Banking as a Service Market

Banking as a Service Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702479 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

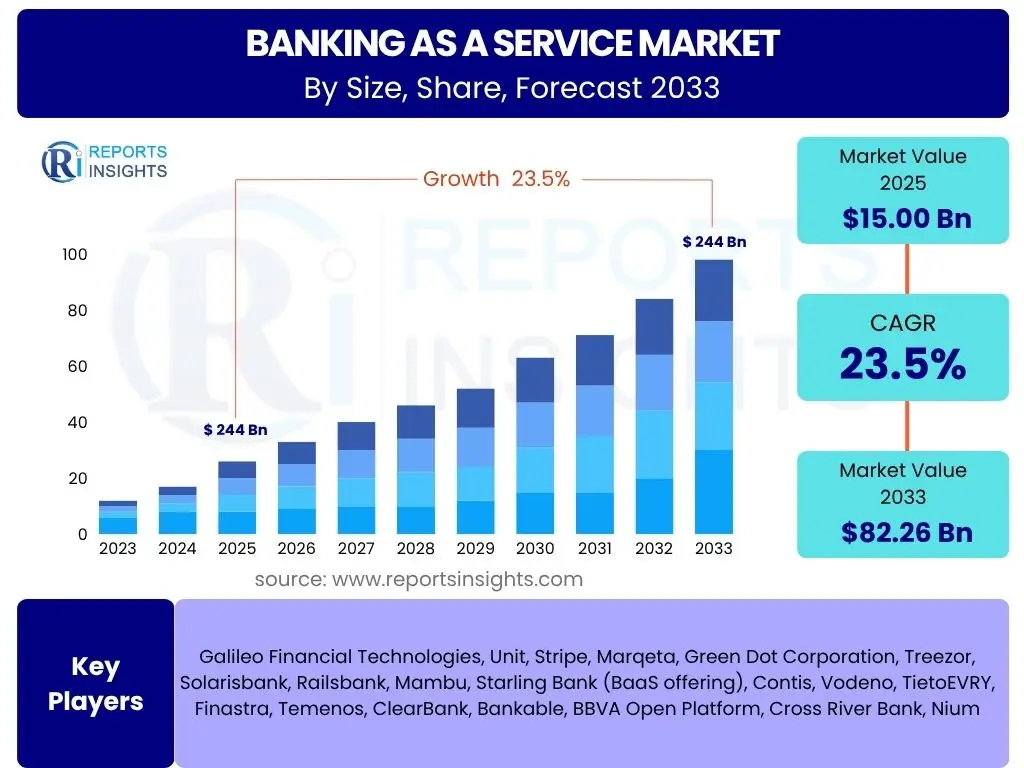

Banking as a Service Market Size

According to Reports Insights Consulting Pvt Ltd, The Banking as a Service Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 23.5% between 2025 and 2033. The market is estimated at USD 15.00 Billion in 2025 and is projected to reach USD 82.26 Billion by the end of the forecast period in 2033.

Key Banking as a Service Market Trends & Insights

The Banking as a Service (BaaS) market is undergoing a significant transformation, driven by an increasing demand for embedded finance solutions and digital-first banking experiences. Common user questions often revolve around how traditional financial institutions are adapting, the role of API-driven platforms, and the emergence of new business models. A key trend is the growing collaboration between established banks and fintechs, enabling non-financial companies to seamlessly integrate banking functionalities into their core offerings. This shift is redefining the competitive landscape, pushing incumbent banks to adopt more agile and modular approaches to service delivery.

Furthermore, the market is seeing a strong emphasis on hyper-personalization and niche financial products, catering to specific customer segments or industry verticals that were traditionally underserved. This includes specialized lending, payment solutions, and loyalty programs built directly into consumer applications. Regulatory frameworks are also evolving to support open banking initiatives, fostering greater data sharing and innovation, which further propels the adoption of BaaS models. The focus is increasingly on creating a seamless and invisible banking experience for the end-user, where financial services are integrated into daily digital interactions rather than being a separate, standalone activity.

- Proliferation of Embedded Finance: Integration of financial services into non-financial platforms.

- API-First Strategy Adoption: Widespread use of APIs for seamless service integration and modularity.

- Increased Collaboration: Strategic partnerships between traditional banks, fintechs, and non-financial entities.

- Focus on Niche Markets: Development of specialized banking products for specific industries or customer segments.

- Regulatory Support for Open Banking: Evolving regulations promoting data sharing and innovation.

- Shift to Cloud-Native Solutions: Greater reliance on cloud infrastructure for scalability and efficiency.

- Enhanced Personalization: Leveraging data to offer customized financial products and user experiences.

AI Impact Analysis on Banking as a Service

Common user questions regarding AI's impact on Banking as a Service often center on its role in automation, risk management, and customer experience enhancement. Artificial intelligence is poised to revolutionize BaaS by enabling highly intelligent and efficient operations, from fraud detection and prevention to predictive analytics for credit scoring and customer behavior analysis. AI-powered algorithms can process vast amounts of data at unprecedented speeds, allowing BaaS providers to offer more personalized and proactive financial services. This capability is crucial for identifying emerging trends, optimizing service delivery, and maintaining a competitive edge in a rapidly evolving market.

Moreover, AI contributes significantly to the scalability and automation of BaaS platforms. By automating routine tasks such as onboarding, compliance checks, and customer support (via chatbots or virtual assistants), AI reduces operational costs and improves efficiency, allowing human resources to focus on more complex, value-added activities. While concerns exist about data privacy and the ethical implications of AI in financial decisions, the overall expectation is that AI will drive greater innovation, security, and accessibility within the BaaS ecosystem, enabling new forms of financial products and services that were previously unfeasible.

- Automated Onboarding and KYC: Streamlining customer verification processes with AI.

- Enhanced Fraud Detection: Utilizing machine learning for real-time anomaly detection and prevention.

- Personalized Financial Products: AI-driven insights for tailored recommendations and services.

- Predictive Analytics for Risk Assessment: Improving credit scoring and risk management models.

- Operational Efficiency: Automation of routine tasks, reducing manual intervention and costs.

- Customer Service Augmentation: AI-powered chatbots and virtual assistants for instant support.

- Data Security and Compliance: AI for monitoring and ensuring adherence to regulatory standards.

Key Takeaways Banking as a Service Market Size & Forecast

User inquiries about the key takeaways from the Banking as a Service market size and forecast frequently highlight the implications of its robust growth trajectory for various stakeholders, including traditional banks, fintechs, and non-financial brands. The primary insight is the undeniable shift towards a more modular, API-driven financial landscape, where the emphasis moves from owning the customer relationship entirely to facilitating embedded financial services. This rapid expansion underscores the increasing acceptance and demand for flexible, customizable banking functionalities that can be seamlessly integrated into diverse consumer and business applications. The market's significant projected growth signals a strong move away from monolithic banking models towards a distributed, interconnected financial ecosystem.

Another crucial takeaway is the imperative for both incumbent financial institutions and emerging fintechs to embrace collaborative strategies. The future success in the BaaS market lies in forming strategic partnerships that leverage the strengths of each participant: the regulatory expertise and trust of banks combined with the technological agility and innovation of fintechs. The forecast indicates that businesses across various sectors, not just finance, will increasingly seek to embed financial services, making BaaS a critical enabler for new revenue streams and enhanced customer experiences. This transformation necessitates a proactive approach to technology adoption, regulatory compliance, and a deep understanding of evolving customer needs to capitalize on the vast opportunities presented by this growing market.

- Rapid Market Expansion: BaaS is a high-growth sector reshaping financial services.

- Modular Banking Future: Emphasis on API-driven, customizable financial components.

- Strategic Collaboration is Key: Success hinges on partnerships between banks and fintechs.

- Embedded Finance Dominance: Financial services becoming integral to non-financial products.

- New Revenue Streams: BaaS enables businesses across sectors to offer financial products.

- Digital Transformation Imperative: Banks must accelerate digitalization to remain competitive.

- Regulatory Adaptation: Continuous evolution of frameworks to support innovation while ensuring stability.

Banking as a Service Market Drivers Analysis

The Banking as a Service market is propelled by a confluence of powerful drivers stemming from both technological advancements and evolving consumer expectations. A primary driver is the accelerating digital transformation across industries, compelling businesses to integrate financial services directly into their user journeys for enhanced convenience and stickiness. This push is complemented by the rising demand for customized financial products and solutions that cater to specific niche markets or individual preferences, moving away from generic banking offerings. The proliferation of APIs has significantly lowered the barriers to entry for non-financial companies, allowing them to easily consume and offer banking functionalities without building an entire banking infrastructure from scratch, fostering a more collaborative and innovative ecosystem.

Furthermore, the inherent cost efficiency offered by BaaS models is a significant incentive for businesses, as it eliminates the need for substantial upfront investments in technology and regulatory compliance. This allows companies to focus on their core competencies while leveraging specialized financial partners. Supportive regulatory environments, particularly the global movement towards Open Banking and PSD2 in Europe, are also playing a crucial role by mandating data sharing and fostering competition, thereby creating a fertile ground for BaaS adoption. These drivers collectively point towards a future where banking services are unbundled, distributed, and seamlessly integrated into the fabric of daily digital life.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Accelerating Digital Transformation | +1.8% | Global, particularly North America, Europe, APAC | Short to Medium Term (2025-2029) |

| Increasing Demand for Customized Financial Products | +1.5% | Global, highly relevant in developed markets | Medium to Long Term (2027-2033) |

| Proliferation of APIs and Cloud Technologies | +2.0% | Global, foundational for all regions | Ongoing (2025-2033) |

| Cost Efficiency and Reduced Time-to-Market | +1.2% | Global, highly attractive to SMEs and startups | Short to Medium Term (2025-2029) |

| Supportive Regulatory Frameworks (Open Banking) | +1.0% | Europe, North America, parts of APAC | Medium to Long Term (2027-2033) |

Banking as a Service Market Restraints Analysis

Despite its significant growth potential, the Banking as a Service market faces several substantial restraints that could impede its trajectory. One of the most prominent challenges is the complex and fragmented regulatory landscape across different jurisdictions. Financial services are heavily regulated, and operating globally or even across multiple countries requires navigating a maze of varying compliance requirements, licensing, and data privacy laws, which can be costly and time-consuming for BaaS providers and their clients. This regulatory burden often leads to slower adoption rates, especially for smaller players or those operating in multiple geographies, as it necessitates significant legal and compliance expertise.

Another key restraint is the inherent concern around data security and privacy. As BaaS involves sharing sensitive financial data through APIs and cloud platforms, the risk of data breaches, cyberattacks, and unauthorized access remains a significant apprehension for both financial institutions and end-users. Building and maintaining trust in a highly interconnected ecosystem requires robust security protocols, continuous monitoring, and transparent data handling practices, which adds to the operational complexity and cost. Furthermore, integrating legacy IT systems of traditional banks with modern BaaS platforms can be a formidable technical challenge, often characterized by high costs, interoperability issues, and resistance to change, thus slowing down the transition for incumbent players.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Regulatory Complexity and Compliance Burden | -0.8% | Global, particularly multi-country operations | Ongoing (2025-2033) |

| Data Security and Privacy Concerns | -1.0% | Global, especially in regions with strict data protection laws | Ongoing (2025-2033) |

| Integration Challenges with Legacy Systems | -0.7% | Developed markets with established financial infrastructures | Short to Medium Term (2025-2029) |

| Lack of Standardization Across APIs and Platforms | -0.5% | Global, impacts seamless interoperability | Medium Term (2027-2031) |

| Reputational Risks for Partnering Brands | -0.6% | Global, impacts trust and adoption | Short to Medium Term (2025-2029) |

Banking as a Service Market Opportunities Analysis

The Banking as a Service market is rich with opportunities, primarily stemming from the increasing digital maturity of various industries and the global push towards financial inclusion. A significant opportunity lies in the expansion of BaaS into new industry verticals beyond traditional financial services, such as healthcare, logistics, automotive, and real estate, where embedded finance can create novel value propositions and revenue streams. Businesses in these sectors are actively seeking to integrate payments, lending, and other financial tools directly into their core services, enabling a seamless customer experience and unlocking untapped market potential. This diversification represents a major growth avenue for BaaS providers looking to broaden their client base and application scope.

Furthermore, emerging markets, particularly in Asia Pacific, Latin America, and Africa, present vast opportunities due to their rapidly growing digital populations, high mobile penetration rates, and often underserved traditional banking sectors. BaaS can facilitate financial inclusion by enabling non-bank entities to offer accessible and affordable financial services to populations previously excluded from the formal financial system. The continuous evolution of blockchain and distributed ledger technologies also offers a unique opportunity for BaaS platforms to enhance security, transparency, and efficiency in cross-border payments and asset management. Moreover, the growing focus on hyper-personalization and creating niche financial products tailored to specific demographics or professional groups opens up avenues for specialized BaaS offerings that cater to unique market demands.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into New Industry Verticals | +1.8% | Global, particularly developed economies | Medium to Long Term (2027-2033) |

| Growth in Emerging Markets and Financial Inclusion | +1.5% | APAC, Latin America, MEA | Long Term (2029-2033) |

| Integration of Blockchain and DLT | +1.2% | Global, especially for cross-border transactions | Medium to Long Term (2027-2033) |

| Demand for Niche and Personalized Financial Services | +1.0% | Developed markets, caters to specific demographics | Short to Medium Term (2025-2029) |

| Further Development of Open Banking Ecosystems | +0.9% | Europe, spreading to other regions | Ongoing (2025-2033) |

Banking as a Service Market Challenges Impact Analysis

The Banking as a Service market, while promising, is not without its significant challenges that demand strategic navigation. One major challenge is the inherent interoperability issues arising from a lack of universal standards for APIs and data exchange protocols across different BaaS providers and traditional banking systems. This fragmentation can hinder seamless integration and scaling, leading to increased development costs and slower deployment times for businesses attempting to leverage multiple financial partners. Ensuring smooth communication and data flow between diverse platforms remains a critical hurdle that requires industry-wide collaboration and standardization efforts, which are currently nascent.

Another crucial challenge is the talent gap, specifically the scarcity of professionals with expertise spanning both traditional banking regulations and cutting-edge financial technology. Building and maintaining robust BaaS platforms requires a unique blend of skills in areas like cloud computing, API development, cybersecurity, and deep regulatory knowledge, which is in high demand and short supply. Furthermore, maintaining customer trust and managing reputational risks are paramount. Any service disruption, security breach, or compliance failure by a BaaS provider or their banking partner can severely damage the brand reputation of the non-financial company embedding the services, highlighting the need for stringent due diligence and robust service level agreements. Navigating these complexities effectively is crucial for sustained market growth.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Interoperability and Standardization Issues | -0.7% | Global, affects multi-vendor strategies | Ongoing (2025-2033) |

| Talent Gap in FinTech and Regulatory Expertise | -0.6% | Global, particularly in rapidly growing hubs | Short to Medium Term (2025-2029) |

| Maintaining Customer Trust and Managing Reputational Risk | -0.8% | Global, highly sensitive to service failures | Ongoing (2025-2033) |

| Intense Competition from Traditional Banks and New Entrants | -0.5% | Developed markets, leading to price pressure | Medium Term (2027-2031) |

| Ensuring Robust Cybersecurity for Interconnected Systems | -0.9% | Global, critical for financial integrity | Ongoing (2025-2033) |

Banking as a Service Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Banking as a Service (BaaS) market, offering detailed insights into its current size, historical performance, and future growth projections from 2025 to 2033. It meticulously examines key market trends, drivers, restraints, opportunities, and challenges that influence the market landscape. The report also includes a thorough segmentation analysis by component, type, enterprise size, and end-user, providing a granular view of market dynamics across various categories. Furthermore, it highlights regional market performance and profiles leading companies, offering a holistic understanding for stakeholders and strategic decision-makers.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 15.00 Billion |

| Market Forecast in 2033 | USD 82.26 Billion |

| Growth Rate | 23.5% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Galileo Financial Technologies, Unit, Stripe, Marqeta, Green Dot Corporation, Treezor, Solarisbank, Railsbank, Mambu, Starling Bank (BaaS offering), Contis, Vodeno, TietoEVRY, Finastra, Temenos, ClearBank, Bankable, BBVA Open Platform, Cross River Bank, Nium |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Banking as a Service market is intricately segmented to provide a comprehensive understanding of its diverse applications and operational models. This segmentation highlights the various facets of the BaaS ecosystem, ranging from the core components that facilitate these services to the specific types of deployments, the size of enterprises leveraging them, and the wide array of end-user industries benefiting from embedded financial capabilities. Analyzing these segments helps in identifying key growth pockets, understanding demand patterns, and tailoring solutions to meet distinct market needs, thereby offering a granular view of the market's structure and its potential for expansion across different verticals and client profiles.

- By Component: This segment differentiates between the core platform infrastructure and the complementary services offered within the BaaS model.

- Platform: Refers to the technological backbone, including APIs, core banking systems, and regulatory engines that enable financial services.

- Services: Encompasses the support, consulting, compliance, and operational services provided alongside the platform.

- By Type: This segmentation categorizes BaaS offerings based on their underlying technological architecture.

- API-based: Focuses on granular financial functionalities exposed via APIs for third-party integration.

- Cloud-based: Highlights solutions primarily hosted and delivered through cloud infrastructure for scalability and accessibility.

- Hybrid: Combines elements of both API-based and cloud-based models, often incorporating on-premise components.

- By Enterprise Size: This segment distinguishes between the varying needs and adoption rates of businesses based on their scale.

- Small and Medium-sized Enterprises (SMEs): Typically seek cost-effective and agile solutions to embed financial services.

- Large Enterprises: Often require robust, scalable, and highly customizable BaaS platforms for complex operations.

- By End-user: This crucial segment identifies the diverse industries and entities that are increasingly integrating BaaS.

- Fintechs: Leverage BaaS to rapidly launch innovative financial products without a banking license.

- Neobanks: Utilize BaaS to build their digital-first banking propositions.

- Retail & E-commerce: Embed payment processing, lending, and loyalty programs into their customer journeys.

- Healthcare: Integrates payment solutions, insurance, and financing options for patients and providers.

- Telecommunications: Offers embedded payments, mobile wallets, and credit services to subscribers.

- Other Industries: Includes logistics, manufacturing, travel, and various other sectors adopting embedded finance.

Regional Highlights

- North America: This region leads the Banking as a Service market due to its advanced digital infrastructure, high adoption of fintech innovations, and a robust ecosystem of startups and established technology companies. The presence of major financial hubs and a strong venture capital landscape further fuels investment and innovation in BaaS platforms, driving significant market expansion. The demand for embedded finance solutions across various industries, from retail to software, is particularly strong in the United States and Canada.

- Europe: Driven by progressive regulatory initiatives like PSD2 (Revised Payment Services Directive) and Open Banking, Europe is a key growth region for BaaS. The emphasis on fostering competition and consumer choice has accelerated the adoption of API-driven banking solutions. Countries like the UK, Germany, and the Nordic nations are at the forefront, with a high concentration of specialized BaaS providers and a receptive market for innovative financial services.

- Asia Pacific (APAC): The APAC region exhibits immense growth potential, propelled by rapid digital adoption, increasing mobile penetration, and a large unbanked or underbanked population. Countries such as China, India, Singapore, and Australia are witnessing a surge in fintech innovation and the emergence of digital-first banks. BaaS offers a scalable solution for financial inclusion and for integrating financial services into the vast e-commerce and digital ecosystems prevalent in this region.

- Latin America: This region is experiencing a significant digital transformation, with a growing number of consumers embracing digital payments and online financial services. Governments and regulators are increasingly supporting fintech innovation, creating a fertile ground for BaaS adoption. Brazil, Mexico, and Colombia are notable markets where BaaS is enabling new neobanks and fintechs to address long-standing financial access gaps and drive market development.

- Middle East and Africa (MEA): While still nascent in some areas, the MEA region presents considerable long-term opportunities for BaaS. Growing mobile money adoption, governmental initiatives to promote digital economies, and an expanding young, tech-savvy population are driving the demand for modern financial solutions. BaaS can play a crucial role in enhancing financial inclusion and supporting the diversification of economies away from traditional sectors.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Banking as a Service Market.- Galileo Financial Technologies

- Unit

- Stripe

- Marqeta

- Green Dot Corporation

- Treezor

- Solarisbank

- Railsbank

- Mambu

- Starling Bank (BaaS offering)

- Contis

- Vodeno

- TietoEVRY

- Finastra

- Temenos

- ClearBank

- Bankable

- BBVA Open Platform

- Cross River Bank

- Nium

Frequently Asked Questions

Analyze common user questions about the Banking as a Service market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is Banking as a Service (BaaS)?

Banking as a Service (BaaS) is a model where licensed banks allow third-party businesses (often fintechs or non-financial companies) to connect with their banking systems via APIs. This enables these third parties to offer financial products and services, such as accounts, payments, and lending, directly to their own customers, without needing to acquire their own banking license.

How does BaaS benefit businesses?

BaaS offers several benefits, including faster time-to-market for new financial products, reduced operational costs by leveraging existing banking infrastructure, access to a wider range of financial services, and the ability to create new revenue streams through embedded finance. It allows businesses to focus on their core competencies while seamlessly integrating financial functionalities.

What are the main challenges in BaaS adoption?

Key challenges in BaaS adoption include navigating complex and fragmented regulatory landscapes across different jurisdictions, ensuring robust data security and privacy, integrating with diverse legacy IT systems, and managing reputational risks associated with third-party partnerships. The scarcity of specialized talent combining fintech and regulatory expertise also poses a challenge.

What is the future outlook for the BaaS market?

The BaaS market is projected for significant growth, driven by increasing digital transformation, the proliferation of embedded finance, and supportive regulatory environments like Open Banking. The future outlook points towards greater collaboration between traditional banks and fintechs, expansion into new industry verticals, and the development of hyper-personalized financial products, further solidifying BaaS as a fundamental component of the digital economy.

How does BaaS differ from Open Banking?

While related, BaaS and Open Banking are distinct concepts. Open Banking is a regulatory framework (e.g., PSD2 in Europe) that mandates banks to share customer data securely with third-party providers, with customer consent, via APIs. BaaS, on the other hand, is a commercial model where banks provide financial services (e.g., accounts, payments) as a white-label product for non-bank businesses to integrate directly into their offerings, going beyond just data sharing to actual service provision.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted