Automotive Water Pump Market

Automotive Water Pump Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709635 | Last Updated : December 12, 2025 |

Format : ![]()

![]()

![]()

![]()

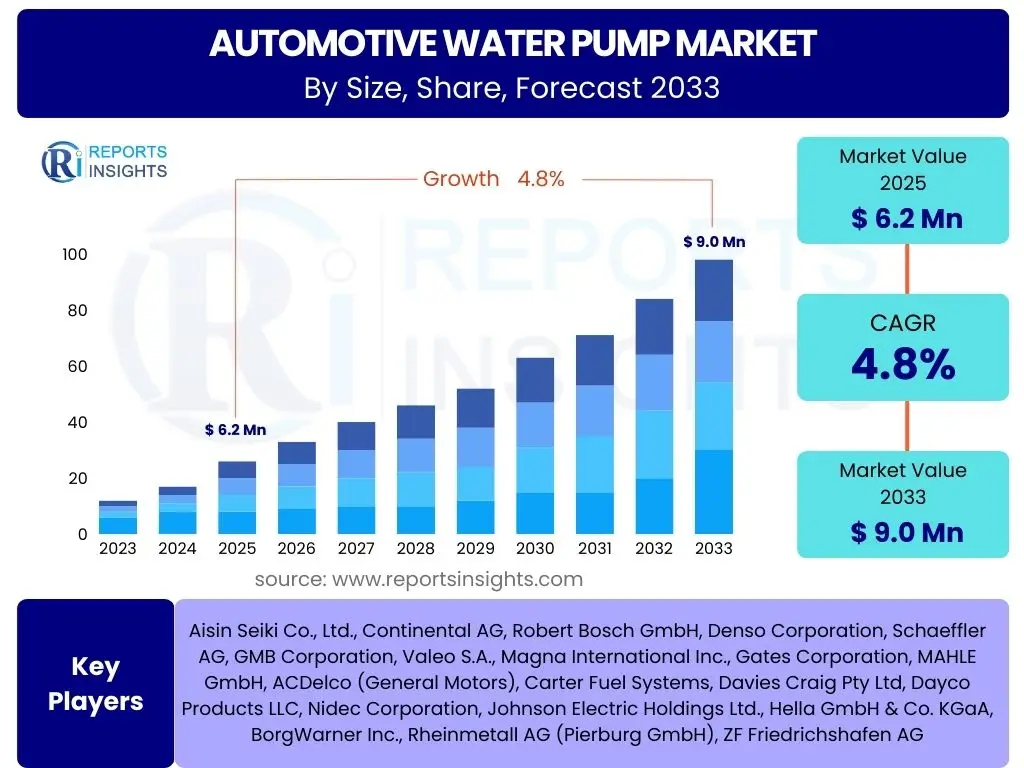

Automotive Water Pump Market Size

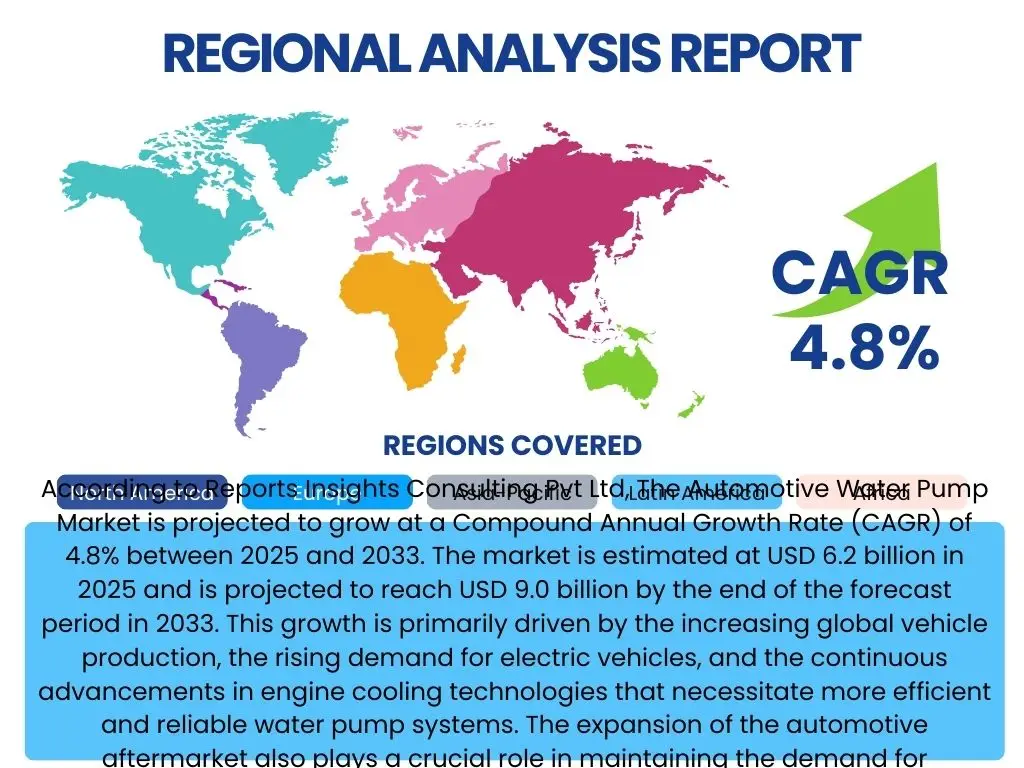

According to Reports Insights Consulting Pvt Ltd, The Automotive Water Pump Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.8% between 2025 and 2033. The market is estimated at USD 6.2 billion in 2025 and is projected to reach USD 9.0 billion by the end of the forecast period in 2033. This growth is primarily driven by the increasing global vehicle production, the rising demand for electric vehicles, and the continuous advancements in engine cooling technologies that necessitate more efficient and reliable water pump systems. The expansion of the automotive aftermarket also plays a crucial role in maintaining the demand for replacement and upgrade components.

The market's expansion is further supported by the stringent emission regulations and fuel efficiency standards imposed by governments worldwide, pushing automotive manufacturers to adopt advanced water pump designs such as electric and variable flow pumps. These sophisticated components contribute to better thermal management, which is critical for both internal combustion engines and electric powertrains. The global shift towards sustainable mobility solutions ensures a sustained demand for innovative water pump technologies capable of optimizing vehicle performance and reducing environmental impact across various vehicle segments.

Key Automotive Water Pump Market Trends & Insights

The automotive water pump market is undergoing significant transformations driven by technological advancements and evolving vehicle architectures, particularly the shift towards electric powertrains. User inquiries frequently highlight a keen interest in how electrification, material innovations, and smart system integration are reshaping the market landscape. There is a clear focus on the increasing adoption of electric water pumps due to their efficiency and control capabilities, alongside the development of lightweight and durable materials designed to enhance component longevity and performance. Furthermore, the integration of smart features and connectivity into water pump systems is emerging as a critical trend, promising improved vehicle diagnostics and predictive maintenance functionalities.

Beyond electrification, trends also emphasize the importance of advanced thermal management systems, which are vital for optimizing the performance and lifespan of both traditional combustion engines and battery packs in electric vehicles. This necessitates water pumps that can offer precise coolant flow control and adapt to varying operational demands. The aftermarket segment also exhibits a trend towards high-quality, durable replacement parts, driven by an aging global vehicle fleet and consumer preference for reliability. These trends collectively point towards a market that is becoming increasingly sophisticated, environmentally conscious, and technologically integrated.

- Shift towards Electric Water Pumps (EWPs) for enhanced efficiency and precise control.

- Integration of variable flow technology to optimize engine temperature and fuel economy.

- Development of lightweight materials (e.g., advanced plastics, aluminum alloys) for improved vehicle performance and reduced emissions.

- Increased focus on thermal management systems, particularly for electric vehicle battery cooling.

- Adoption of smart water pump technologies with diagnostic capabilities and connectivity.

- Growing demand for robust and reliable pumps in the automotive aftermarket.

- Emphasis on modular designs to facilitate easier integration and servicing.

AI Impact Analysis on Automotive Water Pump

The impact of Artificial Intelligence (AI) on the automotive water pump market is a burgeoning area of interest, with users frequently querying its potential applications in design, manufacturing, and operational optimization. AI is seen as a transformative tool that can enhance the performance, reliability, and efficiency of water pump systems. Specifically, AI-driven simulations and generative design are revolutionizing the product development cycle, allowing engineers to create optimized pump geometries and material compositions that were previously unattainable through traditional methods. This leads to the development of more durable, lighter, and highly efficient water pumps tailored to specific vehicle requirements.

Furthermore, AI is increasingly being integrated into the manufacturing processes of automotive water pumps. Predictive analytics, powered by AI, can monitor production lines to identify potential failures, optimize machine performance, and reduce waste, thereby improving overall manufacturing efficiency and product quality. In terms of operational impact, AI can enable smart water pumps that utilize sensor data to predict maintenance needs, dynamically adjust flow rates based on real-time driving conditions, and communicate with other vehicle systems for holistic thermal management. This leads to enhanced vehicle performance, extended component lifespan, and proactive servicing, moving towards a more intelligent and responsive automotive ecosystem.

- AI-powered generative design for optimizing water pump geometry and material selection.

- Predictive maintenance algorithms for forecasting pump failures and scheduling proactive servicing.

- Enhanced manufacturing process optimization through AI-driven quality control and anomaly detection.

- Real-time adaptive control of electric water pumps for optimal thermal management based on driving conditions.

- Data analytics for performance monitoring and continuous improvement in pump design and operation.

- Development of smart water pumps with integrated AI capabilities for self-diagnosis and communication.

Key Takeaways Automotive Water Pump Market Size & Forecast

Analysis of user questions regarding the automotive water pump market size and forecast reveals a strong emphasis on understanding the primary growth drivers, the influence of evolving automotive technologies, and the long-term outlook for investment. A key insight is that the market's trajectory is heavily influenced by the dual forces of increasing global vehicle production and the accelerating adoption of electric vehicles. While traditional mechanical pumps will continue to serve a substantial portion of the internal combustion engine (ICE) market, electric water pumps are emerging as the dominant growth segment due to their necessity in advanced thermal management for EVs and their superior efficiency in modern ICE vehicles.

Furthermore, the forecast suggests a resilient market, driven by the indispensable role of water pumps in ensuring optimal engine and battery performance, irrespective of powertrain type. The aftermarket segment is expected to remain robust, offering stable revenue streams. Strategic investments in research and development, particularly in lightweight materials, advanced electronics, and smart control systems, are critical for companies aiming to capitalize on the market's evolving demands. The overall outlook points towards a dynamic market characterized by technological innovation, sustained demand across diverse vehicle types, and a continued focus on efficiency and reliability.

- Sustained market growth driven by global vehicle production and electric vehicle proliferation.

- Electric water pumps are a key growth accelerator, integral to EV thermal management and ICE efficiency.

- Aftermarket demand for replacement parts ensures market stability and consistent revenue.

- Technological innovation in materials and control systems is paramount for market competitiveness.

- Asia Pacific and North America are projected to be significant growth regions due to manufacturing hubs and EV adoption.

- Emphasis on fuel efficiency and emissions reduction drives the adoption of advanced water pump technologies.

Automotive Water Pump Market Drivers Analysis

The automotive water pump market is propelled by several robust drivers, fundamentally linked to the global expansion of the automotive industry and the continuous evolution of vehicle technology. Increasing vehicle production worldwide, particularly in emerging economies, directly translates to a higher demand for both original equipment (OE) and aftermarket water pumps. Moreover, stringent environmental regulations focused on reducing emissions and improving fuel efficiency compel manufacturers to integrate more sophisticated and efficient water pump systems, such as electric and variable flow pumps, into their designs. This regulatory push necessitates components that can precisely manage engine temperatures, optimizing combustion and minimizing energy waste. The growing demand for electric vehicles also significantly contributes, as EVs require dedicated thermal management systems for batteries and power electronics, often relying on multiple electric water pumps.

Furthermore, the aging global vehicle fleet drives consistent demand in the aftermarket segment, where water pumps are critical replacement parts due to wear and tear. Advancements in engine technology, including turbocharging and direct injection, generate higher engine temperatures, requiring more robust and effective cooling solutions. These technological shifts, combined with consumer expectations for enhanced vehicle performance and reliability, create a sustained and expanding need for innovative water pump solutions. The continuous cycle of vehicle innovation and replacement ensures a resilient and growing market for these essential components.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Global Vehicle Production | +1.5% | Asia Pacific, North America, Europe | 2025-2033 |

| Rise in Electric Vehicle (EV) Adoption | +1.2% | China, Europe, North America | 2025-2033 |

| Stringent Emission & Fuel Efficiency Regulations | +0.8% | Europe, North America, Japan | 2025-2033 |

| Advancements in Engine Thermal Management | +0.7% | Global | 2025-2033 |

| Robust Automotive Aftermarket Demand | +0.6% | North America, Europe, Asia Pacific | 2025-2033 |

Automotive Water Pump Market Restraints Analysis

Despite the positive growth trajectory, the automotive water pump market faces several notable restraints that could temper its expansion. One significant challenge is the intense price competition, particularly in the aftermarket segment, which often leads to downward pressure on profit margins for manufacturers. The presence of numerous regional and local players, coupled with a focus on cost-efficiency by vehicle manufacturers, intensifies this competitive landscape. Another restraint stems from the increasing complexity of modern water pump designs, especially electric and variable flow pumps, which require sophisticated manufacturing processes and higher material costs. This complexity can translate into elevated production expenses, potentially limiting broader adoption or increasing end-user costs.

Furthermore, the automotive industry's susceptibility to economic downturns and geopolitical instabilities can impact vehicle sales and, consequently, the demand for water pumps. Supply chain disruptions, as experienced recently, can lead to material shortages and increased lead times, affecting production schedules and market supply. The rapid pace of technological change, while a driver of innovation, can also be a restraint for companies unable to invest sufficiently in research and development, potentially leading to market obsolescence if they fail to adapt to new powertrain requirements. Lastly, the long product lifecycle of traditional internal combustion engine vehicles, combined with the durability of existing water pump technologies, can lead to slower replacement cycles in certain segments, impacting aftermarket sales volumes.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Price Competition & Margin Pressure | -0.9% | Global, particularly Asia Pacific | 2025-2033 |

| High Research & Development Costs | -0.7% | Global | 2025-2033 |

| Supply Chain Disruptions and Material Price Volatility | -0.6% | Global | Short to Mid-term (2025-2028) |

| Technological Obsolescence of Traditional Pumps | -0.5% | Europe, North America | Mid to Long-term (2028-2033) |

| Economic Volatility Affecting Vehicle Sales | -0.4% | Global | Short-term (2025-2027) |

Automotive Water Pump Market Opportunities Analysis

Significant opportunities exist within the automotive water pump market for innovation and strategic growth, particularly driven by the evolving landscape of vehicle technology. One of the most prominent opportunities lies in the surging demand for electric water pumps (EWPs) as the global production and adoption of electric vehicles (EVs) accelerate. EWPs are crucial for precise thermal management of EV batteries, motors, and power electronics, representing a rapidly expanding segment with higher technological requirements and potentially better margins. Furthermore, the development of smart and connected water pumps, integrating sensors and diagnostic capabilities, offers a pathway to differentiate products and provide added value through predictive maintenance and enhanced vehicle reliability. This aligns with the broader automotive trend towards intelligent systems and autonomous driving capabilities.

Another compelling opportunity is the expansion into emerging markets, such as Southeast Asia, Latin America, and parts of Africa, where vehicle ownership is growing rapidly, and infrastructure development is creating new demands for both OE and aftermarket components. Strategic partnerships and collaborations with vehicle manufacturers and technology providers can unlock new product development avenues and market access. Moreover, the focus on sustainable manufacturing practices and the development of water pumps made from recyclable or lighter, more environmentally friendly materials present opportunities not only for compliance with regulations but also for brand differentiation and appeal to environmentally conscious consumers. The continuous need for more efficient and durable components across all vehicle types ensures a fertile ground for companies that can deliver innovative and cost-effective solutions.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand for Electric Water Pumps in EVs | +1.8% | Global, particularly China, Europe, North America | 2025-2033 |

| Development of Smart & Connected Water Pumps | +1.1% | Europe, North America, Japan | 2025-2033 |

| Expansion in Emerging Automotive Markets | +0.9% | Asia Pacific (excl. China), Latin America, MEA | 2025-2033 |

| Technological Advancements in Material Science | +0.7% | Global | 2025-2033 |

| Strategic Partnerships & Collaborations | +0.6% | Global | 2025-2033 |

Automotive Water Pump Market Challenges Impact Analysis

The automotive water pump market navigates several complex challenges that demand strategic foresight and adaptability from industry players. One significant challenge is the rapid technological evolution within the automotive sector, particularly the accelerating shift towards electric vehicles. While EVs offer new opportunities for electric water pumps, they simultaneously pose a long-term threat to the traditional mechanical water pump market for internal combustion engines. This transition requires substantial investment in R&D to develop entirely new product lines and adapt manufacturing processes, creating financial strain for companies heavily invested in legacy technologies. Managing this transition effectively without alienating existing revenue streams is a delicate balance.

Another challenge stems from the increasing complexity of vehicle architectures and thermal management systems. Modern engines and EV powertrains demand highly integrated and intelligent cooling solutions, which means water pumps are no longer standalone components but critical parts of a broader, interconnected system. This requires manufacturers to possess advanced engineering capabilities and collaborate closely with vehicle OEMs from the early design stages, increasing the barriers to entry and the cost of product development. Furthermore, navigating diverse and stringent global regulatory environments, particularly concerning emissions and vehicle safety, adds another layer of complexity. Maintaining quality and durability standards while managing cost pressures in a highly competitive market remains a persistent challenge, alongside the industry's vulnerability to global economic fluctuations and supply chain vulnerabilities.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Transition from ICE to EV Powertrains | -1.1% | Global, particularly developed markets | Mid to Long-term (2028-2033) |

| Integration Complexity with Advanced Vehicle Systems | -0.8% | Global | 2025-2033 |

| Stringent Regulatory Compliance | -0.7% | Europe, North America, China | 2025-2033 |

| Talent Shortage in Advanced Manufacturing & R&D | -0.6% | Global | 2025-2033 |

| Counterfeit Products in Aftermarket | -0.5% | Asia Pacific, Latin America | 2025-2033 |

Automotive Water Pump Market - Updated Report Scope

This comprehensive market insights report provides an in-depth analysis of the global Automotive Water Pump Market, offering a detailed examination of market size, growth drivers, restraints, opportunities, and challenges across various segments and key regions. The scope extends to both original equipment (OE) and aftermarket segments, covering mechanical, electric, and variable flow pump types for passenger cars, commercial vehicles, and electric vehicles. The report incorporates the latest technological advancements, regulatory impacts, and the influence of emerging trends such as AI integration and sustainable manufacturing practices, providing a holistic view of the market landscape and future projections.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 6.2 Billion |

| Market Forecast in 2033 | USD 9.0 Billion |

| Growth Rate | 4.8% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Aisin Seiki Co., Ltd., Continental AG, Robert Bosch GmbH, Denso Corporation, Schaeffler AG, GMB Corporation, Valeo S.A., Magna International Inc., Gates Corporation, MAHLE GmbH, ACDelco (General Motors), Carter Fuel Systems, Davies Craig Pty Ltd, Dayco Products LLC, Nidec Corporation, Johnson Electric Holdings Ltd., Hella GmbH & Co. KGaA, BorgWarner Inc., Rheinmetall AG (Pierburg GmbH), ZF Friedrichshafen AG |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The automotive water pump market is comprehensively segmented to provide a granular understanding of its diverse components and drivers. This segmentation allows for precise analysis of market dynamics across different technologies, vehicle types, materials, and sales channels, reflecting the multifaceted nature of the automotive industry. By examining these distinct segments, stakeholders can identify specific growth opportunities, assess competitive landscapes, and formulate targeted strategies that align with evolving market demands and technological shifts. The primary segmentation categories highlight the transition from traditional mechanical systems to more advanced electric and variable flow solutions, alongside the profound impact of electric vehicle proliferation.

Further granularity is achieved by considering the materials used in water pump construction, which directly influences performance, weight, and cost, as well as the critical distinction between original equipment and aftermarket sales. Each segment exhibits unique growth patterns and competitive dynamics, influenced by factors such as manufacturing trends, consumer preferences, regulatory frameworks, and regional economic conditions. This structured approach to segmentation ensures a detailed and actionable overview of the market's various dimensions, critical for informed decision-making and strategic planning.

- By Type:

- Mechanical Water Pump: Traditional, engine-driven pumps, primarily for ICE vehicles.

- Electric Water Pump: Electronically controlled pumps, offering precise flow and efficiency, crucial for EVs and advanced ICEs.

- Variable Flow Water Pump: Pumps that adjust flow based on cooling needs, optimizing engine temperature and fuel economy.

- By Vehicle Type:

- Passenger Cars: Covering compact, mid-size, luxury, and SUVs, representing the largest volume segment.

- Commercial Vehicles: Including Light Commercial Vehicles (LCV) and Heavy Commercial Vehicles (HCV).

- Electric Vehicles: Specifically Battery Electric Vehicles (BEV), Hybrid Electric Vehicles (HEV), and Plug-in Hybrid Electric Vehicles (PHEV), driving demand for EWPs.

- By Material:

- Cast Iron: Traditional, robust, and cost-effective material.

- Aluminum: Lighter weight, better heat dissipation, increasingly preferred.

- Plastic Composites: Ultra-lightweight, corrosion-resistant, used in specialized applications.

- By Sales Channel:

- Original Equipment Manufacturer (OEM): Pumps supplied directly to vehicle manufacturers for new vehicle assembly.

- Aftermarket: Replacement pumps sold through various channels for vehicle maintenance and repair.

Regional Highlights

- Asia Pacific: Emerging as the dominant market due to high vehicle production volumes, particularly in China and India, and rapid adoption of electric vehicles. Significant investments in automotive manufacturing and increasing disposable incomes contribute to robust growth in both OEM and aftermarket segments.

- Europe: A mature market characterized by stringent emission regulations and a strong push towards electrification. Innovation in electric and variable flow pumps is high, driven by the presence of leading automotive manufacturers and a focus on advanced thermal management systems.

- North America: Experiences steady growth driven by consistent vehicle sales, a strong aftermarket presence, and increasing adoption of SUVs and light trucks. The accelerating transition to electric vehicles is a key factor influencing the demand for advanced water pump technologies.

- Latin America: Expected to show moderate growth with increasing vehicle parc and improving economic conditions. The aftermarket segment plays a crucial role due to an aging vehicle fleet and demand for cost-effective replacement parts.

- Middle East and Africa (MEA): A growing market influenced by rising vehicle sales and infrastructure development, particularly in GCC countries and South Africa. Demand is primarily driven by the need for robust and reliable components suitable for challenging climatic conditions.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Automotive Water Pump Market.- Aisin Seiki Co., Ltd.

- Continental AG

- Robert Bosch GmbH

- Denso Corporation

- Schaeffler AG

- GMB Corporation

- Valeo S.A.

- Magna International Inc.

- Gates Corporation

- MAHLE GmbH

- ACDelco (General Motors)

- Carter Fuel Systems

- Davies Craig Pty Ltd

- Dayco Products LLC

- Nidec Corporation

- Johnson Electric Holdings Ltd.

- Hella GmbH & Co. KGaA

- BorgWarner Inc.

- Rheinmetall AG (Pierburg GmbH)

- ZF Friedrichshafen AG

Frequently Asked Questions

What is an automotive water pump and what is its primary function?

An automotive water pump is a critical component of a vehicle's cooling system responsible for circulating coolant (a mixture of antifreeze and water) through the engine block, cylinder head, radiator, and heater core. Its primary function is to dissipate heat generated by the engine during combustion, preventing overheating and maintaining optimal operating temperature for efficient performance and longevity of engine components.

How is the rise of electric vehicles impacting the demand for automotive water pumps?

The rise of electric vehicles (EVs) is significantly shifting the demand from traditional mechanical water pumps to electric water pumps (EWPs). While EVs do not have internal combustion engines, they require advanced thermal management systems for their batteries, electric motors, and power electronics. EWPs offer precise and on-demand cooling, crucial for optimizing EV performance, range, and battery lifespan, thereby driving growth in the electric water pump segment.

What are the key technological trends in the automotive water pump market?

Key technological trends include the increasing adoption of electric and variable flow water pumps for enhanced efficiency and control, the use of lightweight materials (such as aluminum and plastic composites) to reduce vehicle weight, and the integration of smart features for predictive maintenance and real-time performance monitoring. There is also a strong focus on developing pumps optimized for advanced thermal management systems in both ICE and EV platforms.

Which regions are expected to drive the growth of the automotive water pump market?

Asia Pacific is projected to be the leading growth region, primarily due to high vehicle production volumes, rapid industrialization, and increasing adoption of electric vehicles in countries like China and India. Europe and North America are also significant contributors, driven by stringent emission regulations, technological innovation, and a robust aftermarket segment.

What challenges does the automotive water pump market face?

The market faces challenges such as intense price competition, high research and development costs for advanced pump technologies, and the complexities associated with integrating new pump designs into evolving vehicle architectures. The transition from internal combustion engine vehicles to electric vehicles also presents a long-term challenge for manufacturers heavily invested in traditional mechanical pump technologies, requiring substantial adaptation and innovation.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted