Automotive Tinting Film Market

Automotive Tinting Film Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702445 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

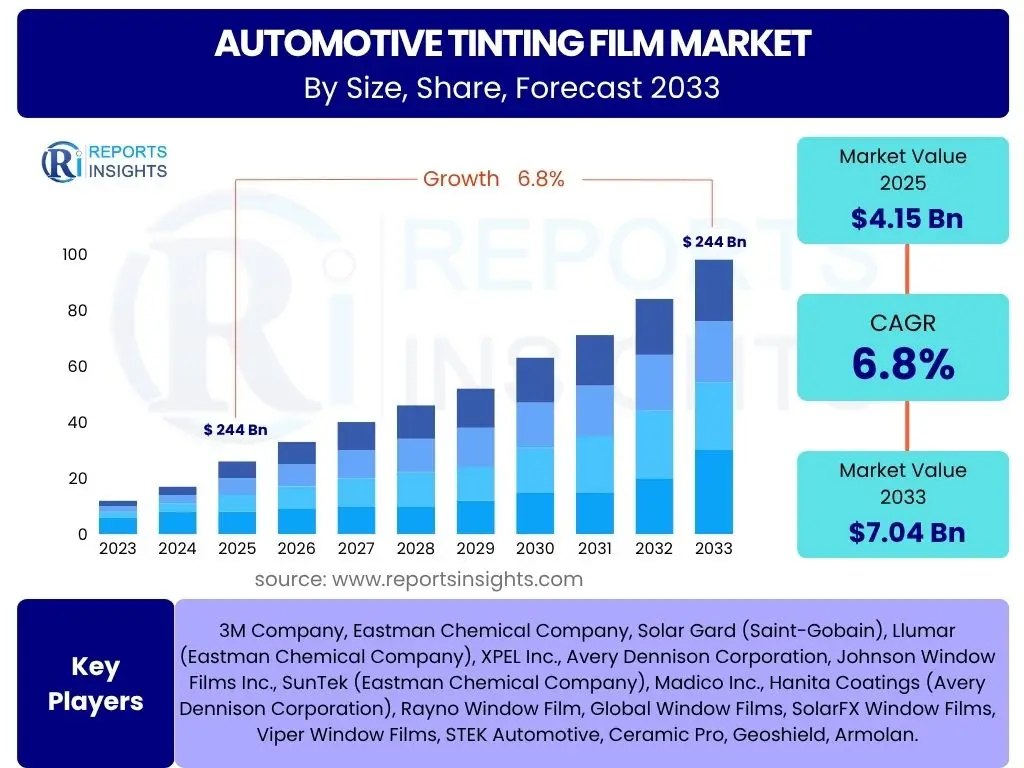

Automotive Tinting Film Market Size

According to Reports Insights Consulting Pvt Ltd, The Automotive Tinting Film Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 4.15 billion in 2025 and is projected to reach USD 7.04 billion by the end of the forecast period in 2033.

Key Automotive Tinting Film Market Trends & Insights

The automotive tinting film market is undergoing significant transformation, driven by evolving consumer preferences and technological advancements. A primary area of interest for users often revolves around the emergence of innovative film types, such as ceramic and smart films, which offer superior performance in heat rejection, UV protection, and durability compared to traditional dyed or metallic films. Consumers are increasingly seeking value beyond mere aesthetics, prioritizing functional benefits like energy efficiency within the vehicle and enhanced safety from shattered glass. The trend towards customization also plays a crucial role, with vehicle owners demanding a wider array of shades and finishes to personalize their cars.

Furthermore, the market is witnessing a surge in demand for DIY (Do-It-Yourself) tinting kits, particularly in the aftermarket segment, propelled by cost-effectiveness and accessibility. However, this trend brings concerns regarding professional installation quality and compliance with local tinting regulations. Sustainability is another emerging theme, with manufacturers exploring eco-friendly materials and production processes to align with global environmental initiatives and consumer demand for green products. The convergence of these trends indicates a dynamic market prioritizing performance, personalization, and environmental consciousness, shaping both product development and consumer purchasing decisions.

- Shift towards advanced film technologies (ceramic, carbon, crystalline) for superior performance.

- Increased consumer demand for functional benefits beyond aesthetics, including UV and heat rejection.

- Growing trend of vehicle customization and personalization drives diverse film options.

- Rise of the DIY tinting film segment, particularly in the aftermarket.

- Emphasis on sustainable and eco-friendly manufacturing processes and materials.

- Integration of smart film technologies offering dynamic tinting capabilities.

- Expansion of application in commercial vehicles and public transport.

AI Impact Analysis on Automotive Tinting Film

Common user inquiries regarding the impact of AI on the automotive tinting film sector frequently explore how artificial intelligence can revolutionize various stages, from manufacturing to consumer experience. Users are keen to understand if AI can lead to more efficient production, enhance the quality and properties of tinting films, or even personalize the selection and installation process. There is a general expectation that AI could introduce a new level of precision and predictive capability, potentially addressing common industry challenges like material waste or inconsistent application. The overarching theme is one of curiosity about how a seemingly traditional industry can leverage cutting-edge AI to foster innovation and improve overall value.

AI's influence is anticipated to manifest primarily through optimization, automation, and data-driven insights. In manufacturing, AI algorithms can analyze vast datasets from production lines to predict equipment failures, optimize material usage, and ensure consistent product quality, thereby reducing waste and enhancing efficiency. For research and development, AI can accelerate the discovery of novel materials with improved properties, such as enhanced thermal insulation or optical clarity, by simulating molecular structures and predicting performance outcomes. Moreover, AI-powered tools can assist in supply chain management, demand forecasting, and even in customer interaction, offering personalized recommendations based on vehicle type, regional climate, and aesthetic preferences, ultimately streamlining operations and elevating the customer journey in the automotive tinting film market.

- Manufacturing Optimization: AI-driven predictive maintenance and quality control for film production lines, minimizing defects and waste.

- Material Innovation: AI algorithms accelerating the discovery and development of new film compositions with enhanced properties (e.g., durability, heat rejection, transparency).

- Personalized Customer Experience: AI-powered recommendation engines guiding consumers to ideal film types based on their needs, vehicle, and local regulations.

- Supply Chain Efficiency: AI for demand forecasting, inventory management, and logistics optimization, ensuring timely availability of film products.

- Automated Cutting and Installation: AI-assisted precision cutting machines and potentially augmented reality (AR) tools to aid installers, reducing errors and improving application quality.

Key Takeaways Automotive Tinting Film Market Size & Forecast

Users frequently inquire about the most critical insights derived from the market size and forecast for automotive tinting films, seeking a concise understanding of where the market is headed and the underlying factors driving its trajectory. The primary concern is often related to identifying the most lucrative segments, the impact of technological advancements on future growth, and the regional dynamics shaping market expansion. Stakeholders are keen to grasp the overarching narrative of market resilience and opportunity, particularly in the face of evolving regulatory landscapes and shifting consumer demands. The emphasis is on actionable intelligence that can inform strategic decision-making and investment priorities within this specialized automotive aftermarket segment.

The automotive tinting film market is poised for robust expansion, predominantly fueled by increasing consumer awareness regarding vehicle aesthetics, privacy, and the functional benefits of UV and heat protection. The aftermarket segment is expected to remain a dominant force, driven by vehicle customization trends and the aging global vehicle parc. Growth will be significantly influenced by advancements in film technology, particularly the adoption of ceramic and smart films, which offer premium performance attributes. While regulatory variations across regions present a nuanced challenge, they also create distinct opportunities for compliant and innovative product offerings. The Asia Pacific region is anticipated to emerge as a key growth engine due to rising disposable incomes, increasing vehicle sales, and a growing emphasis on comfort and luxury features in automobiles, signaling a promising outlook for the industry as a whole.

- The market exhibits steady growth driven by aesthetic appeal, privacy needs, and functional benefits like UV protection and heat rejection.

- Technological advancements, particularly in ceramic and smart films, are pivotal for future market expansion and premium segment growth.

- The aftermarket segment continues to be the largest contributor, propelled by vehicle customization and a growing installed base of vehicles.

- Asia Pacific is projected to be the fastest-growing region, owing to increasing vehicle ownership and rising consumer awareness.

- Compliance with diverse regional tinting regulations remains a critical factor influencing product development and market penetration.

- The industry is witnessing an ongoing shift towards high-performance and durable film solutions.

Automotive Tinting Film Market Drivers Analysis

The automotive tinting film market is significantly propelled by a confluence of factors, primarily centered around consumer demands for enhanced vehicle comfort, safety, and aesthetic personalization. The escalating global temperature and heightened awareness regarding the detrimental effects of UV radiation on vehicle interiors and occupants drive the adoption of films offering superior heat and UV rejection. This is further complemented by a growing desire for privacy and security among vehicle owners, particularly in urban environments. As disposable incomes rise across emerging economies, more consumers are willing to invest in aftermarket accessories that enhance their driving experience and protect their investment.

Technological advancements also play a crucial role, with manufacturers continuously innovating to produce films with better performance characteristics, such as improved clarity, durability, and signal friendliness (for GPS and mobile devices). The increasing sales of new vehicles globally, coupled with a robust aftermarket for vehicle upgrades and maintenance, provide a consistent demand base for tinting films. Moreover, specific regional trends, such as the increasing popularity of SUVs and luxury vehicles, often correlate with a higher propensity for tinting film adoption, contributing substantially to market expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for UV and Heat Protection | +1.5% | Global, particularly hot climates like MEA, APAC, Southern US | 2025-2033 (Long-term) |

| Rising Vehicle Customization and Aesthetics Trends | +1.2% | North America, Europe, parts of APAC | 2025-2033 (Long-term) |

| Growing Awareness of Privacy and Security Benefits | +0.8% | Global, especially urban areas and regions with higher crime rates | 2025-2030 (Mid-term) |

| Technological Advancements in Film Manufacturing | +1.0% | Global, driving premium segment growth | 2025-2033 (Long-term) |

| Increasing Global Vehicle Production and Sales | +0.7% | APAC (China, India), Latin America | 2025-2030 (Mid-term) |

Automotive Tinting Film Market Restraints Analysis

Despite significant growth drivers, the automotive tinting film market faces several restraints that could impede its expansion. One of the most prominent challenges is the varied and often stringent regulatory landscape concerning tint darkness and reflectivity across different countries and even within states or provinces. These regulations, primarily implemented for road safety and law enforcement visibility, can limit the permissible tint levels, thereby restricting consumer choices and market demand for darker films. Non-compliance can lead to legal penalties for both installers and vehicle owners, creating apprehension and a barrier to adoption for certain film types.

Another significant restraint is the prevalence of low-quality, inexpensive counterfeit products in the market. These products, often lacking proper UV protection, clarity, or durability, can damage the industry's reputation by delivering poor performance and short lifespans. Furthermore, the perceived high cost of professional installation, especially for premium-grade films, can deter price-sensitive consumers, pushing them towards cheaper, often inferior, DIY options or away from tinting altogether. Economic downturns affecting automotive sales or consumer discretionary spending can also temporarily dampen market growth, as tinting films are often considered a non-essential accessory.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Strict and Varied Tinting Regulations | -1.2% | Europe, parts of North America, specific Asian countries | 2025-2033 (Long-term) |

| Availability of Low-Quality/Counterfeit Products | -0.9% | Global, particularly emerging markets with less stringent quality control | 2025-2030 (Mid-term) |

| High Installation Costs for Premium Films | -0.6% | Global, affects price-sensitive consumer segments | 2025-2033 (Long-term) |

| Economic Volatility Impacting Automotive Sales | -0.5% | Global, varies by economic cycle | Short-term (cyclical) |

Automotive Tinting Film Market Opportunities Analysis

The automotive tinting film market is ripe with opportunities, primarily stemming from the continuous evolution of smart technologies and the expanding global automotive parc. The most significant opportunity lies in the development and proliferation of dynamic or smart films that can electronically adjust their transparency, offering unparalleled flexibility to drivers in adapting to varying light conditions and privacy needs while adhering to regulations. These advanced films present a premium segment with higher profit margins and significant growth potential as vehicle technology progresses towards more integrated and intelligent systems. Furthermore, increasing urbanization and a growing emphasis on personal safety provide a niche for security films that strengthen glass against breakage and smash-and-grab incidents, appealing to a broader consumer base concerned with crime prevention.

Emerging markets, particularly in Asia Pacific, Latin America, and the Middle East & Africa, represent substantial untapped potential. These regions are experiencing rapid economic growth, rising disposable incomes, and increasing vehicle ownership, leading to a burgeoning demand for automotive enhancements. Strategic partnerships between film manufacturers and original equipment manufacturers (OEMs) or large automotive aftermarket chains can facilitate broader market penetration and accelerate the adoption of advanced tinting solutions. Additionally, the increasing demand for energy-efficient solutions in vehicles, driven by environmental awareness and fuel cost concerns, creates an opportunity for films that offer superior thermal insulation, reducing the load on vehicle air conditioning systems and improving fuel economy. This combination of technological advancement, geographic expansion, and evolving consumer priorities signals a fertile ground for sustained market growth.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Dynamic and Smart Tinting Films | +1.8% | Global, high-end vehicle market, tech-savvy regions | 2027-2033 (Long-term) |

| Expansion in Emerging Economies (APAC, LATAM, MEA) | +1.5% | Asia Pacific (China, India), Latin America, Middle East & Africa | 2025-2033 (Long-term) |

| Increasing Demand for Safety and Security Films | +1.0% | Global, urban areas, regions with security concerns | 2025-2030 (Mid-term) |

| Strategic Partnerships with OEMs and Large Retail Chains | +0.9% | Global, particularly established automotive markets | 2025-2033 (Long-term) |

| Growing Focus on Vehicle Energy Efficiency | +0.7% | Global, driven by environmental regulations and fuel costs | 2025-2033 (Long-term) |

Automotive Tinting Film Market Challenges Impact Analysis

The automotive tinting film market faces several formidable challenges that could impact its trajectory. A significant hurdle is the constant battle against counterfeit products and the proliferation of low-quality films. These inferior alternatives not only dilute market value but also undermine consumer trust in the overall quality and benefits of tinting films, often leading to poor performance, premature degradation, and dissatisfaction. This issue is particularly acute in regions with less stringent intellectual property enforcement and quality control mechanisms. Another challenge lies in the dynamic and often inconsistent regulatory landscape regarding tint darkness and type. Compliance with varying local and national laws requires significant investment in product diversification and market-specific strategies, adding complexity for manufacturers and installers operating across multiple jurisdictions.

Furthermore, the availability of a skilled workforce for precise and proper film installation remains a persistent challenge. Improper installation can lead to bubbling, peeling, or uneven application, directly impacting the film's aesthetic appeal and functional performance, thus diminishing customer satisfaction and potentially deterring future installations. The rapid pace of technological change within the automotive industry, particularly with the advent of smart glass technologies, poses a long-term threat to traditional tinting films. While currently a niche, the increasing integration of factory-tinted or electronically dimmable glass in premium vehicles could eventually reduce the aftermarket demand for conventional films. Addressing these challenges requires concerted efforts in consumer education, quality assurance, regulatory advocacy, and continuous innovation to maintain market relevance.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Prevalence of Counterfeit and Low-Quality Films | -1.0% | Global, prominent in emerging markets | 2025-2033 (Long-term) |

| Lack of Skilled Professional Installers | -0.8% | Global, particularly affecting installation quality and consistency | 2025-2030 (Mid-term) |

| Evolving and Inconsistent Regulatory Landscape | -0.7% | Global, varying by country/region (e.g., Europe, US states) | 2025-2033 (Long-term) |

| Threat from OEM Factory-Tinted/Smart Glass Solutions | -0.5% | Global, affecting premium and new vehicle segments | 2030-2033 (Long-term) |

Automotive Tinting Film Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Automotive Tinting Film Market, covering market size, trends, drivers, restraints, opportunities, and challenges across various segments and regions. It offers a detailed forecast from 2025 to 2033, incorporating insights from historical data, and assesses the impact of emerging technologies like AI. The scope also includes a competitive landscape analysis, profiling key market players and their strategies, to equip stakeholders with actionable intelligence for strategic decision-making and identifying growth avenues within this dynamic industry.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 4.15 billion |

| Market Forecast in 2033 | USD 7.04 billion |

| Growth Rate | 6.8% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | 3M Company, Eastman Chemical Company, Solar Gard (Saint-Gobain), Llumar (Eastman Chemical Company), XPEL Inc., Avery Dennison Corporation, Johnson Window Films Inc., SunTek (Eastman Chemical Company), Madico Inc., Hanita Coatings (Avery Dennison Corporation), Rayno Window Film, Global Window Films, SolarFX Window Films, Viper Window Films, STEK Automotive, Ceramic Pro, Geoshield, Armolan. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The automotive tinting film market is extensively segmented to reflect the diverse product offerings and application areas, providing a granular view of market dynamics. These segmentations allow for a detailed analysis of specific growth drivers, consumer preferences, and competitive landscapes within each category. Understanding these segments is crucial for manufacturers and distributors to tailor their strategies, develop targeted products, and identify high-growth niches. The market's complexity necessitates a multi-dimensional approach to segmentation, encompassing the fundamental material composition, the type of vehicle it is applied to, and the primary sales channel through which it reaches the end-consumer. This detailed breakdown highlights the varied demands and opportunities present across the automotive tinting film ecosystem.

By dissecting the market into distinct segments, this analysis sheds light on the dominant product types and emerging categories. For instance, the transition from traditional dyed and metallic films to advanced ceramic and carbon films signifies a market shift towards higher performance and durability. Similarly, the robust aftermarket segment, catering to consumer customization and replacement needs, contrasts with the OEM segment's focus on factory-installed solutions. Analyzing these segments not only illustrates the current market structure but also provides predictive insights into future growth trajectories, innovation hotspots, and areas requiring strategic investment, allowing stakeholders to anticipate market shifts and capitalize on evolving consumer trends effectively.

- By Type:

- Ceramic Film: Known for high heat rejection and UV protection without metallic interference.

- Carbon Film: Offers deep, rich black finish with good heat rejection and fade resistance.

- Metallic Film: Provides excellent heat rejection and glare reduction but can interfere with electronic signals.

- Dyed Film: Primarily for aesthetics and privacy, most affordable, but offers lower performance.

- Hybrid Film: A combination of dyed and metallic layers, balancing performance and cost.

- Crystalline Film: Maximizes clarity while providing superior heat and UV protection.

- By Application:

- Passenger Vehicles: The largest segment, driven by individual consumer aesthetic and comfort needs.

- Commercial Vehicles: Growing segment driven by fleet management, security, and driver comfort.

- By Sales Channel:

- OEM (Original Equipment Manufacturer): Factory-installed tinting as part of vehicle production.

- Aftermarket: Post-purchase installation through professional tint shops, dealerships, or DIY.

- By Property:

- UV Protection: Films specifically designed to block harmful ultraviolet rays.

- Heat Rejection: Films that significantly reduce heat absorption into the vehicle interior.

- Glare Reduction: Films that minimize blinding glare from sun or headlights.

- Privacy: Films that offer increased opacity for enhanced privacy.

- Safety/Security: Films designed to hold shattered glass together upon impact.

Regional Highlights

- North America: This region represents a mature yet dynamic market, characterized by strong aftermarket demand driven by vehicle customization trends and a high prevalence of personal vehicles. Consumer awareness regarding UV protection and interior heat reduction is significant, propelling the adoption of advanced film technologies. Stringent regulations in some states, however, necessitate product innovation to comply with varying Visible Light Transmittance (VLT) laws.

- Europe: The European market is distinctive due to its stringent and fragmented regulatory environment concerning vehicle window tinting. This often limits the darkness levels permitted, fostering demand for lighter, high-performance films primarily focused on heat rejection and UV protection rather than deep tint aesthetics. Growth is also influenced by environmental considerations, pushing for more sustainable film solutions.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region, fueled by burgeoning automotive production, rising disposable incomes, and a rapidly expanding middle class in countries like China and India. The increasing number of vehicles on the road, coupled with a growing emphasis on comfort and luxury features, drives significant demand for tinting films. Warmer climates in Southeast Asia also contribute to the demand for heat-rejecting films.

- Latin America: This region exhibits steady growth, primarily driven by increasing vehicle ownership and a rising concern for vehicle security and privacy. The aftermarket segment is robust, with consumers seeking cost-effective solutions for aesthetic upgrades and basic protection. Economic stability and local manufacturing capabilities will further influence market expansion.

- Middle East and Africa (MEA): The MEA region is characterized by extreme climatic conditions, making heat rejection a primary driver for automotive tinting film adoption. High disposable incomes in some Gulf Cooperation Council (GCC) countries also contribute to demand for premium films and luxury vehicle customization. Privacy and security considerations are also significant factors influencing consumer preferences in this region.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Automotive Tinting Film Market.- 3M Company

- Eastman Chemical Company (including Llumar, SunTek, Vista)

- Saint-Gobain (including Solar Gard, Quantum)

- XPEL Inc.

- Avery Dennison Corporation (including Hanita Coatings)

- Johnson Window Films Inc.

- Madico Inc.

- Rayno Window Film

- Global Window Films

- SolarFX Window Films

- Viper Window Films

- STEK Automotive

- Ceramic Pro

- Geoshield

- Armolan

- Sun Control Films Pvt. Ltd.

- American Standard Window Film (ASWF)

- Huber Optik (Huper Optik)

Frequently Asked Questions

What are the primary benefits of installing automotive tinting film?

Automotive tinting film offers a multitude of benefits that extend beyond mere aesthetics. Firstly, it provides significant heat rejection, reducing the interior temperature of the vehicle and decreasing the strain on the air conditioning system, which can lead to improved fuel efficiency. Secondly, it blocks a substantial amount of harmful ultraviolet (UV) rays, protecting both the vehicle's interior from fading and cracking, and occupants from skin damage and eye strain. Thirdly, tinting films enhance privacy by limiting visibility into the car, contributing to a sense of security for passengers and valuables. Lastly, in the event of an accident, security tinting films can help hold shattered glass together, minimizing the risk of injury from flying shards.

Are automotive tinting films legal for all vehicles and regions?

The legality of automotive tinting films varies significantly by region, country, and even by specific state or province. Regulations typically govern the Visible Light Transmittance (VLT), which dictates how much light can pass through the tinted window, as well as the reflectivity of the film. These laws are primarily in place for road safety, ensuring drivers' visibility and allowing law enforcement to see inside a vehicle. It is crucial for vehicle owners to research and comply with local laws before installing tinting film, as non-compliance can result in fines, penalties, or the requirement to remove the tint. Many manufacturers offer films that meet specific regional regulations, and professional installers are generally knowledgeable about local compliance requirements.

What are the different types of automotive tinting films available in the market?

The automotive tinting film market offers a diverse range of film types, each with unique properties and benefits. Dyed films are typically the most affordable, primarily offering privacy and glare reduction, but with less effective heat rejection and prone to fading. Metallic films provide excellent heat rejection and strengthen glass, but can interfere with electronic signals. Carbon films offer a rich, non-reflective black finish, good heat rejection, and do not interfere with electronics. Ceramic films are considered premium, offering superior heat rejection, UV protection, and optical clarity without any metallic content, thus avoiding signal interference. Hybrid films combine dyed and metallic layers for a balance of performance and cost, while crystalline films maximize light transmission while still offering significant heat and UV protection.

How does automotive tinting film contribute to vehicle safety?

Automotive tinting film enhances vehicle safety in several ways. Firstly, by reducing glare from the sun, headlights, and reflective surfaces, it improves driver visibility and reduces eye strain, contributing to safer driving conditions, especially during dawn, dusk, or bright sunny days. Secondly, certain types of tinting films, particularly thicker security or safety films, can hold shattered glass together in the event of a collision or impact. This prevents glass fragments from scattering inside the vehicle, significantly reducing the risk of injury to occupants. Additionally, the increased privacy offered by darker tints can deter smash-and-grab thefts, adding a layer of security for belongings left inside the vehicle.

What is the typical lifespan of automotive tinting film, and how can it be maintained?

The lifespan of automotive tinting film varies depending on its type, quality, environmental exposure, and installation quality. High-quality, professionally installed films, especially ceramic or carbon varieties, can last anywhere from 5 to 10 years or even longer, maintaining their color, clarity, and performance. Lower-quality or DIY films may begin to bubble, peel, or fade within a few years. Proper maintenance is crucial for longevity. This includes avoiding abrasive cleaners or ammonia-based products, which can damage the film's adhesive or finish. Cleaning tinted windows with a soft cloth and mild, tint-safe cleaning solution is recommended. Regular gentle cleaning and avoiding direct scratches or impacts will help preserve the film's appearance and functional properties over its lifespan.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted