coating and Lamination Processes | +0.6% | Global | 2025-2033 |

Barrier Film Market Challenges Impact Analysis

The barrier film market faces several formidable challenges that necessitate strategic innovation and adaptation from industry players. One significant hurdle is the inherent complexity in achieving a balance between high-performance barrier properties, cost-effectiveness, and environmental sustainability. While multi-layer films offer excellent protection, their composite nature makes them notoriously difficult to recycle, leading to increasing pressure from regulators and consumers for more eco-friendly, yet equally effective, alternatives. Developing mono-material solutions that can match the barrier capabilities of multi-layer films, particularly for sensitive applications, remains a substantial technical and financial challenge for manufacturers.

Another key challenge involves navigating the fragmented and evolving regulatory landscape surrounding packaging materials, especially concerning food contact safety and plastic waste management. Compliance with diverse regional and national regulations can be complex and costly, requiring significant investment in testing and certification. Furthermore, intense competition among existing players, coupled with the capital-intensive nature of advanced film production technologies, can limit market entry and put pressure on pricing. The rapid pace of technological change also demands continuous investment in research and development to stay competitive, particularly as new material innovations and processing techniques emerge, requiring agile responses from the industry to maintain relevance and market share.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Balancing Performance, Cost, and Sustainability Requirements | -1.0% | Global | 2025-2033 |

| Complexities of Recycling Multi-Layer Structures | -1.2% | Global, particularly Europe | 2025-2033 |

| Fragmented and Evolving Regulatory Landscape | -0.8% | Europe, North America, key national markets | 2025-2030 |

| High Initial Investment for Advanced Production Technologies | -0.6% | Global | 2025-2030 |

| Supply Chain Disruptions and Raw Material Shortages | -0.5% | Global | 2025-2027 |

Barrier Film Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Barrier Film Market, offering a detailed understanding of its current size, historical trends, and future growth projections. It covers a wide array of market dynamics, including key drivers, restraints, opportunities, and challenges influencing market trajectory. The report segments the market extensively by various material types, technologies, and applications, providing granular insights into specific market performances and growth potentials across different categories. Furthermore, it meticulously highlights regional market performances and key country-level contributions, alongside profiling leading market participants and their strategic initiatives, offering a holistic view for stakeholders seeking to navigate and capitalize on opportunities within this evolving industry.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.95 Billion |

| Market Forecast in 2033 | USD 5.08 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Amcor plc, Berry Global Group Inc., Mondi plc, Sealed Air Corporation, Huhtamaki Oyj, Constantia Flexibles Group GmbH, DuPont de Nemours Inc., BASF SE, Mitsubishi Chemical Corporation, Kuraray Co Ltd, Mitsui Chemicals Inc., Winpak Ltd, Kureha Corporation, Charter Next Generation (CNG), Flair Flexible Packaging Corporation, Novolex (A Family of Brands), Toray Plastics (America) Inc., Cosmo Films Ltd, Schur Flexibles Group, Uflex Ltd |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Barrier Film Market is comprehensively segmented to provide granular insights into its diverse components, reflecting the varied applications and technological approaches within the industry. This segmentation helps in understanding specific market dynamics, identifying high-growth areas, and strategizing effectively. The market is primarily broken down by the type of material used, which dictates the film's barrier properties and suitability for different applications. Furthermore, the segmentation by technology highlights the various manufacturing processes employed to achieve desired film characteristics, from multi-layer coextrusion to advanced coating techniques.

Applications form a crucial segmentation, illustrating where barrier films are predominantly utilized, with the food and beverage sector being the largest consumer due to its critical need for product preservation and extended shelf life. Other significant applications include pharmaceuticals, cosmetics, and industrial packaging, each with unique requirements for barrier properties. The end-use industry segmentation provides a deeper dive into the specific sectors adopting these films, offering a more nuanced view of market demand drivers and emerging opportunities across the entire value chain.

- By Material:

- Polyethylene (PE)

- Polypropylene (PP)

- Polyethylene Terephthalate (PET)

- Ethylene Vinyl Alcohol (EVOH)

- Polyvinylidene Chloride (PVDC)

- Polyamide (Nylon)

- Polyethylene Naphthalate (PEN)

- Others

- By Technology:

- Coextrusion

- Lamination

- Metallization

- Coating

- Others

- By Application:

- Food & Beverage

- Meat, Poultry, Seafood

- Dairy

- Bakery

- Confectionery

- Snacks

- Fruits & Vegetables

- Beverages

- Pharmaceuticals & Healthcare

- Cosmetics & Personal Care

- Industrial

- Agriculture

- Others

- Food & Beverage

- By End-Use Industry:

- Food Packaging

- Pharmaceutical Packaging

- Industrial Packaging

- Medical Device Packaging

- Agricultural Packaging

- Others

Regional Highlights

- North America: This region represents a mature and technologically advanced market for barrier films. It is characterized by high adoption rates of advanced packaging solutions, stringent food safety regulations, and a growing emphasis on sustainable packaging. Innovation in material science and smart packaging technologies is a key driver, alongside robust demand from the convenience food and pharmaceutical sectors. The presence of major market players and significant investment in research and development further solidifies its position.

- Europe: Europe is a leader in adopting sustainable and circular economy principles in packaging, heavily influencing the barrier film market. Stringent environmental regulations, particularly concerning plastic waste and recyclability, drive innovation towards mono-material, bio-based, and compostable barrier films. The region exhibits strong demand from the dairy, meat, and ready-meal segments, coupled with a growing focus on pharmaceutical and medical packaging due to an aging population and advanced healthcare infrastructure.

- Asia Pacific (APAC): The APAC region is projected to be the fastest-growing market for barrier films, driven by rapid urbanization, increasing disposable incomes, and the booming e-commerce sector. Countries like China, India, and Japan are experiencing a surge in demand for packaged food and beverages, pharmaceuticals, and personal care products. This growth is further supported by significant industrial expansion and increasing foreign investments in manufacturing capabilities, making it a pivotal market for future growth.

- Latin America: This region is an emerging market for barrier films, experiencing steady growth due to improving economic conditions, expanding retail infrastructure, and a rising middle-class population. The demand for packaged food products, particularly in Brazil, Mexico, and Argentina, is a key driver. While sustainability trends are gaining traction, the market remains price-sensitive, balancing cost-effectiveness with performance requirements.

- Middle East and Africa (MEA): The MEA region is witnessing gradual growth in the barrier film market, primarily driven by increasing population, urbanization, and the development of the food processing and pharmaceutical industries. Investment in infrastructure and the growth of organized retail are contributing to the rising demand for packaged goods. However, market growth is often influenced by geopolitical stability and economic diversification efforts.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Barrier Film Market.- Amcor plc

- Berry Global Group Inc.

- Mondi plc

- Sealed Air Corporation

- Huhtamaki Oyj

- Constantia Flexibles Group GmbH

- DuPont de Nemours Inc.

- BASF SE

- Mitsubishi Chemical Corporation

- Kuraray Co Ltd

- Mitsui Chemicals Inc.

- Winpak Ltd

- Kureha Corporation

- Charter Next Generation (CNG)

- Flair Flexible Packaging Corporation

- Novolex (A Family of Brands)

- Toray Plastics (America) Inc.

- Cosmo Films Ltd

- Schur Flexibles Group

- Uflex Ltd

Frequently Asked Questions

What is a barrier film and what is its primary purpose?

A barrier film is a type of packaging material specifically designed to prevent or significantly reduce the permeation of gases, moisture, aromas, and other external elements into or out of a packaged product. Its primary purpose is to protect the product from degradation, extend its shelf life, maintain freshness, and preserve its quality, particularly for sensitive items like food, pharmaceuticals, and electronics.

What are the main types of materials used in barrier films?

Barrier films commonly utilize various polymeric materials, often in multi-layer structures, to achieve specific barrier properties. Key materials include Polyethylene (PE) for moisture barrier, Polypropylene (PP) for heat resistance, Polyethylene Terephthalate (PET) for strength, Ethylene Vinyl Alcohol (EVOH) for oxygen barrier, Polyvinylidene Chloride (PVDC) for broad spectrum barrier, and Polyamide (Nylon) for puncture resistance and gas barrier. Bio-based and recyclable alternatives are also emerging.

Which industries are the primary consumers of barrier films?

The food and beverage industry is the largest consumer of barrier films, utilizing them for packaging meat, dairy, snacks, and beverages to extend shelf life and maintain freshness. Other significant consumers include the pharmaceutical and healthcare sector for protecting medicines and medical devices, cosmetics and personal care for preserving product integrity, and industrial applications for sensitive components.

How do barrier films contribute to sustainability efforts in packaging?

Barrier films contribute to sustainability by extending product shelf life, thereby reducing food waste and spoilage, which has a significant environmental footprint. Innovations are focusing on developing recyclable mono-material barrier films, bio-based and compostable alternatives, and lightweighting solutions to minimize material usage and reduce transportation emissions. These advancements aim to align performance with environmental responsibility.

What are the key factors driving the growth of the barrier film market?

The primary drivers include the increasing global demand for packaged foods and beverages, particularly for extended shelf life, the rapid expansion of e-commerce necessitating robust packaging, and stringent food safety and pharmaceutical regulations. Additionally, technological advancements in material science and increasing consumer awareness regarding product quality and freshness are propelling market growth.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted