Automotive Rubber Injection Molding Part Market

Automotive Rubber Injection Molding Part Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706392 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

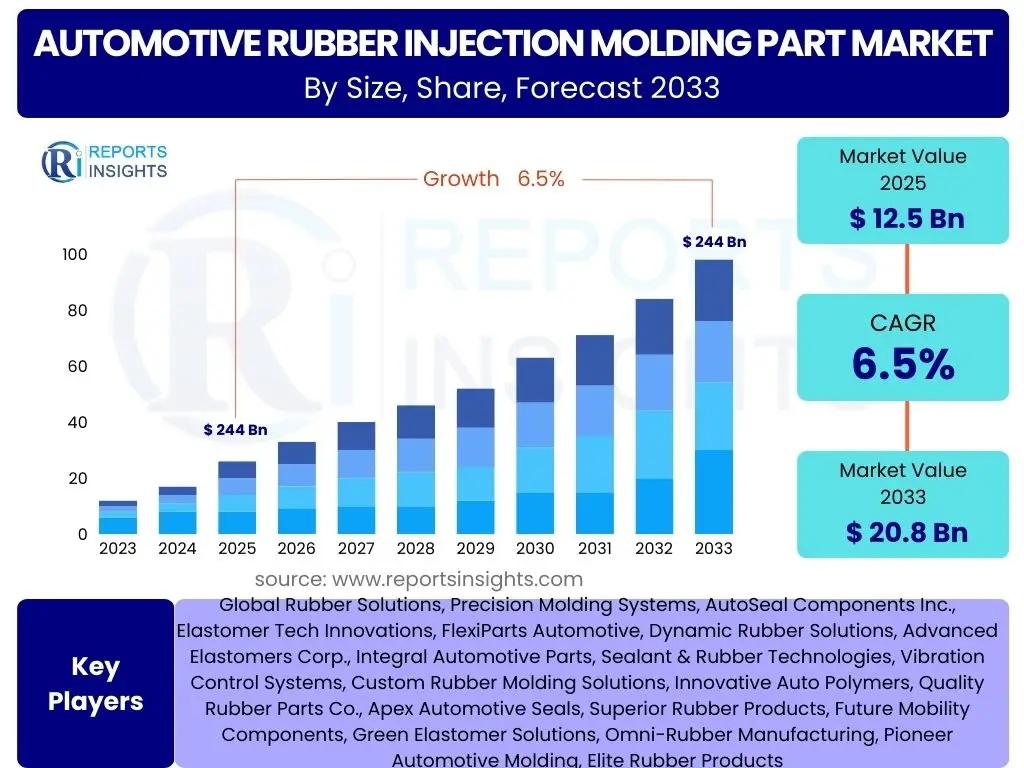

Automotive Rubber Injection Molding Part Market Size

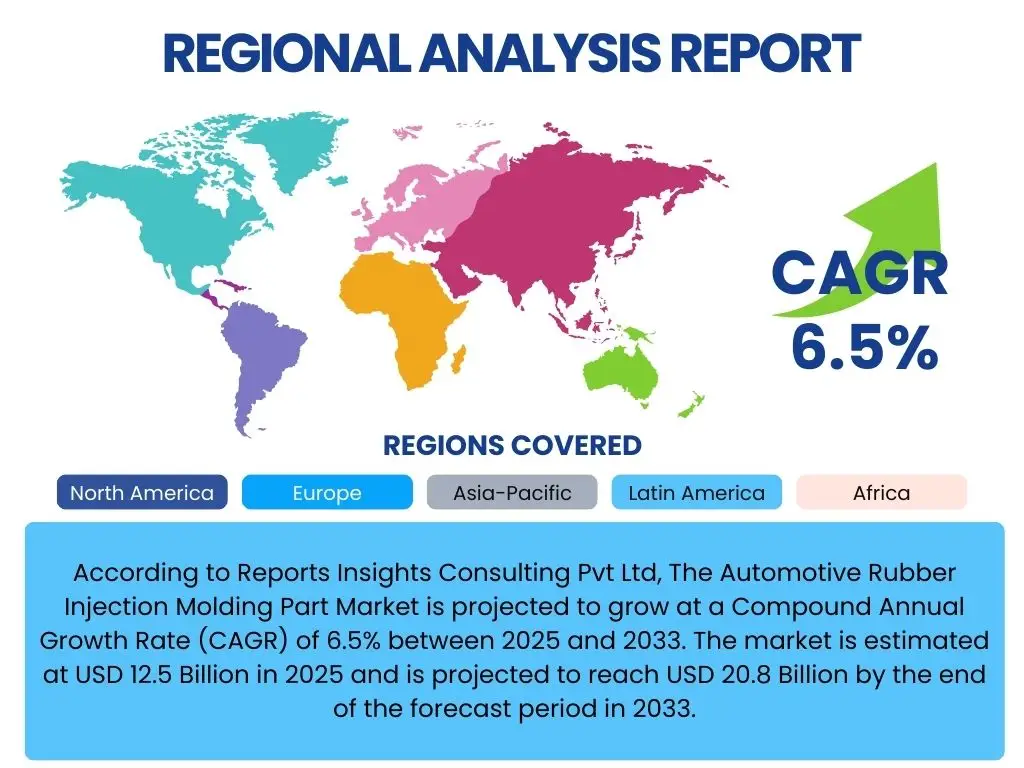

According to Reports Insights Consulting Pvt Ltd, The Automotive Rubber Injection Molding Part Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2025 and 2033. The market is estimated at USD 12.5 Billion in 2025 and is projected to reach USD 20.8 Billion by the end of the forecast period in 2033.

Key Automotive Rubber Injection Molding Part Market Trends & Insights

User inquiries frequently highlight the evolving landscape of automotive manufacturing, particularly focusing on how technological advancements and shifting consumer preferences are impacting rubber injection molded parts. There is significant interest in understanding the industry's response to sustainability demands, the integration of smart manufacturing processes, and the implications of electric vehicle (EV) proliferation. Users are keen to identify emerging material innovations and how these contribute to enhanced performance, weight reduction, and extended component lifespan in modern vehicles. The drive for greater efficiency in production methods and the adoption of more complex geometries for parts also represent areas of high user curiosity.

The market is witnessing a notable pivot towards lightweighting solutions, driven by the dual objectives of improving fuel efficiency in internal combustion engine (ICE) vehicles and extending range in EVs. This trend necessitates the development and adoption of advanced rubber compounds that offer superior strength-to-weight ratios. Furthermore, the increasing complexity of vehicle systems, particularly in autonomous and connected cars, demands higher precision and reliability from rubber components, leading to a surge in demand for sophisticated molding technologies. The global push for environmental responsibility is also a central theme, with a growing emphasis on sustainable manufacturing practices, recyclable materials, and energy-efficient production processes. This involves not only the materials themselves but also the optimization of the injection molding process to minimize waste and energy consumption.

- Lightweighting initiatives to enhance fuel efficiency and EV range.

- Rising adoption of advanced and high-performance elastomers.

- Increasing demand for complex and precision-molded components.

- Growing focus on sustainable and eco-friendly manufacturing processes.

- Integration of smart manufacturing and automation (Industry 4.0) in production lines.

- Shift towards electric vehicles driving new material and design requirements.

AI Impact Analysis on Automotive Rubber Injection Molding Part

User questions related to the impact of AI on the Automotive Rubber Injection Molding Part sector primarily revolve around efficiency gains, quality control, and predictive capabilities. There is a strong interest in understanding how AI can optimize production parameters, reduce defects, and accelerate design iterations. Concerns often include the initial investment required for AI integration, the need for specialized skills, and data privacy issues. Users also explore the potential of AI in supply chain management and its role in fostering greater automation within manufacturing facilities, envisioning a future where production lines are more intelligent and self-optimizing.

AI's influence is transformative, enabling manufacturers to move beyond traditional trial-and-error methods to data-driven decision-making. Through machine learning algorithms, AI can analyze vast datasets from production lines, identifying optimal temperature, pressure, and cure times for different rubber compounds, thereby minimizing material waste and energy consumption. This leads to significant improvements in operational efficiency and cost reduction. Furthermore, AI-powered vision systems are revolutionizing quality inspection, detecting minute flaws in real-time that human inspectors might miss, ensuring a consistently high standard of finished products. The ability of AI to predict equipment failures also allows for proactive maintenance, reducing downtime and extending the lifespan of machinery.

Beyond the manufacturing floor, AI is beginning to impact the design phase, with generative design tools exploring optimal part geometries for specific performance requirements, often resulting in lighter, more durable, and more complex components. In supply chain management, AI algorithms can predict demand fluctuations, optimize inventory levels, and identify potential disruptions, enhancing resilience and responsiveness. The long-term trajectory indicates that AI will increasingly enable autonomous production environments, where systems continuously learn and adapt, leading to unprecedented levels of efficiency, precision, and innovation in the automotive rubber injection molding part market.

- Predictive maintenance of molding machinery, reducing downtime.

- Enhanced quality control through AI-powered visual inspection systems.

- Optimization of molding parameters (temperature, pressure) for improved output and reduced waste.

- Accelerated design and prototyping through AI-driven generative design.

- Improved supply chain forecasting and inventory management.

- Robotics and automation integration for increased efficiency and precision.

- Real-time anomaly detection in production, preventing defects.

Key Takeaways Automotive Rubber Injection Molding Part Market Size & Forecast

User inquiries frequently focus on discerning the most impactful drivers and inhibitors shaping the Automotive Rubber Injection Molding Part market's trajectory, along with the most promising areas for future growth. There is a keen interest in understanding how global megatrends, such as vehicle electrification and increasing stringent regulatory environments, translate into specific market opportunities and challenges for manufacturers of these critical components. Users seek clarity on where investment opportunities lie and what strategic shifts companies are making to capitalize on the projected growth, especially within emerging economies and technological niches.

The market is poised for robust expansion, primarily fueled by the accelerating global production of vehicles, particularly the significant surge in electric vehicle manufacturing which demands new types of high-performance rubber components for battery sealing, thermal management, and vibration isolation. Concurrently, the increasing focus on vehicle lightweighting across all vehicle segments continues to drive innovation in material science, pushing the adoption of advanced elastomers. Despite this positive outlook, the market faces headwinds from volatile raw material prices and the need for substantial capital investments in advanced molding technologies, which can pose barriers to entry and expansion for smaller players. However, these challenges also create opportunities for companies that can innovate in material sourcing, process efficiency, and automation.

The forecast period suggests that companies capable of adapting to stringent quality standards and evolving design complexities will gain a competitive edge. The shift towards sustainable materials and manufacturing processes is not merely a regulatory compliance issue but is increasingly becoming a competitive differentiator, appealing to both consumers and automotive OEMs. Furthermore, regional market dynamics show significant growth potential in Asia Pacific, driven by high automotive production volumes and increasing disposable incomes, while North America and Europe will focus on premiumization, advanced technology adoption, and regulatory-driven innovations. Strategic partnerships and investments in R&D will be crucial for sustained growth in this dynamic market.

- Strong growth driven by increasing global vehicle production, especially EVs.

- Technological advancements in materials and molding processes are crucial for market expansion.

- Lightweighting and performance enhancement remain core objectives.

- Sustainability and circular economy principles are influencing material selection and production.

- Asia Pacific is expected to remain a dominant growth region.

- Raw material price volatility and high investment costs pose significant challenges.

Automotive Rubber Injection Molding Part Market Drivers Analysis

The Automotive Rubber Injection Molding Part market is primarily propelled by several synergistic factors, reflecting the dynamic evolution of the global automotive industry. A significant driver is the continuous increase in overall vehicle production worldwide, which inherently boosts the demand for a vast array of rubber components. This is coupled with the escalating adoption of electric vehicles (EVs), which, despite having fewer moving parts than internal combustion engine (ICE) vehicles, require specialized rubber components for battery sealing, thermal management, and noise/vibration/harshness (NVH) mitigation, often demanding higher performance characteristics.

Furthermore, stringent emission regulations and fuel efficiency standards imposed by governments globally compel automotive manufacturers to focus on lightweighting and enhancing the efficiency of all vehicle parts. Rubber injection molded parts contribute significantly to these objectives by reducing overall vehicle weight and improving sealing capabilities. Advances in rubber material science, leading to the development of higher-performance elastomers with improved durability, temperature resistance, and chemical resistance, also serve as a crucial driver, enabling new applications and improving existing ones across various automotive systems, from powertrain to chassis and interior components.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Global Vehicle Production | +1.8% | Global, particularly Asia Pacific, North America | 2025-2033 |

| Rapid Growth in Electric Vehicle (EV) Sales & Production | +2.2% | Global, particularly China, Europe, North America | 2025-2033 |

| Stringent Emission Regulations & Fuel Efficiency Standards | +1.5% | Europe, North America, China | 2025-2033 |

| Growing Demand for Lightweight Components | +1.3% | Global | 2025-2033 |

| Advancements in Rubber Materials & Compound Formulations | +1.0% | Global, particularly developed economies | 2025-2033 |

Automotive Rubber Injection Molding Part Market Restraints Analysis

The Automotive Rubber Injection Molding Part market faces several significant restraints that could temper its growth trajectory. A primary concern is the volatility and unpredictability of raw material prices, particularly for synthetic rubbers (like EPDM, NBR, FKM) and various chemical additives, which are often derived from crude oil. These fluctuations directly impact manufacturing costs, profitability, and can lead to difficulties in long-term production planning and pricing strategies. Such cost pressures can compel manufacturers to absorb losses or pass on increased costs, potentially affecting competitiveness.

Another substantial restraint is the high initial investment required for sophisticated injection molding machinery and tooling. The precision and complexity demanded by modern automotive applications necessitate advanced equipment, which can be prohibitively expensive for smaller companies or new entrants. This high capital expenditure also extends to the ongoing maintenance and upgrades required to keep pace with technological advancements and quality standards. Furthermore, the inherent complexity of designing and manufacturing intricate rubber parts, especially those with tight tolerances or multi-material requirements, demands specialized expertise and rigorous quality control, adding to operational complexities and potential costs.

Competition from alternative materials, such as advanced plastics, composites, and thermoplastic elastomers (TPEs), also poses a restraint. While rubber offers unique properties like elasticity and sealing capabilities, other materials are constantly improving in performance, often offering advantages in terms of weight, recyclability, or ease of manufacturing for certain applications. Supply chain disruptions, often triggered by geopolitical events, natural disasters, or global health crises, can severely impact the availability of raw materials or finished components, leading to production delays and increased costs, as evidenced by recent global events.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in Raw Material Prices | -1.5% | Global | Short to Medium-Term (2025-2028) |

| High Initial Investment & Tooling Costs | -1.2% | Global | Long-Term (2025-2033) |

| Intense Competition from Alternative Materials | -1.0% | Global | Long-Term (2025-2033) |

| Complexities in Design & Manufacturing for Precision Parts | -0.8% | Global | Long-Term (2025-2033) |

| Global Supply Chain Disruptions & Geopolitical Risks | -0.7% | Global | Short to Medium-Term (2025-2028) |

Automotive Rubber Injection Molding Part Market Opportunities Analysis

Despite existing restraints, the Automotive Rubber Injection Molding Part market presents significant opportunities for growth and innovation. One major avenue stems from the burgeoning growth in emerging economies, particularly in Asia Pacific, Latin America, and parts of Africa. These regions are experiencing rapid industrialization, urbanization, and increasing disposable incomes, leading to a surge in automotive production and sales. This demographic and economic shift creates a vast untapped market for rubber injection molded parts, as vehicle penetration rates continue to rise and the demand for affordable yet reliable transportation increases.

Another crucial opportunity lies in the continuous advancements in automation and smart manufacturing technologies, often grouped under Industry 4.0. The integration of robotics, artificial intelligence (AI), and data analytics into the injection molding process can significantly enhance efficiency, precision, and quality control, while reducing labor costs and waste. This allows manufacturers to produce more complex and higher-performance parts with greater consistency. Furthermore, the increasing focus on sustainability and the circular economy in the automotive industry is opening doors for innovative approaches to material sourcing, including the use of recycled rubber and bio-based elastomers, as well as the development of parts designed for easier end-of-life recycling. This commitment to eco-friendly practices can also serve as a strong competitive differentiator.

The rising demand for specialty rubbers and custom-engineered solutions also offers a lucrative niche. As vehicle designs become more complex and performance demands escalate, particularly for electric and autonomous vehicles, there is a growing need for bespoke rubber components tailored to specific applications, such as high-temperature seals for battery packs or advanced vibration dampeners for sensitive electronic systems. Companies that can offer highly specialized materials and custom manufacturing capabilities will find significant market traction. Moreover, opportunities exist in strategic collaborations between material suppliers, molders, and automotive OEMs to co-develop next-generation solutions, fostering innovation and accelerating market penetration for new technologies.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Emerging Automotive Markets | +1.7% | Asia Pacific, Latin America, Africa | Long-Term (2025-2033) |

| Advancements in Automation & Industry 4.0 Technologies | +1.4% | Global | Long-Term (2025-2033) |

| Increasing Focus on Sustainable & Recyclable Materials | +1.1% | Europe, North America, Japan | Long-Term (2025-2033) |

| Rising Demand for Specialty Rubbers & Custom Solutions | +1.0% | Global | Long-Term (2025-2033) |

| Strategic Collaborations & Partnerships | +0.9% | Global | Long-Term (2025-2033) |

Automotive Rubber Injection Molding Part Market Challenges Impact Analysis

The Automotive Rubber Injection Molding Part market is confronted by several significant challenges that necessitate strategic responses from industry players. One pervasive challenge is the persistent shortage of skilled labor, particularly operators and technicians proficient in advanced injection molding processes, material science, and automation technologies. This deficit can lead to production bottlenecks, increased labor costs, and difficulties in adopting new, complex manufacturing systems. The aging workforce in many developed regions exacerbates this issue, requiring substantial investment in training and talent development programs.

Furthermore, the automotive industry's rapid technological evolution, especially with the advent of electric and autonomous vehicles, poses a continuous challenge. Manufacturers of rubber parts must constantly adapt to evolving vehicle architectures, new material requirements (e.g., for battery thermal management or high-voltage applications), and increasingly stringent performance specifications. This demands significant investment in research and development, alongside flexible production capabilities to meet dynamic OEM demands. Maintaining consistently high-quality assurance for precision rubber components, often operating under extreme conditions, also remains a critical challenge, as even minor defects can lead to significant safety or performance issues in vehicles.

Geopolitical uncertainties and their cascading effects on global supply chains also represent a formidable challenge. Trade disputes, tariffs, and regional conflicts can disrupt the flow of raw materials, components, and finished products, leading to increased lead times, higher logistics costs, and production inefficiencies. Navigating complex environmental regulations and ensuring compliance with ever-tightening standards for material usage, emissions from manufacturing processes, and waste management adds another layer of complexity for manufacturers, requiring continuous investment in greener technologies and sustainable practices.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Skilled Labor Shortage | -1.3% | Global, particularly Developed Economies | Long-Term (2025-2033) |

| Rapid Technological Changes & Innovation Cycles | -1.0% | Global | Long-Term (2025-2033) |

| Maintaining High Quality Assurance for Precision Parts | -0.9% | Global | Long-Term (2025-2033) |

| Geopolitical Uncertainties & Supply Chain Resilience | -0.8% | Global | Short to Medium-Term (2025-2028) |

| Environmental Compliance & Sustainability Pressure | -0.7% | Europe, North America, Japan | Long-Term (2025-2033) |

Automotive Rubber Injection Molding Part Market - Updated Report Scope

This report provides a comprehensive analysis of the Automotive Rubber Injection Molding Part market, covering key market dynamics, segmentation, regional insights, and the competitive landscape. It offers a detailed examination of market drivers, restraints, opportunities, and challenges, providing a strategic outlook for stakeholders. The scope includes an in-depth analysis of market size and forecast from 2025 to 2033, with 2024 as the base year and historical data from 2019 to 2023. This report aims to equip businesses with actionable insights to navigate the evolving market and identify growth prospects across various segments and geographies.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 12.5 Billion |

| Market Forecast in 2033 | USD 20.8 Billion |

| Growth Rate | 6.5% |

| Number of Pages | 247 |

| Key Trends | >|

| Segments Covered | >|

| Key Companies Covered | Global Rubber Solutions, Precision Molding Systems, AutoSeal Components Inc., Elastomer Tech Innovations, FlexiParts Automotive, Dynamic Rubber Solutions, Advanced Elastomers Corp., Integral Automotive Parts, Sealant & Rubber Technologies, Vibration Control Systems, Custom Rubber Molding Solutions, Innovative Auto Polymers, Quality Rubber Parts Co., Apex Automotive Seals, Superior Rubber Products, Future Mobility Components, Green Elastomer Solutions, Omni-Rubber Manufacturing, Pioneer Automotive Molding, Elite Rubber Products |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Automotive Rubber Injection Molding Part market is meticulously segmented to provide a granular understanding of its diverse landscape and to identify specific growth drivers and trends within each category. These segments are defined by product type, material used, vehicle application, and end-use, reflecting the varied requirements and applications of rubber components across the automotive industry. This comprehensive segmentation allows for a detailed analysis of market dynamics, competitive positioning, and strategic opportunities, enabling stakeholders to make informed decisions and tailor their offerings to specific market needs. The intricate interplay between material innovations and application-specific demands drives the evolution within these segments.

- By Product Type: This segment includes critical components such as Gaskets & Seals (essential for fluid containment), Hoses (for fluid and air transfer), O-rings (for sealing applications), Mounts (for vibration isolation), Bushings, Diaphragms, Grommets, Bellows, Boots, Weatherstripping (for environmental sealing), and Vibration Dampeners (for noise and vibration reduction).

- By Material: Key materials utilized encompass EPDM (Ethylene Propylene Diene Monomer) for weather resistance, Silicone for high-temperature applications, Nitrile Rubber (NBR) for oil resistance, Hydrogenated Nitrile Butadiene Rubber (HNBR) for enhanced temperature and chemical resistance, Fluoroelastomer (FKM) for extreme conditions, Natural Rubber (NR) for elasticity, Butyl Rubber for air impermeability, and other specialized compounds.

- By Vehicle Type: The market is analyzed across Passenger Vehicles (sedans, SUVs, compacts), Commercial Vehicles (Light Commercial Vehicles, Heavy Commercial Vehicles), and the rapidly expanding Electric Vehicles sector (Battery Electric Vehicles, Plug-in Hybrid Electric Vehicles, Fuel Cell Electric Vehicles), each having distinct rubber component requirements.

- By Application: Segments include Powertrain Systems (engine mounts, seals), Chassis Systems (suspension bushings), Interior Systems (anti-vibration pads, grommets), Exterior Systems (weatherstripping, moldings), HVAC Systems (duct seals), Braking Systems (seals, diaphragms), Steering Systems, Fuel Systems, and various Sealing Systems.

- By End-Use: The market is divided into Original Equipment Manufacturer (OEM) for new vehicle production and Aftermarket for replacement parts and repairs.

Regional Highlights

- Asia Pacific (APAC): Dominates the market due to high volume automotive production in countries like China, India, Japan, and South Korea. Rapid industrialization, increasing disposable incomes, and the strong presence of major automotive OEMs and component manufacturers contribute to its significant market share. The region is also a hub for EV manufacturing, further boosting demand.

- Europe: Characterized by stringent emission norms and a strong focus on premium and luxury vehicles. Germany, France, and the UK are key markets, driving demand for high-performance and precision-engineered rubber parts for fuel efficiency, NVH reduction, and advanced sealing applications. Growing EV adoption in the region also stimulates demand for new component designs.

- North America: A mature market with significant demand from the large passenger and commercial vehicle sectors. The region is witnessing a robust shift towards electric vehicles and an increasing focus on lightweighting and advanced safety features, driving innovation in rubber materials and molding processes. The presence of major automotive players and a strong aftermarket segment support market growth.

- Latin America: Expected to show steady growth driven by increasing automotive production, particularly in Brazil and Mexico. Economic development and urbanization are fostering demand for new vehicles, translating into increased opportunities for automotive rubber injection molding parts, especially for cost-effective and durable solutions.

- Middle East and Africa (MEA): Emerging as a potential growth region, albeit from a smaller base. Investments in infrastructure, rising vehicle sales in certain countries, and the development of local manufacturing capabilities are gradually contributing to market expansion. The demand is often for reliable and robust components suitable for diverse climatic conditions.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Automotive Rubber Injection Molding Part Market.- Global Rubber Solutions

- Precision Molding Systems

- AutoSeal Components Inc.

- Elastomer Tech Innovations

- FlexiParts Automotive

- Dynamic Rubber Solutions

- Advanced Elastomers Corp.

- Integral Automotive Parts

- Sealant & Rubber Technologies

- Vibration Control Systems

- Custom Rubber Molding Solutions

- Innovative Auto Polymers

- Quality Rubber Parts Co.

- Apex Automotive Seals

- Superior Rubber Products

- Future Mobility Components

- Green Elastomer Solutions

- Omni-Rubber Manufacturing

- Pioneer Automotive Molding

- Elite Rubber Products

Frequently Asked Questions

What is automotive rubber injection molding?

Automotive rubber injection molding is a manufacturing process where raw rubber compounds are injected into a mold cavity under high pressure and temperature to create precise, complex-shaped rubber components for vehicles. This method is crucial for producing parts with tight tolerances and consistent quality.

What are the primary applications of rubber injection molded parts in automobiles?

These parts are essential across various vehicle systems, including sealing applications (gaskets, O-rings, weatherstripping), vibration isolation (mounts, bushings, dampeners), fluid transfer (hoses), and protection (boots, bellows) in powertrains, chassis, interior, exterior, and braking systems.

What materials are commonly used in automotive rubber injection molding?

Common materials include EPDM for weather resistance, Silicone for high-temperature stability, Nitrile Rubber (NBR) for oil and fuel resistance, HNBR for enhanced durability, and FKM for extreme chemical and heat resistance, selected based on specific application requirements.

How do electric vehicles (EVs) impact the demand for automotive rubber injection molded parts?

EVs drive demand for specialized rubber components for battery sealing, thermal management, EMI shielding, and vibration control in quieter vehicle environments. While some traditional parts may be reduced, new high-performance and lightweight rubber solutions are increasingly required.

What are the key trends shaping the automotive rubber injection molding market?

Key trends include lightweighting initiatives, the adoption of advanced and sustainable elastomers, increasing automation and Industry 4.0 integration in manufacturing, and the growing demand for precision-molded components to meet stringent performance and safety standards in modern vehicles.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted