Aviation Seat Belt Market

Aviation Seat Belt Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708216 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

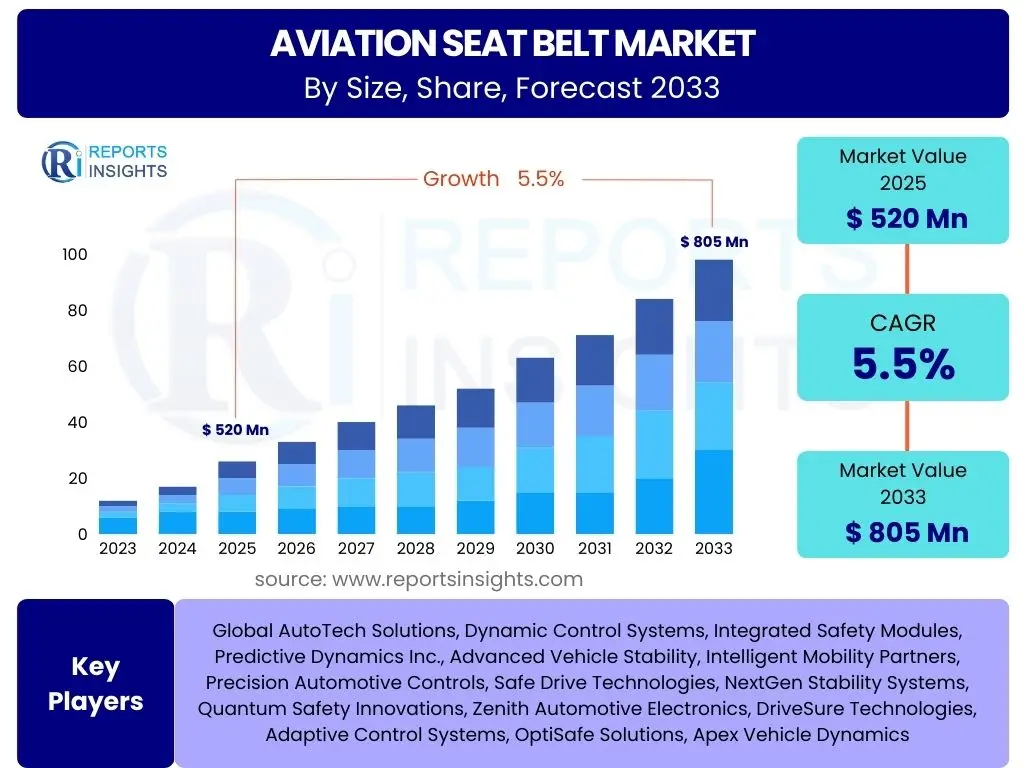

Aviation Seat Belt Market Size

According to Reports Insights Consulting Pvt Ltd, The Aviation Seat Belt Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.5% between 2025 and 2033. The market is estimated at USD 520 Million in 2025 and is projected to reach USD 805 Million by the end of the forecast period in 2033.

Key Aviation Seat Belt Market Trends & Insights

The aviation seat belt market is currently undergoing significant evolution, primarily driven by a continuous focus on enhancing passenger safety and comfort, alongside operational efficiency. Key trends include the integration of advanced materials to achieve lighter yet stronger designs, the development of intelligent seat belt systems with enhanced safety features, and a growing emphasis on modular and customizable solutions. These innovations are largely influenced by stringent regulatory frameworks and the increasing demand for improved passenger experience in both commercial and private aviation sectors. Furthermore, the expansion of global air travel and the modernization of existing aircraft fleets are acting as critical catalysts for market growth, encouraging manufacturers to invest in research and development for next-generation safety solutions.

Manufacturers are also exploring the use of sustainable materials and more ergonomic designs to align with broader industry trends toward environmental responsibility and passenger well-being. The aftermarket segment is experiencing robust growth as airlines prioritize maintenance, repair, and overhaul (MRO) services to extend the lifespan of their assets and comply with evolving safety standards. This dual focus on new installations and aftermarket upgrades creates a dynamic landscape where innovation and compliance intersect, driving the overall market forward while addressing contemporary challenges in aviation safety and performance.

- Emphasis on lightweight, high-strength materials such as advanced composites and specialized polyesters for fuel efficiency and reduced operational costs.

- Integration of smart technologies, including sensor-based monitoring for seat belt usage, tension, and impact detection, enhancing in-flight safety protocols.

- Growing demand for enhanced ergonomics and comfort features, such as improved buckle designs and adjustable restraint systems, particularly in premium cabins.

- Increased adoption of modular and customizable seat belt solutions to cater to diverse aircraft types and cabin configurations, offering greater flexibility to aircraft manufacturers and airlines.

- Stringent and evolving global aviation safety regulations continuously push for higher performance standards and drive product innovation and replacement cycles.

- Expansion of global aircraft fleet, driven by rising air passenger traffic and the need for fleet modernization, directly fuels demand for new seat belt installations.

AI Impact Analysis on Aviation Seat Belt

The influence of Artificial Intelligence (AI) on the aviation seat belt market is primarily indirect, focusing on optimizing design, manufacturing processes, and predictive maintenance rather than direct integration into the seat belt mechanism itself. Users frequently inquire about how AI can contribute to enhanced safety, efficiency, and material innovation within this critical component sector. AI algorithms are being leveraged for advanced simulations during the design phase, allowing engineers to test a multitude of scenarios for crashworthiness, ergonomic comfort, and material stress under various conditions, thereby accelerating product development cycles and enhancing safety integrity. This capability minimizes the need for costly physical prototypes and provides deeper insights into product performance.

Furthermore, AI-driven analytics play a crucial role in the manufacturing process, optimizing production lines for precision, quality control, and identifying potential defects before they escalate. Predictive maintenance, another significant application, utilizes AI to analyze data from in-service components, including seat belt systems, to forecast potential failures or maintenance requirements. This proactive approach ensures operational reliability, reduces unexpected downtimes, and enhances overall aircraft safety by ensuring components are serviced or replaced optimally. While AI is not expected to be embedded within the seat belt itself, its transformative impact on the surrounding ecosystem of design, production, and maintenance is substantial, leading to safer, more efficient, and potentially more cost-effective aviation seat belt solutions.

- Optimization of seat belt design through AI-powered simulations, enhancing crashworthiness and ergonomic performance with reduced prototyping costs and time.

- Predictive maintenance analytics for seat belt components, leveraging AI to forecast wear and tear, ensuring timely replacements and maximizing operational safety and reliability.

- Quality control in manufacturing via AI vision systems and data analytics, identifying defects and ensuring compliance with stringent aviation standards during production.

- Supply chain optimization using AI, improving inventory management and logistics for seat belt components, thereby enhancing production efficiency and reducing lead times.

- Data-driven insights from in-flight performance monitoring (not directly from seat belt, but related cabin safety systems) informing future seat belt design improvements.

Key Takeaways Aviation Seat Belt Market Size & Forecast

The aviation seat belt market is set for consistent growth, driven by an unwavering commitment to safety, continuous advancements in material science, and the expanding global air travel industry. A primary insight reveals that stringent international and national aviation safety regulations serve as the fundamental backbone, consistently pushing for product innovation, upgrades, and scheduled replacements. This regulatory environment ensures a baseline demand that is further amplified by the ongoing modernization of global aircraft fleets, where older aircraft are being replaced or retrofitted with newer, more compliant, and often more technologically advanced seat belt systems. The projected growth underscores the essential and non-negotiable nature of seat belts as critical safety components.

Furthermore, the market's trajectory is also influenced by increasing passenger expectations for comfort and enhanced safety features, particularly within premium travel segments. This has spurred manufacturers to invest in ergonomic designs, advanced buckle mechanisms, and lighter, more durable materials that contribute to both safety and passenger experience. The aftermarket segment represents a significant revenue stream, driven by maintenance, repair, and overhaul (MRO) activities that are crucial for maintaining fleet airworthiness. Overall, the market showcases resilience and steady expansion, supported by a confluence of regulatory mandates, technological innovation, and an ever-growing demand for air travel globally.

- The market exhibits stable growth, primarily propelled by global air traffic expansion and the imperative for enhanced passenger safety standards.

- Regulatory compliance is a dominant force, necessitating continuous innovation and mandating periodic upgrades and replacements of seat belt systems across fleets.

- Technological advancements in materials, such as lightweight and high-strength fabrics, are crucial for meeting both safety requirements and aircraft performance goals.

- Both original equipment manufacturers (OEMs) and the aftermarket segment contribute significantly to market revenue, with MRO services playing a critical role in sustained demand.

- The Asia Pacific region is anticipated to be a key growth hub, driven by robust fleet expansion and increasing air passenger volumes.

Aviation Seat Belt Market Drivers Analysis

The aviation seat belt market is significantly influenced by several key drivers that ensure its steady expansion and continuous innovation. Foremost among these is the escalating demand for air travel globally, which directly translates into an increasing number of aircraft in service and a corresponding need for new seat belt installations and replacements. This growth in air traffic, particularly in emerging economies, fuels both the OEM and aftermarket segments. Coupled with this, stringent global aviation safety regulations, enforced by bodies such as the Federal Aviation Administration (FAA) and the European Union Aviation Safety Agency (EASA), mandate the use of certified and often technologically updated seat belts, compelling airlines and aircraft manufacturers to adopt the latest safety standards.

Moreover, the ongoing modernization and expansion of commercial and private aircraft fleets worldwide drive demand. Airlines are either upgrading existing aircraft with advanced safety features, including new seat belt systems, or acquiring new, larger capacity aircraft that require full installations. Passenger comfort and experience are also emerging as significant drivers, particularly in competitive markets. Manufacturers are responding by designing more ergonomic and user-friendly seat belts that enhance the overall travel experience, especially in premium cabin configurations. These synergistic factors collectively underscore the robust growth trajectory of the aviation seat belt market, as safety, compliance, and passenger satisfaction remain paramount.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Air Passenger Traffic Growth | +1.5% | Asia Pacific, North America, Europe | Short to Long-term |

| Stringent Aviation Safety Regulations | +1.2% | Global (FAA, EASA, CAAC) | Ongoing |

| Aircraft Fleet Modernization & Expansion | +1.3% | North America, Europe, Asia Pacific | Medium to Long-term |

| Technological Advancements in Materials & Design | +0.8% | Global | Medium-term |

Aviation Seat Belt Market Restraints Analysis

Despite its steady growth, the aviation seat belt market faces several notable restraints that can temper its expansion. One significant factor is the high cost associated with research and development (R&D), testing, and certification of new seat belt systems. Meeting the rigorous safety standards set by aviation authorities requires substantial investment and a prolonged approval process, which can deter smaller players and slow down the adoption of innovative designs. This extended lifecycle of product development means that product cycles are often long, and technological upgrades are not as frequent or rapid as in other industries, leading to slower market dynamism.

Another restraint involves the intense competition among a relatively limited number of established manufacturers. This competition often leads to price pressures, impacting profit margins, especially for standard seat belt offerings. Furthermore, the aviation industry, in general, is highly sensitive to global economic conditions. Economic downturns or geopolitical instabilities can significantly impact air travel demand, leading to reduced aircraft orders or delayed fleet modernizations, which subsequently diminishes demand for new seat belts. The supply chain for specialized materials and components can also pose a restraint, with potential disruptions or cost fluctuations affecting production and overall market stability. These elements necessitate strategic planning and resilience from market participants to navigate the challenging operational landscape.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Research & Development (R&D) and Certification Costs | -0.9% | Global | Ongoing |

| Long Product Lifecycle and Replacement Cycles | -0.7% | Global | Long-term |

| Intense Competition Among Established Players | -0.5% | Global | Ongoing |

| Sensitivity to Global Economic Fluctuations | -1.0% | Global | Short to Medium-term |

Aviation Seat Belt Market Opportunities Analysis

The aviation seat belt market is replete with opportunities for growth and innovation, particularly in areas focusing on advanced materials and enhanced functionality. A significant opportunity lies in the development and adoption of ultra-lightweight and sustainable materials. As airlines continuously seek to reduce aircraft weight for fuel efficiency and environmental compliance, there is a strong incentive for manufacturers to innovate with materials like advanced composites, recycled fibers, or bio-based polymers that maintain or even exceed current safety standards while offering a weight advantage. This pursuit of lighter solutions aligns with the broader aviation industry's sustainability goals and can open new avenues for product differentiation.

Another promising area involves the integration of smart technologies into seat belt systems. While direct AI control might be limited, incorporating sensors for real-time monitoring of seat belt status (e.g., fastened/unfastened, tension, impact forces) could provide valuable data for cabin safety, emergency response, and predictive maintenance. Furthermore, the expansion of the aftermarket segment, driven by the increasing average age of aircraft fleets and the continuous need for maintenance, repair, and overhaul (MRO) services, presents a robust opportunity for providers of spare parts, upgrades, and customization services. Emerging markets, particularly in Asia Pacific and Latin America, with their rapidly growing air travel sectors and corresponding fleet expansion, also offer substantial opportunities for both new installations and aftermarket penetration. Customization and personalization of seat belt designs, especially for business jets and first/business class cabins, represent a niche but growing opportunity for premium offerings.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Lightweight & Sustainable Materials | +1.1% | Global | Medium to Long-term |

| Integration of Smart Features & Sensors for Enhanced Safety | +1.0% | North America, Europe | Medium-term |

| Growth in Aftermarket Services (MRO) & Upgrades | +1.2% | Global | Long-term |

| Expansion into Emerging Aviation Markets | +0.9% | Asia Pacific, Latin America | Medium to Long-term |

Aviation Seat Belt Market Challenges Impact Analysis

The aviation seat belt market navigates several significant challenges that can influence its growth trajectory and operational efficiency. One primary hurdle is the complex and constantly evolving regulatory landscape. Compliance with diverse and stringent international and national aviation safety standards (such as those from FAA, EASA, and ICAO) requires continuous adaptation, extensive testing, and costly certification processes. Any changes to these regulations can necessitate significant redesigns and re-certifications, leading to increased expenses and delays for manufacturers. Furthermore, ensuring intellectual property protection for innovative designs and materials is crucial, as counterfeiting and unauthorized reproduction pose risks to brand integrity and safety standards, especially in the aftermarket.

Economic volatility also presents a substantial challenge. The aviation industry is highly susceptible to global economic downturns, geopolitical tensions, and unforeseen events (e.g., pandemics). Such factors can lead to reduced air travel, deferred aircraft purchases, or scaled-back MRO budgets, directly impacting the demand for seat belts. Supply chain disruptions, often stemming from geopolitical events, natural disasters, or raw material scarcity, represent another critical challenge. The reliance on specialized materials and components means that manufacturers must navigate complex global supply networks, and any interruption can significantly affect production schedules and costs. Lastly, the need to balance continuous innovation with cost-effectiveness remains a persistent challenge, as airlines and aircraft manufacturers consistently seek advanced solutions at competitive prices, pushing manufacturers to optimize efficiency without compromising safety or quality.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complex & Evolving Regulatory Compliance | -0.8% | Global | Ongoing |

| Economic Volatility & Geopolitical Instability | -1.1% | Global | Short to Medium-term |

| Supply Chain Disruptions for Specialized Materials | -0.9% | Global | Short-term |

| Counterfeiting and Intellectual Property Protection | -0.6% | Global | Ongoing |

Aviation Seat Belt Market - Updated Report Scope

This comprehensive market research report delves into the intricate dynamics of the global Aviation Seat Belt Market, providing an in-depth analysis of its current size, historical performance, and future growth projections from 2025 to 2033. The report meticulously examines key market trends, significant drivers, restraining factors, emerging opportunities, and critical challenges that shape the industry landscape. It offers a detailed segmentation analysis across various product types, aircraft types, sales channels, materials, and applications, providing granular insights into market distribution and adoption patterns. Furthermore, the report features a robust regional analysis, highlighting key country-level markets and their respective contributions to the overall market growth. A dedicated section profiles leading market players, offering competitive intelligence and strategic insights. The objective is to equip stakeholders with actionable intelligence for informed decision-making, strategic planning, and competitive positioning within the aviation safety components sector.

| Report Attributes | Report Details | ||||||

|---|---|---|---|---|---|---|---|

| Base Year | 2024 | ||||||

| Historical Year | 2019 to 2023 | ||||||

| Forecast Year | 2025 - 2033 | ||||||

| Market Size in 2025 | USD 520 Million | ||||||

| Market Forecast in 2033 | USD 805 Million | ||||||

| Growth Rate | 5.5% | ||||||

| Number of Pages | 255 | ||||||

| Key Trends |

| ||||||

| Segments Covered |

|