B2B Money Transfer Market

B2B Money Transfer Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707906 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

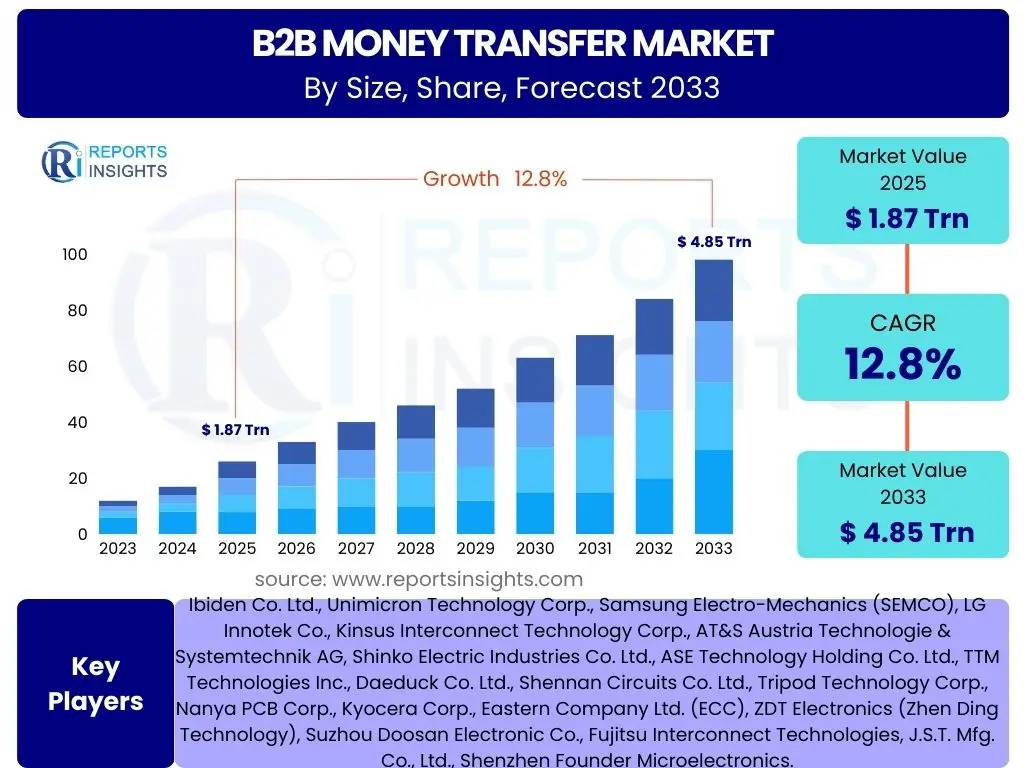

B2B Money Transfer Market Size

According to Reports Insights Consulting Pvt Ltd, The B2B Money Transfer Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.8% between 2025 and 2033. The market is estimated at USD 1.87 Trillion in 2025 and is projected to reach USD 4.85 Trillion by the end of the forecast period in 2033.

Key B2B Money Transfer Market Trends & Insights

The B2B money transfer market is undergoing a significant transformation, driven by a confluence of technological advancements, evolving business demands, and regulatory shifts. Common inquiries reveal a strong focus on efficiency, transparency, and security in cross-border transactions. Businesses are increasingly seeking solutions that reduce processing times, lower costs, and provide real-time visibility into payment statuses. This pursuit of operational excellence is a primary driver behind the adoption of modern payment infrastructure and innovative financial technologies.

Furthermore, the market is characterized by a growing demand for integrated payment solutions that can seamlessly connect with existing enterprise resource planning (ERP) systems and accounting software. This integration capability is crucial for streamlining financial operations, improving reconciliation processes, and enhancing overall treasury management. Regulatory developments, particularly those promoting faster payments and greater transparency, also play a pivotal role in shaping market dynamics and influencing the strategic decisions of service providers.

- Real-time Payment Adoption: Increasing demand for instant settlement of B2B transactions, both domestically and internationally, pushing the adoption of faster payment rails.

- API-led Integration: Widespread use of Application Programming Interfaces (APIs) to embed payment functionalities directly into business workflows, enhancing automation and efficiency.

- Blockchain and DLT Exploration: Continued experimentation and pilot projects leveraging blockchain and Distributed Ledger Technology (DLT) for enhanced security, transparency, and reduced intermediaries in cross-border payments.

- Digitalization of Foreign Exchange (FX): Greater reliance on digital platforms for foreign exchange transactions, offering competitive rates, better transparency, and efficient hedging strategies.

- Enhanced Data Analytics and Reporting: Businesses demand sophisticated tools for tracking, analyzing, and reporting on their payment flows to gain deeper financial insights and improve forecasting.

- Focus on Compliance and Security: Growing emphasis on robust Know Your Customer (KYC), Anti-Money Laundering (AML), and fraud prevention measures, driven by stricter global regulations and rising cyber threats.

AI Impact Analysis on B2B Money Transfer

Artificial Intelligence (AI) is rapidly emerging as a transformative force within the B2B money transfer sector, addressing critical pain points and unlocking new efficiencies. Users frequently inquire about AI's capacity to automate complex tasks, enhance security protocols, and provide deeper insights into transactional data. The technology's ability to process vast amounts of data at unprecedented speeds allows for predictive analytics, informed decision-making, and proactive risk management, thereby revolutionizing traditional payment operations.

Specific applications of AI include advanced fraud detection, where algorithms identify anomalous patterns in real-time, significantly reducing financial losses and improving trust. Furthermore, AI-powered systems are streamlining compliance checks, automating sanction screening, and accelerating the onboarding process for new clients, which are traditionally resource-intensive activities. While the benefits are substantial, concerns regarding data privacy, algorithmic bias, and the need for human oversight in critical decisions remain key considerations for market participants and regulators.

- Fraud Detection and Prevention: AI algorithms analyze transaction patterns in real-time to identify and flag suspicious activities, significantly reducing financial fraud.

- Predictive Analytics for FX Rates: AI models leverage historical data and market trends to forecast currency fluctuations, enabling businesses to optimize their foreign exchange strategies.

- Automated Compliance and KYC/AML: AI-driven solutions automate the screening of transactions and customer data against regulatory databases, streamlining compliance processes and reducing manual effort.

- Intelligent Payment Routing: AI optimizes payment routes based on factors like cost, speed, and success rates, ensuring the most efficient transfer path for each transaction.

- Enhanced Customer Service: AI-powered chatbots and virtual assistants provide instant support, resolving common queries and guiding users through the money transfer process.

- Operational Efficiency and Automation: AI automates repetitive tasks such as data entry, reconciliation, and payment scheduling, freeing up human resources for more strategic initiatives.

Key Takeaways B2B Money Transfer Market Size & Forecast

The B2B money transfer market is poised for robust and sustained growth, signaling a fundamental shift towards more sophisticated, digital-first payment ecosystems. Key inquiries consistently highlight the imperative for businesses to adopt advanced solutions that offer speed, transparency, and cost-effectiveness in their financial operations. This growth trajectory is not merely incremental but represents a transformative phase driven by global economic integration, increasing cross-border trade volumes, and the relentless pursuit of operational efficiencies by enterprises of all sizes.

A significant takeaway is the pivotal role of technological innovation, particularly in areas like real-time payments, API integration, and the emerging applications of AI and blockchain. These technologies are not just incremental improvements but foundational shifts enabling frictionless transactions across diverse geographies and regulatory landscapes. Furthermore, the market's expansion underscores the increasing fragmentation of payment service providers, where specialized fintechs are challenging traditional banking models, leading to a more competitive and innovative environment that ultimately benefits businesses seeking optimized transfer solutions.

- Strong Growth Trajectory: The market is projected to grow substantially, reaching nearly USD 5 trillion by 2033, driven by digitalization and globalization.

- Digitalization Imperative: Businesses are rapidly adopting digital platforms for B2B transfers, moving away from traditional, slower methods to enhance efficiency and transparency.

- Regulatory Evolution: Ongoing and evolving regulatory frameworks, such as those promoting instant payments and cross-border data sharing, significantly influence market development and compliance requirements.

- Fintech Innovation Drives Disruption: Non-bank payment providers and fintech companies are introducing advanced solutions, fostering competition and pushing the boundaries of traditional B2B money transfer services.

- Focus on Cost and Speed: Enterprises prioritize solutions that offer reduced transaction costs and faster settlement times, directly impacting their cash flow and operational agility.

- Increased Demand for Seamless Integration: The ability to integrate money transfer solutions with existing enterprise systems (e.g., ERP, accounting software) is a critical factor for adoption and market success.

B2B Money Transfer Market Drivers Analysis

The B2B money transfer market's robust expansion is primarily fueled by a complex interplay of global economic trends and technological advancements. The increasing volume of cross-border trade, coupled with the relentless pursuit of operational efficiencies by businesses, acts as a significant catalyst. Enterprises are constantly seeking faster, more transparent, and cost-effective methods to manage their international payments, moving beyond legacy systems that often entail delays and high fees. This demand for improved payment infrastructure is pervasive across various industry verticals.

Furthermore, the ongoing digital transformation initiatives within organizations worldwide are accelerating the adoption of advanced payment solutions. Businesses are embracing API-driven platforms, cloud-based services, and integrated financial technologies to automate their payment workflows, reduce manual errors, and enhance real-time financial visibility. Regulatory support for digital payments, coupled with initiatives like open banking, also plays a crucial role in fostering an environment conducive to innovation and wider market adoption.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Globalization of Trade and E-commerce | +2.5% | Global, particularly APAC and Europe | Long-term (2025-2033) |

| Demand for Faster and Cheaper Payments | +2.0% | Global, especially North America and Europe | Mid-term (2027-2030) |

| Digital Transformation Initiatives | +1.8% | Global, across all enterprise sizes | Short-term (2025-2027) |

| Increased Adoption of API-based Solutions | +1.5% | North America, Europe, emerging markets | Mid-term (2027-2030) |

| Regulatory Push for Real-time Payments | +1.2% | Europe (SEPA Instant), India (UPI), Brazil (PIX) | Short-term (2025-2027) |

B2B Money Transfer Market Restraints Analysis

Despite the significant growth prospects, the B2B money transfer market faces several formidable restraints that can impede its full potential. A primary challenge is the highly fragmented and often complex regulatory landscape governing cross-border payments. Diverse compliance requirements across different jurisdictions necessitate substantial investment in legal and technological infrastructure for service providers, increasing operational costs and creating barriers to entry for smaller players. This regulatory patchwork can also lead to inconsistencies in service delivery and increased transaction scrutiny.

Furthermore, cybersecurity risks and the persistent threat of financial fraud represent significant hurdles. As B2B money transfers become increasingly digitalized, they also become more susceptible to sophisticated cyberattacks. Ensuring robust data security and maintaining public trust requires continuous investment in advanced security technologies and strict adherence to data protection regulations. The integration challenges associated with legacy banking systems, and the inherent resistance to change within some traditional financial institutions, also slow down the adoption of newer, more efficient payment methods.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complex and Fragmented Regulatory Landscape | -1.5% | Global, especially EU and Asia | Long-term (2025-2033) |

| Cybersecurity Threats and Data Breaches | -1.0% | Global | Long-term (2025-2033) |

| High Costs of Compliance and Implementation | -0.8% | Global, particularly for new entrants | Mid-term (2027-2030) |

| Integration Challenges with Legacy Systems | -0.7% | North America, Europe (older financial institutions) | Mid-term (2027-2030) |

| Foreign Exchange Volatility | -0.5% | Global, particularly emerging markets | Short-term (2025-2027) |

B2B Money Transfer Market Opportunities Analysis

The B2B money transfer market presents significant untapped opportunities for innovation and expansion, particularly in emerging economies and through the adoption of transformative technologies. The rapidly expanding e-commerce sector and the rise of digital-native businesses create a continuous demand for scalable, efficient, and globally accessible payment solutions. There is immense potential in catering to Small and Medium-sized Enterprises (SMEs) that often lack access to sophisticated treasury management tools and affordable cross-border payment options, representing a vast underserved market segment.

Moreover, the ongoing development and increased acceptance of blockchain and Distributed Ledger Technology (DLT) offer avenues for creating highly secure, transparent, and near real-time payment networks that bypass traditional banking intermediaries. Strategic partnerships between established financial institutions and agile fintech companies are also crucial, allowing for the co-creation of innovative services and the leveraging of complementary strengths to reach broader customer bases. The increasing focus on supply chain finance and embedded payments within various industry verticals further opens new revenue streams and enhances operational integration for businesses.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Emerging Markets (APAC, LATAM, MEA) | +2.5% | Asia Pacific, Latin America, Middle East & Africa | Long-term (2025-2033) |

| Development of Blockchain and DLT-based Solutions | +2.0% | Global, especially financial innovation hubs | Mid-term (2027-2030) |

| Strategic Partnerships between Fintechs and Banks | +1.8% | North America, Europe, Asia Pacific | Mid-term (2027-2030) |

| Focus on SME Segment for Cross-border Payments | +1.5% | Global, all regions | Long-term (2025-2033) |

| Integration with Supply Chain Finance Platforms | +1.2% | Global, manufacturing and logistics sectors | Short-term (2025-2027) |

B2B Money Transfer Market Challenges Impact Analysis

The B2B money transfer market, while dynamic, is continually challenged by several systemic and operational hurdles that impact its growth and efficiency. Managing the inherent volatility of foreign exchange rates, especially for businesses operating across multiple currencies, remains a significant concern, directly affecting profitability and financial planning. This necessitates advanced hedging strategies and real-time currency conversion capabilities, which not all providers can consistently offer at competitive rates. The complexity of achieving seamless interoperability among a vast array of disparate payment systems and financial networks also poses a considerable technical challenge.

Furthermore, the persistent threat of financial crime, including money laundering and terrorism financing, demands continuous investment in robust fraud prevention and anti-money laundering (AML) technologies. Service providers must navigate an increasingly stringent global compliance landscape, where regulatory non-adherence can result in severe penalties and reputational damage. The intense competition within the market, driven by both traditional banks and innovative fintechs, compels continuous innovation and pressure on pricing, which can be challenging for maintaining profitability while investing in necessary infrastructure upgrades.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Managing Foreign Exchange (FX) Volatility | -1.2% | Global, particularly for companies with international trade | Long-term (2025-2033) |

| Achieving Interoperability Across Diverse Systems | -1.0% | Global, affecting seamless cross-border transfers | Long-term (2025-2033) |

| Combatting Financial Crime and Fraud | -0.9% | Global, a constant concern for all participants | Long-term (2025-2033) |

| Intense Competition and Pricing Pressures | -0.7% | North America, Europe (mature markets) | Mid-term (2027-2030) |

| Maintaining Regulatory Compliance in Evolving Landscape | -0.6% | Global, particularly for multi-jurisdictional operations | Short-term (2025-2027) |

B2B Money Transfer Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the B2B Money Transfer Market, offering strategic insights into its current landscape, future projections, and the underlying factors influencing its growth. The report covers a detailed market size and forecast, examining key trends, drivers, restraints, opportunities, and challenges across various segments and major geographic regions. It aims to equip stakeholders with critical data and analytical perspectives to make informed business decisions, navigate the competitive environment, and identify lucrative growth avenues within the evolving B2B payments ecosystem.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.87 Trillion |

| Market Forecast in 2033 | USD 4.85 Trillion |

| Growth Rate | 12.8% CAGR |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | J.P. Morgan Chase & Co., Wells Fargo & Company, Citigroup Inc., Bank of America Corporation, HSBC Holdings plc, Standard Chartered PLC, Deutsche Bank AG, BNP Paribas SA, SWIFT, Western Union Business Solutions, TransferMate, Payoneer Inc., Ripple Labs Inc., Stripe, Inc., Wise (formerly TransferWise), Airwallex, NIUM, WorldFirst, Remitly for Business, Currencycloud |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The B2B money transfer market is extensively segmented to provide a granular understanding of its diverse components and the unique demands of various business environments. This segmentation allows for targeted analysis of market penetration, growth opportunities, and competitive dynamics across different operational parameters. Understanding these distinct segments is crucial for solution providers to tailor their offerings, optimize their market strategies, and address specific pain points within the B2B payment ecosystem.

Key segmentation categories include transaction type, which differentiates between cross-border and domestic transfers, as well as bulk and payroll payments, reflecting varying operational complexities and regulatory requirements. Furthermore, the market is analyzed by end-user industry, recognizing that sectors like BFSI, retail, manufacturing, and healthcare have distinct payment volumes, frequency, and security needs. Technological segmentation, encompassing blockchain, API-based, and cloud-based solutions, highlights the ongoing shift towards advanced digital infrastructures, while company size segmentation acknowledges the differing payment scale and resource availability between SMEs and large enterprises.

- By Transaction Type:

- Cross-border Payments: Transfers between different countries, often involving currency conversion and multiple intermediaries.

- Domestic Payments: Transfers within the same country, typically faster and less complex.

- Bulk Payments: High-volume transactions, such as vendor payments or salary disbursements.

- Payroll Payments: Specific transfers for employee salaries and associated benefits.

- By End-user Industry:

- BFSI (Banking, Financial Services, and Insurance): High-volume, high-value transfers, stringent regulatory compliance.

- Retail & E-commerce: Frequent, often smaller-value cross-border payments for suppliers and logistics.

- Manufacturing: Payments for raw materials, international supply chain transactions, and machinery.

- Healthcare: Payments for medical supplies, international research collaborations, and specialized services.

- IT & Telecommunications: Payments for software licenses, global service providers, and infrastructure.

- Government: Public sector payments, international aid, and inter-governmental transfers.

- Logistics & Transportation: Payments for freight, shipping, fuel, and cross-border customs.

- Others: Including education, media, and professional services.

- By Technology:

- Blockchain/DLT: Solutions leveraging distributed ledger technology for enhanced security, speed, and transparency.

- API-based: Platforms offering open APIs for seamless integration into existing business systems.

- Cloud-based: Software-as-a-Service (SaaS) payment platforms accessible over the internet.

- Traditional Banking Platforms: Legacy systems offered by conventional financial institutions.

- By Company Size:

- Small and Medium-sized Enterprises (SMEs): Businesses with lower transaction volumes but increasing need for accessible and affordable solutions.

- Large Enterprises: Corporations with high transaction volumes, complex treasury management, and global payment needs.

Regional Highlights

- North America: This region represents a mature and technologically advanced market for B2B money transfers, characterized by high adoption rates of digital payment solutions and a strong presence of key fintech innovators. The drive for operational efficiency and the continuous evolution of payment infrastructure, including real-time payment initiatives, are key factors influencing growth.

- Europe: Driven by robust regulatory frameworks such as PSD2 and SEPA, Europe leads in fostering open banking and harmonized cross-border payments. The region exhibits high demand for instant payments, and fintech partnerships are common, aiming to provide seamless, transparent, and cost-effective solutions across its diverse economies.

- Asia Pacific (APAC): APAC is the fastest-growing market, propelled by rapid economic expansion, increasing cross-border trade, and high mobile payment adoption rates. Countries like India, China, and Southeast Asian nations are undergoing significant digital transformation, presenting immense opportunities for innovative B2B money transfer solutions.

- Latin America: This region is witnessing increasing digitalization and a growing need for efficient cross-border payment solutions, especially with expanding trade links. Government initiatives promoting financial inclusion and digital payment adoption are creating a favorable environment for market expansion, though regulatory inconsistencies can pose challenges.

- Middle East and Africa (MEA): The MEA region is emerging as a significant market due to increasing trade activities, investment in digital infrastructure, and a push for economic diversification. Growth is primarily driven by the need for faster and more affordable payment corridors, particularly for remittances and corporate treasury management.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the B2B Money Transfer Market.- J.P. Morgan Chase & Co.

- Wells Fargo & Company

- Citigroup Inc.

- Bank of America Corporation

- HSBC Holdings plc

- Standard Chartered PLC

- Deutsche Bank AG

- BNP Paribas SA

- SWIFT

- Western Union Business Solutions

- TransferMate

- Payoneer Inc.

- Ripple Labs Inc.

- Stripe, Inc.

- Wise (formerly TransferWise)

- Airwallex

- NIUM

- WorldFirst

- Remitly for Business

- Currencycloud

Frequently Asked Questions

What is the B2B Money Transfer Market?

The B2B money transfer market encompasses all financial transactions between businesses, including cross-border and domestic payments for goods, services, payroll, and other operational expenses. It involves the transfer of funds through various channels, from traditional banks to modern fintech platforms.

What drives the growth of B2B money transfers?

Growth is primarily driven by the globalization of trade, the increasing demand for faster and more cost-effective payment solutions, digital transformation initiatives within businesses, and the widespread adoption of API-based and cloud-based payment technologies.

How does AI impact B2B money transfers?

AI significantly impacts B2B money transfers by enhancing fraud detection, automating compliance checks, providing predictive analytics for foreign exchange rates, optimizing payment routing, and improving operational efficiency through process automation.

What are the main challenges in B2B cross-border payments?

Key challenges include navigating complex and fragmented regulatory landscapes, managing foreign exchange volatility, ensuring cybersecurity, achieving interoperability across diverse payment systems, and dealing with intense market competition and pricing pressures.

Which technologies are transforming B2B money transfers?

Transformative technologies include blockchain and Distributed Ledger Technology (DLT) for enhanced security and transparency, API-driven solutions for seamless integration, real-time payment systems for instant settlements, and artificial intelligence for automation and advanced analytics.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted